Dark Matter. Soon To Be Revealed?

The debate around the House Republicans’ proposal for a border adjusted (destination-based cash flow) tax will, I think, force an important debate about the impact of corporate tax strategies on global trade flows.* My guess is that tax strategies do have a significant impact on the trade data (one hint: the trade deficit in pharmaceutical the U.S. now runs with Ireland and Switzerland). And in turn I suspect that the revenue projections from the House’s proposals will depend in part on how firms are expected to adapt to a world where export revenues booked in the U.S.—including export revenues from the royalties on intellectual property—are not taxed. A world where the U.S. suddenly becomes tax competitive with Ireland, the Netherlands and others.

I suspect that the size of the impact will surprise many people.

I first started looking at the impact of firms’ tax strategies on the balance of payments back in early 2006, as part of a debate over the sustainability of the U.S. trade and external deficit. One argument at the time was that Americans had nearly magical skills at cross-border investing—magic that produced a surplus on net foreign direct investment (FDI) income (the dividends that American firms receive on their foreign investment relative to the dividends foreign firms receive on their U.S. investments) that would perpetually negate the United States’ interest payments on its net external debt. That magical surplus on investment income in the balance of payments effectively made conventional measures of U.S. external debt sustainability moot.

Harvard’s Ricardo Hausmann has always had a way with words. He named the forces that kept the U.S. income balance positive even as the U.S. ran persistent trade and current account deficits: dark matter.

Time, I think, has helped bring the sources of dark matter—or, put differently, the sources of the United States’ exorbitant privilege—into the light. I suspected back in 2006, and now suspect even more strongly now, that “dark matter” is largely a function of the tax strategies employed by firms like Apple (here is a 2005 Wall Street Journal article focusing on another large tech firm).

The “income” the U.S. earns on its equity investment abroad now heavily shows up in low-tax jurisdictions. The “stock” position is now relatively balanced (the market value of U.S. direct investment abroad was $7 trillion at the end of 2015, which is not that different from the $6.5 trillion value of foreign direct investment in the U.S). The net income the U.S. earns on investments abroad essentially comes from the difference between the low cash returns foreign companies report on their U.S. equity investment and the large returns American firms report on their non-repatriated (e.g. tax deferred) income abroad.

One implication of this analysis is that the U.S. trade balance could change significantly if “tax” considerations led American firms to want to report the income that now shows up offshore in low-tax jurisdictions globally as onshore income. The royalties American firms receive “onshore” might jump significantly, and royalties count as service exports in the trade data.

The Original Puzzle

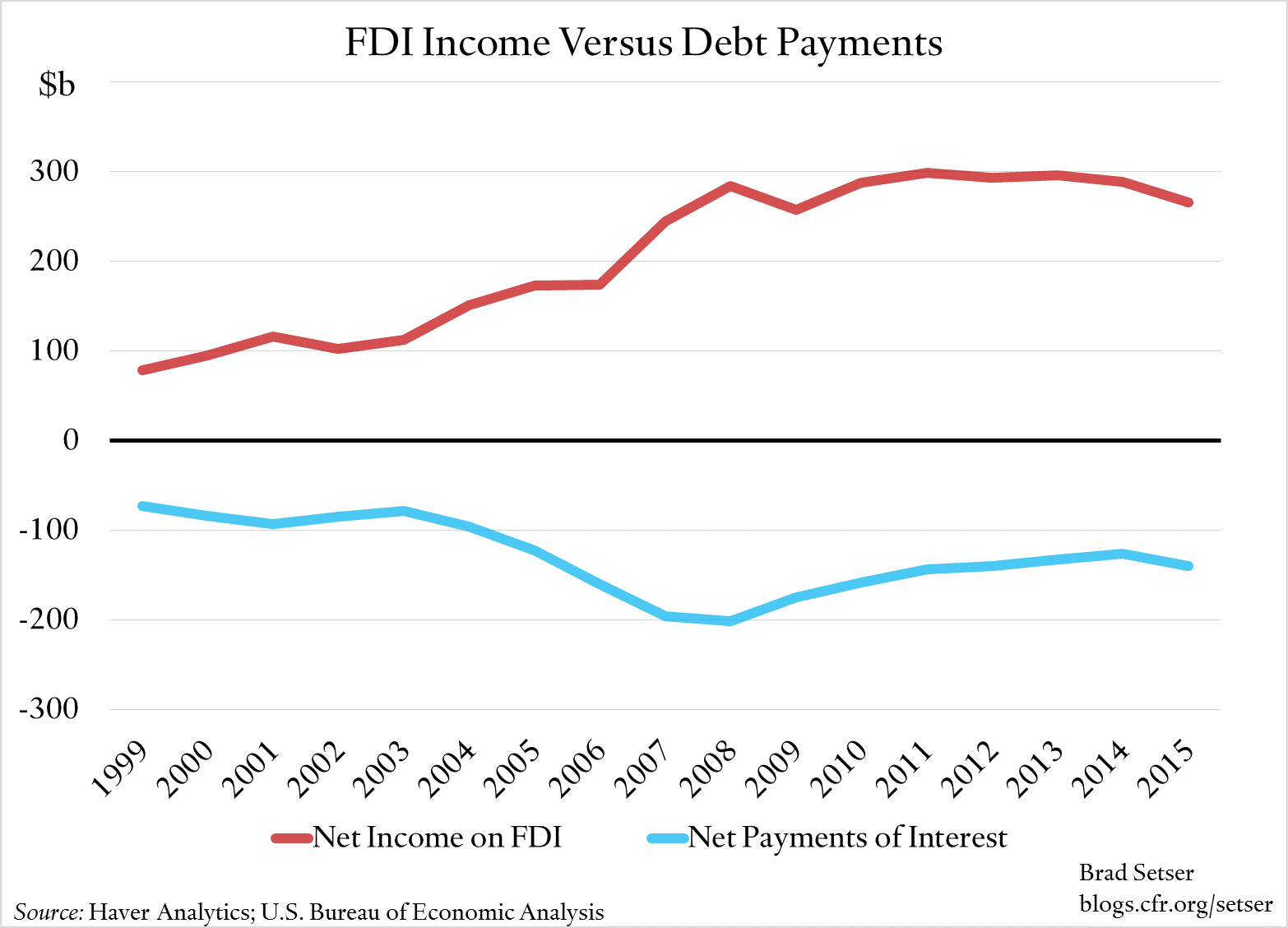

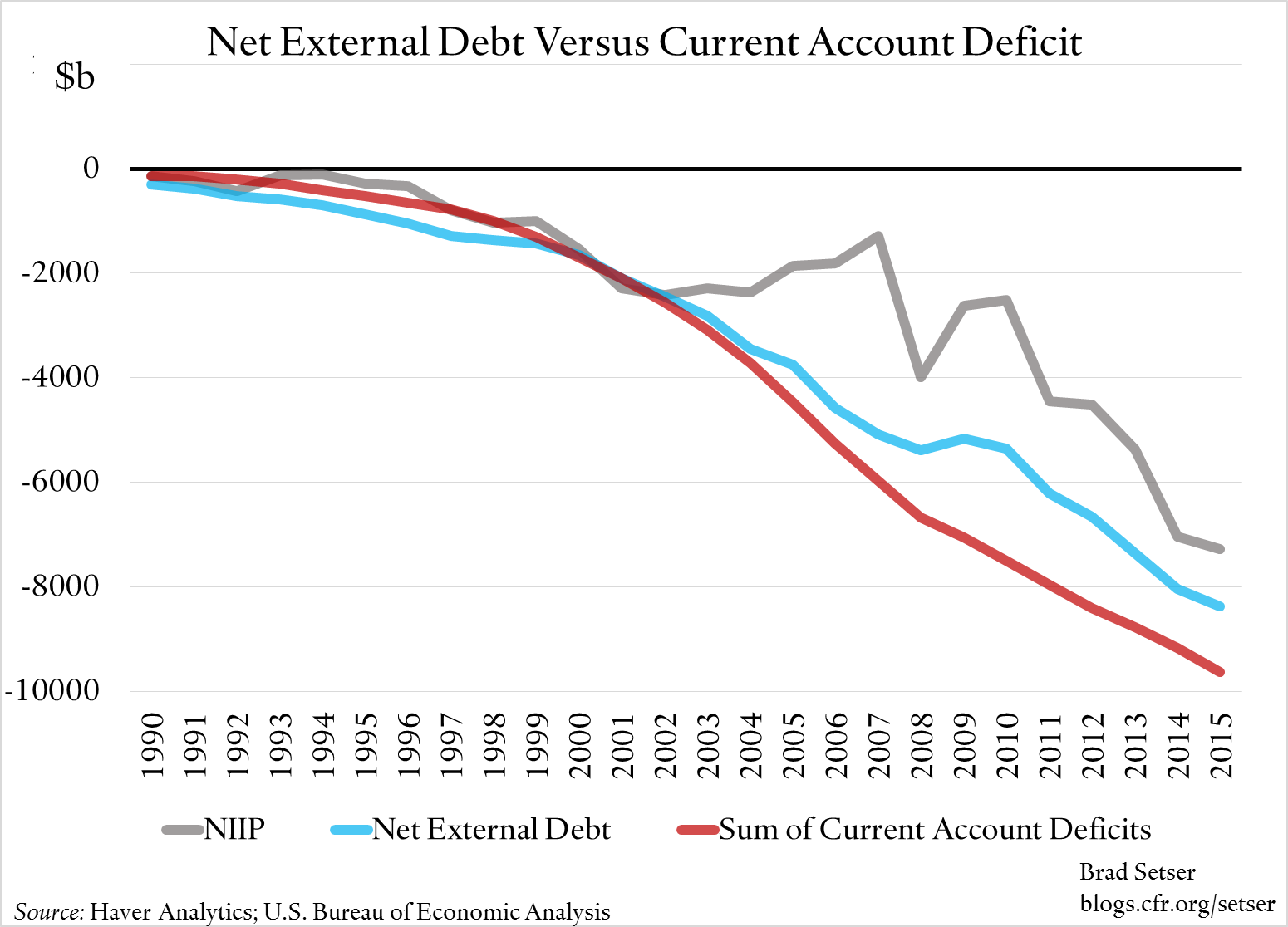

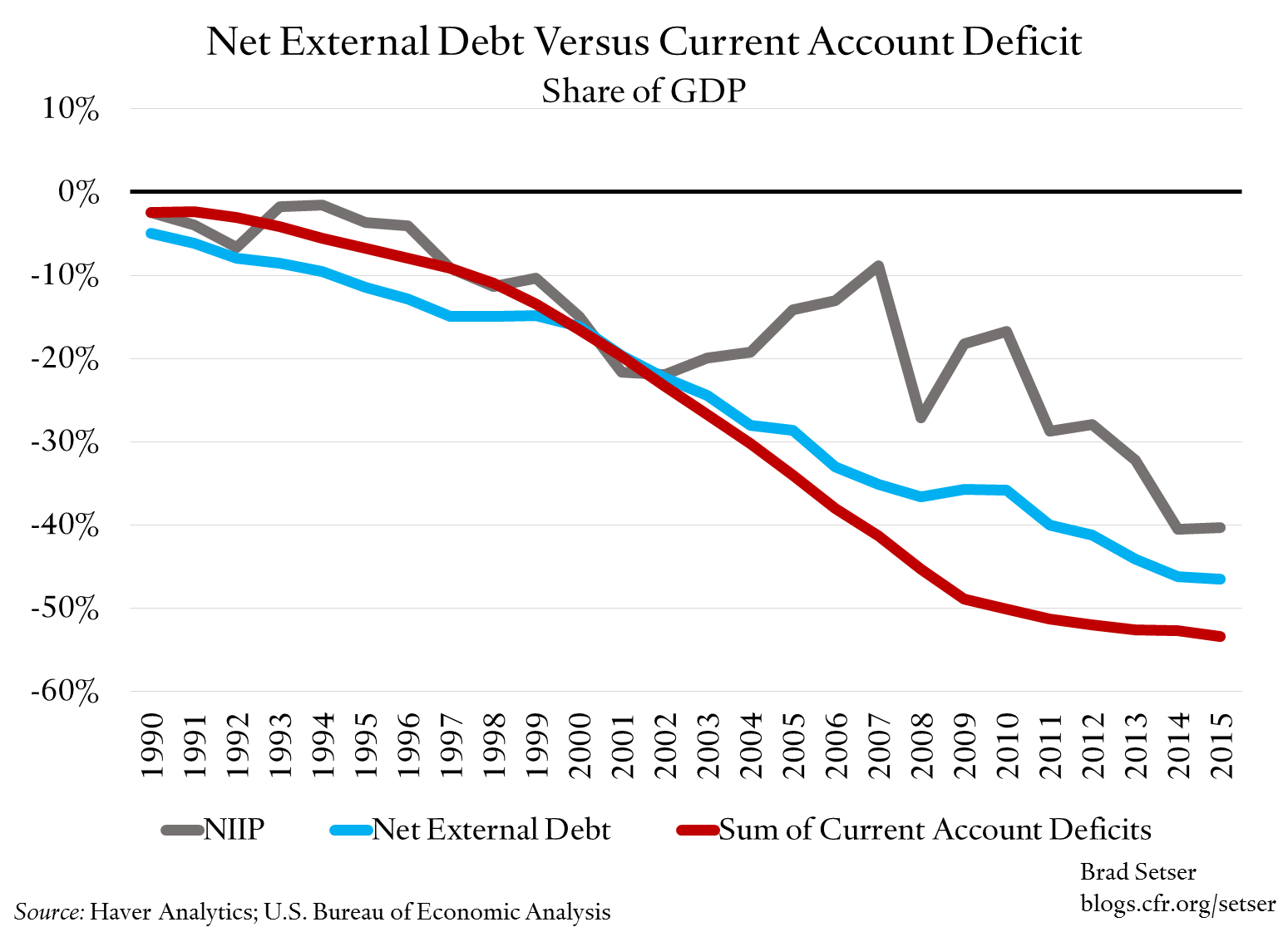

I should start with the basics. The U.S. has run persistent trade and current account deficits (the last U.S. surplus, was, gulp, in the 1970s). That implies a buildup of foreign claims on the United States: a current account deficit means that you need to borrow from the world, or sell equity to the world. Yet even with persistent current account deficits, the U.S. doesn’t, on net, pay interest and dividends to the world. OK, the U.S. does pay interest, but interest payments are more than offset by dividend receipts. The balance on investment income is positive.

Hausmann and his co-author Federico Sturzenegger (now the central bank governor in Argentina) said that this must be explained by an invisible asset on the U.S. international balance sheet that offset the obvious debts. But if you start to disaggregate the U.S. external balance sheet—and the income balance (the sum of interest and dividend payments)—the U.S. income surplus becomes a lot less mysterious.

The evolution of U.S. external debt—if you strip equities off the balance sheet—is actually not that hard to explain. Net external debt has gone up predictably, more or less in line with the sum of U.S. current account deficits.

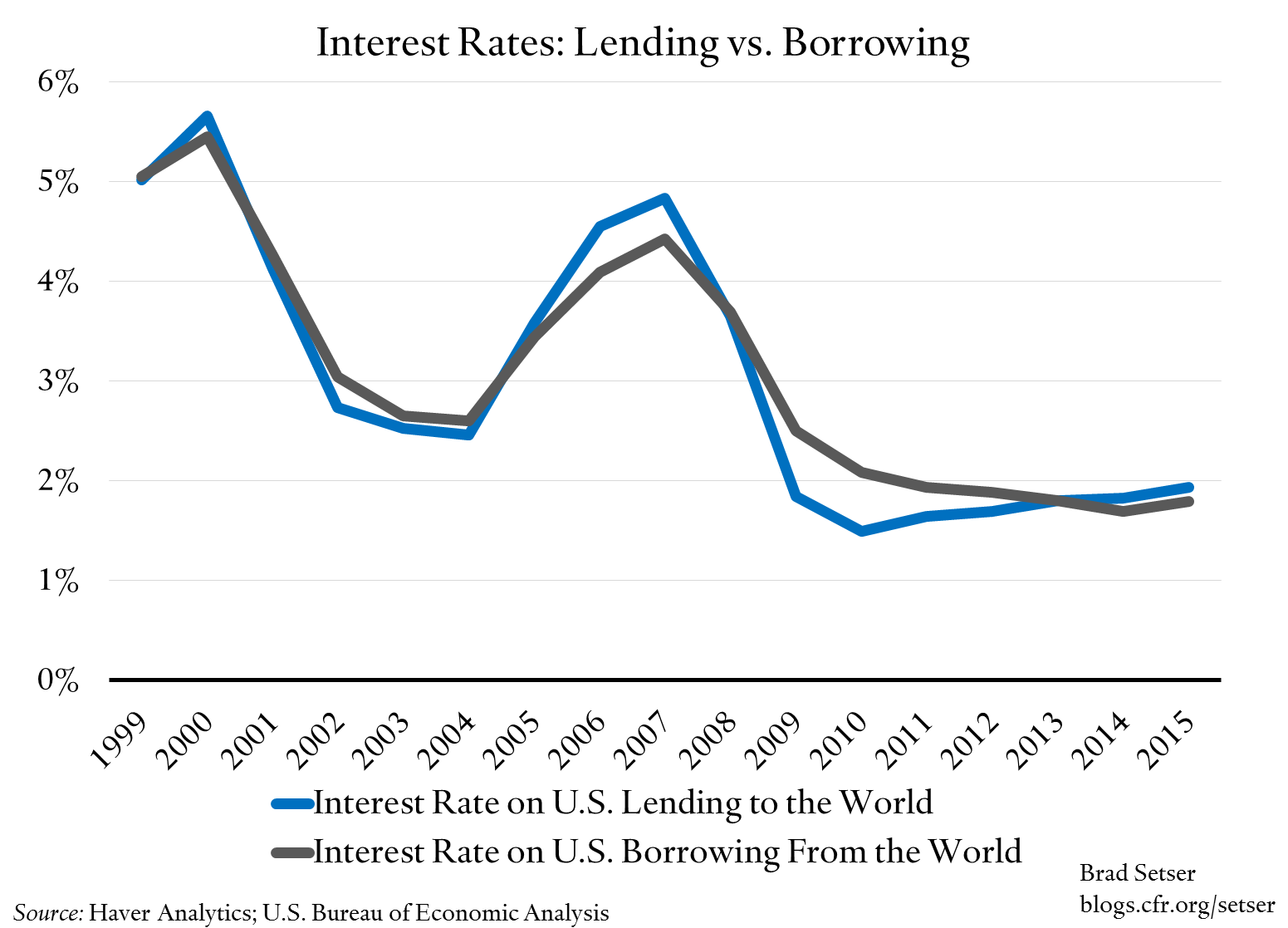

The interest that the U.S. pays on that debt has fallen since 2007. In 2006, the average interest rate the U.S. paid on its external debt was about 4.5 percent. Now it is about 2.0 percent (2.5 percent on debt securities, 0.5 percent on bank loans). The U.S. earns a tiny bit more on its lending to the world than it pays on its borrowing, but given the discrepancy in the size of the respective stocks, the impact of this difference is negligible. The fall in the United States’ net interest bill since the crisis reflects the fall in U.S. interest rates, not a clever financial arbitrage.

The Income Surplus All Comes from Foreign Direct Investment

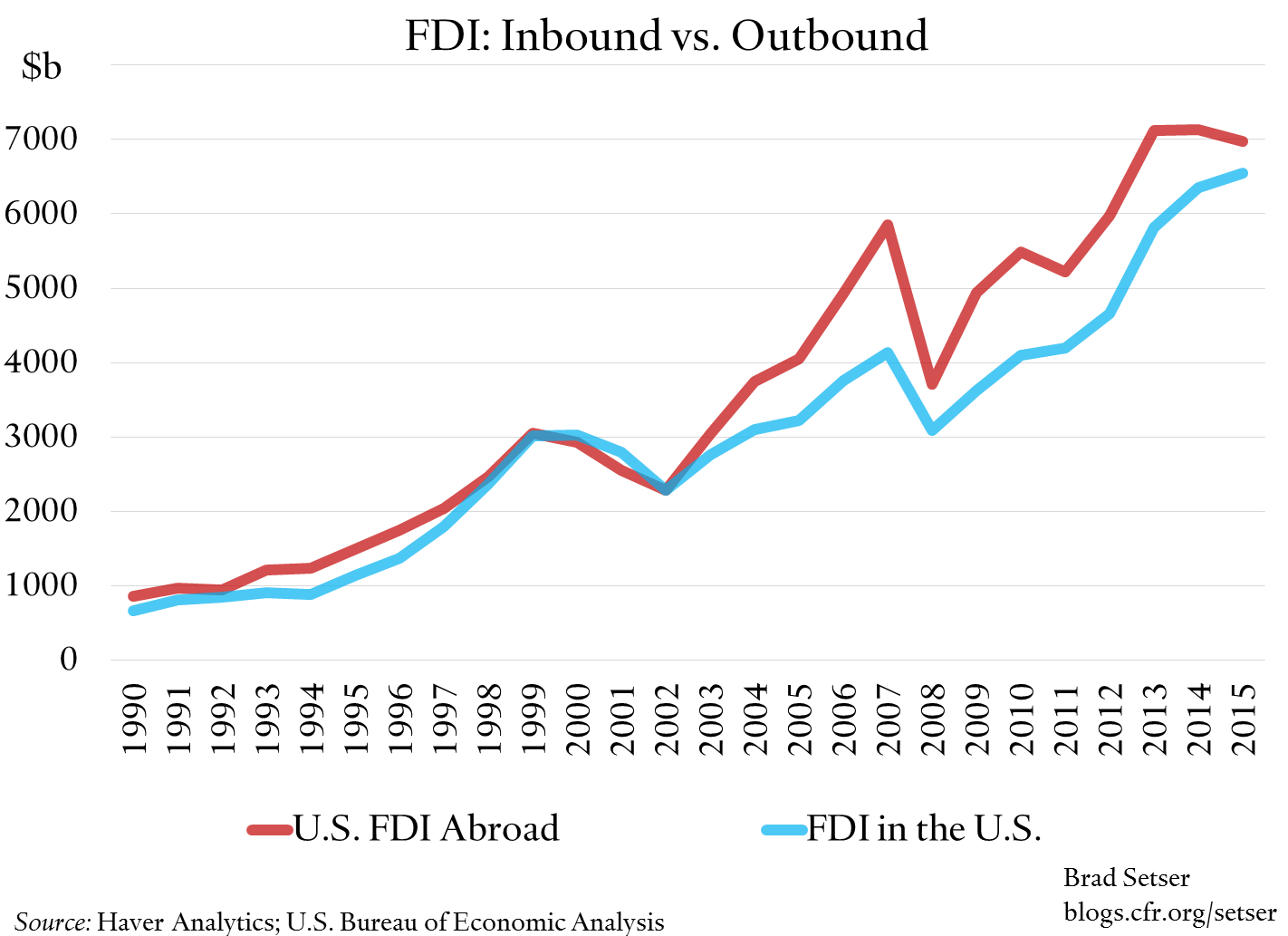

The interesting bit—the true dark matter—all comes from foreign direct investment (FDI). The United States. now has a bit more FDI abroad than foreigners have direct investment in the United States. U.S. direct investment abroad is around $7 trillion, or just under 40 percent of U.S. GDP. Foreign direct foreign investment in the U.S. is around $6.5 trillion, or just over 35 percent of GDP. But the gap isn’t that big (*). Net FDI assets are about 3 percent of GDP.

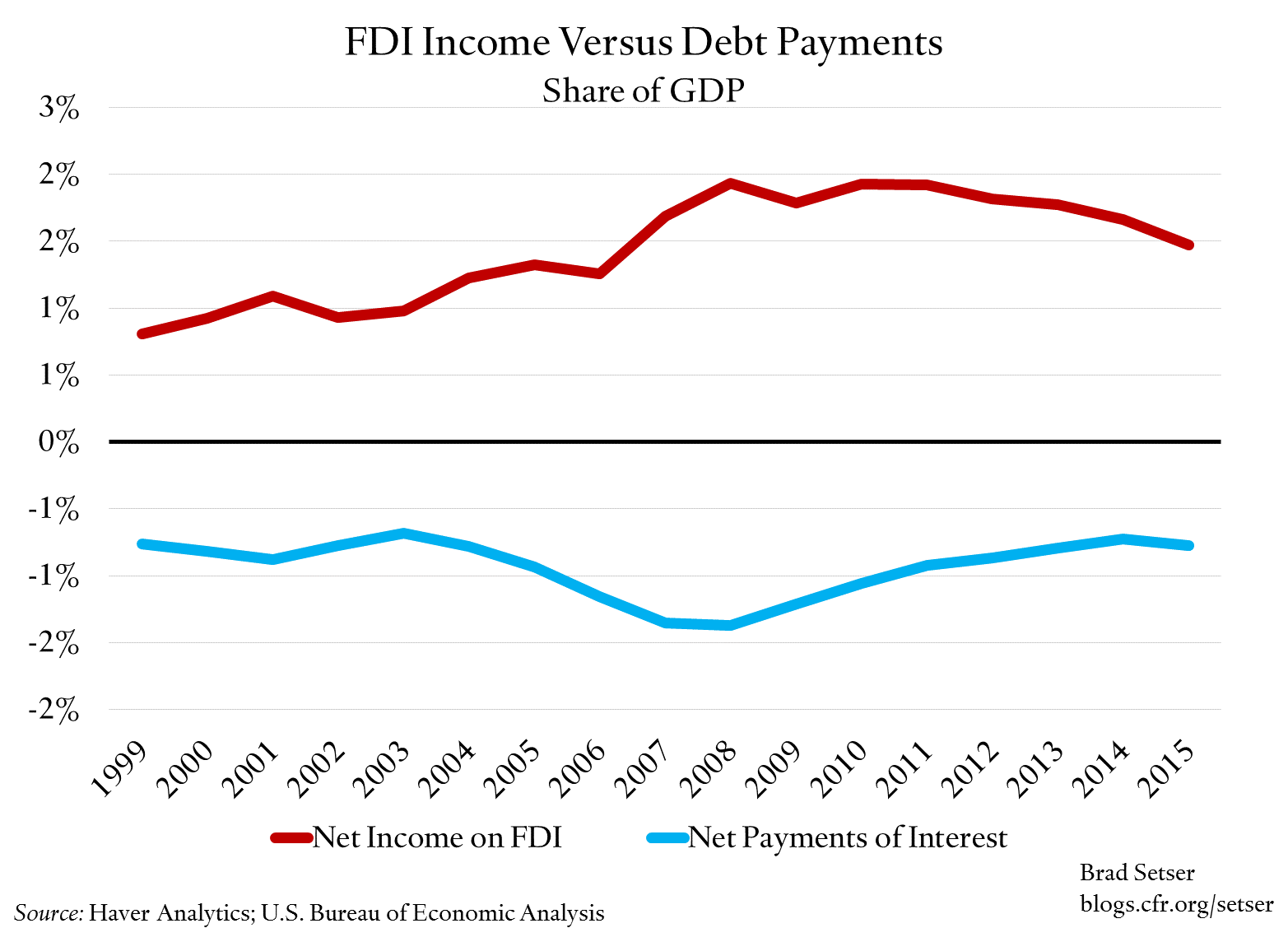

Yet net FDI income (think the dividends the U.S. receives on its equity investment abroad, net of the dividends the U.S. pays to foreigners who have invested in the U.S.) is 1.5 percent of U.S. GDP (it was 2 percent a few years back). Dark matter!

So what explains the gap? U.S. direct investment abroad earns about 6 percent. Foreign investment in the U.S. earn about 2.5 percent. So even though the U.S. has invested about as much in the world as the world has invested in the U.S., the U.S. economy receives far more from its investment abroad than the U.S. pays to investors from the rest of the world.

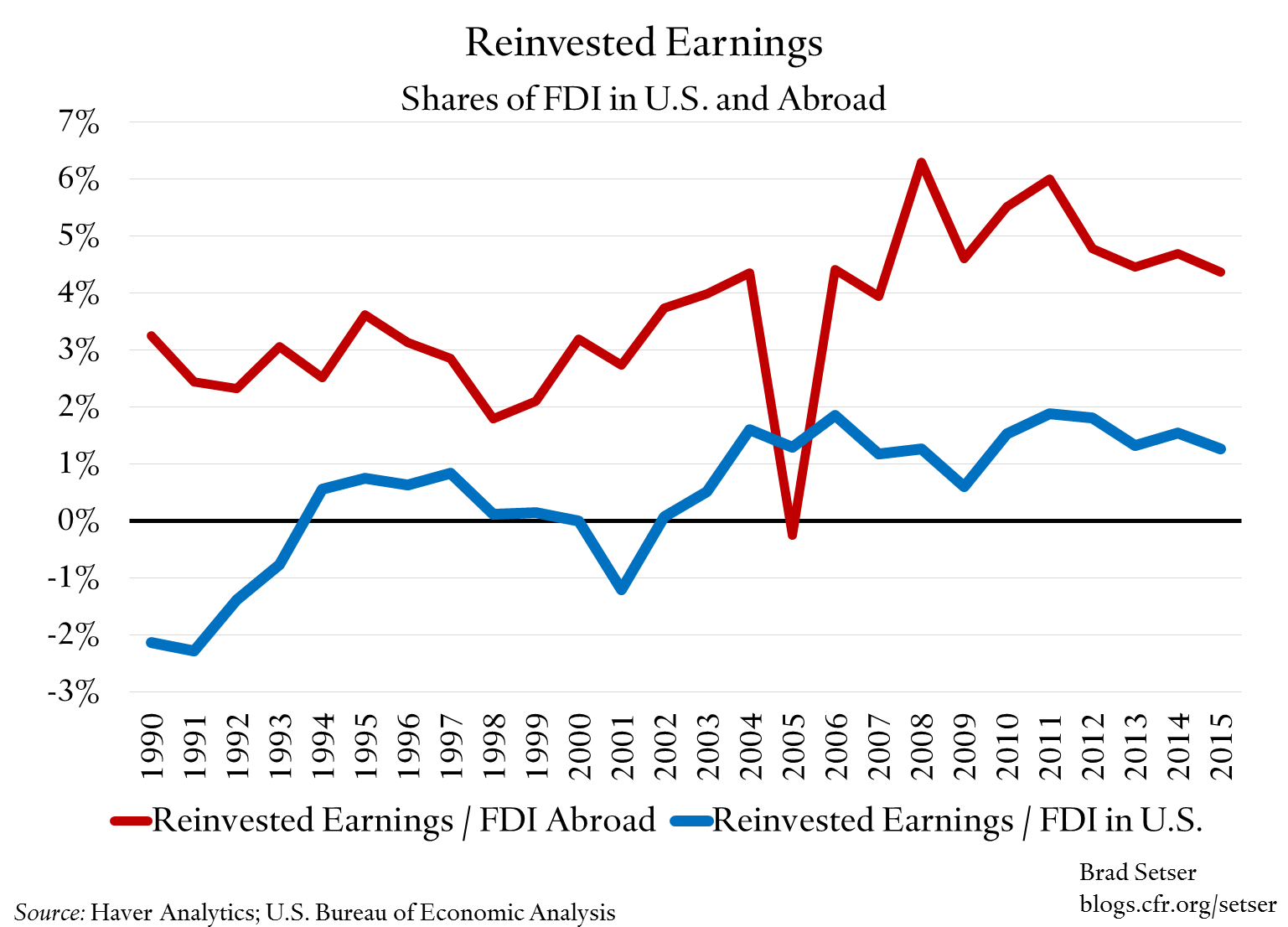

The Income Surplus Comes From “Reinvested Earnings” and Those Earnings Are Mostly in Tax Havens

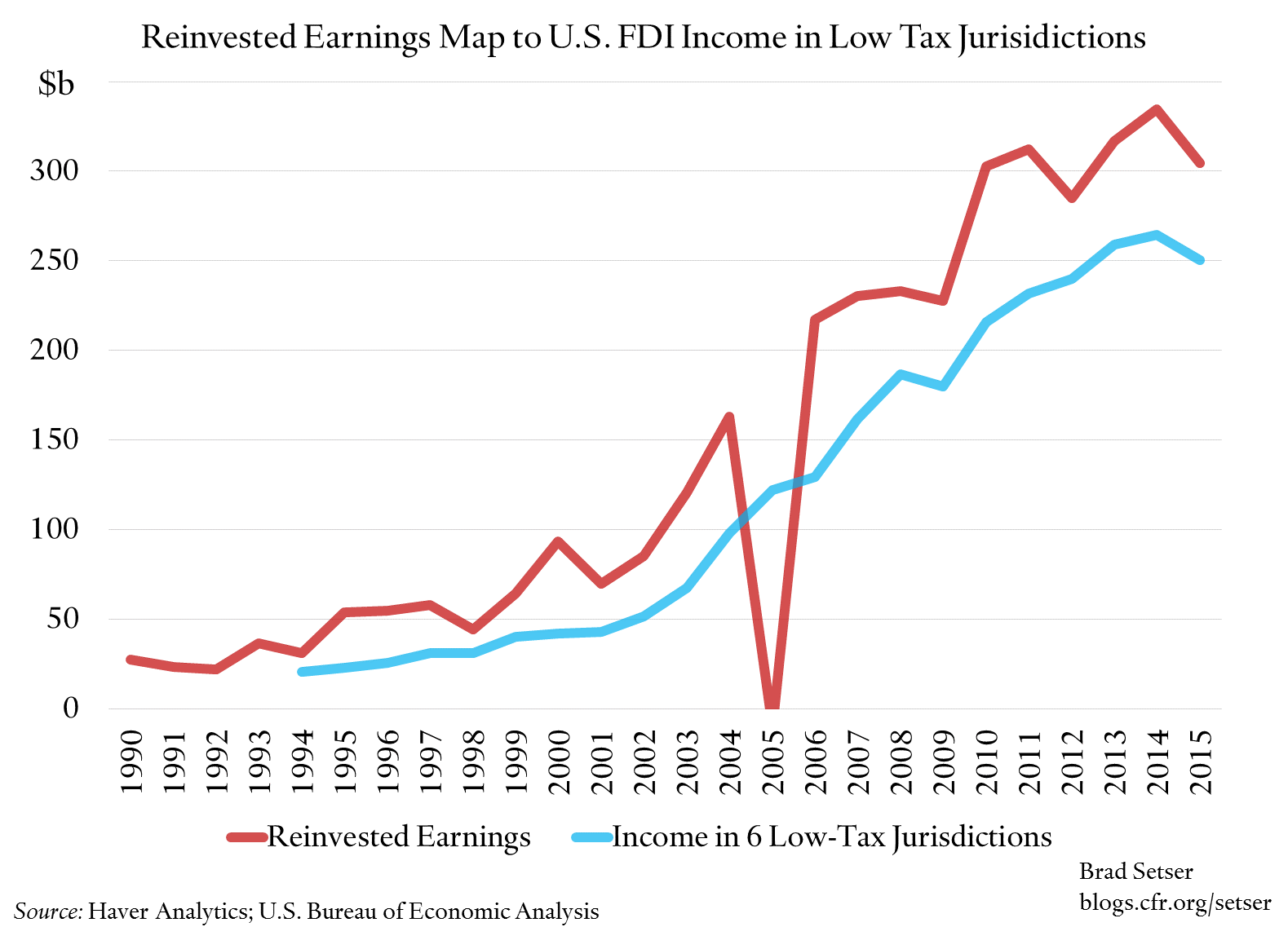

If you disaggregate further, the gap is almost entirely from income earned abroad that is reinvested abroad. Cash dividend returns are similar.

And that is where the U.S. tax code comes in. Profits U.S. multinationals earn abroad are tax-deferred so long as they are held abroad. The profits are reported to the U.S., but no tax is paid until the funds are formally brought home. This rather clearly creates incentives to locate profits abroad, by adjusting transfer prices for example. And to locate profits in locations that offer obvious tax advantages.

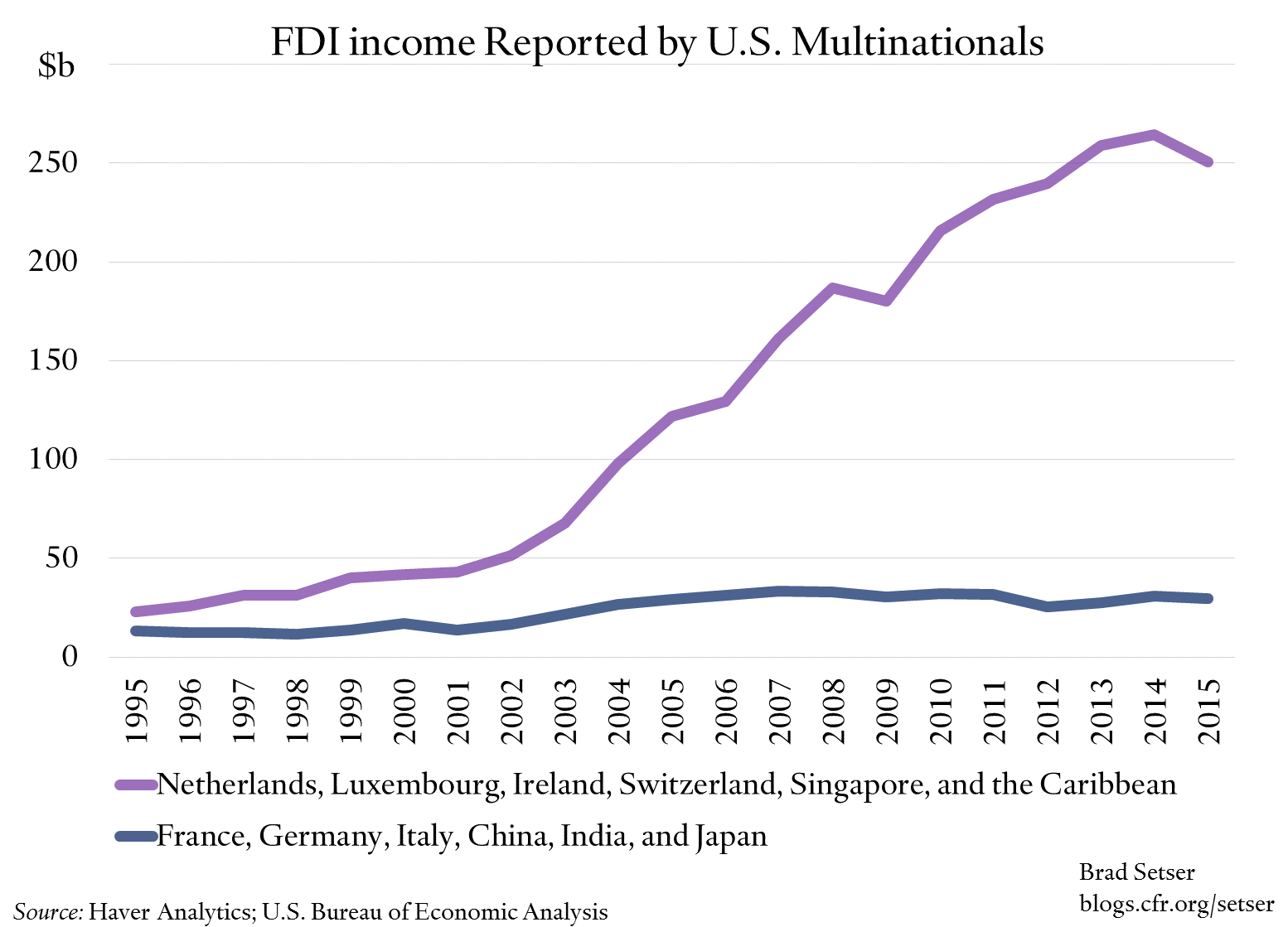

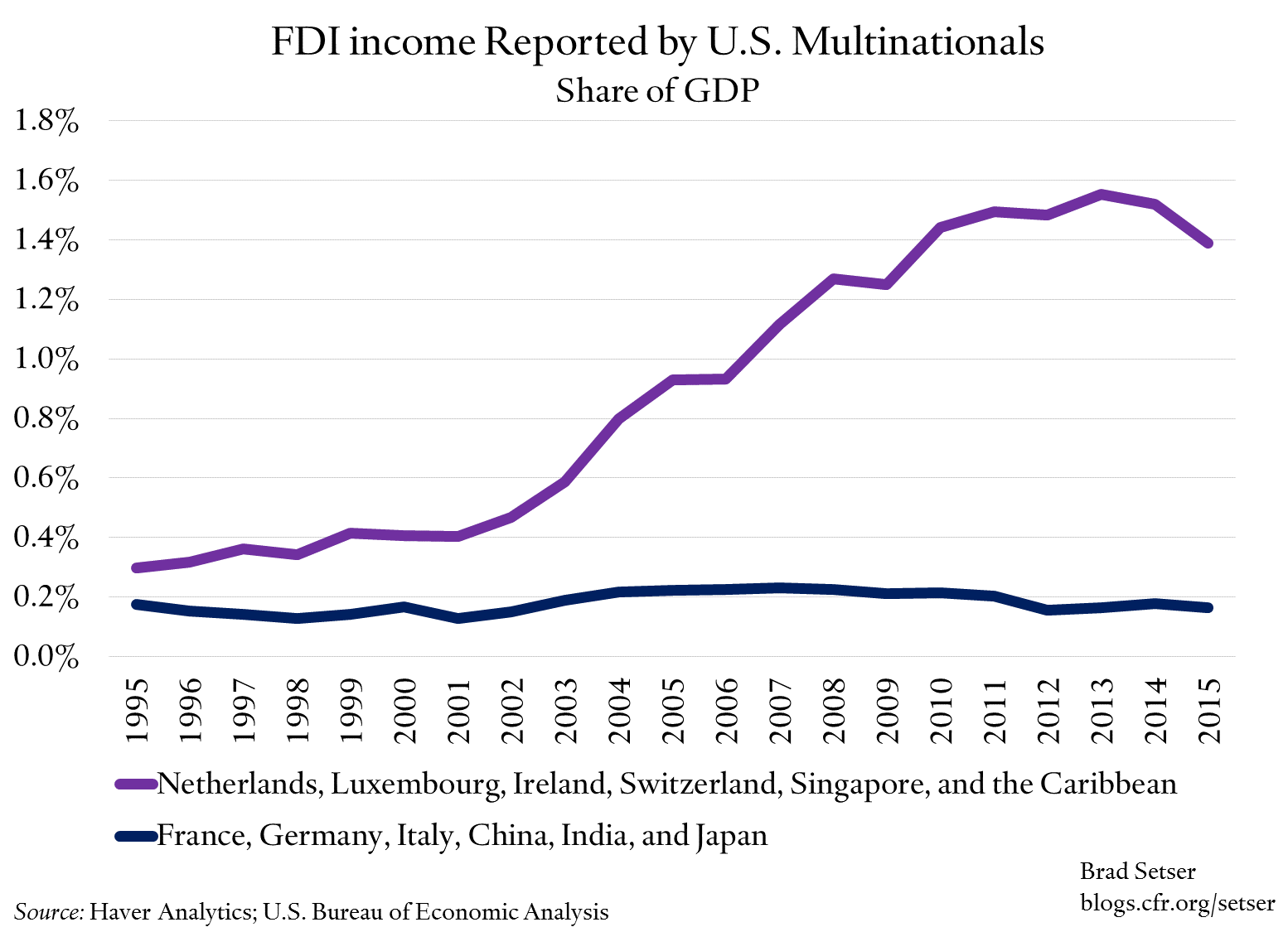

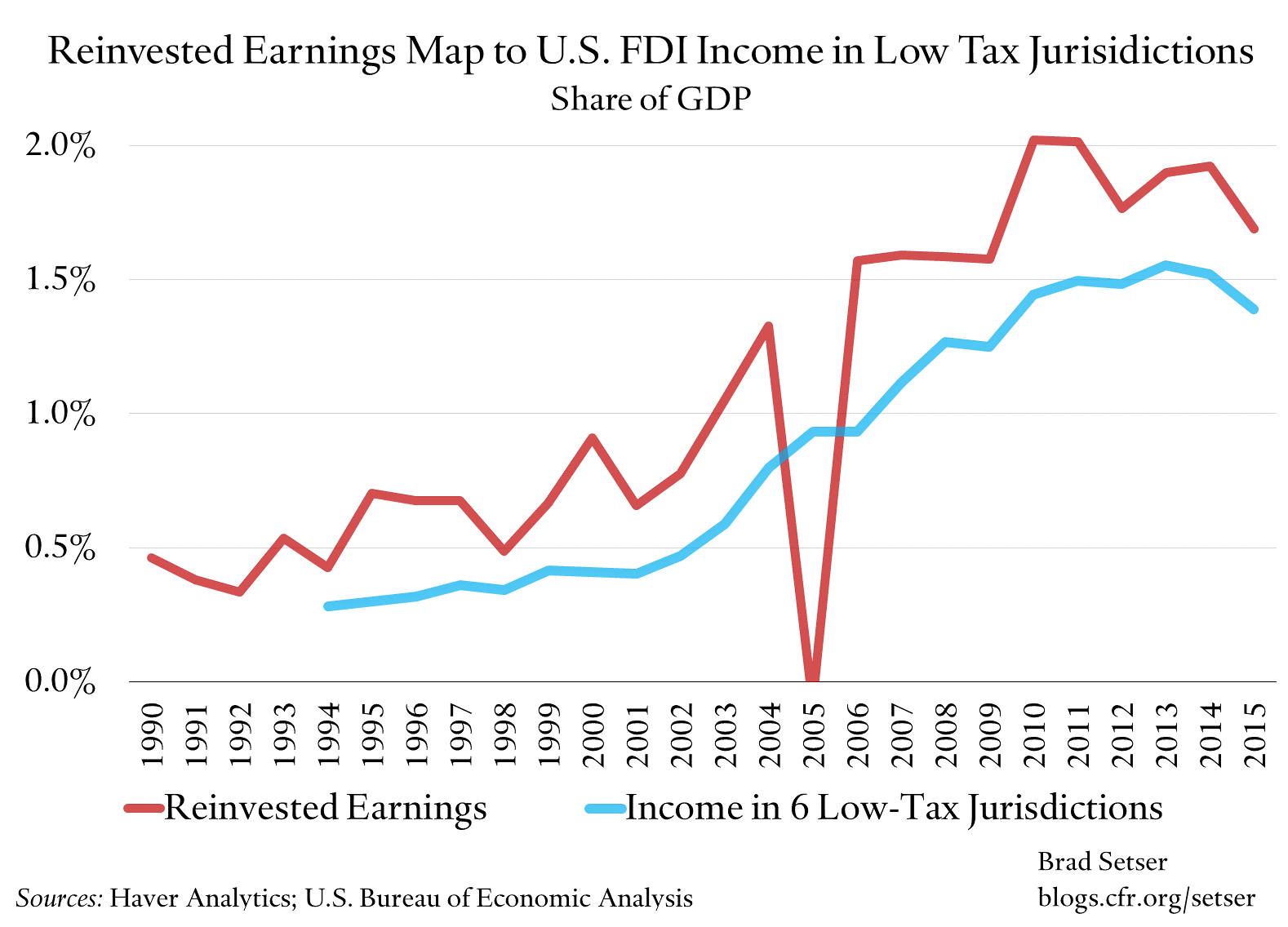

The U.S. balance of payments data is really good, with an incredible level of detail available if you dig. So it isn’t all that hard to compare the profits (income in balance of payments speak) U.S. multinationals report in a set of tax havens to say the income they report in Germany, France, Italy, Japan, China and India.

Rather striking.

The profits American firms report in these low-tax jurisdictions also map quite well to the overall level of “reinvested” (e.g. tax-deferred) earnings of U.S. firms abroad.

European and Japanese firms (and Chinese firms, who all seem to enter the U.S. through various tax havens of their own—actual reported investment from China in the balance of payments remains very small) have no such incentives to show income in the U.S.. That presumably is why the reported returns of foreign firms in the U.S.—as measured by the income payments in the balance of payments—are quite low.

Voila! Dark matter. Or, less elegantly, the traces that the tax strategies of large multinationals leave in the balance of payments data.

I am not at all convinced that this is entirely healthy.

Since 1995, U.S. exports of capital goods, autos, and consumer goods have barely risen as a share of GDP—they have been flat at about 5 percent of U.S. GDP. Over that time period, U.S. imports of capital goods, autos, and consumer goods rose by 2.0 percent of GDP

And, over that same time period, the non-repatriated (reinvested, and in large part perpetually tax-deferred) income earned abroad by U.S. multinationals has increased by over 1 percent of GDP. Income earned abroad and reinvested abroad by U.S. multinationals has gone from about 0.5 percent of U.S. GDP in 1995 to about 1.7 percent of U.S. GDP (it was as high as 2.0 percent of GDP before the dollar strengthened, reducing the dollar value of many firms offshore earnings, in late 2014).

The fact that a lot of the gains from globalization seem to be able to avoid taxation has distributional consequences, of course. I suspect it explains the common sense that the rules have been “rigged.”

But it also potentially has a big impact on the revenues that can be expected from any border adjustment.

If a lot of the revenue and profit that U.S. firms now report in the world’s low tax jurisdictions suddenly showed up in United States, the U.S. trade deficit would fall (what is now a profit booked in say Ireland would show up as profit in the U.S.; the current account would not change, but the balance between the income surplus and the trade deficit would shift—see this post on Apple). Profits on exports revenues are not taxed in a destination based cash flow tax—indeed, a firm that exports effectively gets a partial rebate on its wage bill (if I have understood everything correctly, see Chad Bown’s presentation at Peterson).

The net result: if all the surplus from reinvested earnings in the 2015 balance of payments appeared on the export line, the goods and services trade deficit would fall from 2.75 percent of GDP to about 1.5 percent of GDP.

That may well paint a more honest picture of the U.S. economy. But it also means the border adjustment would generate significantly less net revenue than forecast.

* Alan Auberbach and Michael Devereaux are among the main intellectual architects of a destination-based cash flow tax (papers: here and here). Their new working paper (with Michael Keen and John Vella) on the topic thoughtfully highlights many of its features. In particular I would note the distinction they draw between a world where all countries adopt such a tax and a world where one country adopts the tax. The Peterson Institute also recently hosted an excellent conference on the topic: conference materials are here.

Appendix items: Selected charts in USD billions rather than as a share of GDP: