When Is the Next X Date?

By experts and staff

- Published

By

- Robert KahnSteven A. Tananbaum Senior Fellow for International Economics

In my post yesterday, I mentioned in passing the uncertainty about when we would again hit the debt limit (“X Date”). The question is complicated. Yesterday’s agreement extends the debt limit until February 7, and it allows the U.S. government to replenish or repay the extraordinary measures that it took in order to finance the deficit from May until yesterday.

Alec Phillips at Goldman Sachs suggests that the extraordinary measures this time might only get us to sometime in March, but it’s also possible to project a new X Date of May, June or July.

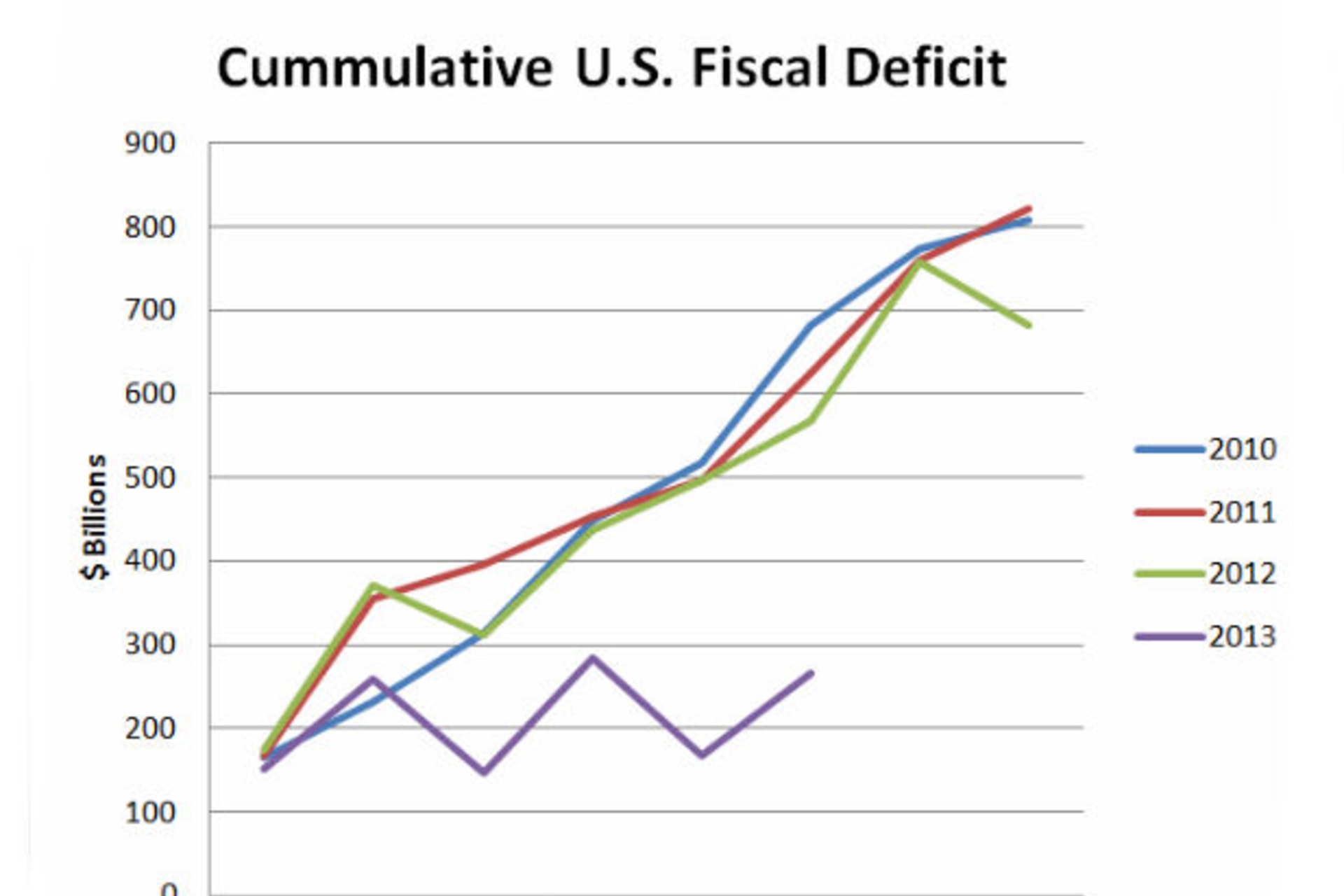

The chart above shows the cumulative deficit of the U.S. government starting February for the last four years. (I took three-fourths of the reported monthly February deficit to approximate a February 7 start date.) It shows that 2013 looks a lot different from previous years, which reflects a falling deficit and also some of the effects of the fiscal cliff at end 2012. But if we assume that 2014 looks broadly like 2013, only with a smaller deficit, then you can see a story where the X Date is pushed off to April 15, and then until summer.

When the debt limit hits could be important for both political and economic reasons, coming in the midst of primary campaigns for the 2014 midterm elections. Proximity to the X Date also would make it hard for the Fed to make decisions on tapering asset purchases, which some believe could be on the table at their March 19-20 monetary policy meeting. Perhaps the debt limit will be addressed in the December spending negotiations. I hope so. But if those negotiations fail, as have past efforts at grand bargains, then we may be facing another debt limit showdown in 2014. My intuition is that, to the extent Treasury is able to push back the X Date, it should do so. Using the debt limit as leverage for a political or economic agenda is dreadful at any time, but seems less likely to result in a cliff hanger the later in 2014 it is addressed.