Will Powell Be an Accidental Hawk?

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Benjamin Della RoccaAnalyst, Center for Geoeconomic Studies

Fed Chair nominee Jerome (Jay) Powell was a logical choice for Fed chair. A business-friendly Republican, he is likely to push forward President Trump’s deregulation agenda in the financial sector while continuing the Yellen Fed’s softly-softly approach to monetary tightening—an approach that has kept markets unusually calm and cheerful. Yet the course on which he’s heading looks more hawkish than he intends.

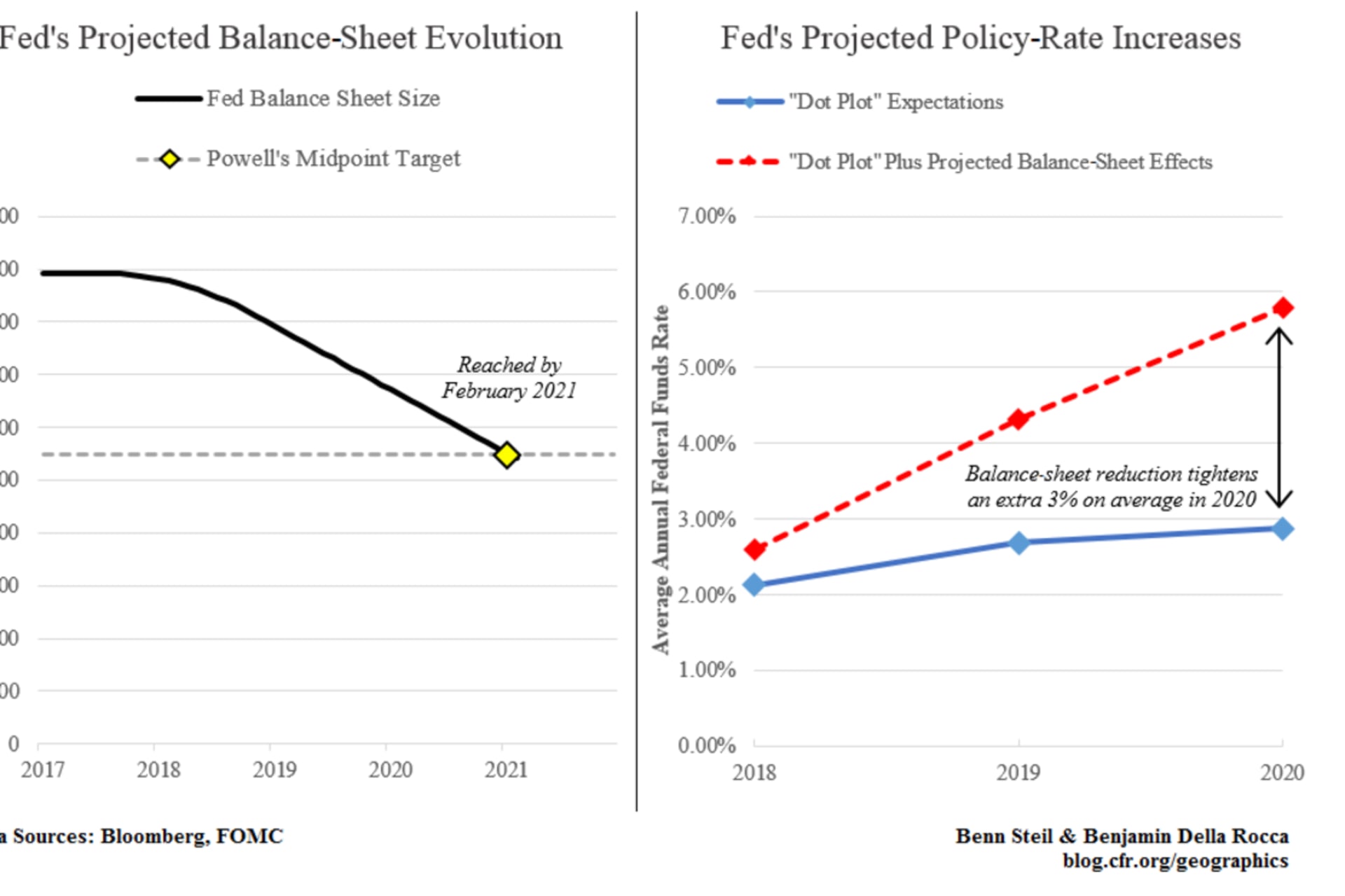

In October, the Fed began implementing a long-term program of reducing its crisis-bloated balance sheet by letting maturing securities run off. Powell sees the balance sheet coming down from a high of $4.5 trillion in October 2014 to a new normal of $2.5-3.0 trillion. Though he offers no timetable, he has emphasized the importance for market stability of sticking to the planned reduction pace, once set. That pace has the balance sheet hitting Powell’s midpoint target in February 2021, as shown in our left-hand graphic above.

Powell considers the roll-off largely inconsequential as a tool of monetary tightening. The effects would be “pretty modest,” he told CNBC—“a few basis points here and there.” Powell’s colleagues on the Federal Open Markets Committee (FOMC), as well as the markets, seem to agree. The Fed announced its plans for balance-sheet reduction back in June. Yet the “dot plot” rate projections of FOMC members have hardly budged since the end of last year. Likewise, market estimates of the effective federal funds rate through 2019 have moved little from pre-announcement levels, and in fact have risen slightly.

We think the Fed and the markets have gotten this wrong. Using Fed economists’ own estimates of the effect of central-bank asset purchases on 10-year Treasury yields, we calculate that balance-sheet reduction at the announced pace is equivalent, in its effect on boosting end-2018 10-year rates, to a one percent hike in the Fed’s policy rate. The logic is explained in our recent Business Insider piece.

Our math also suggests that between now and February 2021, when the balance sheet is projected to shrink to Powell’s midpoint target, asset run-offs will produce a tightening in monetary conditions approximately equivalent to a 3.5 percentage-point increase in the Fed’s policy rate—as shown in the right-hand figure above. This impact is so large that the Fed would be obliged to push the policy rate back down to zero in order to effect the degree of tightening that its dot plot now indicates as appropriate.

The bottom line is that, unless Powell changes his mind on keeping balance-sheet roll-offs on auto-pilot, policy rates will not only rise more slowly than expected but are likely to start falling by 2020.