China’s New and “Improved?” BOP Data

China promised a better balance of payments report. What it delivered instead is a set of implausible numbers that deserve a closer look from the IMF.

China released its “improved” balance of payments data for the first time at the end of the first quarter.

It isn’t much of an improvement. If I was an external referee, I would argue that the IMF should ask China to revise and resubmit.

In theory, China was going to provide a bit more of a breakdown of its investment income returns. And it did provide a line item for its Q1 FDI returns ($30 billion, a 3.3 percent implied return), as well as its non-FDI returns ($36.5 billion, which works out to a return of under 2 percent on China’s non FDI assets; SAFE managed 3 percent in the low for long era from 2011 to 2020).

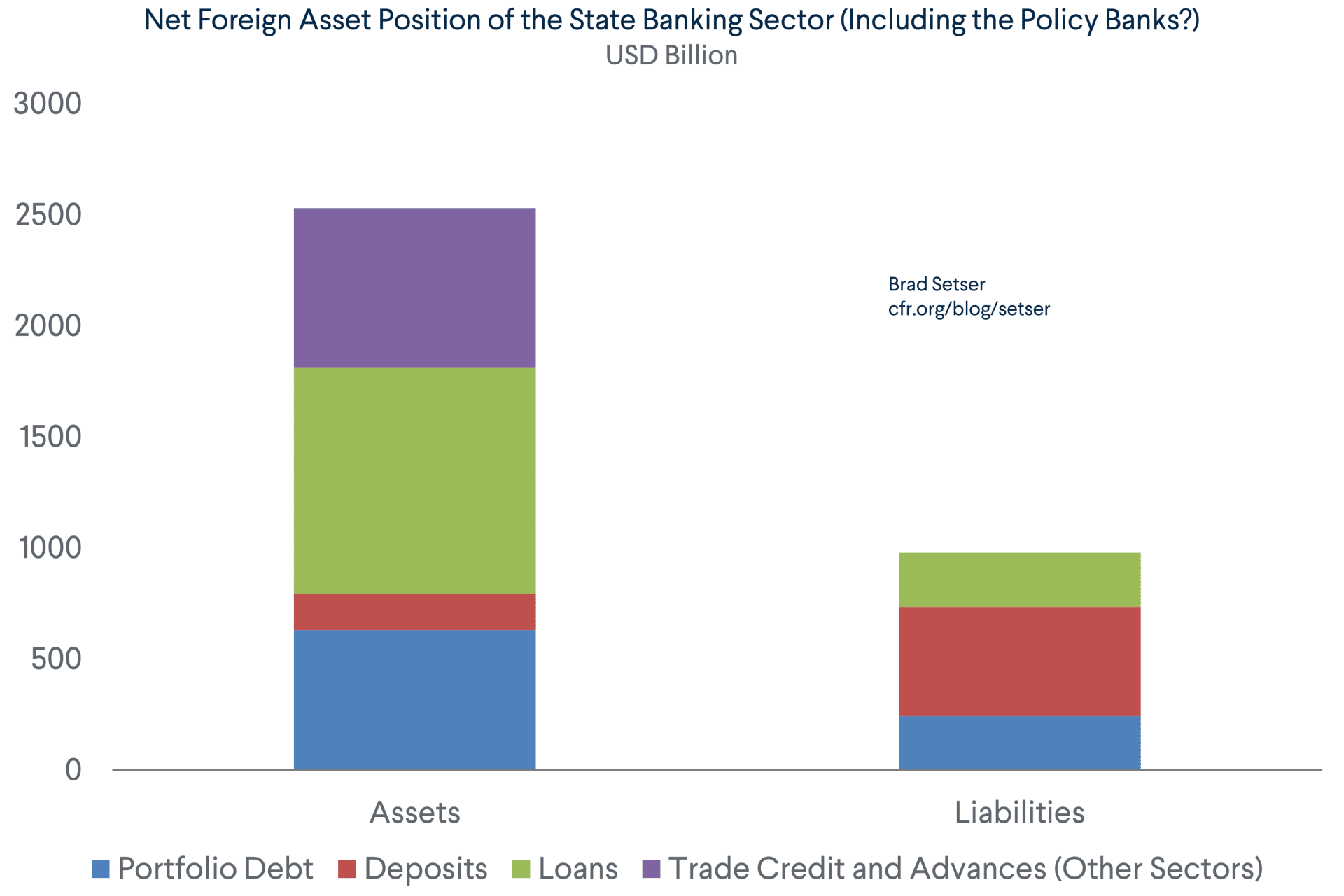

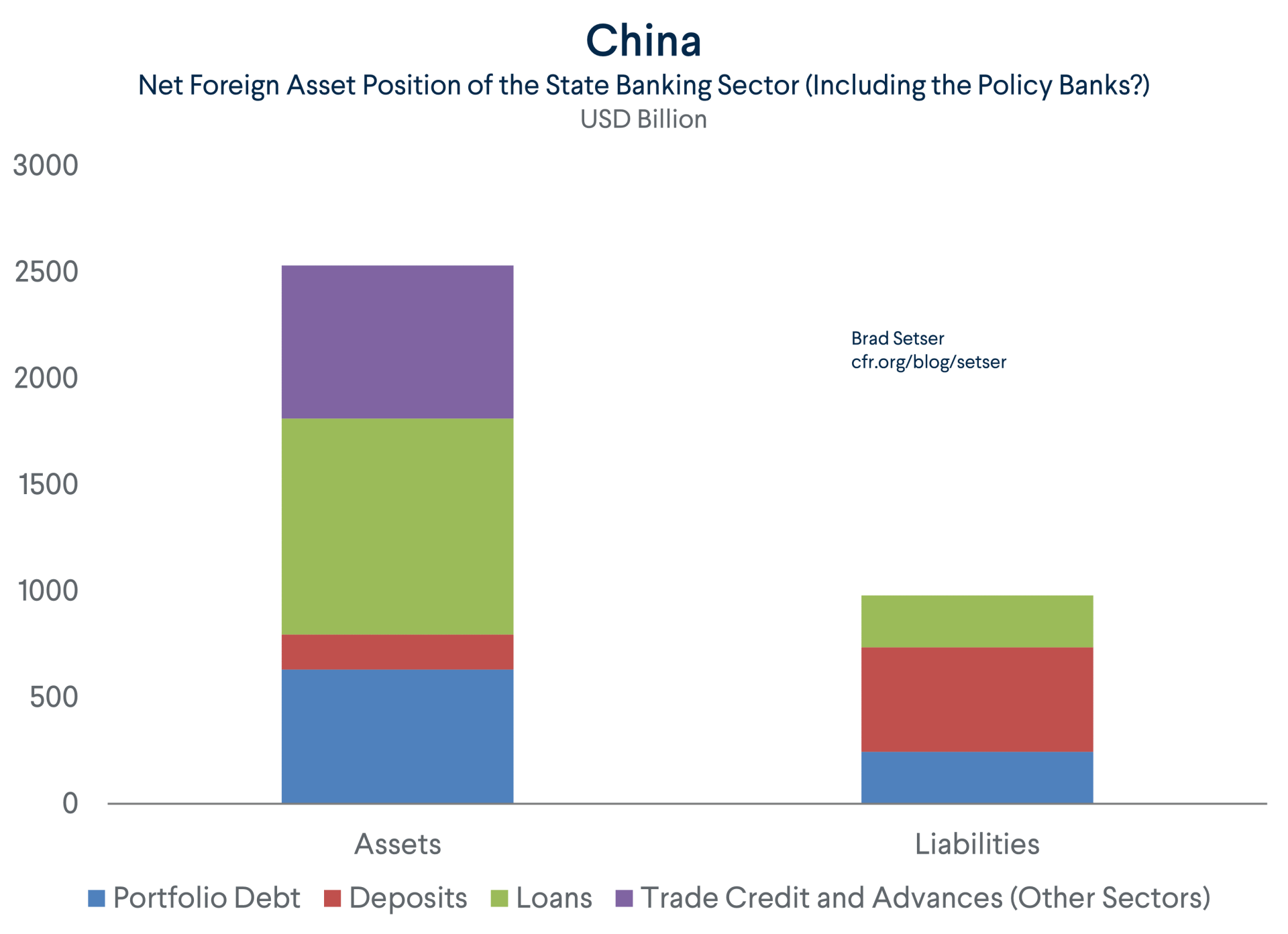

The new and improved data was also supposed to break out its portfolio investment and banking data (“Other”) by sector.

That breakdown is comically bad.

“Portfolio equity, government” is usually where the foreign equity investments of sovereign funds are reported. It is here where, for example, Singapore’s Government Investment Corporation enters the data. And where Korea’s massive National Pension Service enters the data. And where Norges Bank Investment Management enters the data.

Yet China reported a zero.

That is obviously false. The CIC reported $451 billion in “foreign “Financial assets at fair value through profit or loss” at the end of 2024—it obviously has an equity book. And most people think China’s $400 billion plus National Social Security Fund (the analogue to Korea’s National Pension Service) has a modest foreign portfolio. Zero is clearly not the right number.

Consider loans under “Other investment.”

$1.015 trillion of the total $1.030 trillion in loans were from “deposit-taking corporations.”

That makes sense, you might think, as banks take in deposits and make loans.

Except two of China’s biggest lenders—the China Development Bank (CDB) and Export-Import Bank of China (China Exim)—aren’t “deposit-taking corporations.” The policy banks raise funds by selling bonds to the market -- and of course that includes selling bonds to the “deposit-taking corporations.”

The total here also doesn’t line up with other data sources.

For example, the foreign currency sources and uses table for the state commercial banks that the PBOC publishes monthly reports $409 billion in foreign currency loans.

That leaves up to $600 billion for RMB-denominated loans, or potentially for the CDB and Exim if China bundled their external lending with the state banks (presumably the policy banks should be a line item under “other financial institutions” but that is clearly not what China did for “loans”).

Now look at “Trade credit and advances”:

China reports $720 billion in total credit credit assets. Zero though come from the banks (hmmm) and all are in “Other sectors”—that has to be Exim (most of it is short-term as well, $706 billion of the whole $720 billion).

The thing here is that everyone who has worked on frontier market restructurings or looked at China’s external lending—say, to Zambia, Sri Lanka, or Ecuador—knows that Exim and the CDB provided a lot of credit to these countries. To Angola and Venezuela too.

So, it isn’t really plausible that all the long-term loans are from deposit-taking corporations (not the policy banks) and all the trade credit is short-term and from “other financial institutions” (though China didn’t do any breakdown of “Other” in its reporting…)

In fact, China’s disclosure here is so obviously incomplete that the IMF should send it back and ask China to resubmit with some real numbers.

The IMF statistics department likes to say that it doesn’t judge the quality of its members’ data. That has been its excuse for not challenging the results of China’s “survey-based” methodology for calculating the transfer of value tied to “exports” in the current account.*

In this case, China clearly didn’t make much of an effort to produce real numbers. Bad reporting is almost worse than incomplete reporting.

The available disclosure did let me estimate the net foreign asset position of the deposit-taking institutions and the policy banks in the NIIP—it is roughly $1.5 trillion. But it would be nice to be able to break this out by the obvious regulatory categories that China uses—namely the commercial banks and the policy banks. That was the point of the exercise, not getting obviously incomplete entries for the key line items.**

* The official position of the Bureau of Statistics is that China is correctly implementing its latest guidance note, unlike the U.S.—never mind the quarterly inconsistencies that have developed with the new methodology, and never mind that China cannot credibly explain the source of the gaps created between the current reported numbers and what the numbers would be under the old customs-based methodology.

** A number of emerging economies do produce good, detailed balance of payments data—Korea, Brazil, and Turkey all come to mind. These countries all have very complete data, and all actually report monthly. China, with a very controlled financial account, should have a much easier time generating high quality data. The low quality of its latest disclosure will only add to the questions many have about the accuracy of China’s external reporting.