Online Store

Online Store

Introduction

Over the last several decades, governments have collectively pledged to slow global warming. But despite intensified diplomacy, the world is already facing the consequences of climate…

Should the ECB Go on a Bund Buying Spree?

More on:

Should the European Central Bank finally join the Fed, the Bank of England, and the Bank of Japan and deliver a good, stiff dose of Quantitative Easing?

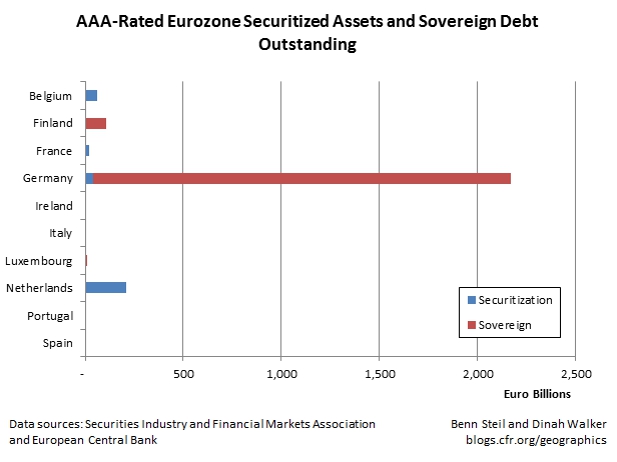

Maybe, came the surprise response from the hawkish Bundesbank president on March 25. But “any private or public assets that we might buy,” Jens Weidmann warned, “would have to meet certain quality standards.”

That’s a big but, as the quality of Eurozone assets has deteriorated markedly since 2009. In fact, as today’s Geo-Graphic shows, if the ECB were to limit its asset purchases to the universe of AAA-rated Eurozone sovereign debt and securitized assets a whopping 80% of the total available would be German Bunds.

But would a Eurozone QE program focused on gobbling up Bunds be such a bad idea? We don’t think so.

First, it might actually play a useful role in helping to eliminate structural imbalances within the Eurozone by pushing up German prices and wages disproportionately. “While buying Greek or Portuguese paper could help tame deflation there,” an unnamed Eurosystem official recently told Reuters, “the falling consumer prices in these countries were part of a natural adjustment of their economies to become more competitive, and were actually welcome.”

Second, through the so-called portfolio-balance effect the prices of other Eurozone assets will also be pushed up (and their yields down) as Eurozone banks replace the Bunds they sell to the ECB with other securities. The Fed’s purchases of Treasurys and MBS most surely boosted asset prices across the spectrum in the United States (and abroad – just ask the ever-voluble Brazilian finance minister); the effect should be similarly broad in Europe.

Finally, if a AAA focus for Eurozone QE were the price of getting Germany on board politically, it would be a small price to pay. Mario Draghi’s 2012 pledge to do “whatever it takes” remains in the background should he ultimately feel the need to operationalize OMT (Outright Monetary Transactions) and push down sovereign yields in Spain, Portugal, Italy, or elsewhere.

Financial Times: ECB Policymakers Plot QE Road Map

Bernanke: Monetary Policy Since the Onset of the Crisis

The Economist: Turning Over a New Leaf?

Bloomberg: Weidmann, Citing QE Legitimacy, Paves Way for ECB Consensus

Follow Benn on Twitter: @BennSteil

Follow Geo-Graphics on Twitter: @CFR_GeoGraphics

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”

More on: