Introduction

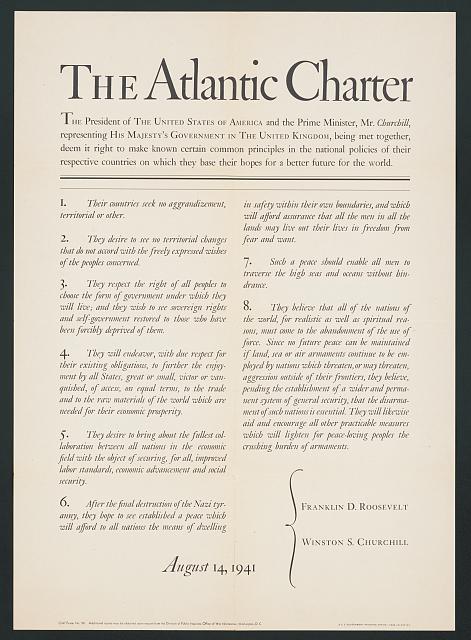

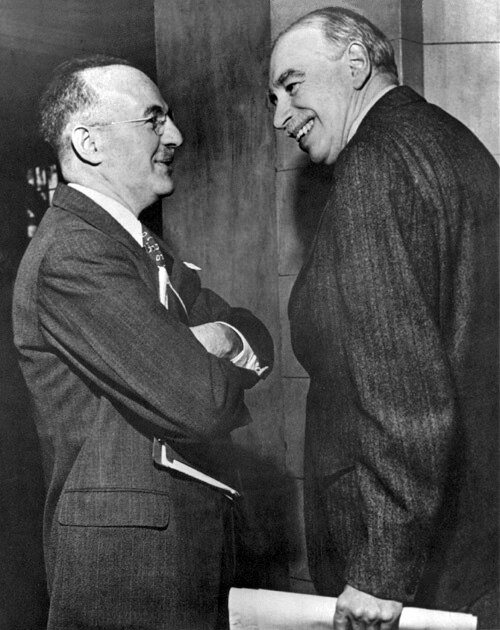

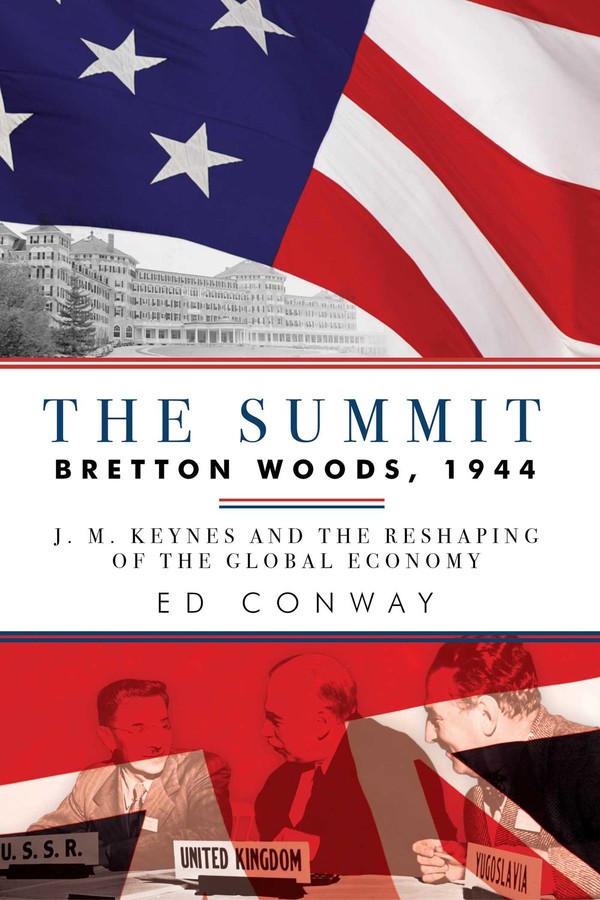

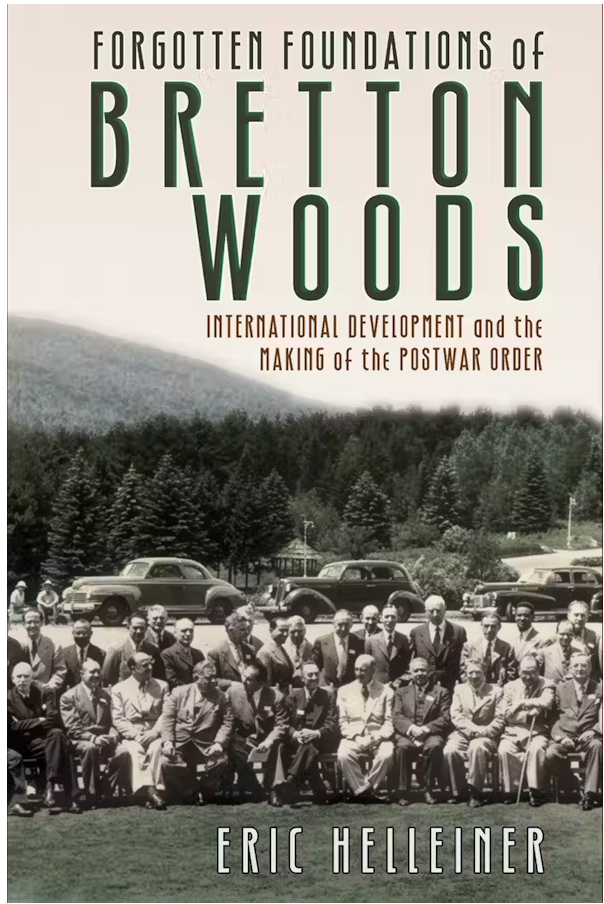

As the United States fought World War II, President Franklin D. Roosevelt was looking to lay the foundation for the world that would follow the fighting. He believed that the war had started in part because countries had pursued wrong-headed trade and monetary policies in the 1930s that intensified the Great Depression and fueled nationalism. FDR also knew that American firms and farmers would want to export to foreign markets once the war ended. Intent on correcting the mistakes of the past and hoping to spur future prosperity, Roosevelt convened a meeting of forty-four countries in July 1944 in Bretton Woods, New Hampshire. For three weeks, the delegates to the conference—known formally as the United Nations Monetary and Financial Conference—hammered out the rules for a new international monetary system. At its heart lay two new multilateral institutions, the International Monetary Fund (IMF) and the International Bank for Reconstruction and Development (most commonly known as the World Bank), which became the pillars of the postwar global economic order. SHAFR historians ranked the creation of the Bretton Woods System as the seventh-best U.S. foreign policy decision.

A list of featured comments

What Historians Say

Joseph Parrott

Associate Professor of History, Ohio State UniversityShaffer Bonewell

Doctoral Candidate in the Department of History, Southern Methodist University