Time to Stop Forecasting China’s Surplus Away

China could run a 10 percent of GDP external surplus if its savings rate stays over 40 percent of GDP.

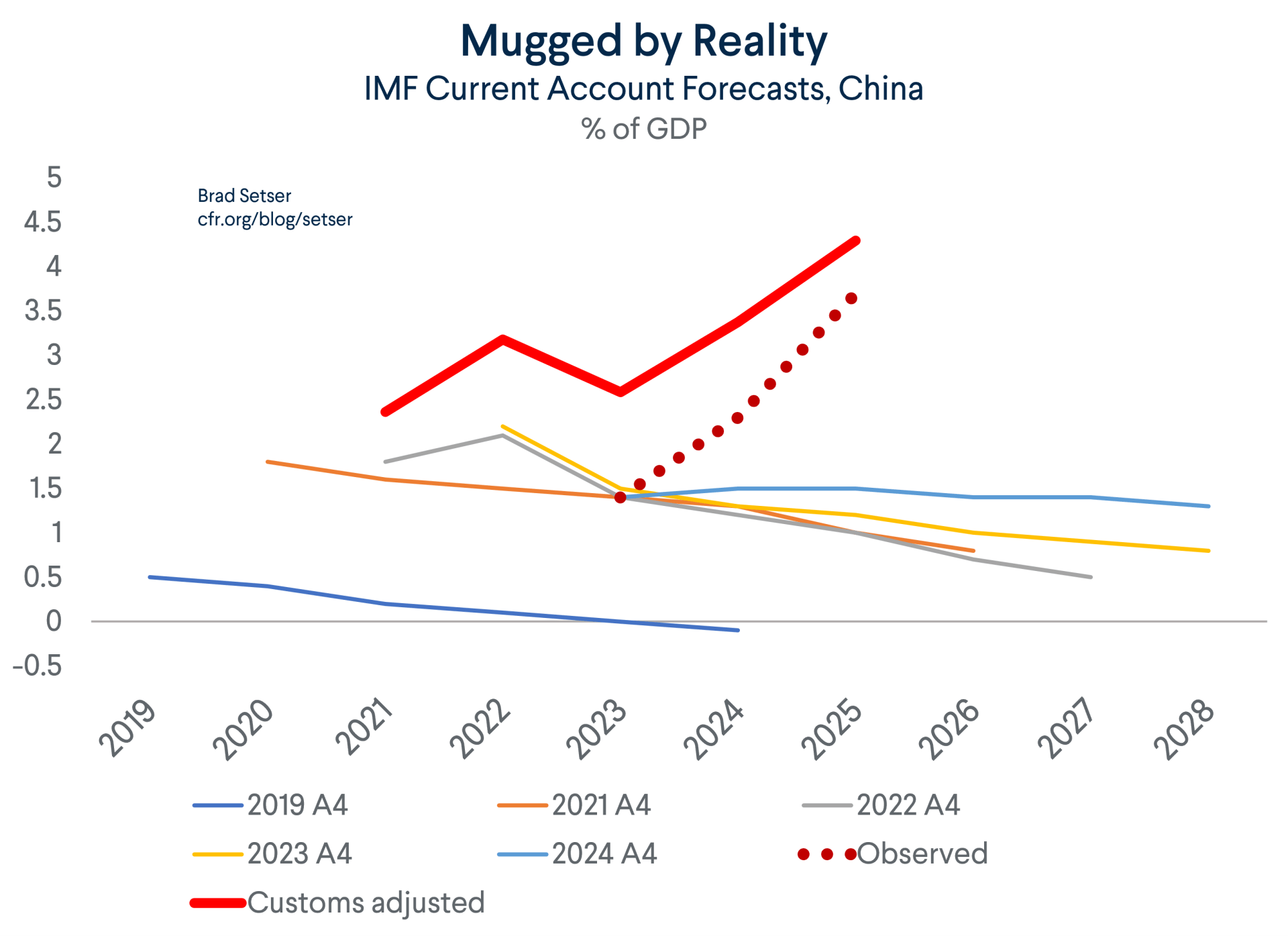

The IMF, rather consistently, has forecast that China’s surplus will fall over time.

And, until very recently, the IMF more or less forecast that it would fall back to around 1 percent of China’s GDP.

That was the IMF’s forecast in 2020, 2021, 2022, 2023, and 2024.

The 2026 forecast in the latest World Economic Outlook is a bit better, but the surplus still trends back down to 2.5 percent of China’s GDP over time even in the absence of any projected large policy changes.

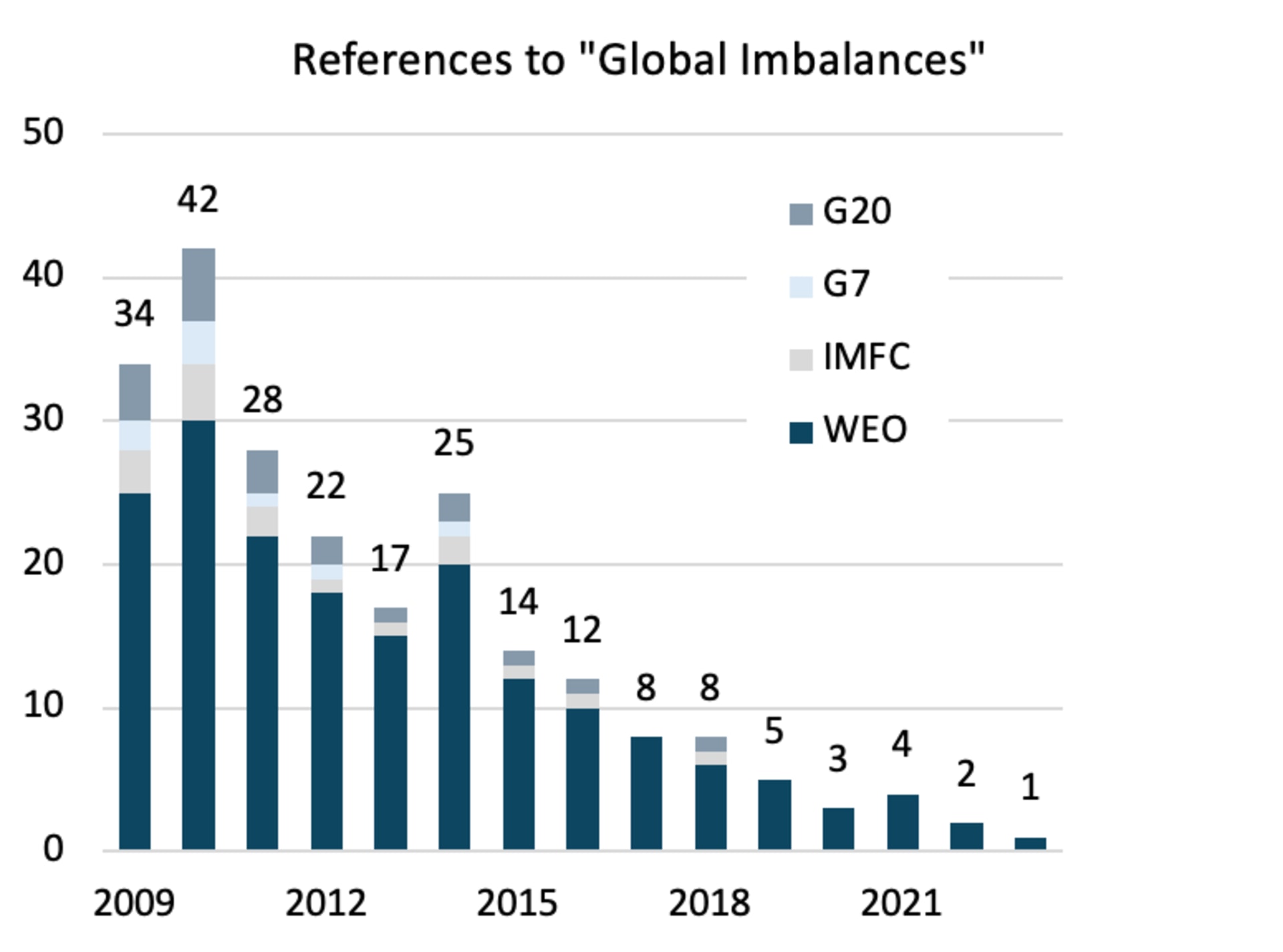

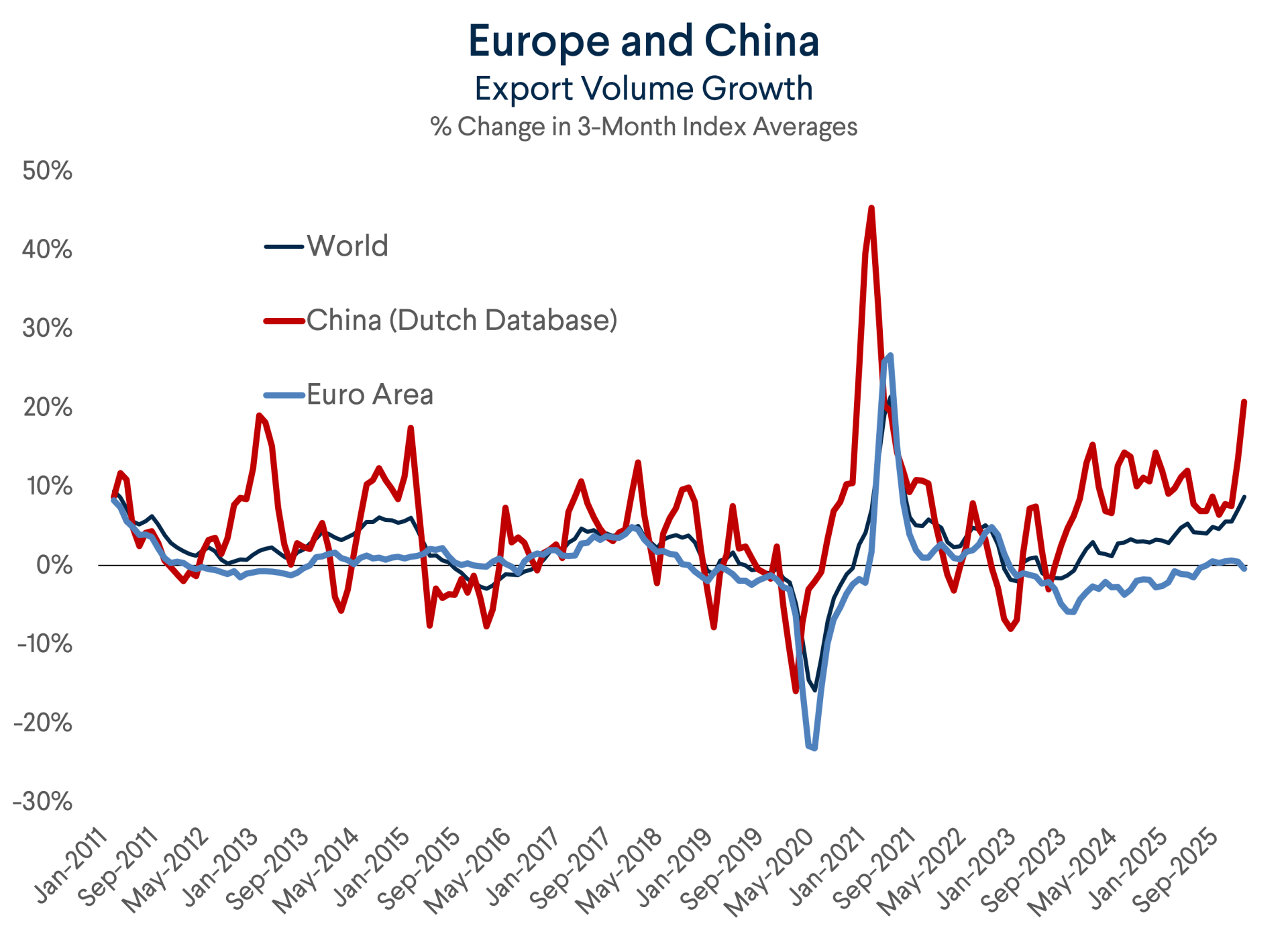

The systemic underestimation of China’s surplus was part-and-parcel of an IMF that, until last year, generally deemphasized imbalances (imbalances were judged to be small and on a declining path through the summer of 2024; fragmentation was consistently judged to the be bigger risk). See this chart from Shahin Vallee of the German Council on Foreign Affairs:

The IMF’s past tendency to forecast imbalances away has long been a source of frustration to me: lazy balance of payments forecasts were a symbol of an institution that often needed to be reminded of its actual mandate. It is mostly fiscal had become it is almost all fiscal, at least when it came to the Fund’s assessments of China.

There were three reasons back in 2023 to think that China’s surplus would trend up.

One was that China’s property bubble burst, and the bursting of property bubbles leads to falls in investment and often a rise in the surplus (or, if the property boom led to a deficit, to a reversal in the current account—as happened with Thailand in 1995 or Spain in 2008-2009). The best source on this is, well, the IMF (2024 ESR, Box 1.3).

The second was that China’s exchange rate had depreciated significantly, and the IMF’s own work (from back in the spring of 2015) would suggest that a weaker real exchange should push the external surplus up, not down (this was a real problem with the 2023 and 2024 forecasts).

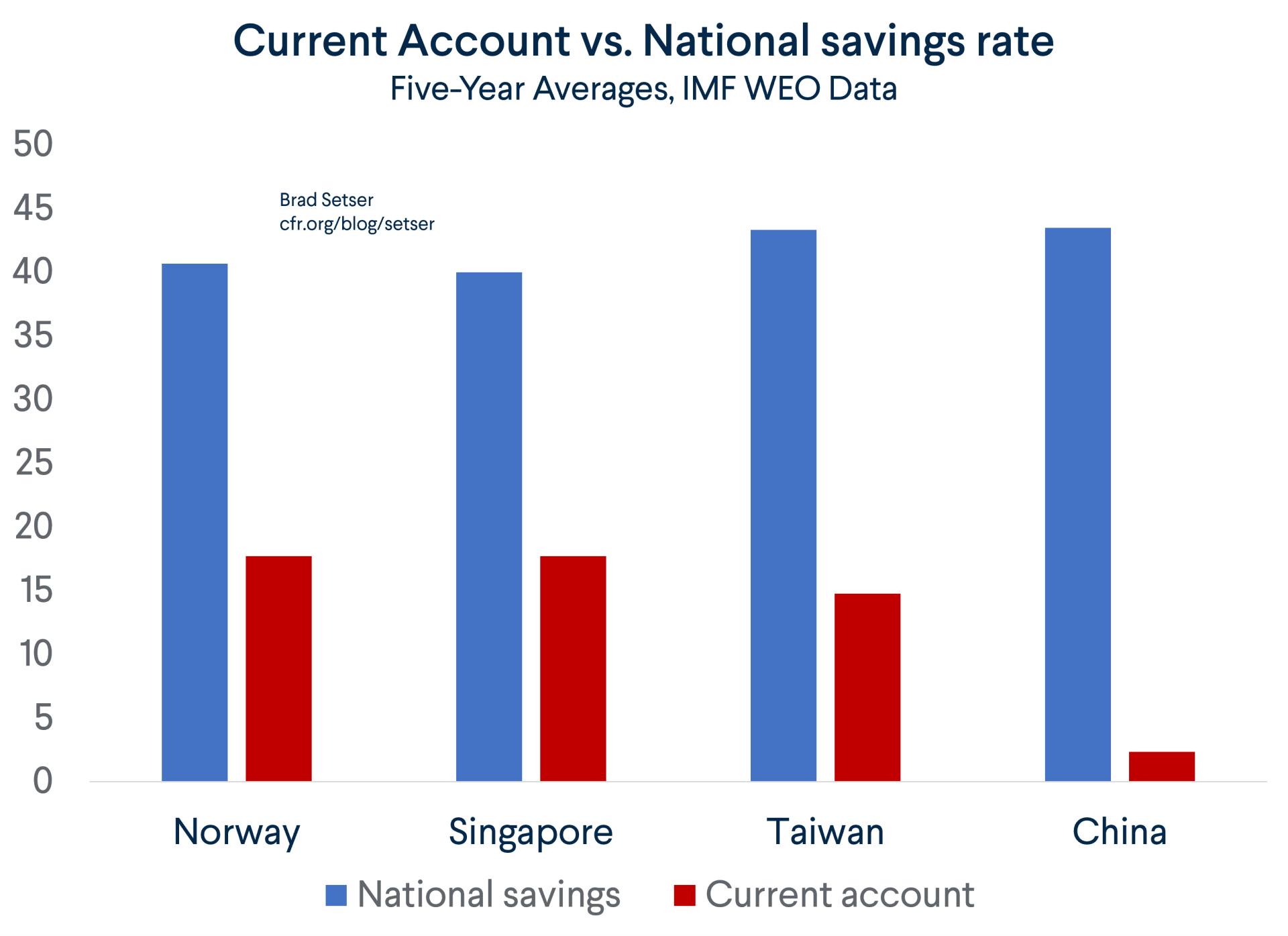

The third is that the persistence of China’s extremely high national savings rate suggest an underlying tendency toward a large external surplus. Most economies with savings rates of over 40 percent of GDP actually have current account surpluses of over 10 percent of GDP. China, even with a true current account surplus that is now close to 5 percent of GDP, is a bit of an outlier.

There was thus no real basis for the IMF to forecast a fall in China’s external surplus.

I make no claims to being a great forecaster, but I did see this coming; I said as much in my 2022 Foreign Affairs article:

“Back in 2009, China’s economy was able to pivot away from exports toward domestic real estate investment to mitigate the global fallout from the U.S. housing crisis because China’s financial system was strong enough to support this shift. Plus, China needed more housing and modern infrastructure. Today, China could not reverse that pivot with a large move away from real estate and back to exports without significant disruption, in part because its share of the global economy has roughly tripled in the years since the global financial crisis.”

Of course, debates about the past are never just debates about the past, as there is a real—if somewhat muted debate—over whether China’s trading partners should push for a policy mix that reduces China’s surplus, or more or less accept that the only way out of China’s fiscal, property and banking mess is an even larger external surplus.

Of course, no one explicitly says that they would welcome a bigger surplus. But if an international institution’s policy advice is monetary easing (to fight deflation), fiscal consolidation (because of off-balance sheet fiscal risks) and more exchange rate flexibility it is effectively advocating for the country to export its way out of its domestic troubles.

There is a variant of this argument which claims that it is impossible for China to generate a real appreciation now, as any nominal appreciation will be met with more depreciation. In reality, of course, nominal prices are sticky (even in China) and nominal moves do generate real moves (the last 8 months have been a case in point).

Of course, it is much more difficult for the IMF or any other body to recommend explicitly that China export its way out of its domestic property downturn now than it was during the peak of the Covid crisis. After five or so years of export-led growth, China’s surplus is not only big—it is much bigger than the IMF’s models imply it should be.

China’s leading think tanks now tend to argue that China’s surplus is just a function of China’s evolving pattern of comparative advantage, and thus something that China’s trading partners should accept. That claim is of course incomplete; comparative advantage implies both exporting and importing more, as both trading partners specialize.

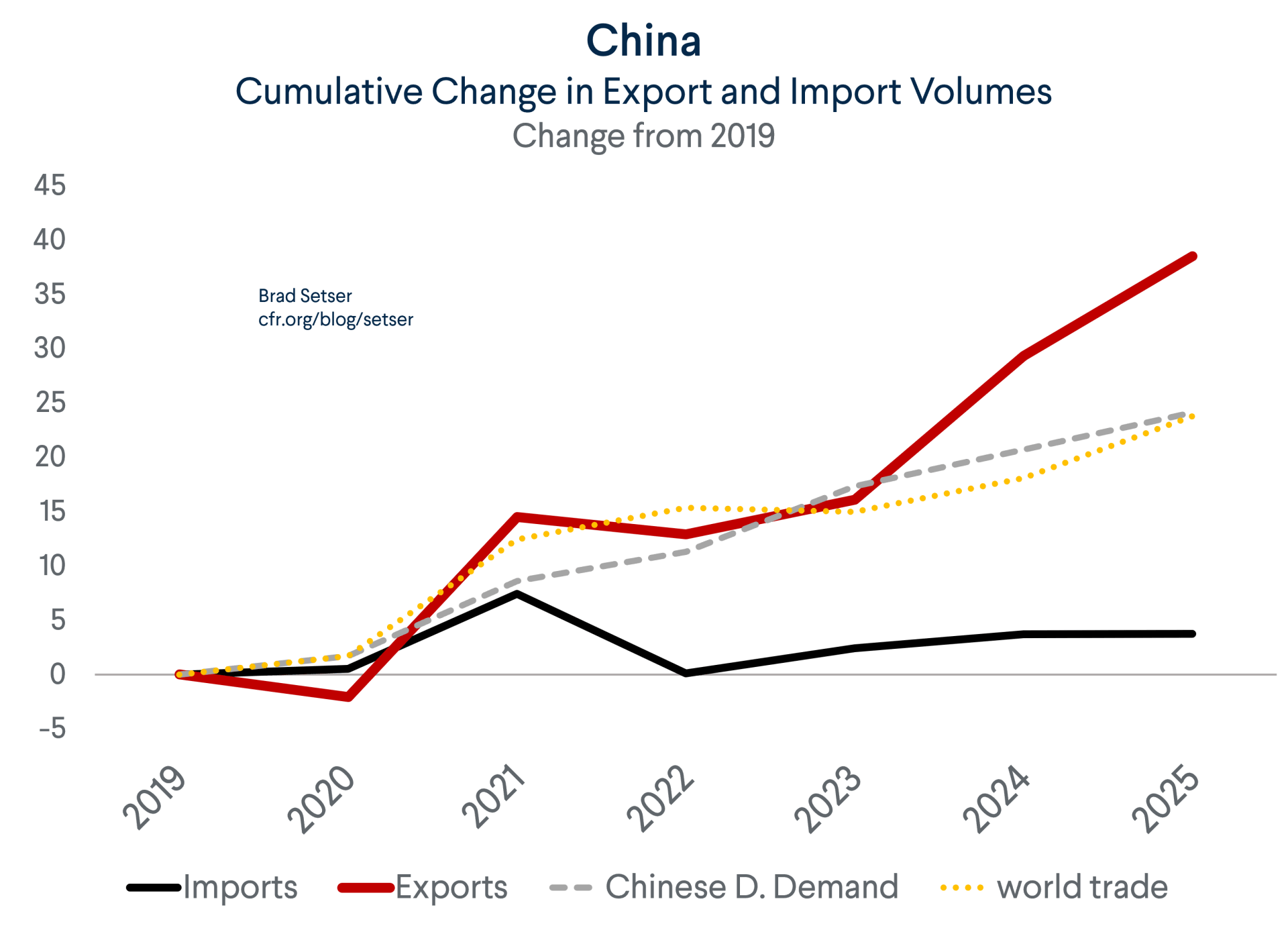

Over the last five years, China’s exports have soared—growing faster than either global trade (especially in real terms) or China’s own economy—while China’s import growth has been unimpressive. Even almost non-existent. The surge in both exports and imports in Q1 seems to stem primarily from imports of previous metals and a faulty semiconductor price adjustment (which ends up overstating import volumes, roughly one quarter of China’s imports of manufactures are chips).

The basic question facing China and its trading partners now is whether it is worth pushing China to change its pattern of growth, or whether, well, China’s trading partners should just, well, chill, and accept China’s “comparative advantage in industrial policy” will result in an ever more unbalanced Chinese economy.

I think the answer is obvious.

A deindustrialized Europe isn’t in the interest of its military allies, including (for now, at least) the United States.

A deindustrialized and politically radicalized Europe isn’t in the interest of Europe’s neighbors.

And a China that controls more of global supply will be in a stronger position to impose its policy preferences on the rest of the world. It will be very difficult to reduce weaponizable supply chain dependencies on China if the world is being more, not less, dependent on China in aggregate. Growing dependencies on base chemicals even as dependencies on the chemical precursors for active pharmaceuticals remain unresolved suggests the EU and the U.S. (together, or more likely separately) aren’t yet prepared to effectively counter Chinese supply chain warfare.

All this matters, of course, because without a change in China’s savings rate, any fall in investment should push China’s surplus up more. The IMF’s latest policy package for China recommends a permanent reduction to subsidized industrial investment (fair enough) and a modest and temporary half point of GDP in fiscal support for consumption (paragraph 63).

The claim is that the reduction in inefficient investment will on its own raise demand today as consumers will instantly realize that they will be wealthier in the future and thus raise current consumption. I am more of a bird in hand kind of guy; households who lose jobs building new factories aren’t going to suddenly raise their consumption. A stronger push to support consumption would be needed to avoid a rise in the current account surplus if investment in both property and new manufacturing capacity are depressed.

The bigger point is that China is a bit of an outlier.

For example, it has a managed currency that is an independent vector of policy, one that isn’t just a reflection of monetary policy choices.

And conventional policy advice needs to be recalibrated, at least in my view, in the context of an economy of China’s size that saves 40 percent of its GDP. Singapore doesn’t have China’s scale—its 20 percent surplus is too high, but doesn’t generate large global spillovers.

China’s move back to surplus of 5 percent of its GDP has resulted in large, negative spillovers to other manufacturing driven economies.* A move toward a 10 percent or 15 percent of GDP surplus would have even bigger negative implications for China’s trading partners. That should give even conventional macroeconomists pause because they advocate solutions to China’s domestic imbalances that would imply even larger Chinese external imbalances—and a more distorted global economy.

* Correctly measured, as China clearly understates its investment income and the 2022 “survey” based adjustment to the goods line in the balance of payments still may knock a percentage point off the recorded surplus. A survey based methodology is something the IMF recommends (mistakenly in my view) but that doesn’t change the fact that the introduction of this methodology revised China’s surplus down in ways that neither the IMF or SAFE have been able to explain.