China’s Customs-BOP Gap Is Not a Customs Problem

This is a joint blog with Brian Peters, a former risk manager and supervision officer at the Federal Reserve Bank of New York.

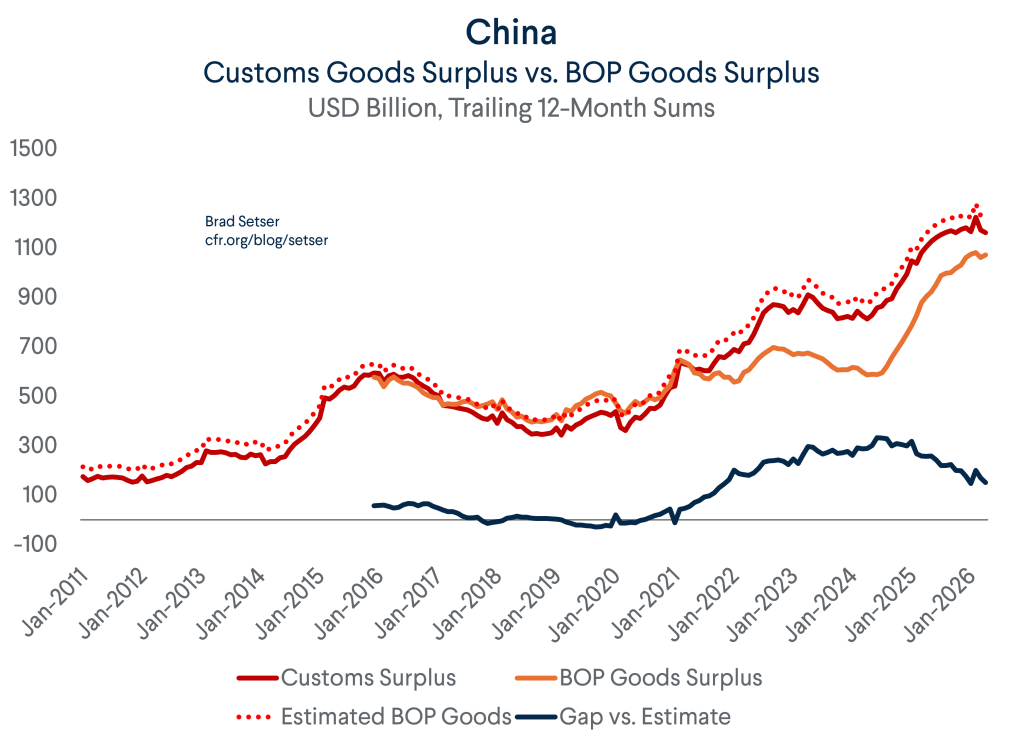

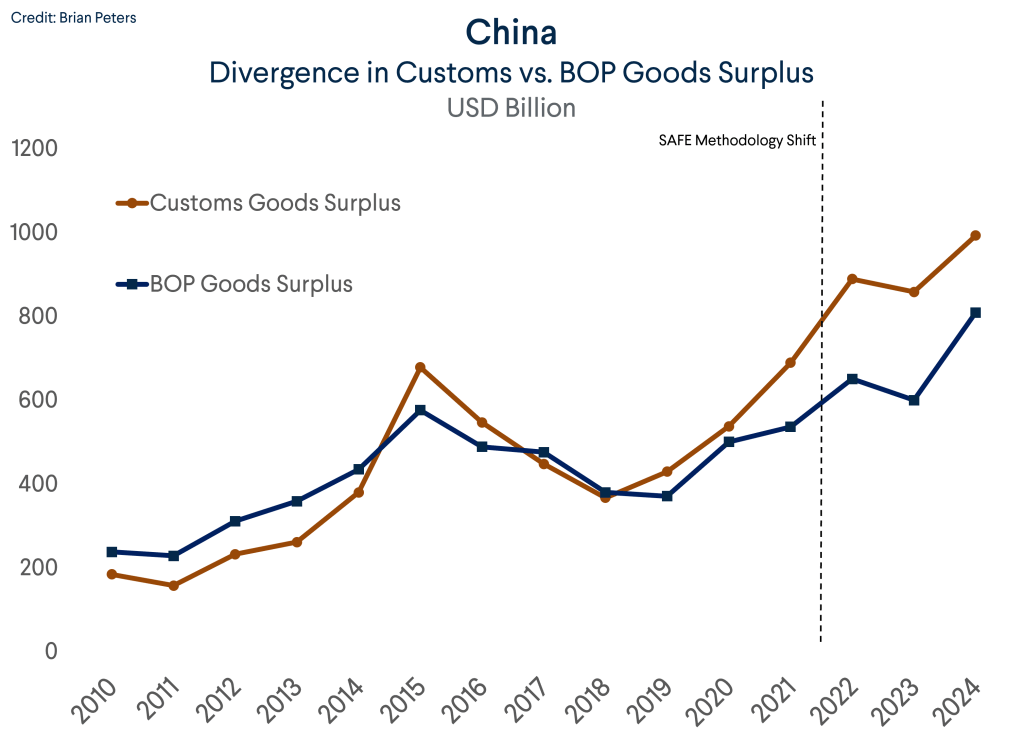

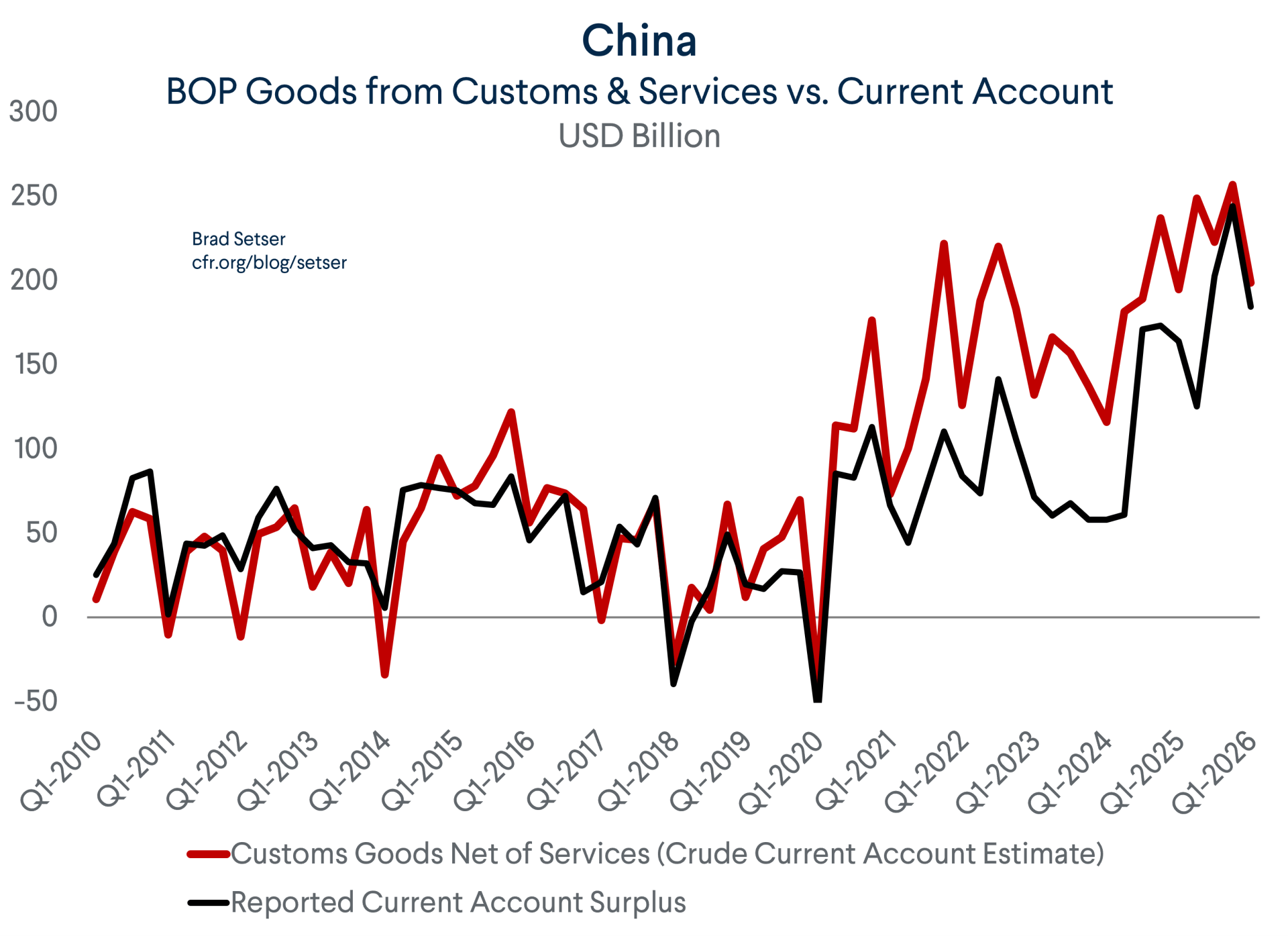

There are two significant reasons why China’s reported current account surplus ($735 billion) is much smaller than its goods surplus ($1.2 trillion), even after accounting for the ~$200 billion services deficit.

The first is that China inexplicably reports a $125 billion investment income deficit despite having $4 trillion in net foreign assets, even as Chinese interest rates are well below global interest rates. No one has been able to provide a credible explanation for this, including the IMF (see Box 1 of the 2025 External Sector Report– though no one in the official sector is yet willing to adjust China’s reported data to get rid of this gap.

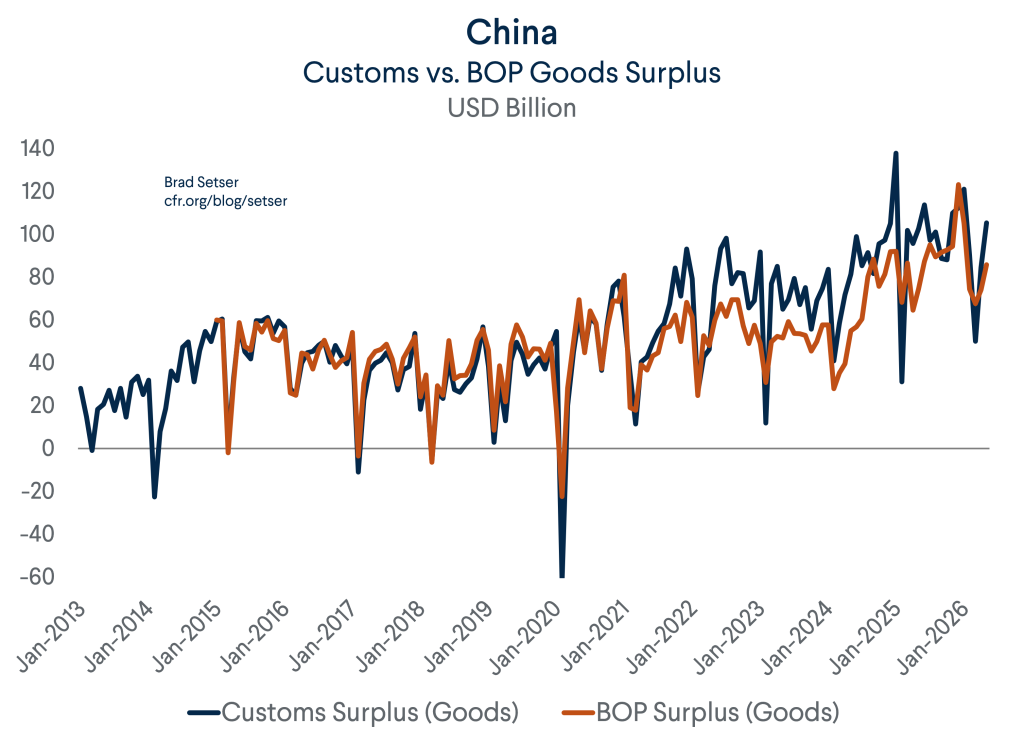

The second is that China now reported a substantially smaller surplus in the goods account of the balance of payments than the goods surplus that is reported by China customs (GACC). This gap only really emerged after China introduced a new methodology for calculating the goods balance in the balance of payments in 2022 (now phased into the 2021 data). In theory, this new series should be an improvement—but China never really has been able to explain what it is doing and why the new methodology lowered the reported overall surplus rather than just shifting around the components of the balance of payments (the most complete explanation of China’s methodology is provided in Appendix VII of the IMF’s 2024 Staff Report).*

It is possible to replicate the methodology that China previously used to calculate the goods balance in its balance of payments, as it was a straightforward adjustment to the customs data. The gap between the surplus in the old data and in the new data was around $150 billion in 2021, $240 billion in 2022, and peaked at roughly $260 billion in 2023, before falling back to $184 billion in 2024. A different high frequency dataset suggests a substantial fall to around $150 billion in 2025.

This gap is not a rounding error; it is larger than most countries’ current account balances. And it mechanically reduced the estimated undervaluation in the IMF’s methodology by about 7 percent in 2025.

Three explanations have been put forward for the gap.

Chang Ma and Shang-Jin Wei have argued in a serious paper that customs likely overstates exports through VAT-refund fraud and understates imports through tariff evasion, and that once you adjust for those distortions, the new SAFE numbers are reasonable—while the SAFE downward adjustment doesn’t stem from direct estimates of these forms of tax and tariff fraud, SAFE’s adjustment is directionally right, as the customs surplus is overstated.

China’s official line is narrower: SAFE points to bonded-warehouse and “factoryless”-production accounting, where goods that do not physically cross China’s borders are nonetheless attributed to Chinese trade flows. It specifically argued two things—the foreign firms that use contract manufactures to produce goods in China for the Chinese market should enter into the balance of payments goods data even if the goods never cross a customs border (technically true), and that the customs price reported by contract manufactures on their exports to global firms overstated the amount they actually received for their output (an empirical question, and one where the available data doesn’t support SAFE’s claim that smart phone prices are overstated in the customs data).

An earlier post on this blog offered a third reading, which is that the timing and quarterly volatility of the customs-BOP gap are not consistent with either of those statistical-reclassification stories, and the residual is more plausibly being constructed inside the SAFE adjustment itself so as to reduce reported errors in the balance of payments data.

What we haven’t had until recently is independent partner data to put the question on a different footing.

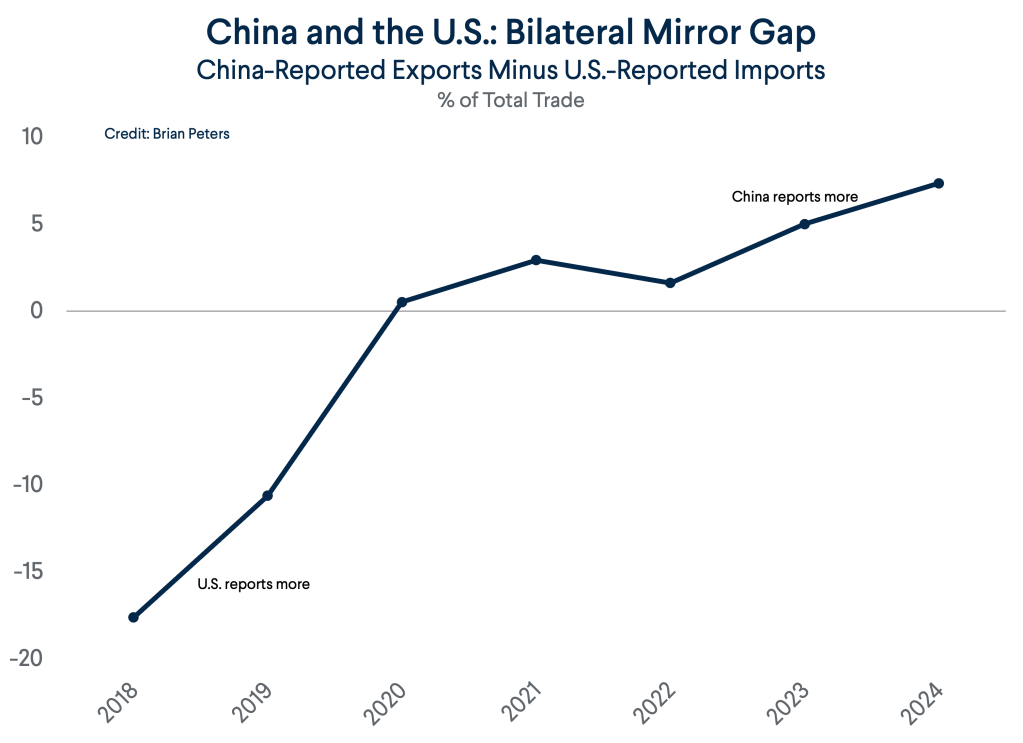

UN Comtrade provides exactly that. At least in principle, every dollar that leaves China’s customs as an export to the United States is also recorded as a dollar of U.S. imports from China. The two numbers should agree, up to the standard valuation gap; China reports on an FOB basis, the U.S. records on a CIF basis with a small markup for transshipment and insurance.

When the two series diverge persistently, you have direct evidence that one side is misreporting, and you can usually tell which side, because partner-side reporting is not subject to the same domestic accounting incentives. This is all the more true after taking into account “port” effects; trade through Hong Kong traditionally pulled U.S. imports above China’s reported exports.

The cumulative bilateral mirror gap, summed over 2018 through 2024, comes in at +1.3 percent —a headline that conceals as much as it reveals, as we discuss below. It is not consistent with VAT-refund fraud running anywhere near the scale required to explain a $184 billion customs-BoP discrepancy. If China were systematically inflating its export numbers at customs to facilitate fraudulent refund claims, the partner-side import data should show the inflation; it does not.

The bilateral pair, however, conceals a structural break. From 2010 through 2019 the USA–CHN mirror gap averaged roughly +14 percent, with the U.S. consistently recording more imports from China than China reported as exports to the US. From 2020 forward the gap inverts to roughly −3.5 percent, with China reporting more exports to the US than the US records as imports from China.

The break is sharp, it lines up with 2020, and several plausible candidates could be driving it: Section 301 tariffs and the resulting valuation wedge between transactional and customs prices, COVID-era logistics distortions, FDI relocation that puts more of the final value-added outside Chinese customs, and ordinary measurement drift. Mirror data alone cannot separate these candidates, but the level shift is real, and it is worth a separate examination.

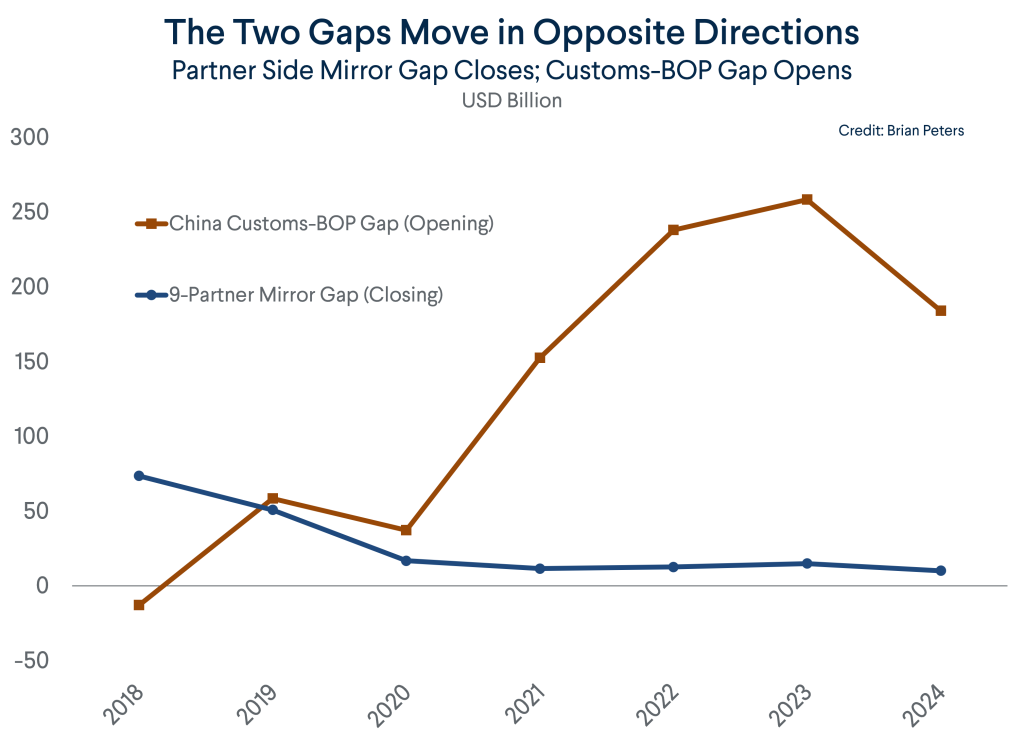

The bilateral story matters less, however, than what the mirror gap has done in aggregate across China’s major trading partners over the same window in which the customs-BOP gap was opening up. A balanced panel of nine major partners with consistent Comtrade reporting in every year (U.S., Japan, Korea, the UK, the Netherlands, Italy, India, Mexico, and Malaysia), covering roughly $640 billion of Chinese goods exports in 2024 shows the sum of mirror discrepancies falling from about $74 billion in 2018 to about $10 billion in 2024. The panel notably excludes Hong Kong, where Chinese exports are dominated by re-export routing that breaks the bilateral mirror logic, and a handful of other partners (Germany, Russia, Vietnam) where Comtrade public-preview data has reporting gaps. An unbalanced 12-partner panel that adds those three shows a larger fall, from $106 billion to $10 billion, but some of that reflects composition drift, so the balanced nine-partner figure is the cleaner read.

This is the key observation. The partner-side mirror gap closed in 2018–2020 and has stayed within a $10–17 billion range from 2020 forward. The customs-BOP gap then opened up sharply from 2021, reaching $259 billion in 2023 and $184 billion in 2024. The two divergences are not synchronous, and the order matters: the mirror gap closed first, and the customs-BOP gap then opened up by an order of magnitude while the mirror gap stayed flat. If the customs-BOP gap were being driven by misreporting at China’s customs interface—VAT fraud, tariff evasion, or anything else that systematically distorts bilateral flows—it should show up as a widening mirror gap, or at least a non-closing one.

That has a simple implication. Whatever is driving the divergence between the customs goods surplus and the SAFE goods surplus is invisible to partner customs. It is not “China’s customs is over-reporting exports relative to what partners receive.” It is not “China’s customs is under-reporting imports relative to what partners ship.” It is something internal to the SAFE construction of the goods balance.

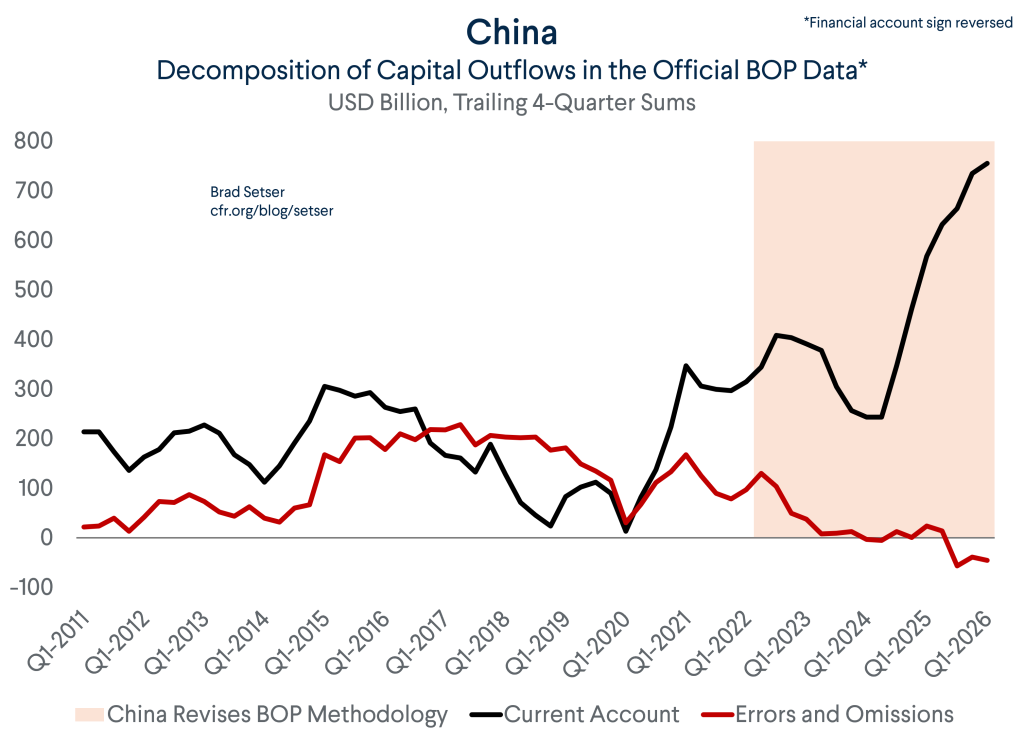

This narrows the potential explanations considerably. The possibilities that survive the mirror test are: bonded-warehouse and factoryless-production accounting (China’s official explanation), value-of-services-embedded-in-goods reclassification at the BOP boundary, transfer-pricing adjustments at the BOP level that customs does not make, and discretionary smoothing of the residual. The corroborating evidence has always been the fit between the reported current account residual and the foreign asset accumulation of China’s state banks; that fit otherwise has no plausible mechanical explanation, and the mirror exercise foreclosing the customs side channels makes that bank flow correspondence harder, not easier, to dismiss as coincidence.

The first two are statistical artifacts; you would expect them to be relatively stable from quarter to quarter and concentrated in identifiable sectors. The third should leave fingerprints in the services or primary income account. The fourth, which earlier posts on this blog have flagged, is that SAFE is constructing the goods balance to keep the BOP residual error close to zero.

The mirror data does not directly demonstrate that fourth reading, but it is consistent with it in a way the other three are not, particularly given the quarterly volatility of the customs-BOP gap.

There is a temptation to read China’s customs-BOP gap as a generic EM story about capital controls and managed FX, the kind of thing one might expect from any country with a similar policy mix. However, cross-country panel evidence on the customs-BOP gap shows that the larger systematic deviations come from multinational-residence reclassification (Ireland, Singapore, Luxembourg, sometimes the Netherlands), not from capital controls manipulation. China’s case is distinctive; it is not a generic feature of managed FX with capital controls.

What does any of this mean for the underlying Chinese current account surplus? On its face, not much directly. Mirror data does not tell you where the gap is; it tells you what you can rule out. It forecloses the customs-misreporting channel as a quantitatively significant driver, which leaves the SAFE-side adjustment as the most important piece of the puzzle. And that adjustment has been incredibly volatile in recent quarters (with the last big gap that still impacts the trailing 4 quarter sum back in q2 2025).

The case that the underlying current account surplus is meaningfully larger than the reported $735 billion has been made on this blog before; the mirror exercise is a clean check that the customs side of the ledger is what it appears to be, and that the discrepancy lives elsewhere.

* The new methodology clearly shifts Apple’s “in China” profit over to the goods portion of the balance of payments, which should have generated offsetting adjustments to either the services or the income balance.