From Greek Spreads to German Votes to . . . Greek Spreads?

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Dinah WalkerAnalyst, Geoeconomics

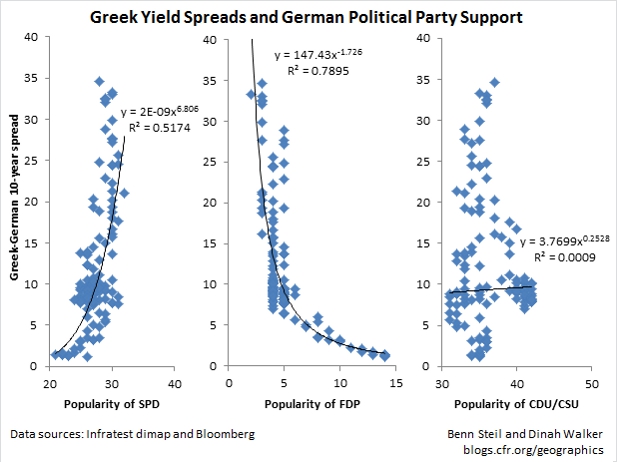

The German federal elections on September 22 could be of enormous consequence for Greek solvency – and the future of the eurozone. Today’s Geo-Graphic shows that Greek solvency may itself be of great consequence to the German elections.

As the figure shows, when the yield spread between German and Greek government bonds falls (and market optimism for Greek solvency rises), support for the small right-of-center, free-market German FDP party rises. (The FDP is currently part of the Merkel-headed, CDU-led government.) When that spread rises, however, support for the FDP falls, while support for the left-of-center SPD party rises. (Support for Merkel’s CDU is invariant to shifts in Greek sentiment.)

The International Monetary Fund has been making waves of late, not least in Germany, by casting doubt on Greece’s solvency – most recently, projecting a financing gap for Greece opening up in August of next year. IMF rules forbid Fund lending to countries with projected financing gaps over the coming twelve months.

Yields on 10-year Greek government bonds are up about 50 basis points over the past month. Market optimism or pessimism on Greece over the next two weeks could have a material impact on the German election outcome. Greco-pessimism could dampen FDP prospects, possibly pushing them out of the Bundestag entirely. The result would be months of uncertainty – as in 2005, when it took two months for a “grand coalition” CDU/CSU/SPD government to be put into place. Another round of elections is a possibility. In any case, it will be very hard to get a coherent German response to Greece – not to mention important wider eurozone issues, such as banking union – for some time. Such a prospect could result in further spiking of Greek yield spreads, reviving the eurozone crisis at a time when the eurozone will be least able to deal with it.

Au weh!

Read about Benn’s latest book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”