Online Store

Online Store

Introduction

Over the last several decades, governments have collectively pledged to slow global warming. But despite intensified diplomacy, the world is already facing the consequences of climate…

More Evidence That LIBOR Is Hazardous to Economic Health

More on:

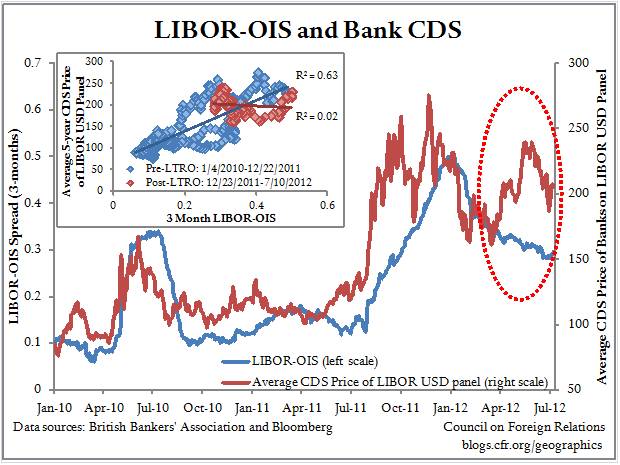

Central bankers necessarily spend a great deal of time studying economic and market data that they believe to be forward-looking indicators of the economy’s health. One such is the so-called “LIBOR-OIS spread” – the spread between the London Interbank Offered Rate (the rate at which major banks can supposedly borrow from each other, unsecured by collateral, for three months) and the Overnight Indexed Swap rate (which reflects market expectations of the overnight unsecured rate over a three-month period). LIBOR is generally higher than OIS because of liquidity and credit risk (the risk that the borrowing bank will default on a loan). European Central bank (ECB) board member Benoît Cœuré, echoing thoughts expressed by Alan Greenspan and others in the past, recently referred to the LIBOR-OIS spread as “a standard measure of tensions in unsecured markets.” It goes up when such tensions go up, and down when such tensions go down.

The LIBOR-OIS spread can be low, however, even when banks are in appalling financial health. How is this possible?

The problem starts when the government begins tracking such a measure to determine whether it needs to do something. The reason is that when statistical measures are targeted for policy purposes they tend to lose the information content that recommended them for that role in the first place. This common pitfall in economic policymaking has been termed “Goodhart’s Law,” having been first articulated by British economist and former Bank of England Monetary Policy Committee member Charles Goodhart back in 1975.

Could Goodhart’s Law be at work with the LIBOR-OIS spread? We believe so. In March, after the ECB ended its Long-Term Refinancing Operations (LTRO), which provided banks with over €1 trillion in 3-year 1%-interest loans, the LIBOR-OIS spread continued the downward trend it started on after the program was launched last December – as shown in the main graphic above. By Cœuré’s logic, this indicated that LTRO had succeeded in addressing earlier worries about the ability of major European banks to attract vital funding.

But look what happens to the price of 5-year credit default swaps (CDS) on the members of the LIBOR bank panel after LTRO ends – it soars. A huge, and highly unusual, gap opens up between the CDS price and the LIBOR-OIS spread. The small box in the upper left of the graphic shows that CDS prices and the LIBOR-OIS spread were highly correlated over the two years to the start of LTRO, but that this relationship collapses thereafter. This indicates that whereas banks are happy to lend to each other for three months, given that they’re now awash with ECB cash, the end of LTRO combined with a renewed deterioration of Spanish and Italian sovereign bond prices led to rapidly revived fears of bank defaults within 5 years.

In other words, the LTRO policy intervention significantly reduced the information content of the LIBOR-OIS spread. CDS prices are now a more valid indicator of the health of the eurozone banking system – which is poor and deteriorating.

Cœuré: The Importance of Money Markets

St. Louis Fed: The LIBOR-OIS Spread as a Summary Indicator

Financial Times: ECB Emergency Aid Is"No Silver Bullet"

Chrystal and Mizen: Goodhart's Law—Its Origins, Meaning and Implications for Monetary Policy

More on: