The Eurozone’s Fiscal Version of the Impossible Trinity?

The eurozone member-states may never be able to run a fiscal policy that is optimal for the eurozone taken as a whole.

The following three propositions all seem to be true:

- The eurozone states that have unquestioned fiscal space generally don’t want to use it, and—at least for now, at the current exchange rate — don’t need to use it to sustain strong growth (Germany now runs a fiscal surplus, as does the Netherlands thanks to an unnecessarily large consolidation in 2016).

- The eurozone states that have domestic slack and would—even now—benefit from a bit of internal stimulus to juice demand and jobs generally lack space under the eurozone’s current fiscal rules to do so. France, Italy, and Spain all need to be bringing their fiscal deficits down to meet the rule requiring medium-term structural fiscal balance (or something close to it).

- The eurozone acting as a whole through common fiscal institutions could in theory be a source of fiscal stimulus for the Eurozone as a whole, as it could borrow against the combined strength of all its members to fund say a bit more public investment commonly. But, well, such common institutions for macro-economic stabilization are, for now, but a glimmer in Macron’s eye. They don’t currently exist, and there is no realistic prospect that a Merkel-led (or non-Merkel led) Germany will ever agree to more than token changes (see the FT’s recent leader on the prospects for fiscal centralization).

The net result has been no fiscal stimulus even when the eurozone’s economy has been demand-constrained, and over-reliance on the ECB and its monetary policy to generate growth.

To be sure, the lack of fiscal support for eurozone growth is no longer as pressing a problem as it once was—the combination of less bad fiscal policy and expansionary monetary policy has generally been working. Demand growth stepped up a notch in 2016, and the latest numbers point to strong growth in q3.

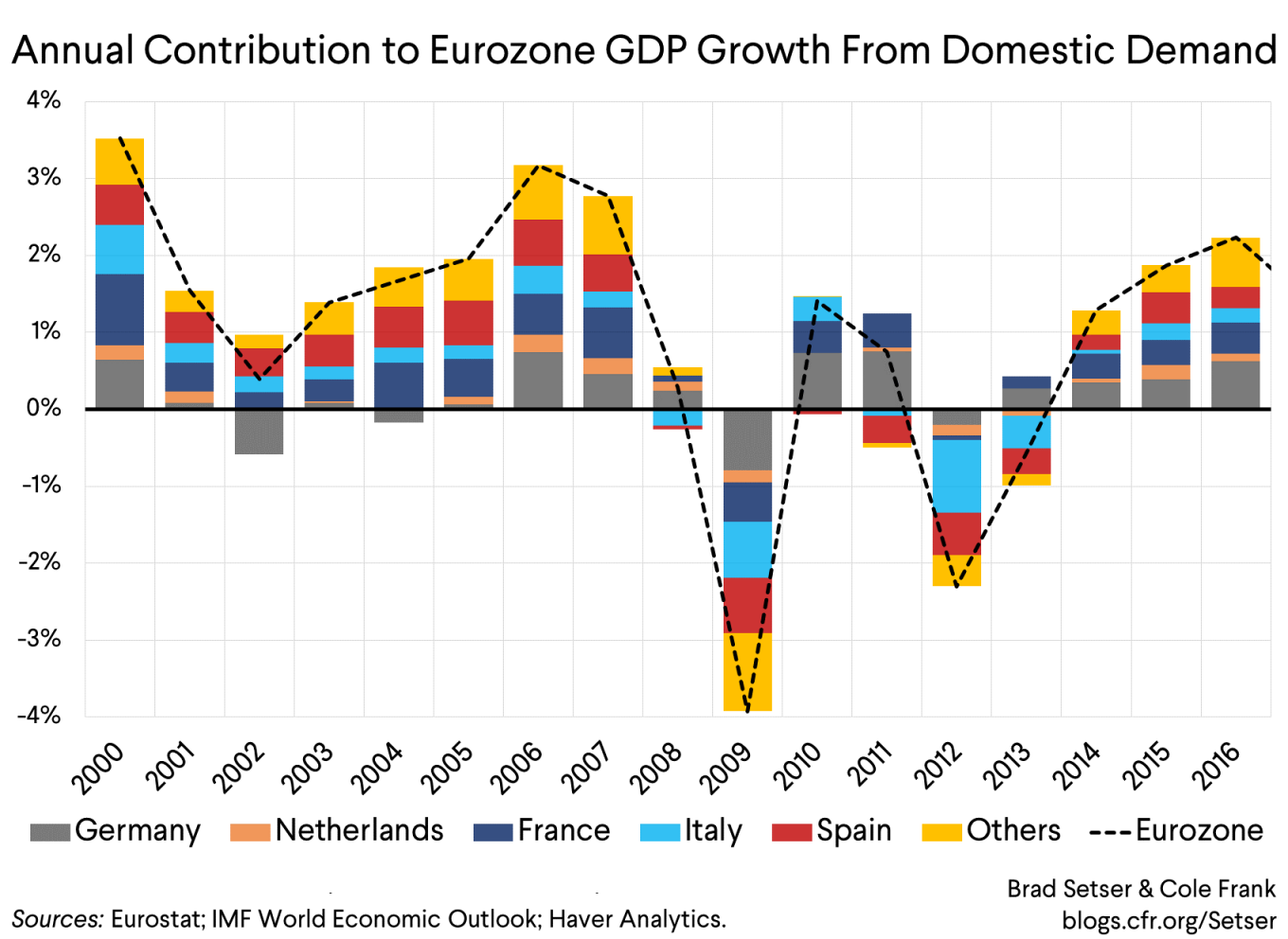

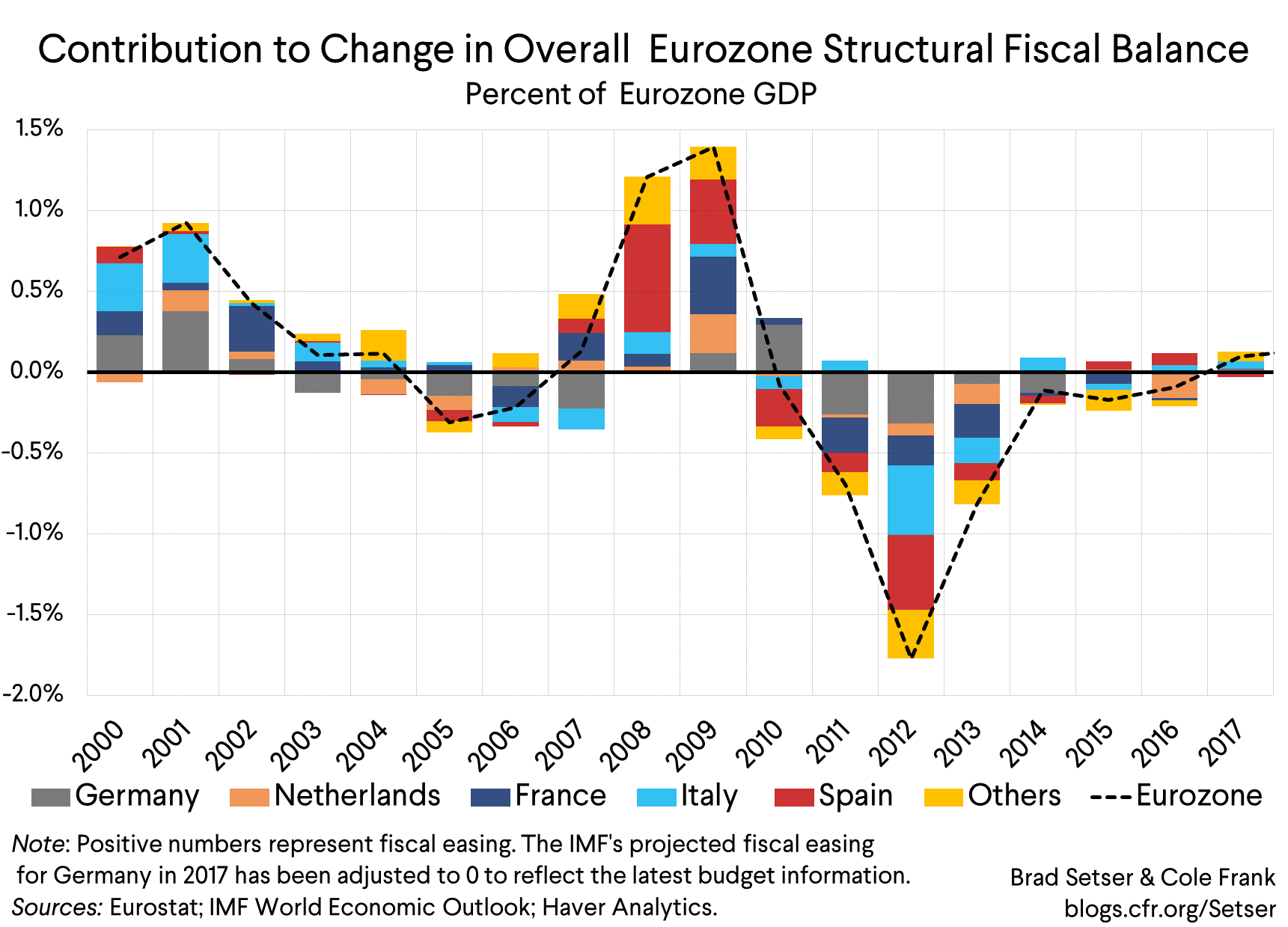

The internal gains from a looser fiscal policy would clearly have been much larger back in 2012 or 2013 or 2014 or 2015 than they are now. Yet if you look back at the eurozone’s aggregate fiscal stance, there continued to be ongoing, though modest, consolidation in 2014 and 2015. That is one reason why eurozone domestic demand only returned to its end-2007 level in 2016.

Given that the eurozone’s growth was being held back by a shortfall in demand and monetary policy was constrained by the difficulties of holding rates much below zero, fiscal policy should have been expansionary for most of this period—whether though the combination of looser national policies that the FT’s Martin Sandbu advocates* or through more central support.

And there more generally is still a case for a looser aggregate fiscal policy in the Eurozone. There is still slack, and a looser fiscal stance in the eurozone would help bring the global economy into better balance.

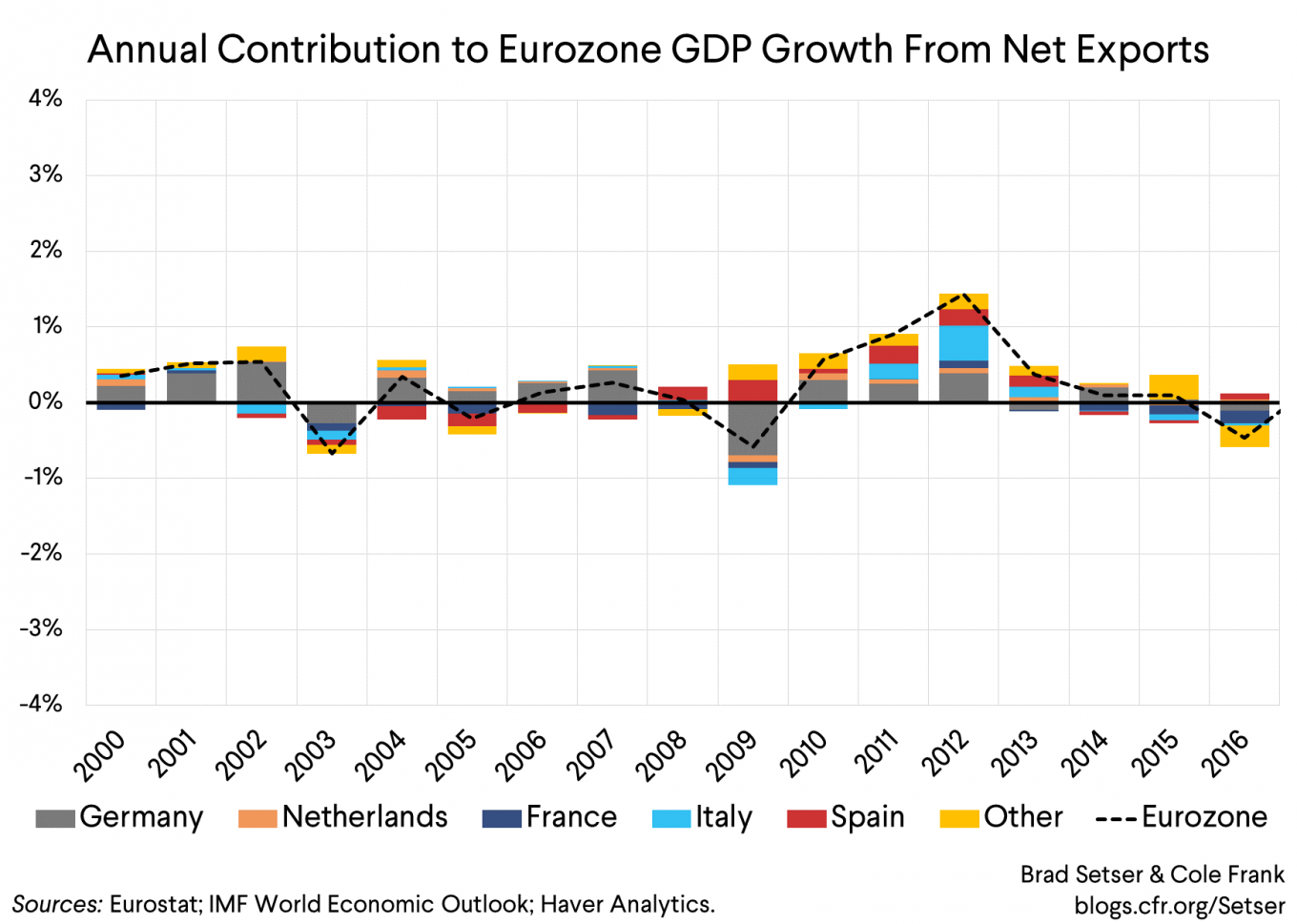

The eurozone’s combined current account surplus was close to 3.5 percent of its GDP in 2016, and after a rise in q3, it looks like the 2017 surplus won’t be significantly smaller. That, in part, reflects the fact that the eurozone’s structural fiscal stance—a deficit of 1 percent of its GDP—is much, much tighter than the fiscal stance of its most important trading partners (the IMF has the structural fiscal balance of Japan, the UK, and the U.S. at around 4 percent of GDP, and well, if you count China’s augmented fiscal balance, its structural deficit would be bigger than that).

The pace of domestic demand growth in the eurozone has accelerated over the last couple of years (including in Germany, see the General Theorist). But demand isn’t yet growing so strongly that net exports are subtracting significantly from growth—e.g. the eurozone isn’t yet consistently giving demand back to the world after drawing so heavily on the rest of the world to dampen its recession in 2011 and 2012. Net exports did subtract from the eurozone’s growth in 2016, but they seem likely to add a bit to 2017 growth. **

Right now though there is no realistic chance that any significant fiscal loosening will happen, even if the Germans might eventually get around to forming a government that cuts tax a bit (though on Germany’s current trajectory, the surplus would rise in the absence of tax cuts, so the cuts may not bring the surplus down much. We will see).

And thanks to the Trump administration’s apparent belief that trade imbalances can be solved through trade policy alone, there isn’t even any real pressure on the eurozone to change its fiscal stance for the benefit of the global economy. I am sure the Germany has taken note of the fact that the U.S. looks poised for a tax cut that would raise the amount the U.S. needs to borrow from the world, and thus the trade deficit. If the eurozone’s fiscal stance is a bit too tight for a monetary union with a quite large external surplus, then it is also true that the United States‘ fiscal stance is a bit too loose for a country with a large external deficit.

* Sandbu has been arguing for a renationalization of fiscal policy to provide individual eurozone member-states more scope for counter-cyclical policies. Given the difficulties of creating a common eurozone budget big enough to make a macroeconomic difference, I have sympathy for his view. For the foreseeable future, the eurozone’s fiscal stance will be the sum of the national fiscal stances of its key members. But I do worry that if renationalization of fiscal policy is paired with new measures to strengthen market discipline (as the Germans are demanding), fear of an adverse market reaction will continue to constrain the fiscal policies of key states in the next downturn. Germany and the Netherlands don’t need to worry, but they also haven’t shown much historical willingness to use their fiscal strength to support demand in a downturn. And while the risks identified by de Grauwe back in 2011 are currently quiescent, I fear they could return.

** So far in 2017 net exports mechanically have added slightly to growth, thanks to a strong q1. I suspect the strong q3 current account surplus augers a positive contribution in q3 as well.