Ireland’s Statistical Cry for Help…

Ireland’s tax authorities have made the job of Ireland’s statistical authorities almost impossible. The distortions in the Irish data are now so big that the impact the data for the entire euro area.

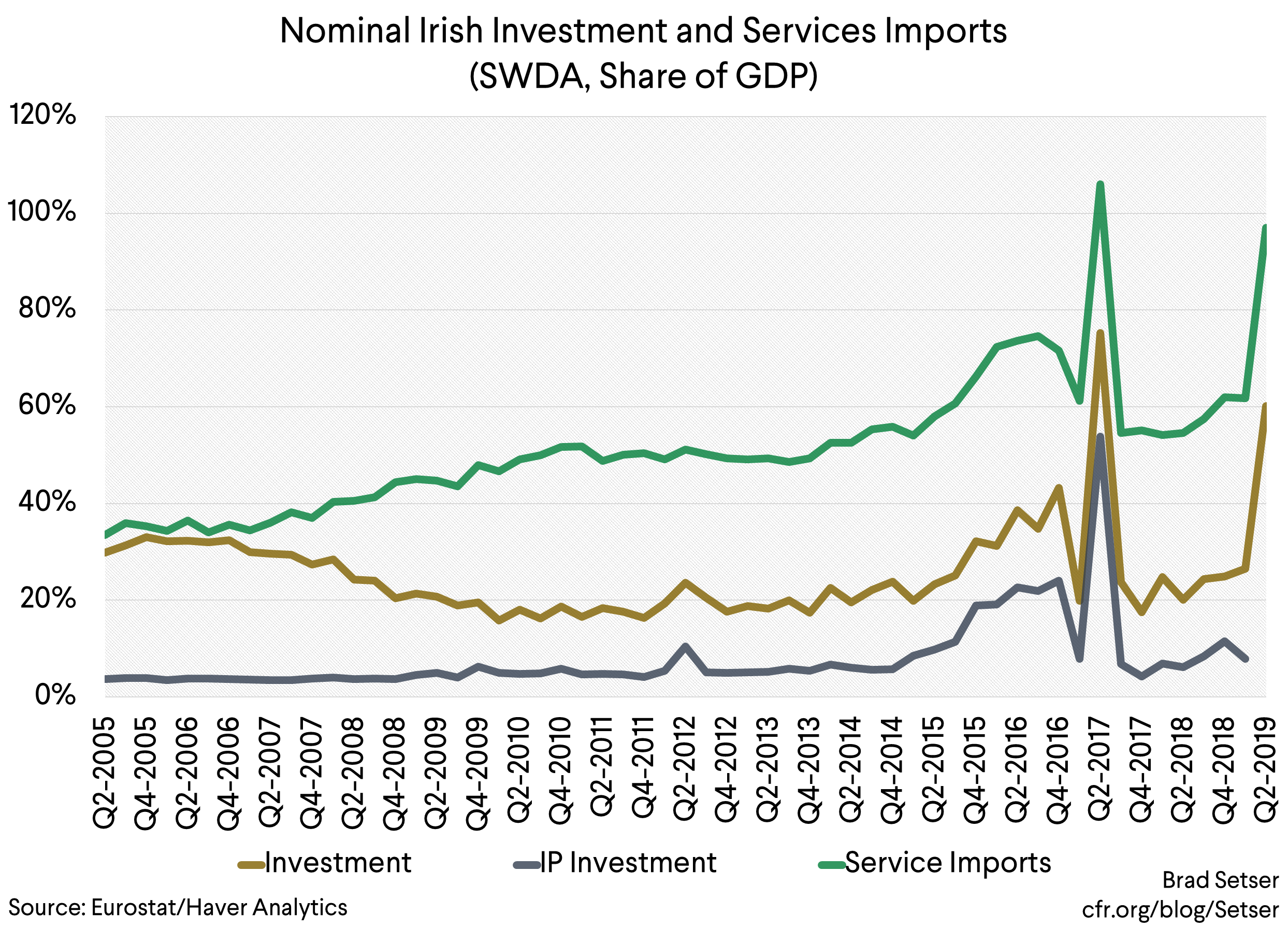

Ireland’s second quarter GDP data is so extreme—so strange—that it almost reads like a plea for a new system of national accounts from the Irish statistical authorities.

Investment went from 27 to 60 percent of Ireland’s GDP in a single quarter.

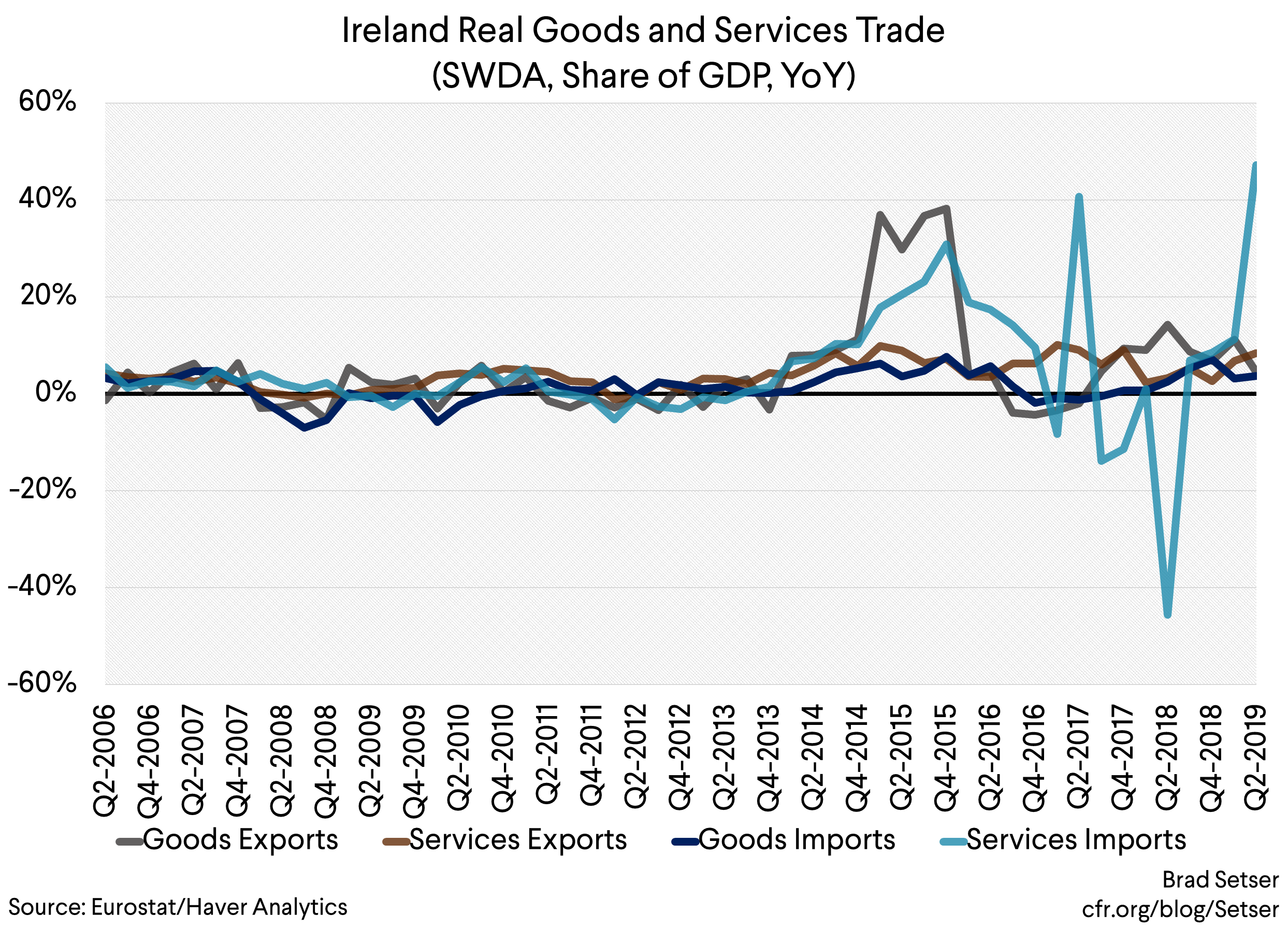

Service imports (no doubt imports of intellectual property) rose from 62 percent of GDP to 97 percent of GDP.

The formal breakdown of investment isn’t out, but the surge in investment is almost certainly the result of a surge in investment in “intellectual property”.

There was a similar surge back in the second quarter of 2017.

It is likely that a large company—Microsoft is an obvious candidate, as the Irish Times reported it shifted around $50 billion in assets from Singapore to Ireland—or a set of large companies decided to consolidate their tax operations in Ireland in the second quarter. That, in practice, likely meant their Irish subsidiary bought the intellectual property of another of their offshore subsidiaries.

One side effect of the global push to end stateless income—with Irish but not Irish for tax purposes companies being one prominent source of stateless income—is that a lot of footloose “phantom” FDI needs a tax home. That includes the Irish (legally) but not-Irish (for tax purposes) leg of a standard double Irish tax structure. And it seems that this stateless income—or almost stateless income (Microsoft’s Singapore subsidiary used to channel its Asian income back to a zero tax jurisdiction in the Caribbean)—decided to move, legally at least, to Ireland.

Ireland isn’t exactly an innocent bystander in this whole process—the capital allowance for intangible assets (CAIA) or “Green Jersey” tax structure was designed to encourage firms with a lot of intangible assets to settle in Ireland.

The tax dodge here is straightforward—a firm can deduct the cost of a large investment in intangibles (say the purchase of a subsidiary’s IP rights) from its Irish tax bill, and it also can deduct the funds it notionally borrows (typically from a subsidiary) to pay for the purchase. Apple pioneered this structure when Apple Ireland borrowed funds from Apple Jersey to, more or less, buy the IP rights that had been assigned to Apple Jersey (hat tip to the reporters who worked through the Paradise Papers). The new Apple Ireland that emerged is a tax resident of Ireland, but has a very low (and totally BEPS compliant) Irish tax rate (Apple now also owes the US GILTI tax on its Irish profits).* And now other companies are likely following suit.

But all this has one big unintended side effect—tax residents of Ireland enter into Ireland’s gross domestic product. As a result Ireland’s economic data at some point ceased to tell us much about Ireland, and instead started to tell us more about the global operations of big (typically American) firms. Stefan Avdjiev, Mary Everett, Philip Lane and Hyun Song Shin more or less have said as much. The Irish tax authorities have basically made the job of the Irish statistical authorities next to impossible.

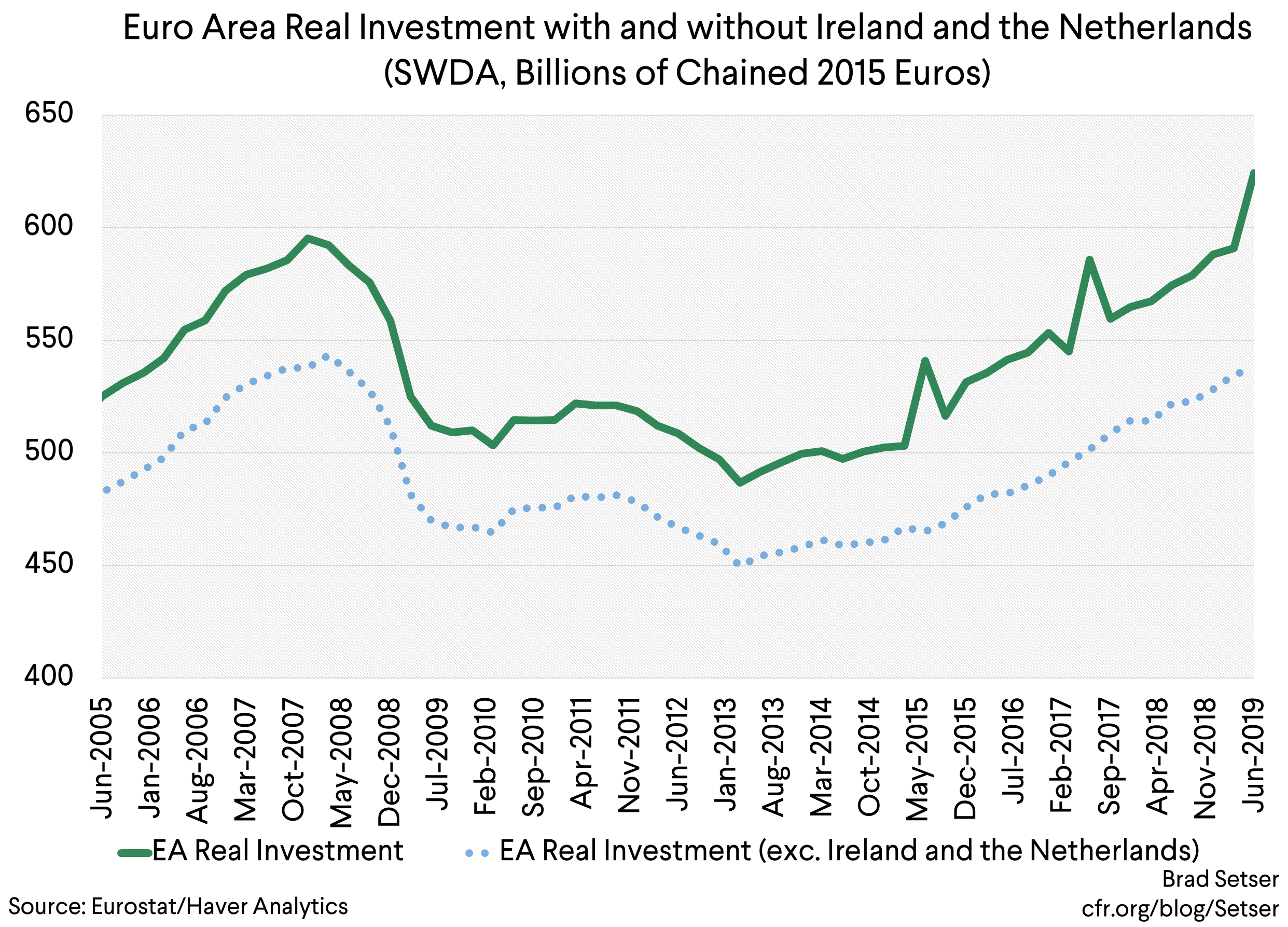

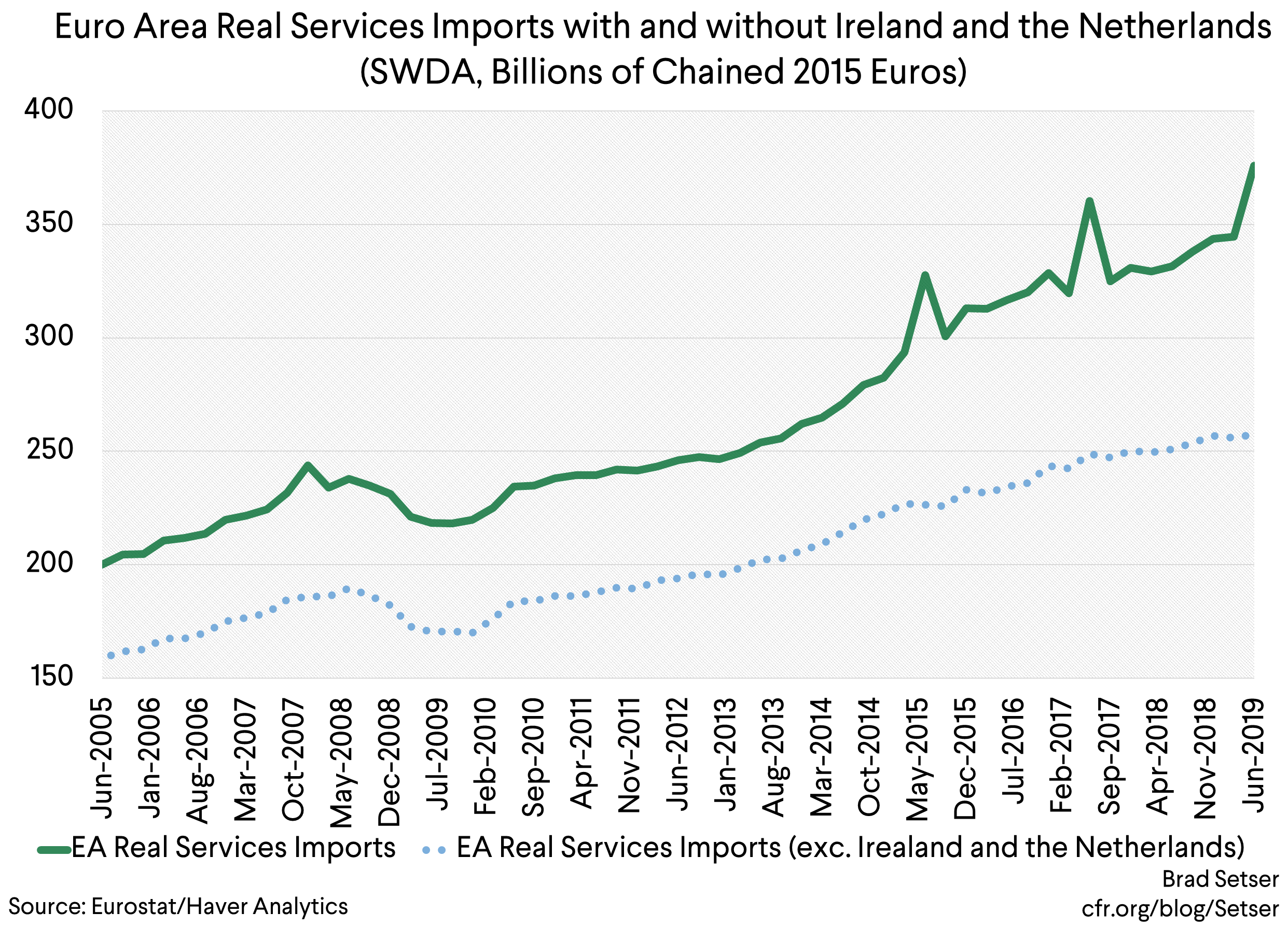

The problem is that Ireland’s data also enters into the broader European aggregates, and “Ireland” the tax entity (the leprechaun providing tax gold to multinational firms, for now) is big enough that it is starting to impact the broader European data. I have heard that some in Europe are looking at measures of the EU-27—and that’s before Britain formally has left the EU.

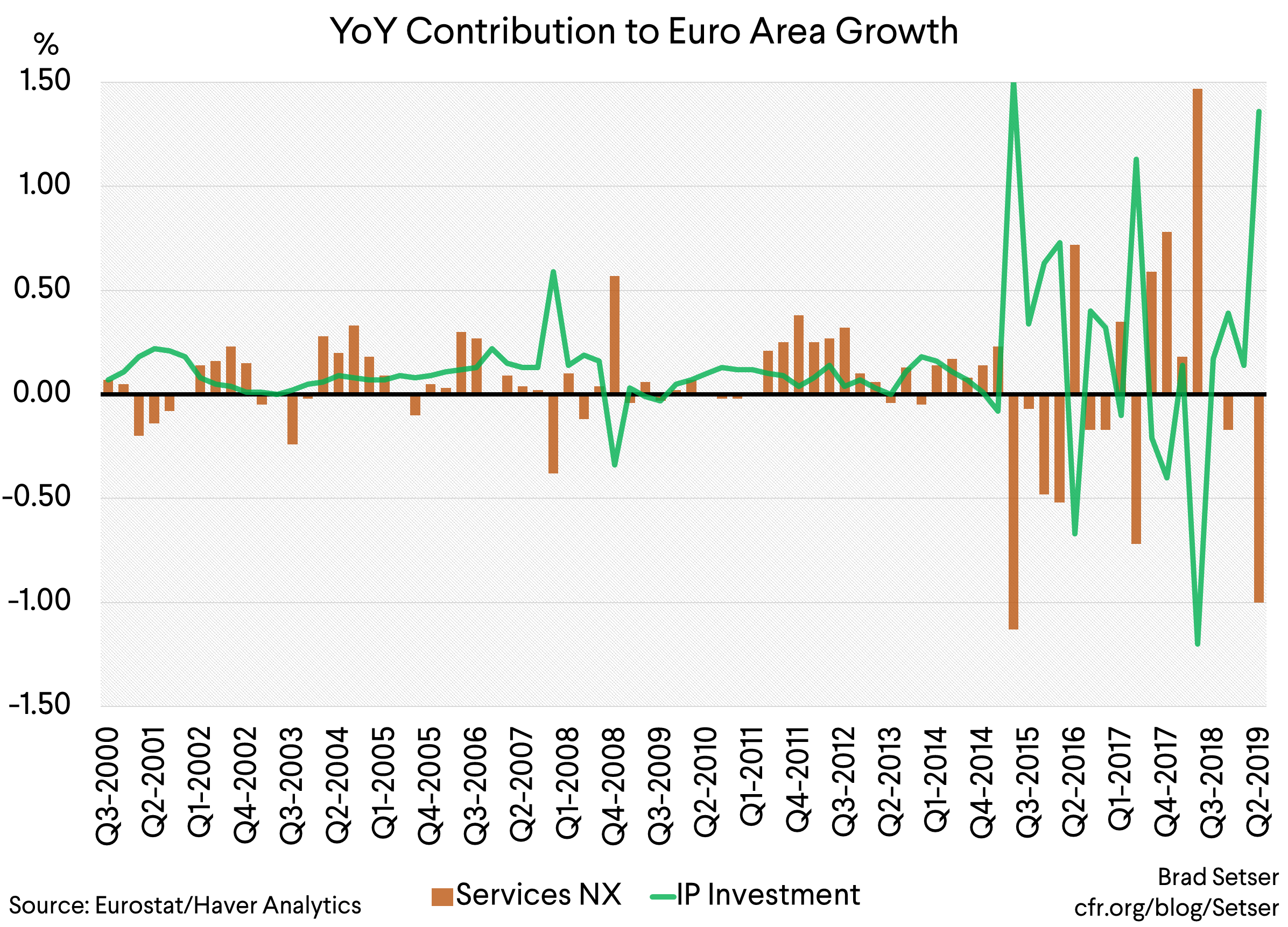

Investment jumped in q2? Ireland.

European services imports surged, so net exports turned negative? Ireland…

The subtraction of services imports from Irish GDP over the last four quarters of data technically is about 39 percent of Irish GDP (real GDP). Normally that kind of crazy number would be a sign that the data was off—or that I made an error in the calculation. But there is no error—the number is a measure of the scale of the distortions tied in all probability to expanded use of the “capital allowance for intangible assets” and the associated swings in “Ireland’s” investment in IP and IP imports.

These kinds of tax gymnastics are the main reasons why Europe as a whole sometimes runs a current account deficit with the United States, something the Germans of all people have increasingly picked up on. Yet the bilateral current account is only in rough balance because Ireland (with the help of some other European tax havens) generates a massive surplus in FDI income for the United States.

Even after the U.S. tax reform, American firms generally still prefer to book their global profits as Irish profits than as U.S. profits.**

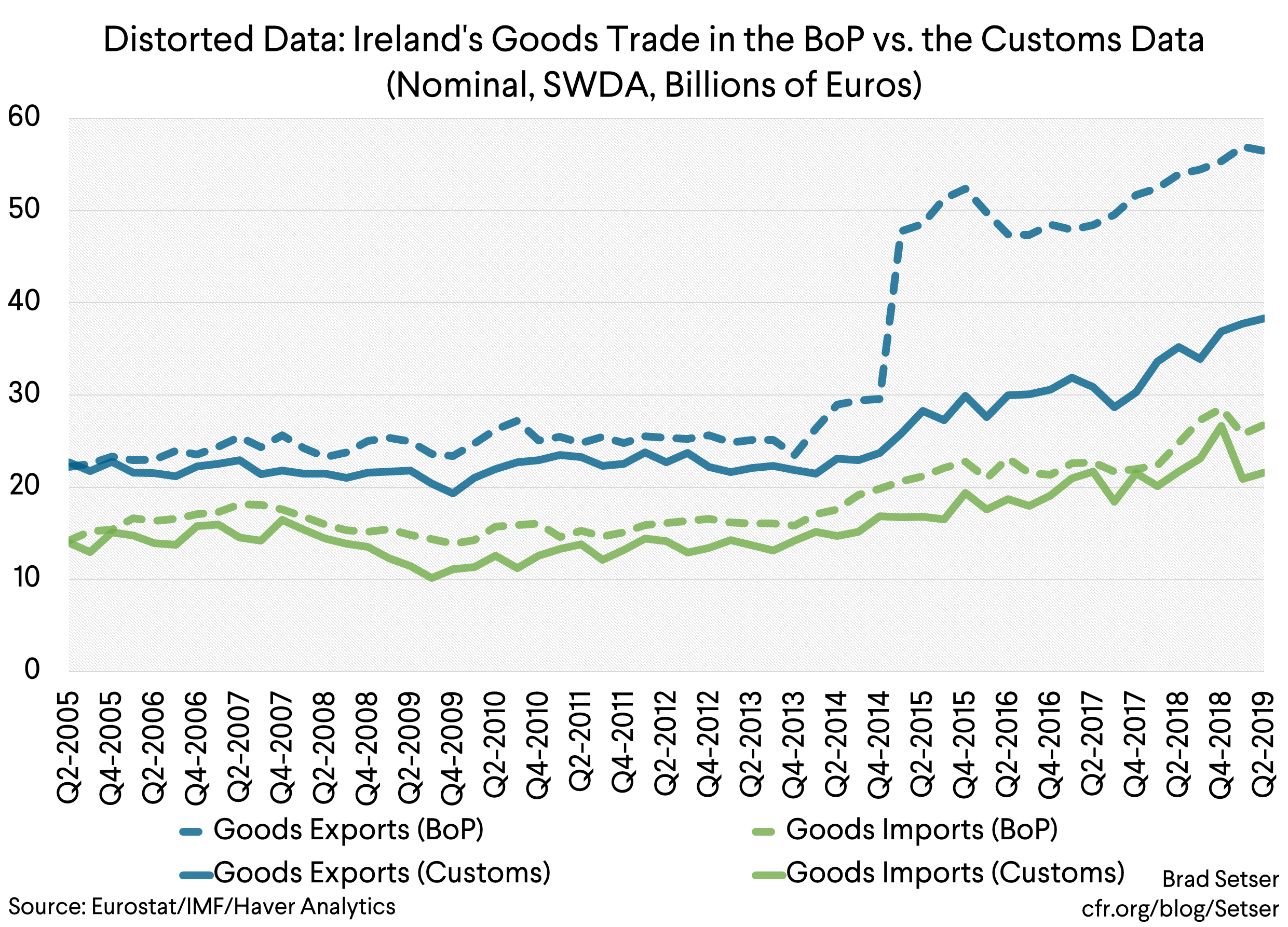

There is another way to see these distortions—after Apple Ireland became a tax resident of Ireland, Ireland ‘s balance of payments data and its customs data started to diverge. The balance of payments data is effectively for “Ireland” the tax entity, and the customs data better reflects real Irish exports. Apple Ireland technically imports cellphones to Ireland for re-export (after being marked up to reflect the value of Apple’s brand and its software) and thus it enters into the balance of payments even though no phones (or almost no phones) physically clear customs in Ireland. Or something like that.

But don’t take even the “real” data at face value. Remember that a lot of Ireland’s real activity—pharmaceutical manufacturing for example—itself is driven by tax. Ireland’s customs exports jumped right after the U.S. tax reform, as did U.S. imports. I at least don’t think that is entirely a coincidence.

The Irish leprechaun (to use Dr. Krugman’s phrase) keeps getting bigger.

And so does the evidence that the world needs fundamental reform to the current system of corporate taxation—though to be honest, the United States could do a lot to improve Irish economic statistics on its own, by changing U.S. tax law in ways that eliminated the incentive to shift paper profits and in some cases real jobs to Ireland and similar low tax jurisdictions.

* I agree with Dr. Stiglitz that the BEPS reforms have not gone far enough.

** Apple Ireland and now Microsoft Ireland (and Google’s Irish-Dutch-Caribbean chain of subsidiaries) collect the global profits of U.S. firms, which register as income in low tax jurisdictions inside the European Union—offsetting the goods surplus that the EU runs with the U.S. Germans looking to explain away Germany’s large external surplus are found of this stat—but it doesn’t really say what they think it says. Adjusting Germany’s surplus with the U.S. to reflect German imports that are booked as Dutch imports because of the “Rotterdam” port effect on the other hand makes sense.