Online Store

Online Store

Introduction

Over the last several decades, governments have collectively pledged to slow global warming. But despite intensified diplomacy, the world is already facing the consequences of climate…

China, not Piketty, Explains “Confused Signals” in U.S. Asset Prices

More on:

The FT’s Ed Luce recently took on the “confused signals” being sent by U.S. stock and bond prices moving in sync (upward).

Which is it, he asks? Are economic prospects good, as stock prices suggest, or bleak, as bond prices suggest?

Both and neither, he offers. High-end retailers like LMVH and Tiffany are doing great, he says, while low-end ones like Walmart and Sears are languishing. The net effect, he concludes, is stock prices buoyed by high-end earnings optimism and bond prices supported by a hollowing out of the American middle class. Growing inequality explains the apparent conundrum.

Given the current fascination with all things Piketty, this makes a charming and topical story. But it is also almost certainly wrong.

The straight average of U.S. company stock prices in the S&P Global Luxury index is actually down 1% this year; market-cap weighted, it’s up only 3.9%. This compares with a 6.1% rise in the S&P overall. As for Luce’s example of Tiffany (LMVH is foreign), its stock price has lagged mid-range retailer Macy’s. In short, there is no discernable Piketty effect in U.S. stock prices.

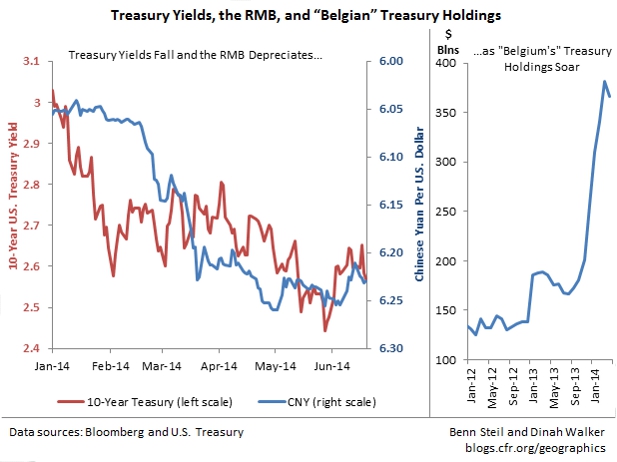

As for bond prices, China’s central bank holds the key.

After more than three years of steady appreciation, the RMB has declined over 3% this year – erasing the past year’s rise. Driven by the Chinese government’s desire to re-juice failing economic growth, RMB depreciation has naturally been accompanied by an increase in China’s foreign exchange reserves.

China usually allocates about 40 percent of its foreign exchange reserves to Treasuries; so far this year, however, its official holdings of Treasuries have actually declined. What explains this? Given that China comes under pressure from the U.S. Treasury and Congress whenever it appears to be pushing down its currency, China is almost certainly disguising its Treasury purchases by holding them in Belgium.

As shown in the graphic above, “Belgium” accumulated abnormal amounts of Treasuries during the first quarter of the year; Brussels-based clearinghouse Euroclear has acknowledged that it is likely responsible for the increase. China’s actions would help explain why Belgium, a country whose GDP is slightly smaller than that of New Jersey's, has become the world’s third largest holder of Treasuries, after only China and Japan.

China and “Belgium” bought a massive combined $59 billion in Treasuries in January, a month in which the supply of Treasuries actually shrank by $42 billion. This would almost surely explain a large part of the decline in Treasury yields that month from 3.03% to 2.64%

In short, the “confused signals” in U.S. asset prices would appear to be driven by China’s efforts to push down the RMB, and not by Pikettification of the U.S. economy.

Financial Times: Look to China for Reasons Behind Strong Demand for Treasuries

New York Fed: Responses to Survey of Primary Dealers

Treasury: Major Foreign Holders of Treasury Securities

Wall Street Journal: China Is in No Rush to Halt Yuan’s Fall

Follow Benn on Twitter: @BennSteil

Follow Geo-Graphics on Twitter: @CFR_GeoGraphics

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”

More on: