By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Benjamin Della RoccaAnalyst, Center for Geoeconomic Studies

“In the age of Trump,” warned a Bloomberg op-ed last year, “America’s biggest foreign creditors are suddenly having second thoughts about financing the U.S. government.” Today, with Trump piling up trade barriers and debt, speculation continues that U.S. policies are scaring foreign investors away from Treasury bonds. More extreme commentators even suggest that Trump has created default risk.

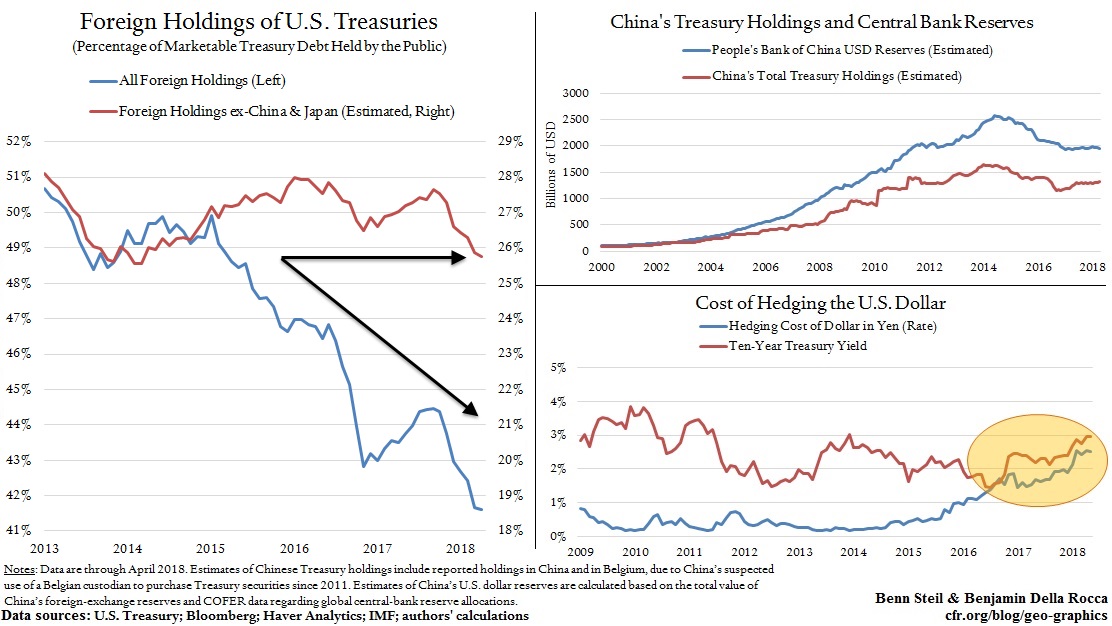

To be sure, foreign demand for Treasury debt has stalled: since 2013, foreign ownership has fallen from 50 to 43 percent of publicly-held marketable Treasury securities. But is U.S. government action behind this decline?

A dive into the data shows not. The figures indicate, first, that the decline in Treasury holdings abroad has not been broad-based. Two countries explain the entirety of it. As the left-hand figure above shows, the collective ownership of Treasury debt by all countries save China and Japan has been steady since 2013.

To the extent that U.S. fiscal policy has spooked bond investors, then, it is, curiously, only Chinese and Japanese ones. But the figures also show that China and Japan each have discernable reasons for halting Treasury purchases that have nothing to do with U.S. behavior.

In China, nearly all U.S. Treasury ownership is accounted for by investment of central bank reserves. And as shown in the top right figure, the People’s Bank of China stopped buying Treasuries once it stopped accumulating dollar reserves, in 2014. In the past, China routinely bought dollars (and therefore Treasuries) to keep its currency down, but in recent years it has been more concerned with halting capital flight and keeping its currency up. Movements in China’s Treasury holdings, then, reflect China’s shifting exchange-rate policy, and not shifts in sentiment about U.S. policy.

Japan’s Treasury holdings, meanwhile, have dropped about $150 billion since 2015. But two factors account for this fall. First, Japanese investors have replaced more than half this sum with long-term U.S. Agency debt (most prominently, Fannie Mae and Freddie Mac securities). Japan’s exposure to U.S. government debt has, therefore, changed much less than movements in its Treasury holdings suggest. Second, the rising cost of holding U.S. assets has tempered Japan’s Treasury demand. When investing abroad, most Japanese institutions hedge against the foreign-exchange risk with currency futures contracts, which require them to pay foreign-currency borrowing costs. U.S. Federal Reserve rate hikes have made borrowing dollars more expensive. In fact, dollar-hedging costs have risen so much in Japan that, as our bottom right chart shows, they nearly equal the yield on ten-year Treasury bonds.

In short, while there may well be good reasons to worry about the trajectory of U.S. budget deficits, they are not yet reflected in foreign willingness to hold Treasuries. There has been no Trump dump.