Online Store

Online Store

Introduction

Over the last several decades, governments have collectively pledged to slow global warming. But despite intensified diplomacy, the world is already facing the consequences of climate…

One graph to rule them all ...

More on:

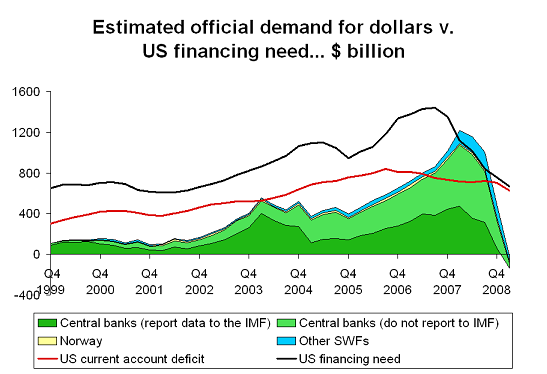

If I had to pick a single graph to explain the evolution of the United States’ balance of payments – and thus, indirectly, the entire story of the world’s macroeconomic “imbalances” – this would be it.

All data is in dollar billions, and is presented as a rolling four quarter sum.*

The red line is the United States current account deficit.

The black line is the United States financing need – defined as the sum of the current account deficit plus US outward FDI and US purchases of foreign long-term securities.** The dip in the total US financing need from mid 2005 to mid 2006 isn’t real. It reflects the impact of the Homeland Investment Act, a holiday on the repatriation of the foreign profits of US multinationals that produced a sharp fall in outward FDI.*** The rise in the United States financing need over the course of 2007 by contrast is real; American investors bought the decoupling story and wanted to invest more abroad.

The shaded area represents official demand for US assets. The inflows from central banks that report data to the IMF and Norway are known. The inflows from central banks that don’t report and other sovereign funds are my own estimates. The key countries that do not report reserves are – in my judgment – China, Saudi Arabia and the other countries in the GCC. I have assumed that the dollar share of their reserves is closer to 70% than 60% (supporting evidence). I by contrast have assumed that the GCC’s sovereign funds have a diverse portfolio.

What does the graph tell us?

In my view, three things:

First, the rise in the US current account deficit from 2002 to 2006 is associated with a rise in official demand for US assets. The quarterly IMF data doesn’t extend back to the late 90s – or to the early 1980s. But trust me, that is a change from past periods when the US current account deficit expanded. To be sure, private investors abroad were also buying US assets. But the rise in the overall US financing need associated with the rise in the current account deficit wasn’t financed by a comparable rise in private demand for US assets.

Second, Official demand for US assets soared from the end of 2005 to the end of 2007 – even by the standards of this decade. That surge was hidden, as the majority came from countries that don’t transparently report the currency composition of their reserves (let alone their sovereign funds). But it happened. At the peak of official asset accumulation in late 2007 and early 2008, official demand for US assets (best I can tell, and if my estimates are off – do tell, and explain, with data) exceeded the total US financing need. Central banks and sovereign funds were financing both the US current account deficit and the “diversification” of private US portfolios. Absent that uptick in official demand, the US would have experienced a dollar crisis before it experienced a banking crisis.

Third, official demand for US assets has fallen quite sharply over the last four quarters. Paul Krugman is right. The US depended on China’s central bank – and other official investors – far less over the last four quarters than it did in late 2007 and early 2008. The collapse in gross private capital flows during the crisis rebounded in the United States’ favor, as Americans scaled back their investment abroad faster than foreigners scaled back their investment in the US. The fiscal deficit may be up, but US “dependence” on central banks for financing fell sharply.

At least through the first quarter. The second quarter of 2009 will be to be different. Reserve growth seems to have resumed.

But there is little doubt that reserve growth slowed sharply from mid 2008 to mid 2009. The countries that report detailed data on their reserves to the IMF reduced their dollar reserves from the end of q1 2008 to the end of q1 2009 by about $130 billion. That is a fact not a guess. Guessing the overall total requires guessing what China (and Saudi Arabia did). But there is little doubt that China’s overall reserve growth slowed – so unless it was diversifying into the dollar, its growth in its dollar reserves must also have slowed.

Wait. Doesn’t the US data (including the Fed custodial accounts) tell a somewhat different story? And doesn’t the US data show record inflows into Treasuries?

All true.

My estimates of dollar reserve growth (and the available data from the IMF) are at odds with the US data showing a pick up in official demand for Treasuries.

What gives?

My explanation: central banks reserve managers pulled funds from banks, the US agencies, and private fund managers – producing an uptick in demand for Treasuries.

We know that this happened inside the US. From the end of q1 08 to the end of q1 09 central banks reduced their dollar deposits in US banks by about $200 billion – providing a lot of the funds that flowed into Treasuries. I would bet the same thing happened globally.

From early 2007 to mid 2008, central bank demand – in even the revised US data – lagged my estimated of global dollar reserve growth. From mid 2008 on, central bank demand in the US data has exceeded my estimate for dolllar reserve growth.

I don’t think central banks shifted out of the dollar as rapidly as the US data implies in late 2007 and early 2008 (the IMF data rules out a shift by those countries that report detailed data to the IMF, so such a shift would have to have come from China and the Gulf). And I don’t think central banks shifted back into dollars on the scale the US data now implies. Rather central banks shifted first into riskier dollar assets (and made greater use of private managers) and then shifted back to traditional reserve assets like Treasuries.

That does though mean that there has been an enormous gap between the rhetoric coming from some important holders of reserves -- rhetoric that suggests a loss of confidence in the long-term value of US Treasuries -- and their actual actions. For all their faults, central bank reserve managers still seem to consider US Treasuries safer than other dollar-denominated assets.

*The underlying data comes from the IMF’s COFER data, the US BEA, the PBoC, SAMA and the national balance of payments of countries with sovereign wealth funds. But I also had to make a few assumptions to flesh out the data, notably assumptions about the dollar share of countries that do not report detailed data about their reserves to the IMF

** I have excluded outward short-term flows because they are highly correlated with short-term inflows; the banking sector doesn’t seem to be a consistent source of net financing for the US.

*** The homeland investment act allowed American firms to repatriate profits earned abroad without paying US corporate income taxes. It led to a $200 billion or so fall in US outward FDI, as American firms (temporarily) stopped reinvesting their foreign profits.

More on: