China’s Q1 Import Surge, Disaggregated

This is a joint post with Cole Frank, a research associate here at the Council on Foreign Relations.

One of the challenges China poses is that by the time something shows up cleanly in the numbers, things often have changed. I feel that risk acutely now. The latest high frequency indicators (iron ore prices…) suggest China’s economy is now decelerating on the back of what appears to be a significant policy tightening.

But that deceleration looks to have come after a very significant upturn.

The hard numbers for q1 2017 point to substantial acceleration in growth late last year and early this year. The trade numbers for one.

In the first quarter of 2017 China’s headline exports totaled $482 billion and its imports $417 billion, up 8 percent and 24 percent, respectively, over the same period last year

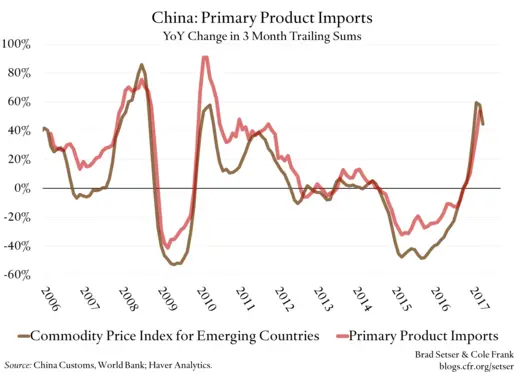

To be sure, a large part of the story comes from the rebound commodity prices over the last year (commodity prices were particularly low in q1 2016). Comparing the year-over-year changes of commodity prices to the value of China’s imports of primary products (the Chinese trade dataspeak for commodities) makes that point pretty clearly:

That said, it’s neither all commodities nor just a price effect. Volumes of both imports and exports are up big year-over-year: q1-2017 import volumes are up just over 15 percent, and export volumes are up almost 10 percent.

The rise in in China’s import volumes reflects a real upturn in growth—driven by its 2015-2016 stimulus. That credit-driven stimulus may well be bad for China, but it clearly has been a boon for the rest of the world.

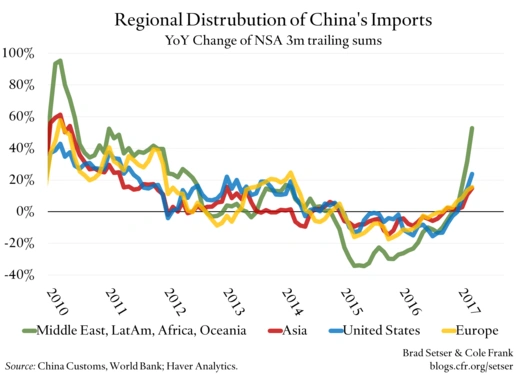

All the major regions of the world economy have seen their exports to China jump. Middle East, Africa, and Latin America, Asia, the United States, and the European Union have all seen solid growth in their exports to China over the last year.

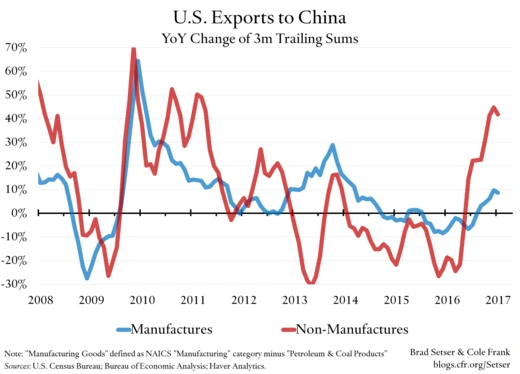

The U.S. has done a bit better than Europe and Asia recently. But this actually isn’t surprising. Nor is it a sign Trump has struck a better deal with China. The real reason is simple: a decent share of U.S. exports to China are commodities, and thus U.S. exports to China tend to be influenced by commodity prices more than European or Asian exports to China. Manufactured exports are up just under 10 percent y/y, while commodity exports are up over 40 percent (soybeans aren’t the only driver here -- they are only up around 25 percent year-over-year).

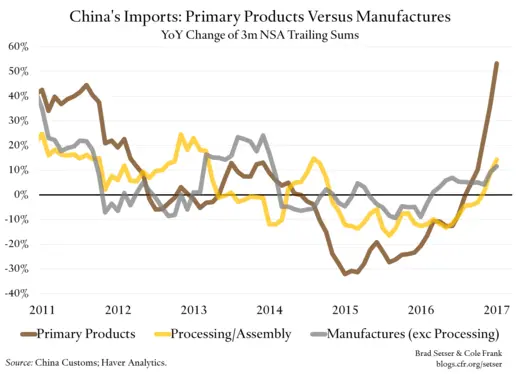

This split in the U.S. data nearly perfectly maps to the split in China’s own data between manufactured imports and primary product (commodity) imports. China’s imports primary products obviously soared in q1, but its of manufactures -- both “processing” imports (imports for reexport) and non-processing imports—manufactured goods for China’s own use—are also up 12 percent year-over-year in q1.

So far, so good even if the rise comes off a low base. Chinese demand clearly has helped re-energize global trade growth this year.

But can it last? Probably not—at least not at the current pace. With China now tightening monetary and credit and perhaps fiscal policy (the line between credit and fiscal policy is thin in China, given than many borrowers are state-backed), it appears unlikely that the current pace of growth in imports will be sustained. China’s April iron ore imports were soft. The April PMI and producer price inflation data in April both point to a slowdown in manufacturing.

And China’s export numbers in March and April were solid. A low base no doubt helps, but I suspect the weakening of the yuan in 2014 and 2015 is also having an impact. China’s surplus averaged $47 billion over March and April—though the trailing 3 quarter sum is held down by February. That is slightly higher than last year’s average monthly goods trade surplus (seasonally adjusted) of around $42 billion. (The surplus was only $30 billion in January then $15 billion in February, in part because of the difficulties getting the seasonal adjustment for the lunar new year right).

With commodity prices down and China’s policy tightening likely to have an impact on import volumes, it looks possible that the (very welcome) fall in China’s overall trade surplus over the last few quarters may be coming to an end.