Currency Moves Can Drive Rebalancing

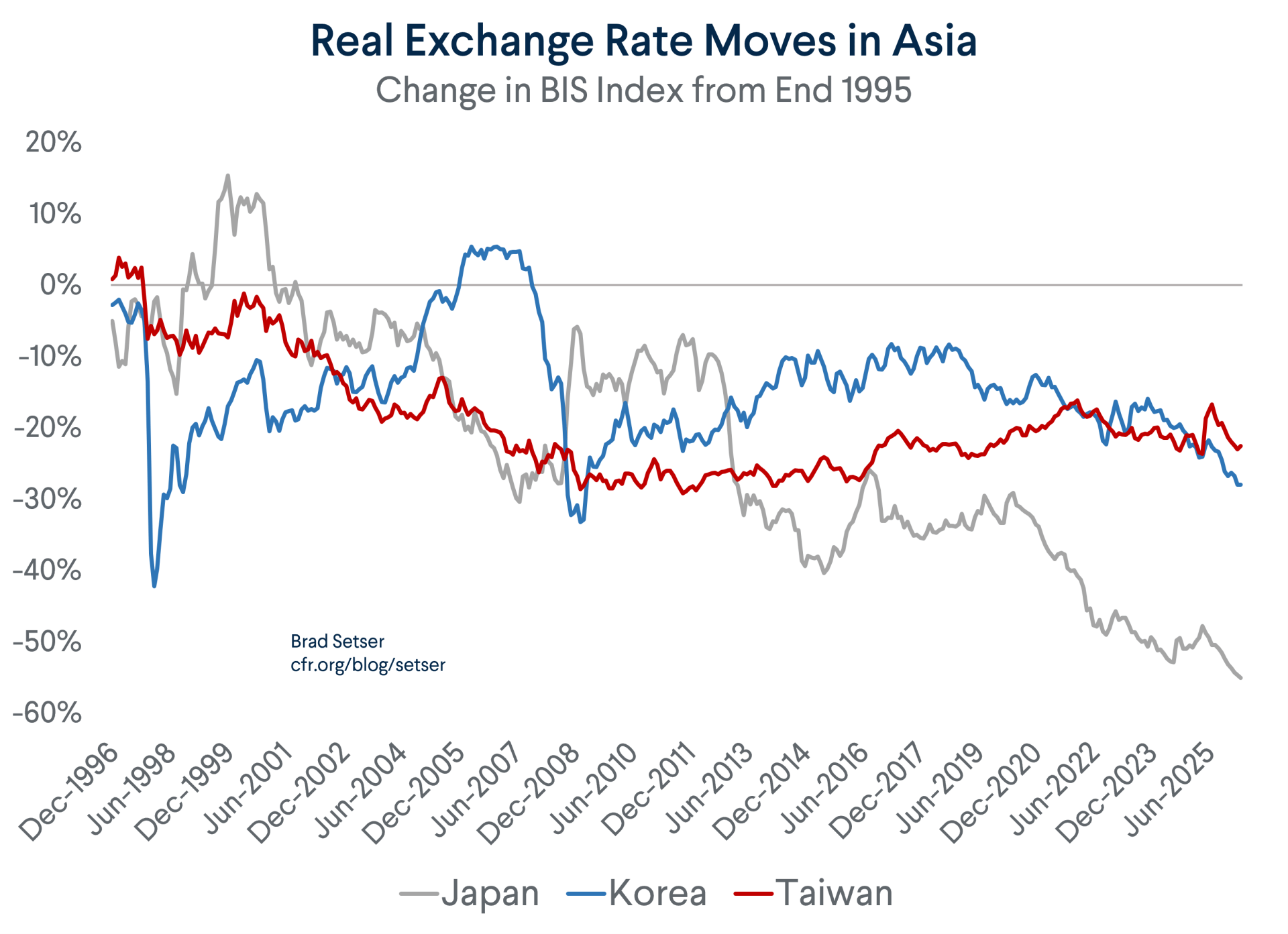

The currencies of Asia’s major economies are all substantially undervalued

This is a joint blog with Shahin Vallée of the German Council on Foreign Relations

Shahin Vallée and I have a piece in Foreign Affairs that calls for bringing currency diplomacy back and making the appreciation of China’s currency the central ask of the G7 and its partners.

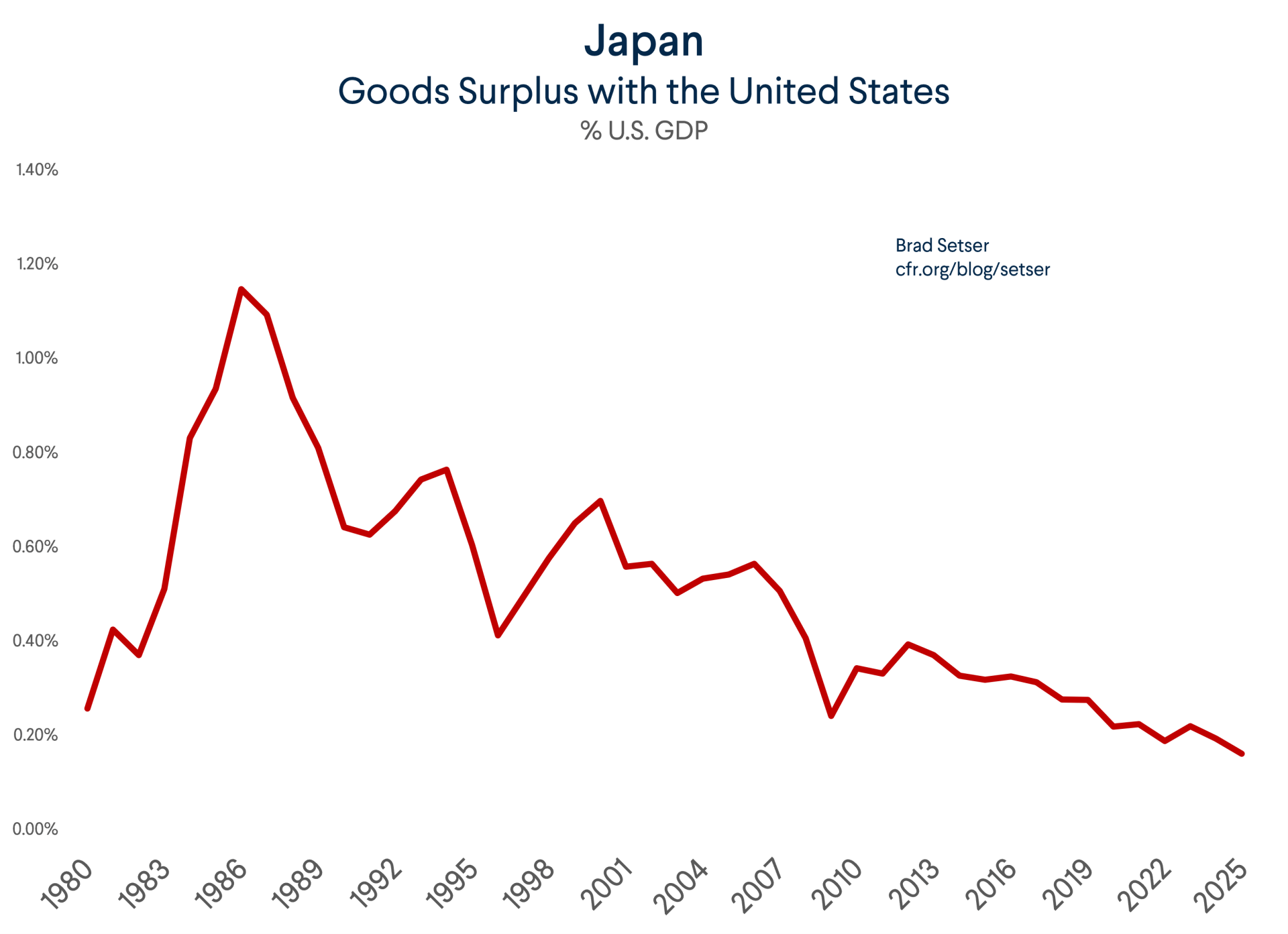

Given the broad weakness of the currencies of all the big Asian surplus economies (Japan’s surplus is from investment income; Korea and Taiwan run exceptionally large trade surpluses) we call for coordinated action to raise the value of all the key Asian currencies. China can strengthen the renminbi by just setting the daily fix at a stronger and stronger level. We would also welcome coordinated G7 support for the won and yen so all the major Asian currencies strengthen.*

Realistically, this isn’t going to happen soon. Prior to the Evian leaders summit the G7 finance ministers and central bank governors of the G7 agreed on a plan that doesn’t even mention the level of the yuan. President Trump remains focused on tariffs and the bilateral U.S.-China trade balance when he is not distracted by Iran or other matters.

But it needs to happen eventually. It is hard to see how global trade imbalances (linked of course to different patterns of savings and demand across countries) can be reduced without a realignment of global exchange rates.

Indeed, our view is that there needs to be renewed appreciation (ha!) of the role that currency can play in bringing down trade imbalances.

That will require a shift in how many in the IMF—and many prominent economists, including the G7 Economist group that the French convened—are thinking about the issue. The current consensus tends to play down the immediate importance of changing the value of key surplus and deficit economies, and to argue that that shifts in underlying policies need to precede and in a sense drive subsequent currency changes. We would reverse that—a currency move will change the flow of trade on its own, and it will then need to be supported with domestic policy changes (including more support for domestic consumption in China and a bit of fiscal restraint in the United States) that make it easier to sustain the change in currency values. We aren’t alone here. Malcolm Scott of Bloomberg put it well: “If exports stall, policy makers will step in to do more to prop up domestic demand, but while ever the external sector remains robust there’s less need for significant stimulus.”

In our view, the proposals that emerged out of recent work by the IMF and a group of prominent international economists convened by France doesn’t provide the needed basis for a global conversation on how best to reduce the risks posed by imbalances—largely because this effort to force a new consensus doesn’t go far enough in three important respects:

First, it misreads the financial history of the pre-global crisis period by neglecting the role of reserve accumulation in the financing of the United States prior to the global financial crisis. Unprecedented reserve growth drove large inflows of official capital into the bond market. There is no surprise that this inflow came as the dollar depreciated – an unwillingness by surplus countries to allow their currencies to appreciate even as U.S. rates were below global rates led to a surge in intervention, and proceeds of that intervention needed to be invested primarily in U.S. safe assets. This core uphill flow was clearly an official flow from Asian central banks; it was pushed out of surplus countries by reserve accumulation not pulled into the U.S. by the high returns on U.S. housing investment. Banks then created synthetic safe assets in part to meet demand from private investors pushed out of the Treasury and Agency market by official actors.

Second, it downplays the role that exchange rates have played in causing or reducing imbalances.

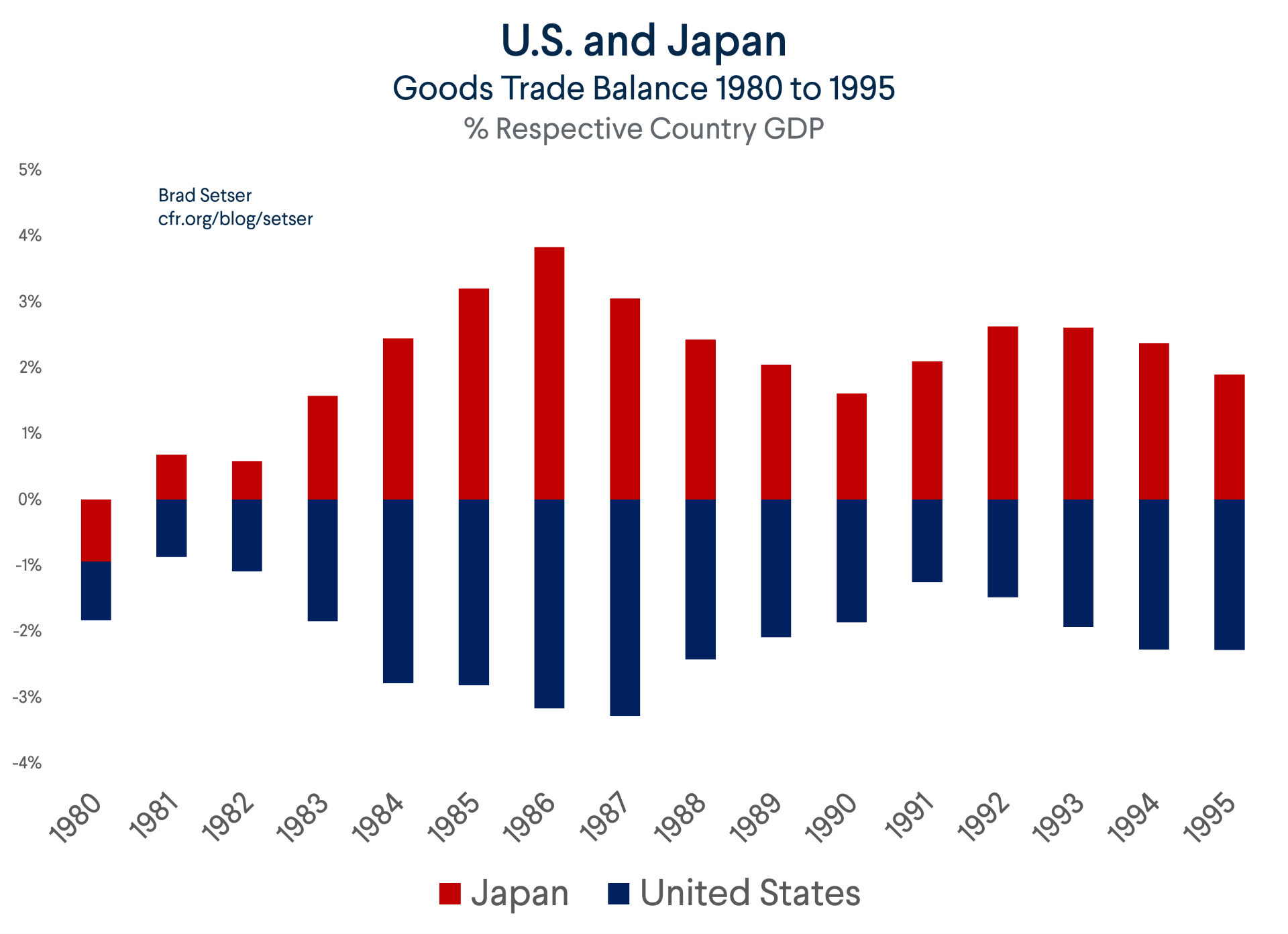

This stems in part from a misreading of the 1980s Plaza Accord that makes exchange rate coordination a sideshow and attributes the entire fall in the U.S. trade deficit to the fiscal consolidation that occurred over the course of Reagan’s second term rather than to the dollar’s large fall.**

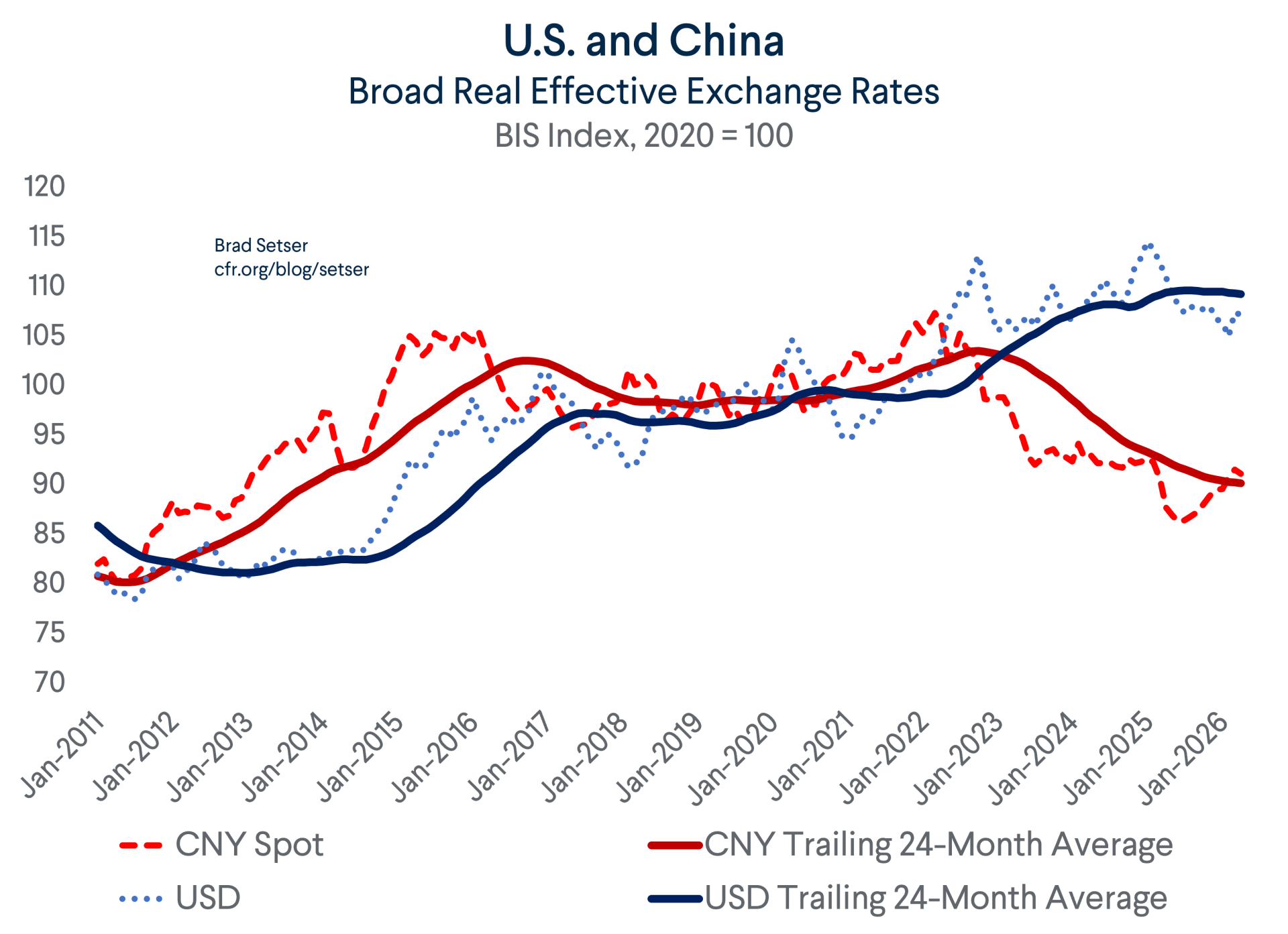

It also draws on an interpretation of the financial history of the last 25 years that ignores the role a weak yuan from 2002 to 2006 played in the rise in China’s external surplus prior the Lehman shock and the role a stronger yuan played in bringing down China’s surplus down during the years after the global financial crisis. This shunted view of history results in a new excuse for ignoring currency intervention, namely that changes in the nominal exchange rates don’t drive changes in the real exchange. There though is ample empirical evidence to the contrary. Domestic prices are sticky and adjust slowly; as a result, nominal exchange rate moves are only offset by changes in the level of domestic prices slowly and partially.

Third, the IMF paper posits a strong dichotomy between “micro” and “macro” industrial policies. This distinction that the IMF draws between “macro” industrial policies (including intervention to weaken a currency) and “micro” industrial policies (sectoral support, whether from directed purchases, directed lending or outright subsidies) is theoretically helpful. But the correlation between macro industrial policies and micro industrial policies across Asia makes sorting out the relative contributions of micro-industrial policies and currency policy difficult. In practice, there is much more continuity between micro and macro industrial policies than in the IMF’s models—and the countries generally judged to have the most successful “micro” industrial policies also often have active “macro”-industrial policies to support exports through undervalued exchange rates. The interaction between the two often seems to generate large and persistent surpluses—the exports from industrial policy success stories making creating a political economy that makes policies suppress domestic consumption more sustainable over time. Sorting out the different impact of macro-industrial policies and micro-industrial policies is all the more difficult because the IMF’s standard framework for external assessment still doesn’t capture many policies—outflows through a sovereign wealth or pension fund, the buildup of foreign exchange in a state banking system—that would appear to meet the IMF’s definition of a “macro” industrial policy, and that in many cases have a clear impact on the foreign exchange market.***

In our view, this work—unfortunately—cannot produce an actionable agenda. It suggests nothing can be done until Chinese domestic policies change or U.S. fiscal policy changes. That is a recipe for inaction, and one that will result in ever more pressure on Europe’s already challenged industrial base. The status quo isn’t static; it is associated with a China that gets its growth heavily from net exports and thus its is associated with an ever-rising Chinese surplus.

Waiting for China to change its pattern of growth through reforms that support household consumption thus isn’t really a tenable option for those countries that are seeing their own exports squeezed by China’s growing surplus. Waiting for the U.S. to bring its fiscal deficit down means accepting the growing weight Treasury supply places on global financial markets will continue. The demand for the world’s goods created by U.S. fiscal deficits helps make up for the demand deficit generated by China’s surplus, but at the cost of a slow build-up of macro-financial risks.

At a time when the global surplus is concentrated in East Asian surplus economies that all have weak currencies—and with China now putting the weight of its state financial sector on the market to limit the pace of yuan appreciation, a coordinated appreciation of Asian currencies is the simplest and easiest way to bring down trade imbalances. China surely cannot be coerced by any actor, neither the U.S. nor the G7 to change its exchange rate policy but it could possibly be persuaded that its own interests would be served by a coordinated revaluation of other currencies in Asia. This is all the more the case if China comes to understand that the alternative to a stronger renminbi is ever growing restrictions on its trade.

Currency diplomacy alone is not sufficient to durably reduce trade imbalances. But it can start the process. If China gets less growth from exports, it will face more pressure to undertake the reforms needed to strengthen domestic sources of growth. The same process would play out in other surplus economies—including Taiwan. And smaller surpluses—or at least a slower pace of growth in the world’s surpluses—would place a bit more pressure on the U.S. to reign in its fiscal deficit.

A bit more coordination to strengthen Asia’s obviously undervalued currencies is thus the right place to start the broader process of a coordinated rebalancing.****

* Korea is already supporting the won by adjusting the allowed hedge ratio of its massive National Pension Service (~ $600 billion in foreign assets, mostly unhedged); Japan could do more to support the yen as well notably through a faster pace of rate normalization. The Bank of Korea’s governor Hyun Shin has already indicated that the Bank of Korea will hike rates further given the demand pressures linked to the memory chip windfall.

** Trade adjusts to changes in exchange rates with a lag (usually thought to be 8 quarters but some work suggests that it might now be more like 12 quarters. The Plaza agreement didn’t bring the U.S. deficit down immediately, but by 1987 the real U.S. trade deficit was clearly shrinking. The overall trade deficit fell from around 3 percent of U.S. GDP to around 1 percent of U.S. GDP) between 1987 and 1990. This fall occurred even with strong demand growth in the US in 1988 and 1989, so it wasn’t just a function of underlying shifts in the global pattern of demand growth. Net exports contributed positively to U.S. growth once the dollar had clearly moved off its 1985 highs across the cycle. Japan’s surplus also fell from 4 percent of GDP to 2 percent of GDP—with a large reduction in its bilateral surplus with the U.S.

*** Ask the Bank of Korea. Former governor Rhee has highlighted how the NPS outflow worked at cross purposes with his efforts to support the Korean won.

**** The IMF’s argument for coordination—namely that it would be easier to bring down surpluses and deficits without a loss of growth if all three of the world’s big economies acted simultaneously—is correct. China needs to do more to support its domestic growth so that slower growth in exports doesn’t reduce output and increase deflationary pressures. The U.S. needs to reduce its fiscal deficit so that it is less of a magnet for imports and capital, and to create space for higher exports without overheating. And with less demand from the U.S., Europe needs to do more to raise investment and to support its own growth.

Colophon

Guest Author

Shahin Vallée