Ten Key Takeaways From Treasury’s Foreign Exchange Report

Brad W. Setser, a CFR senior fellow specializing in global trade, analyzes the U.S. Treasury Department’s June 2025 Report on Macroeconomic and Foreign Exchange Policies of Major Trading Partners of the United States

The U.S. Treasury Department provides a report to Congress each year detailing and assessing developments in international economic and exchange rate policies. This semi-annual report, required by law, focuses on close U.S. trading partners that make up about 78 percent of U.S. foreign trade in goods and services. Given the substantive changes to trade that the United States has adopted since President Donald Trump returned to the White House, this report takes on new significance this year. Brad W. Setser, a senior economics fellow at CFR, went line by line through the executive summary of the June report and broke down the document’s latest conclusions.

Setser: There are no crazy manipulation designations made for political points or other unexpected surprises in this report, but it is still an important document. This report commits the Treasury to making long overdue technical adjustments to its methodology that will increase the odds that countries are labeled “currency manipulators” in the future. Taiwan is at particular risk, as is China. Let’s dive in.

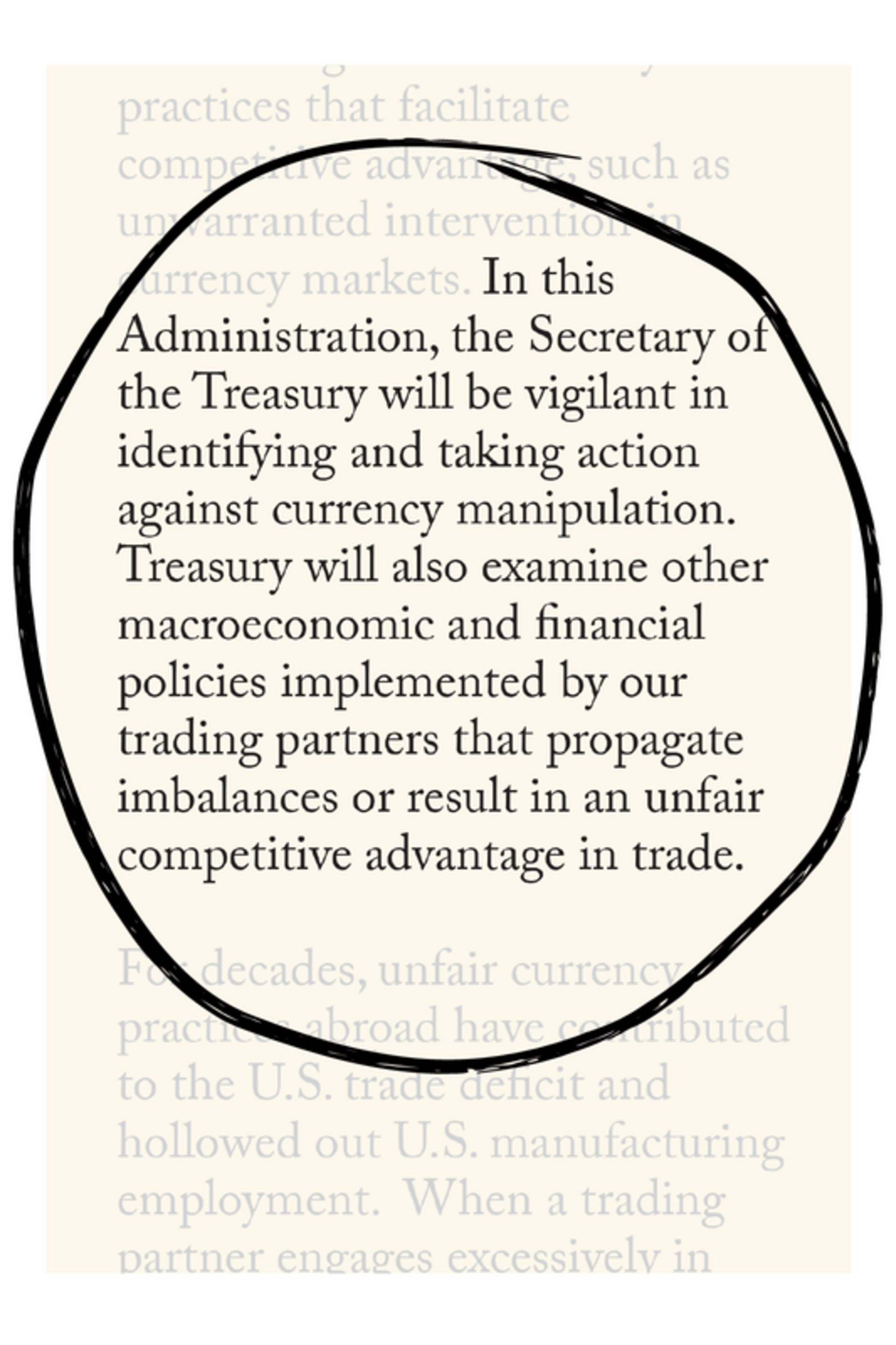

Sounds tough, but this statement is generally in line with past policy. Most recent Treasury secretaries would be comfortable making these points. In fact, Yellen made this clear in 2021, noting that the intentional targeting of exchange rates is “unacceptable.”

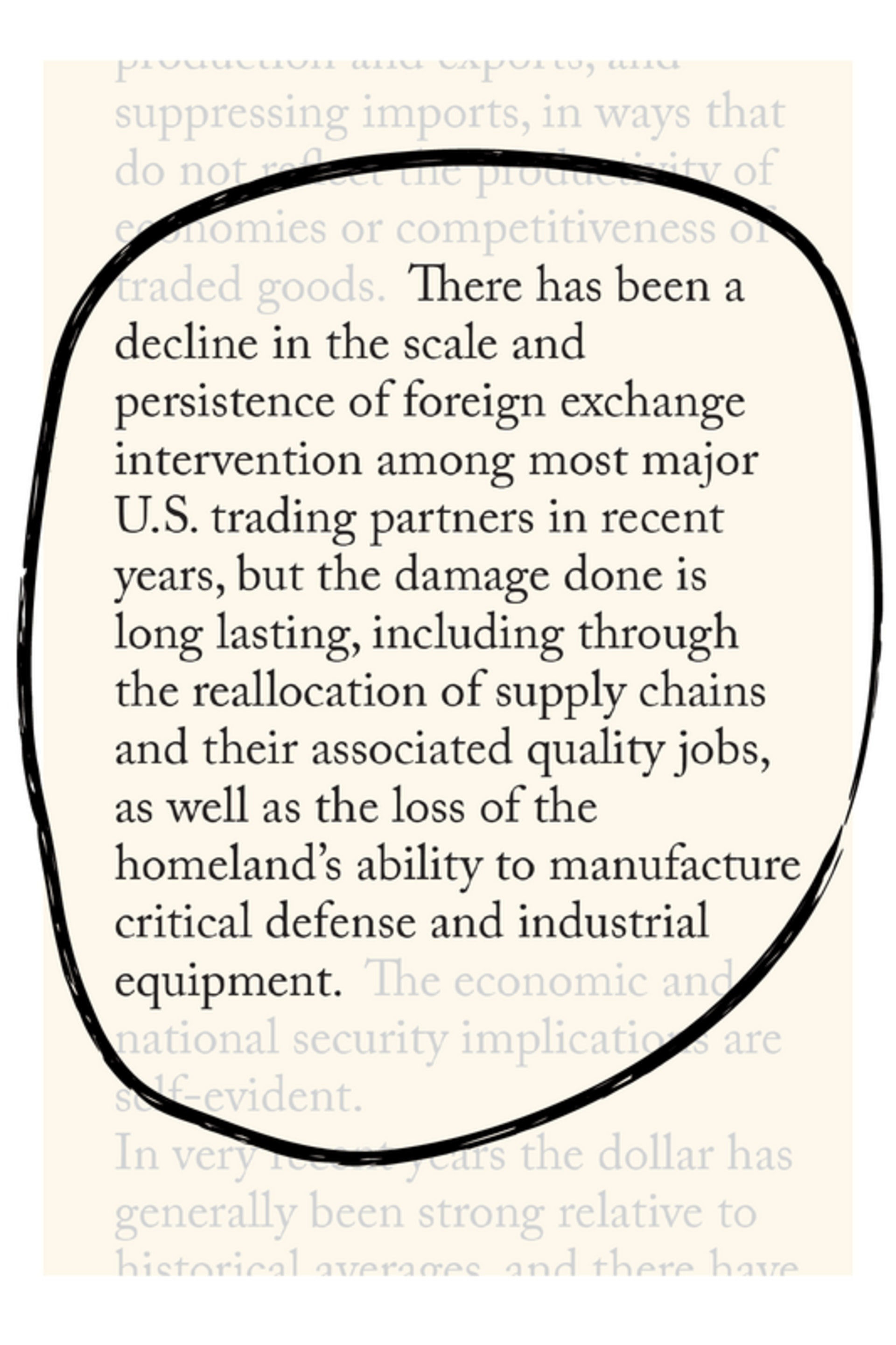

This statement is new, and sets the analytical foundation for looking at past intervention as well as current intervention in future reports. It is also accurate in my view.

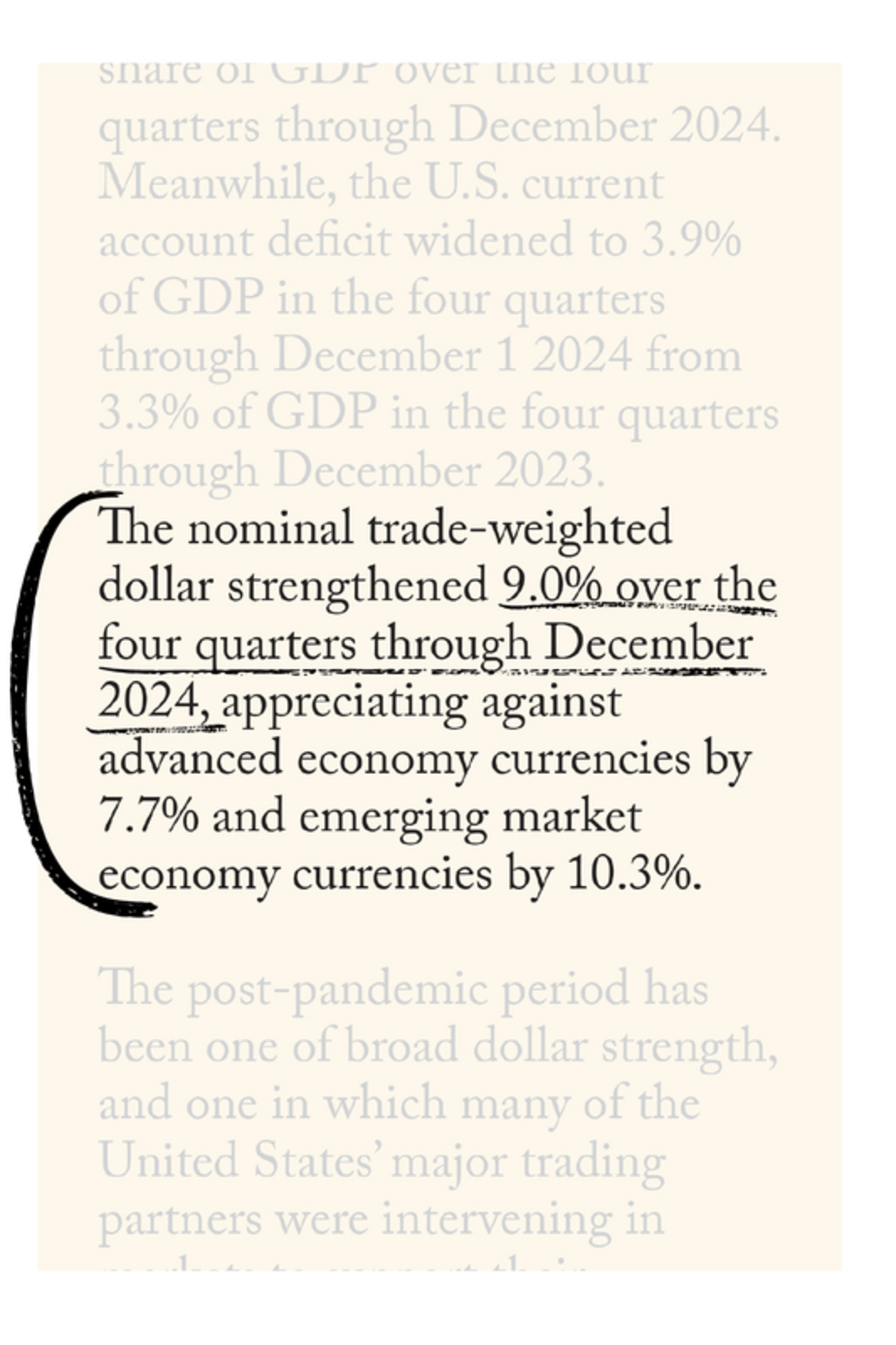

This is something that is often missed in the discussion about the dollar’s reserve currency status. The dollar is exceptionally strong, even for a reserve currency. And if the dollar had stayed at its 2024 levels, the U.S. trade deficit would almost certainly have kept on growing.

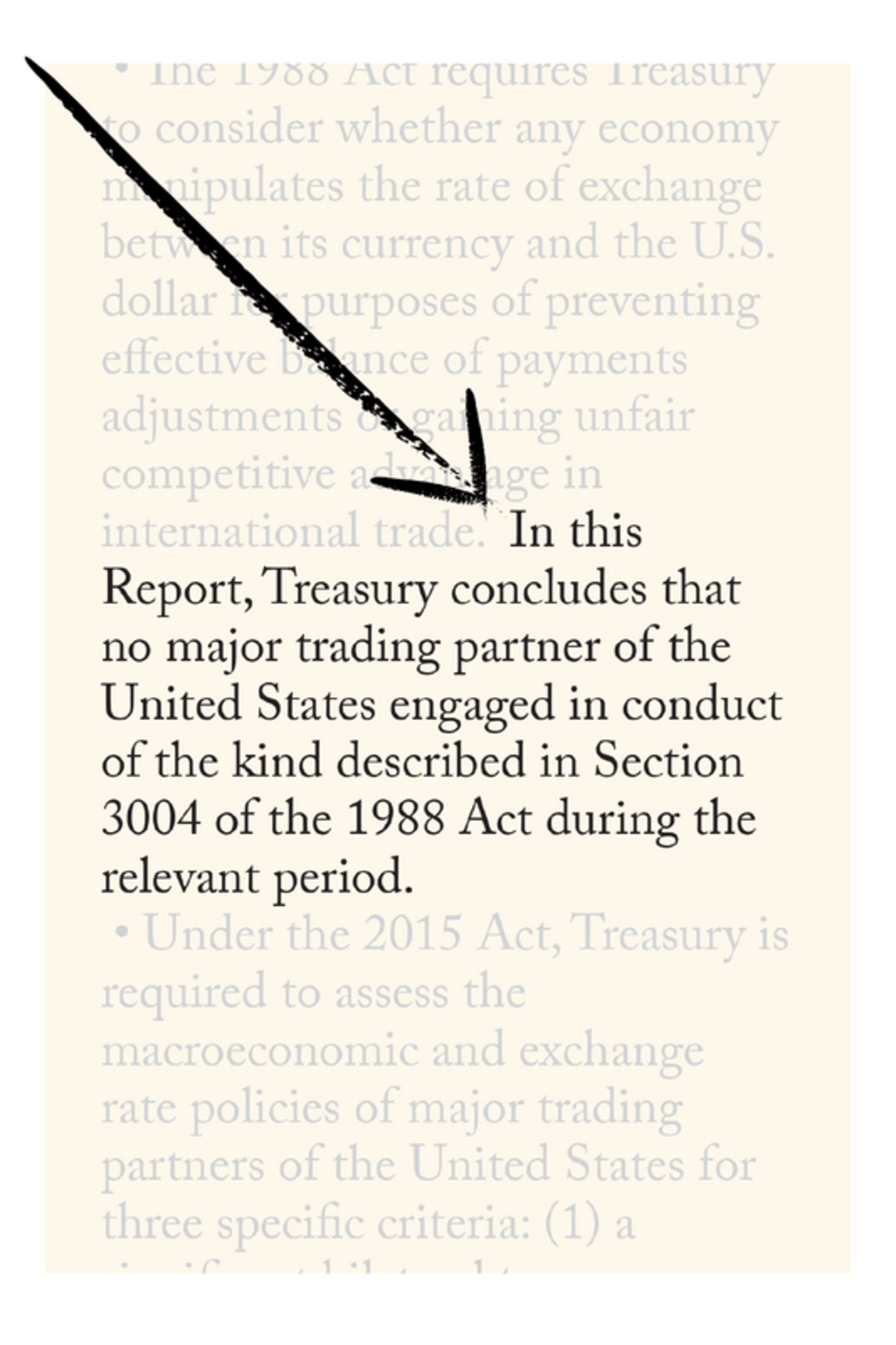

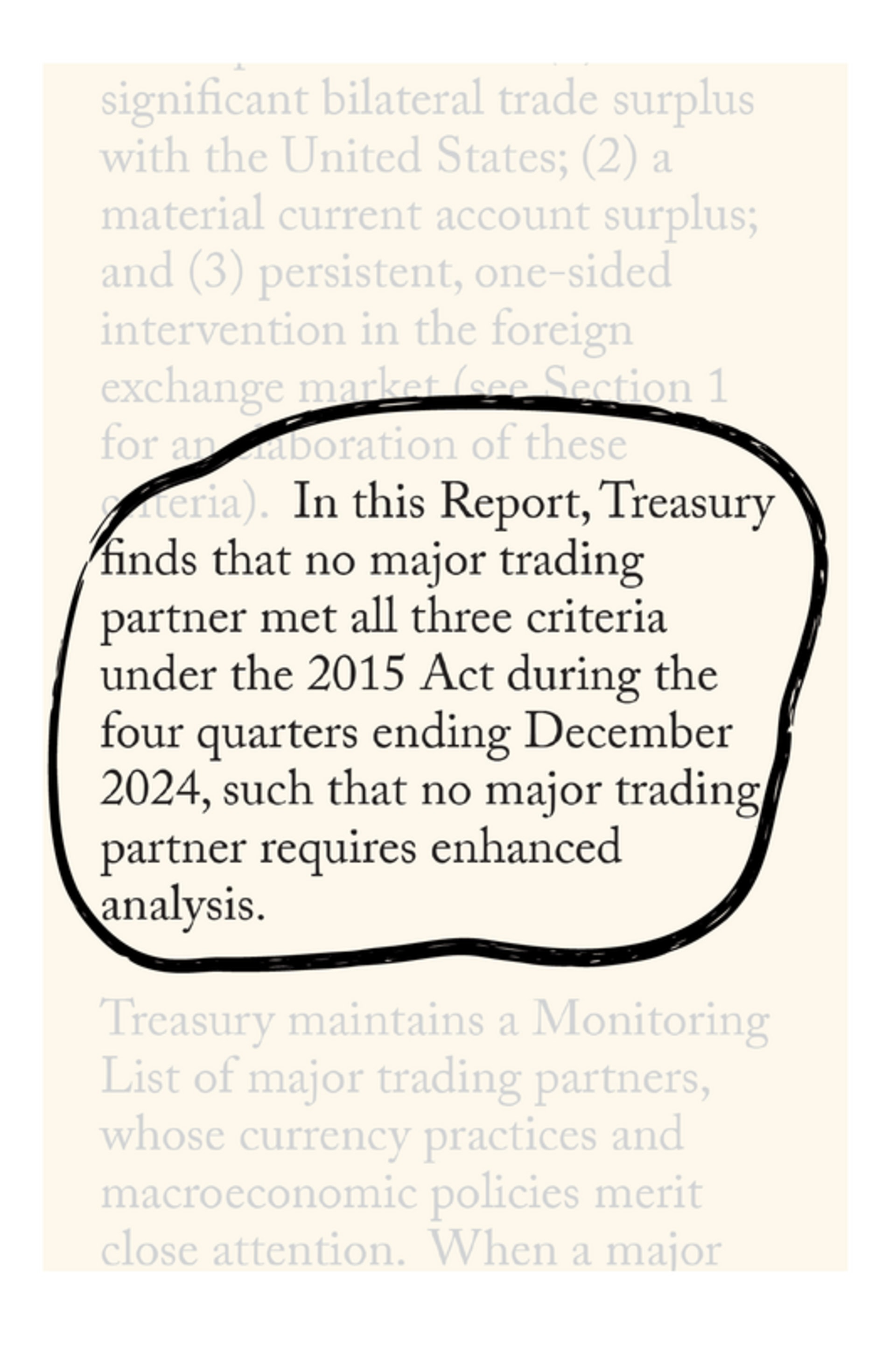

This is often the only line the press reads—no one was called a manipulator. This isn’t a surprise though. No one was really intervening heavily to hold their currency down in 2024.

This is 100 percent as expected. The big economies just weren’t active in the foreign exchange market in 2024. This year will likely be different, as intervention tends to pick up when the dollar depreciates. Taiwan, for example, added $10 billion to its reserves in May. If this pace of intervention is sustained for several months, that would almost assure that it would meet the criteria in the next foreign exchange report.

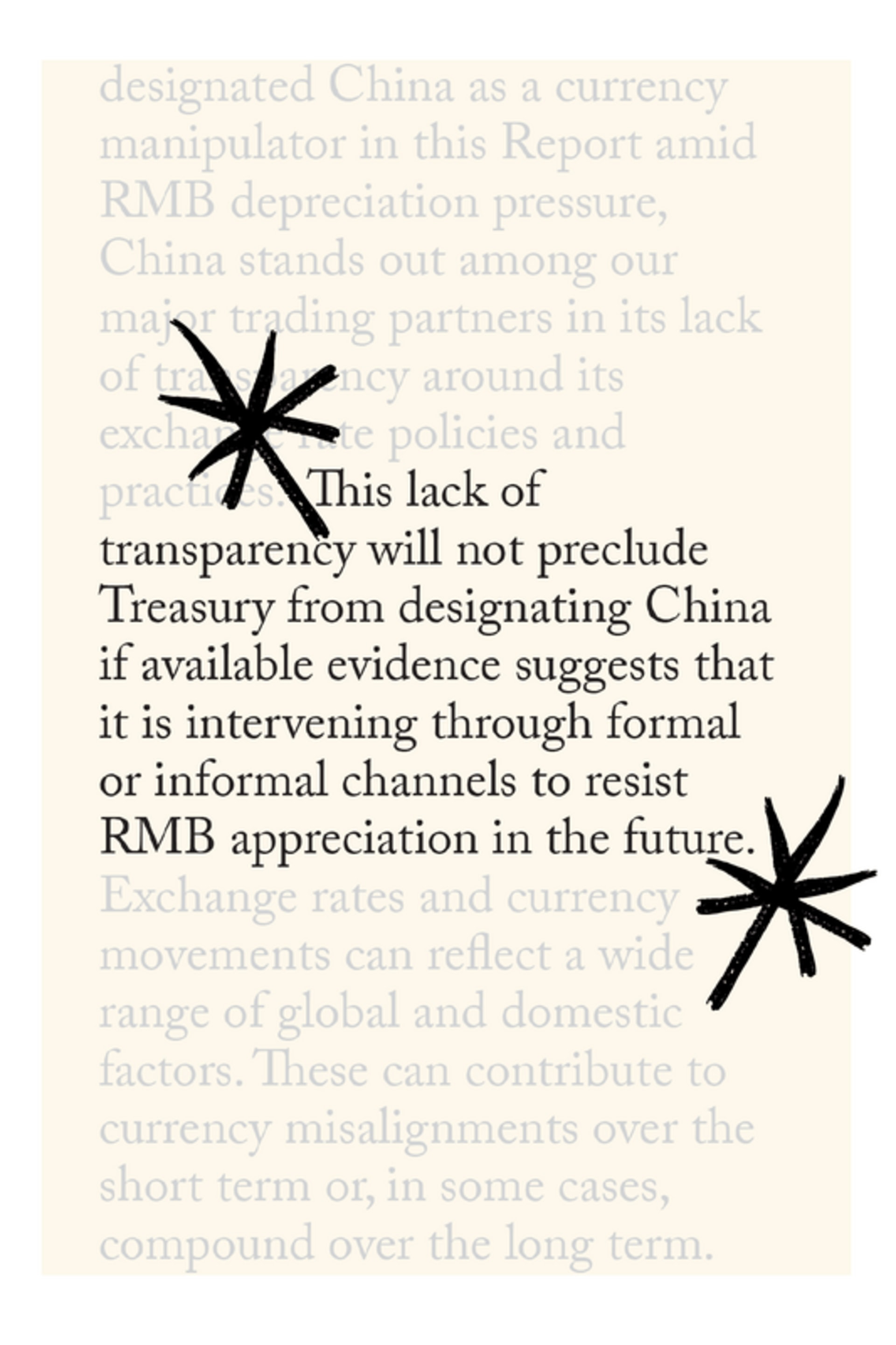

This is probably the most important line in the Executive Summary. China has gotten very good at disguising its intervention. The country’s central bank appears to do very little on its own balance sheets. Instead, all of the activity appears on the balance sheets of the state banks. That won’t stand in the way of a designation going forward, so watch this space. (It is also worth noting that going after China for hidden intervention will require the Treasury career staff to raise their game. This will be much harder than dinging a country for visible intervention.)

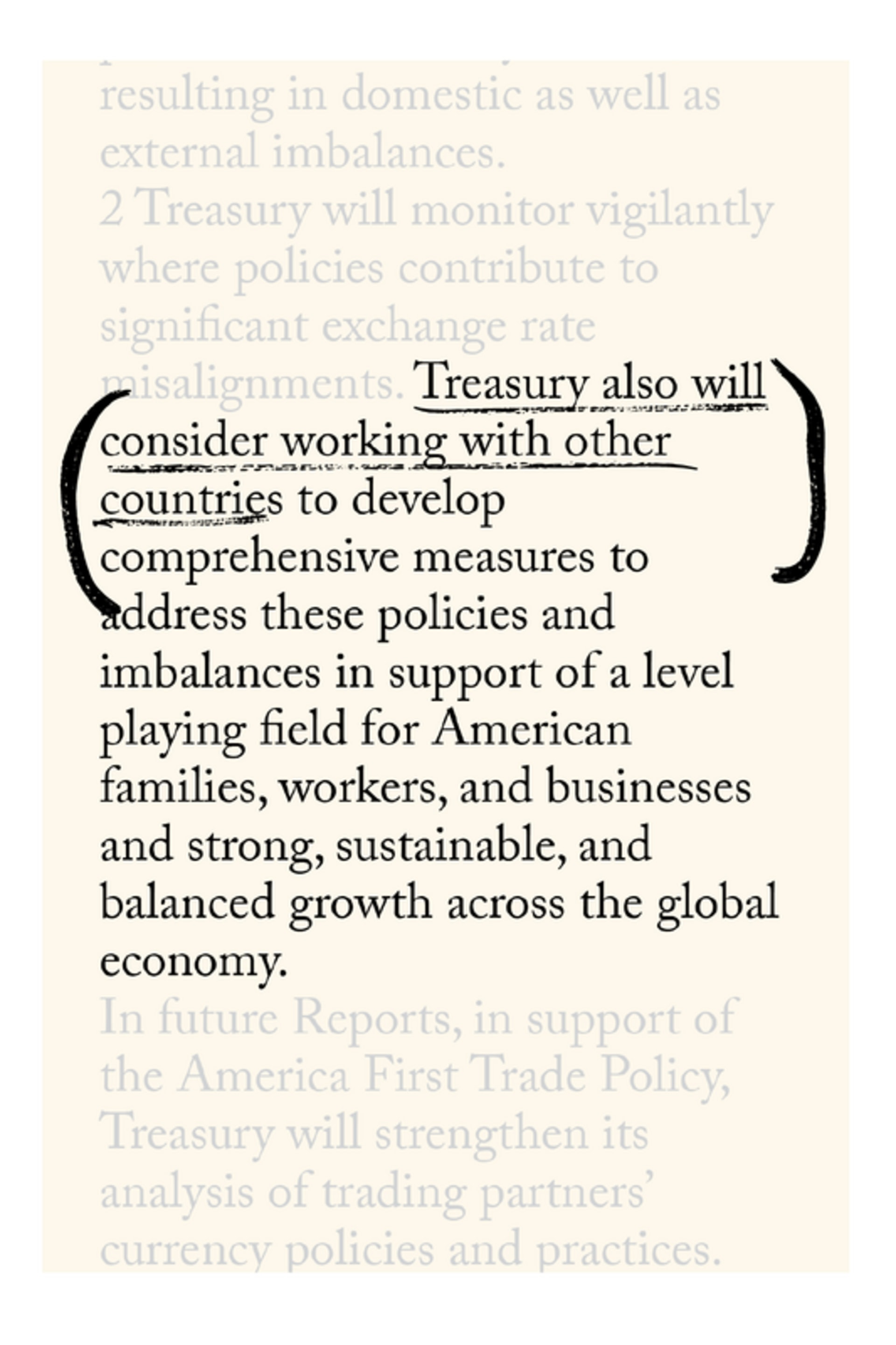

Woah, the Trump administration hasn’t ruled out working with other countries—this may not be just an America alone policy. This could be a reference to more G7 work on the issues of global imbalances. France, which will lead the G7 next year, is quite interested in this. This could turn into something real.

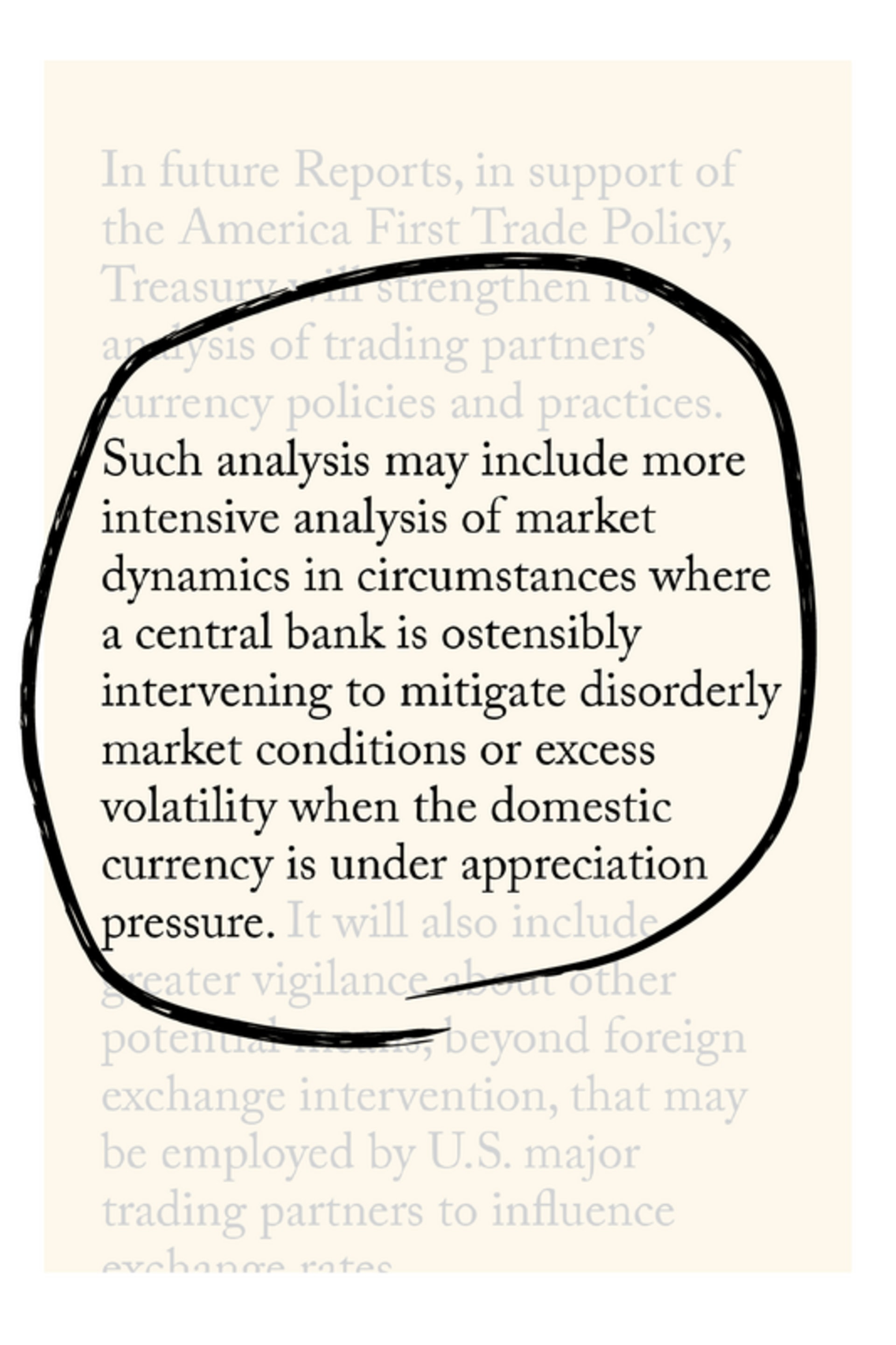

This is an important signal. Countries that intervene always say that they intervene with the intent to “smooth” volatility even if in practice they are targeting a specific level for the currency. Subjecting these claims to more scrutiny is a good change that could have real consequences. Taiwan intervened at the 30 Taiwan dollar to the U.S. dollar mark for most of May.

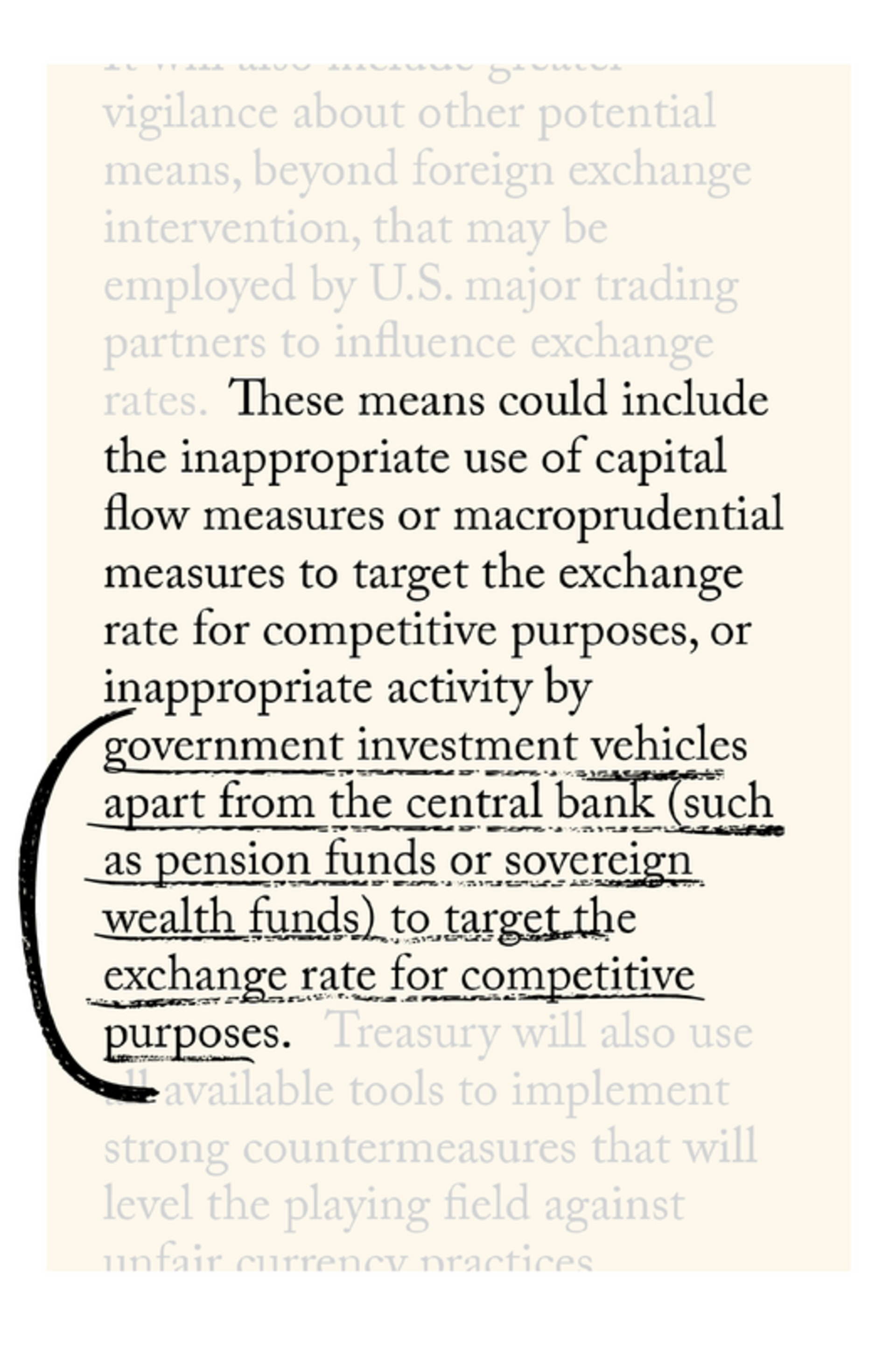

This is new. Until now, the foreign exchange report has ignored the activities of sovereign funds. That makes this shift potentially significant, as Japan, South Korea, and Singapore all have large sovereign funds and large external surpluses.

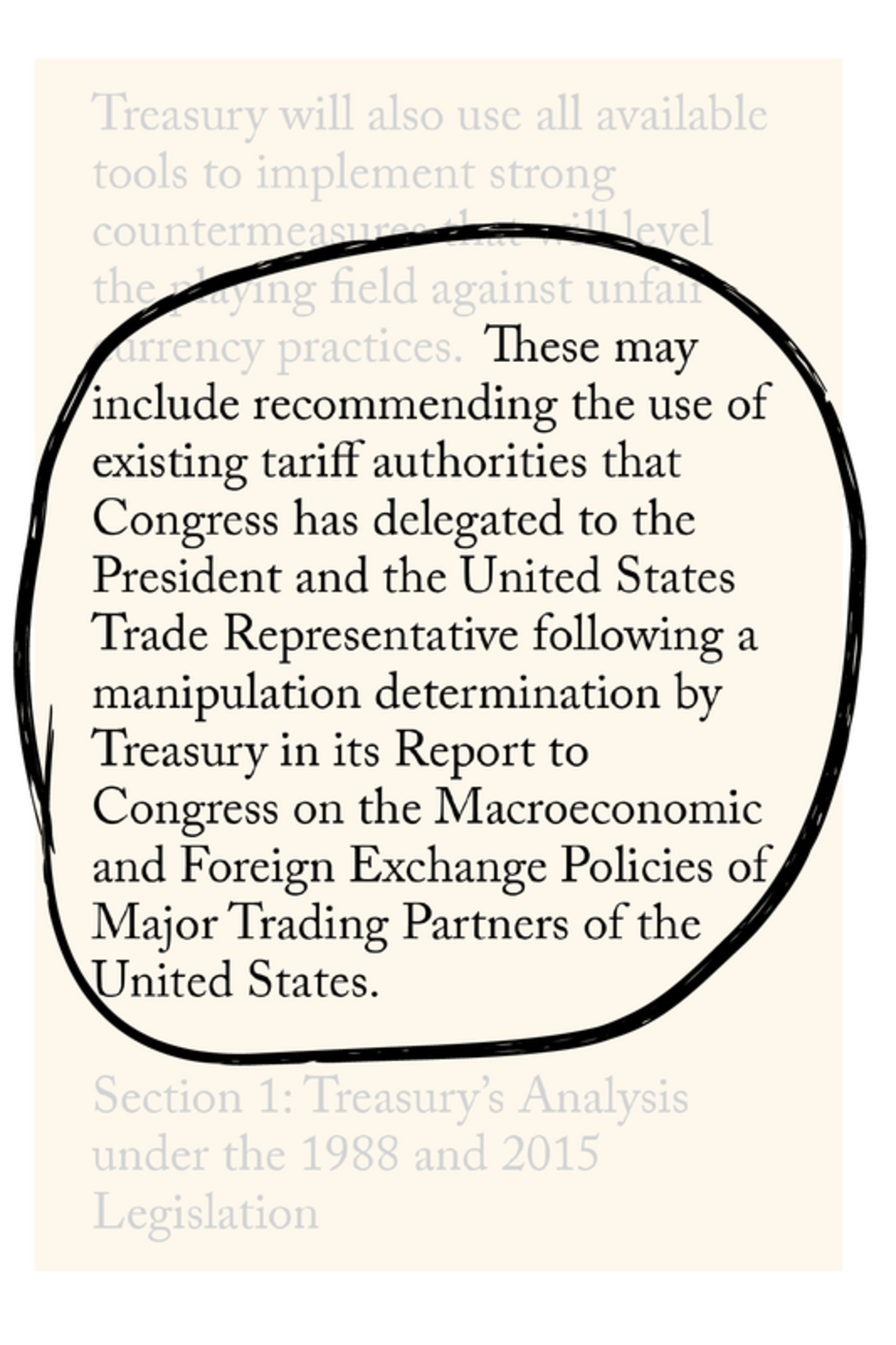

Surprising no one, the Trump administration intends to use tariffs to punish countries judged guilty of currency manipulation. This addresses one of the problems of both the 1988 and 2015 trade laws, namely that they don’t specify meaningful penalties for “manipulation.” The tariff authority that Congress delegated to the U.S. Trade Representative is a reference to section 301 of the Trade Act of 1974, which the Trump administration used against Vietnam for unfair trade practices.

Graphics: Lucky Benson