Mortgages and Monetary Policy Don’t Mix

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Dinah WalkerAnalyst, Geoeconomics

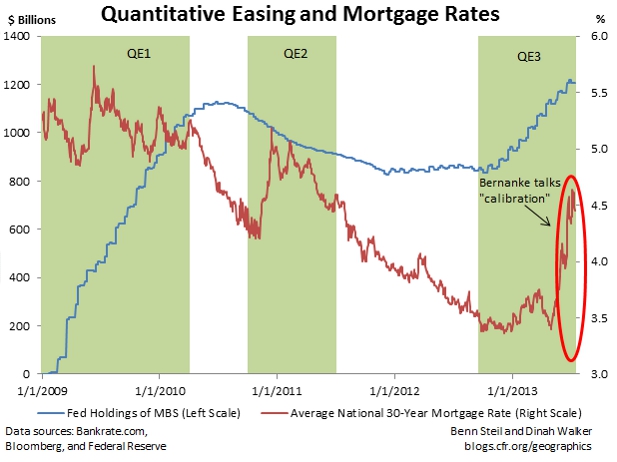

From the beginning of 2009 through this past May 21st, the Fed amassed a portfolio of mortgage-backed securities (MBS) valued at $1.2 trillion. Over this period, the average 30-year fixed mortgage rate fell from 5.33% to 3.65%, and the spread between that rate and the 10-year government borrowing rate fell from 2.8 percentage points to 1.7 percentage points.

Then came talk of “calibration” and “tapering” . . .

“Calibrating” asset purchases to volatile data while pledging to ignore data on rates, as we argued recently in Dow Jones’ Financial News, is a tough line for the Fed to walk. On May 22, and then again on June 19, Chairman Ben Bernanke suggested that the Fed might soon begin reducing the pace of MBS purchases, dependent on developments in the labor market. Mortgage rates soared. The average 30-year rate is now hovering around 4.5%; about half the decline in mortgage rates that the Fed had engineered through its multi-year MBS purchase scheme has evaporated. In consequence, the monthly mortgage payment on a $200,000 home purchased with a 10% down payment has risen by a whopping 10% since calibration talk began. Housing starts also plummeted 10% from May to June, hitting their lowest level since last August, just before the Fed’s latest round of MBS purchases.

This confirms our view, expressed recently in the Wall Street Journal, that the Fed should never have gotten involved in sectoral credit allocation in the first place: it should have limited its interventions to the Treasury market, and let the Treasury take politically charged decisions on whether and how to intervene in specific areas of the economy, such as the mortgage and housing markets. The Fed has only set itself up, as well as the market, for ongoing exit strategy headaches. Mortgages and monetary policy just don’t mix.