Lessons from the Ruble’s Dive

By experts and staff

- Published

- Robert KahnSteven A. Tananbaum Senior Fellow for International Economics

My thoughts on the ruble’s collapse are here. Three points to highlight in particular:

The real test of whether sanctions work starts now. I have for some time believed that it would be an upturn in inflation, and a deep recession, that would be the real test of whether sanctions would create conditions for peace, not a move in Russian stocks and bonds alone. That is because it is only now that the broader Russian public is feeling the costs of President Putin’s policies. No doubt the Russian’s searing experience with hyperinflation in 1998 still resonates with the Russian public. History also reminds us of the fragility of confidence. When crisis happens, exchange rates will move far and fast.

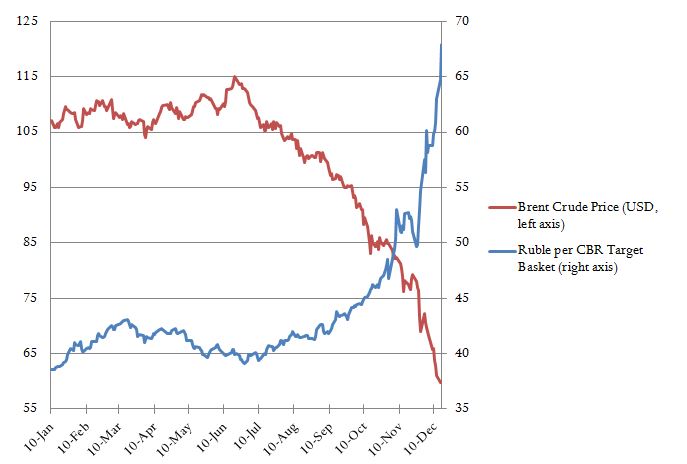

Figure 1: The Ruble and the Price of Crude Oil

Source: Bloomberg; Central Bank of Russia

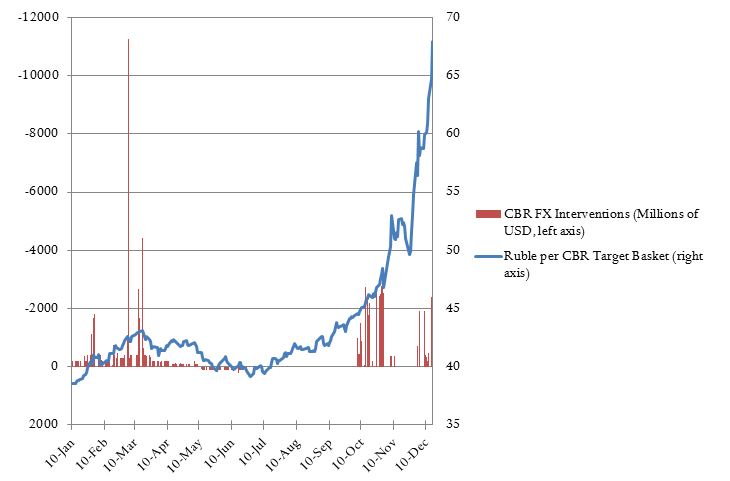

Figure 2: The Ruble and Official Central Bank Currency Intervention*

Source: Central Bank of Russia

*Note that this figure shows only officially reported intervention by the Central Bank of Russia and does not include unreported intervention or intervention carried out by other entities, including the Ministry of Finance.