Finding China in the U.S. TIC Data

A technical post with an important update to my estimate of China’s true holdings of U.S. bonds.

The joint G7 decision to sanction Russia’s reserves after the invasion of Ukraine clearly had a significant impact on China.

Some say that it led China to diversify out of the dollar. I have doubts.

Yes, there was an increased bid for gold from the PBOC. But that bid was, judging from China’s disclosed data, marginal.*

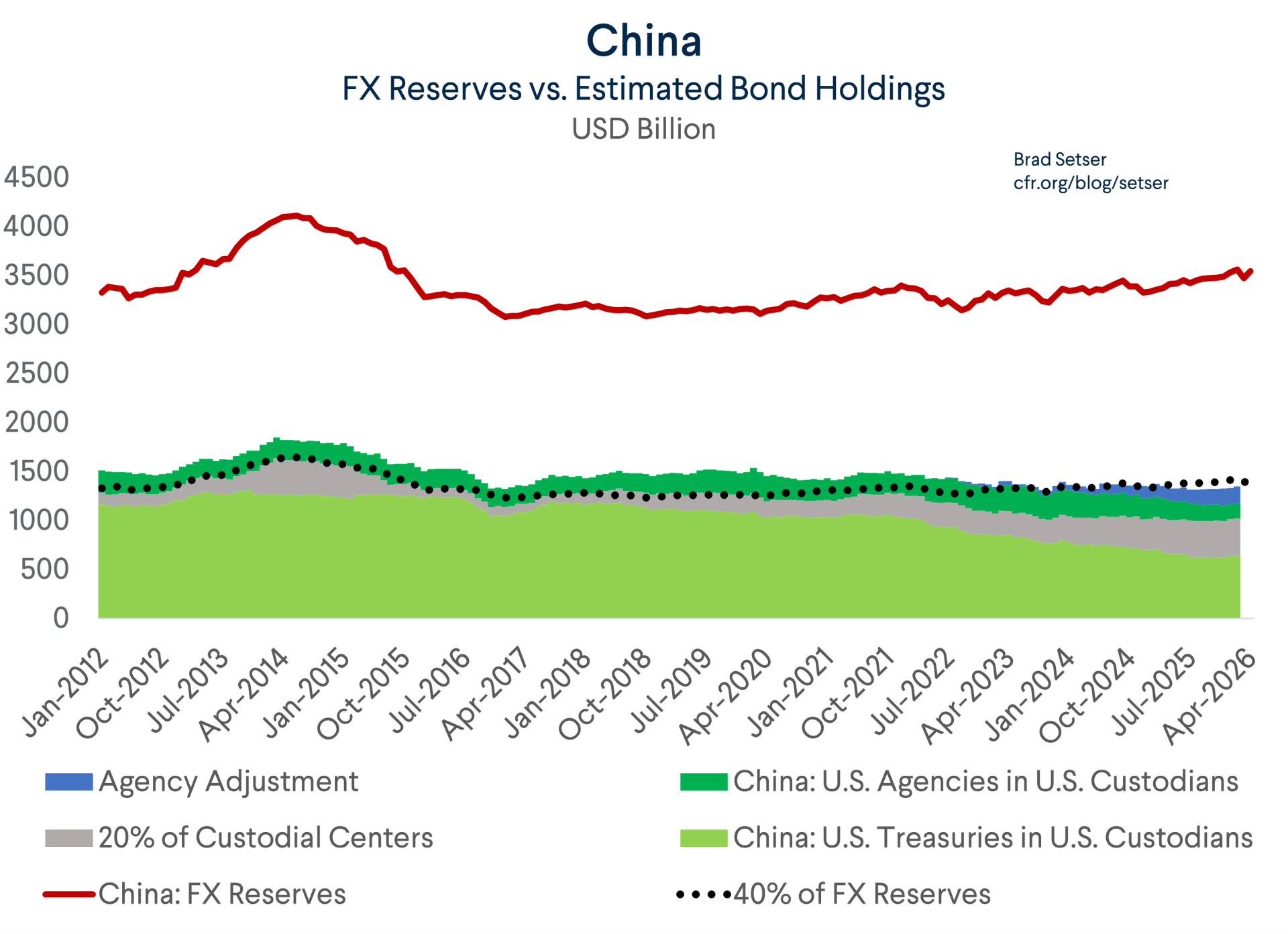

China hasn’t disclosed the currency composition of its reserves since 2020. But it isn’t clear that China’s central bank has shifted its currency composition of its foreign currency holdings around a lot, in part because the dollar share of its reserves was already low (55 percent) and going underweight the dollar means losing yield.

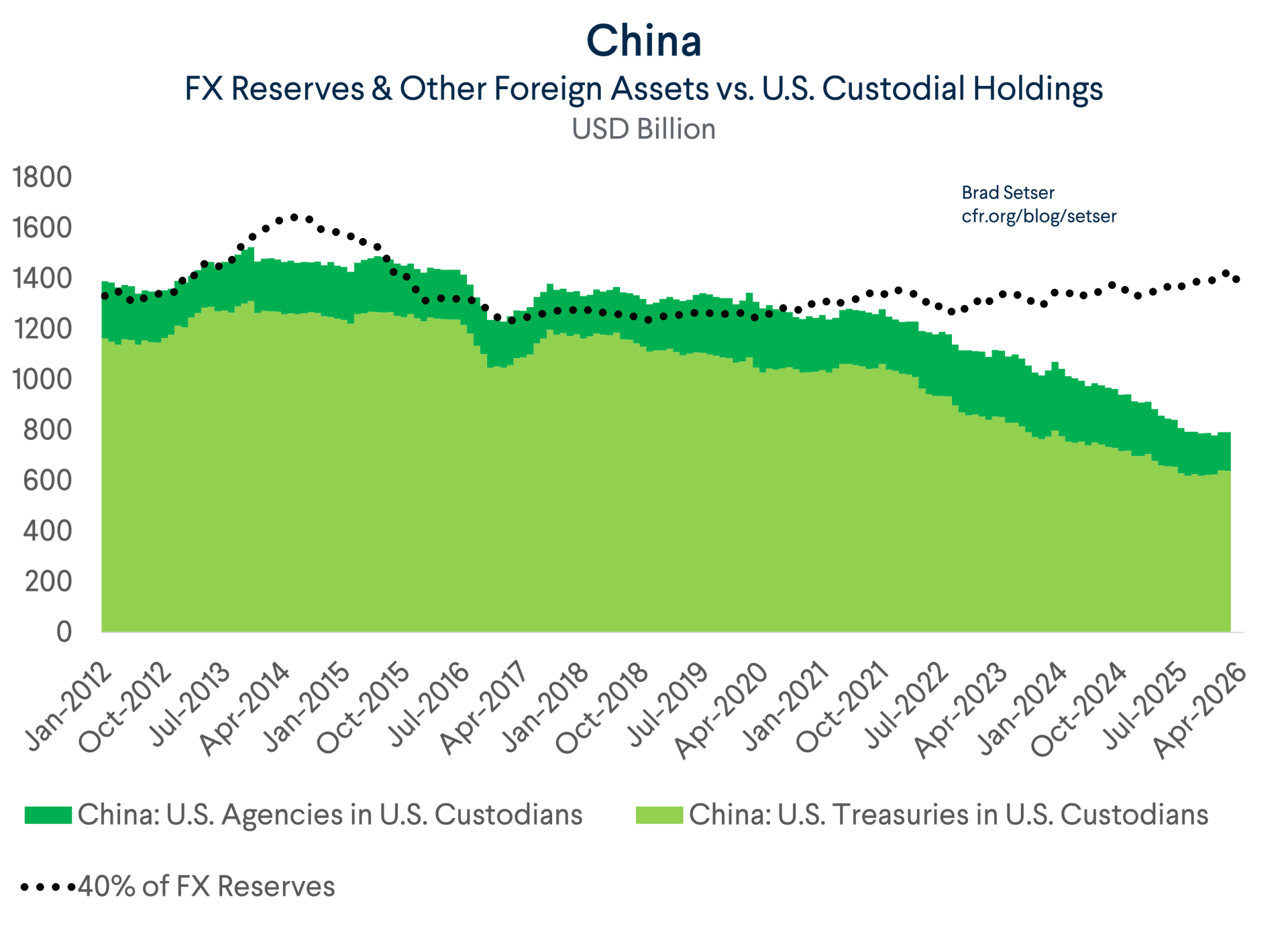

But there is no doubt that China’s holdings did start to disappear from the U.S. data right after the G-7 immobilized Russian reserves in early 2022. There is a clearly fall around this time in the bonds China holds in U.S. custodians.

This often is reported as a move out of the dollar—but it need not be.

There are lots of ways of holding U.S. dollars indirectly through non-U.S. custodians.

The hard part is estimating just how many bonds China holds through the various custodial and financial centers around the world. That is, of course, the subject of this blog.

Estimating China’s true holdings of U.S. assets has gotten harder because it seems like China has diversified not just out of the US, but also out of Euroclear (a large Belgium-based custodian). Its holdings in Belgium were a bit too obvious, and the Euroclear custodial arrangement turns out to be punitive to a sanctioned central bank.

The Origins of the “Belgium Adjustment”

The initial attribution of the bulk of the Treasuries held in Euroclear’s custodial account to China was based on three factors.

First, Belgium entered the data in a strange way. Back during the days of a separate transactions data series, there were almost no direct purchases of U.S. bonds by Belgian entities. Treasuries that ended up in Belgium were all bought in other jurisdictions (London, Paris, sometimes Hong Kong) and then moved to a Belgian custodian. That mapped to the fact that China never appeared cleanly in the purchases data; many of its U.S. holdings also didn’t appear in the transactions data either.

Second, SAFE has an equity stake in Euroclear, which always seemed like a hint.

Third, Belgium’s holdings didn’t move with the other custodial centers, but did move with China’s reserves.

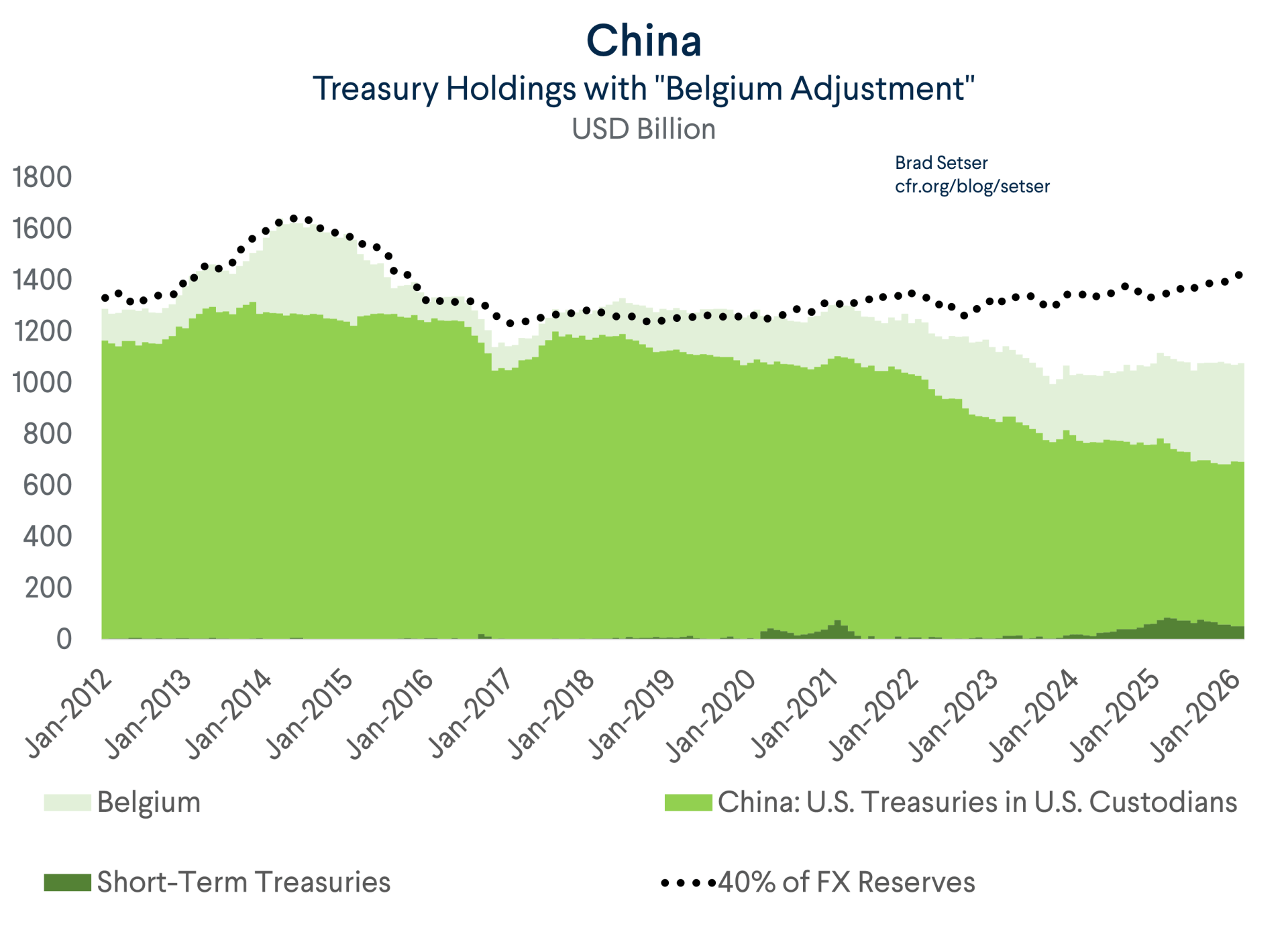

In fact, the adjustment for “Belgium” is essential to get a good fit with changes in China reserves in 2015 and 2016, as the Treasuries in Euroclear were sold before the Treasuries in U.S. custodians.

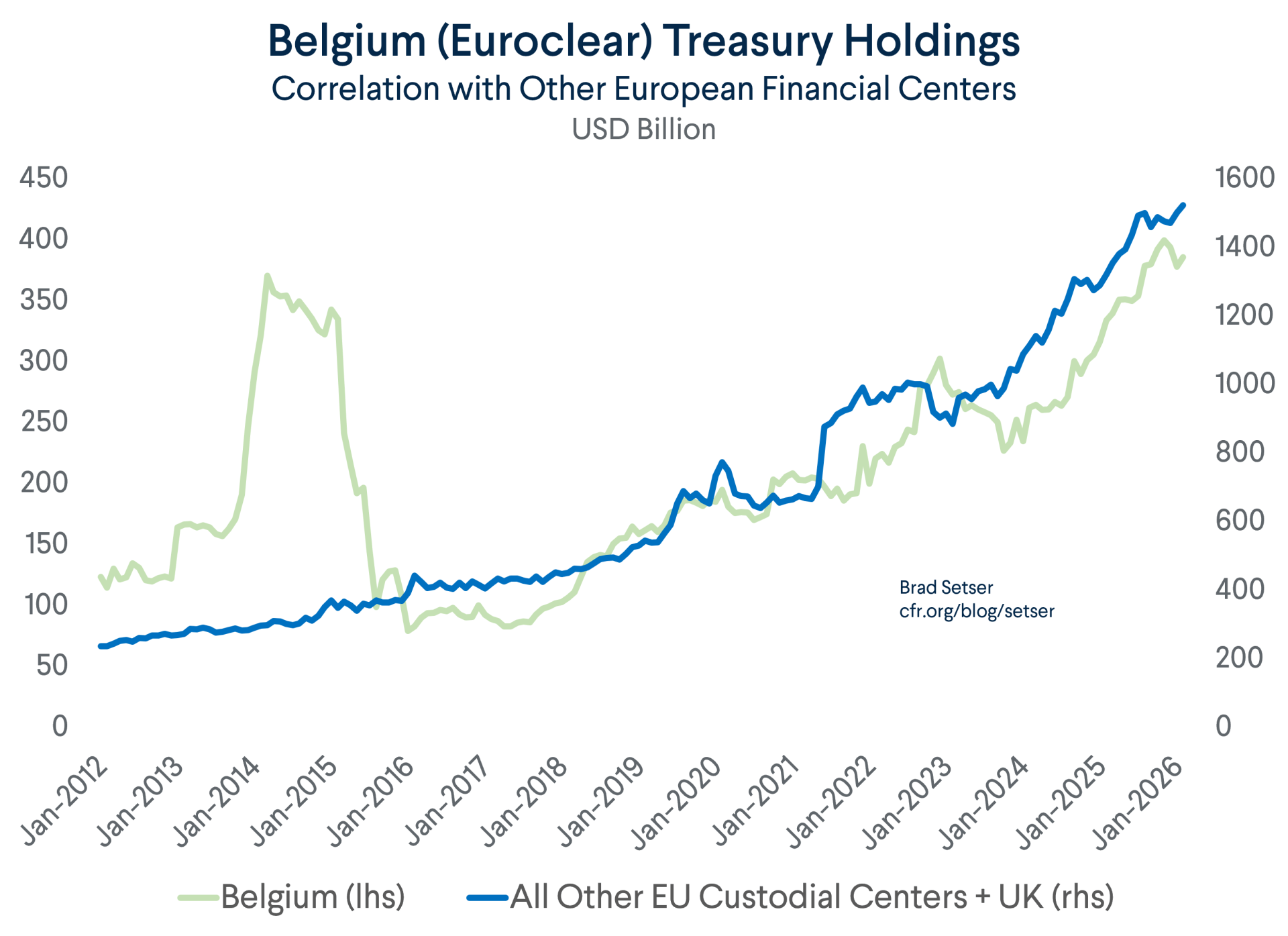

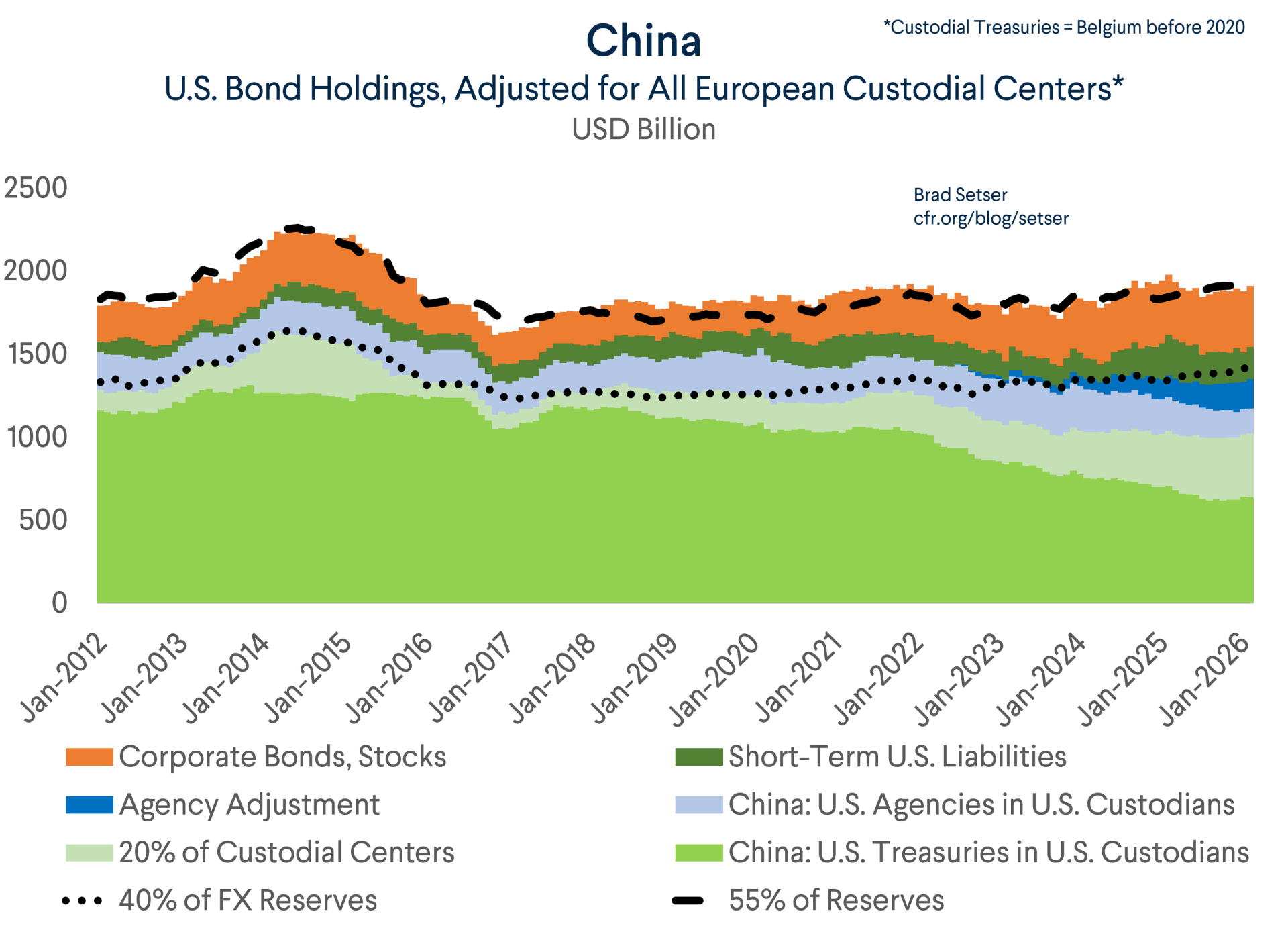

But the attribution to Belgium is now stale. It is essentially based on data from 2010 to 2016. In recent years there has been no real difference between the movement of Treasuries held in Belgium and Treasuries held in other European financial centers.

A new Model for China’s Treasury Holdings—Using all European financial centers

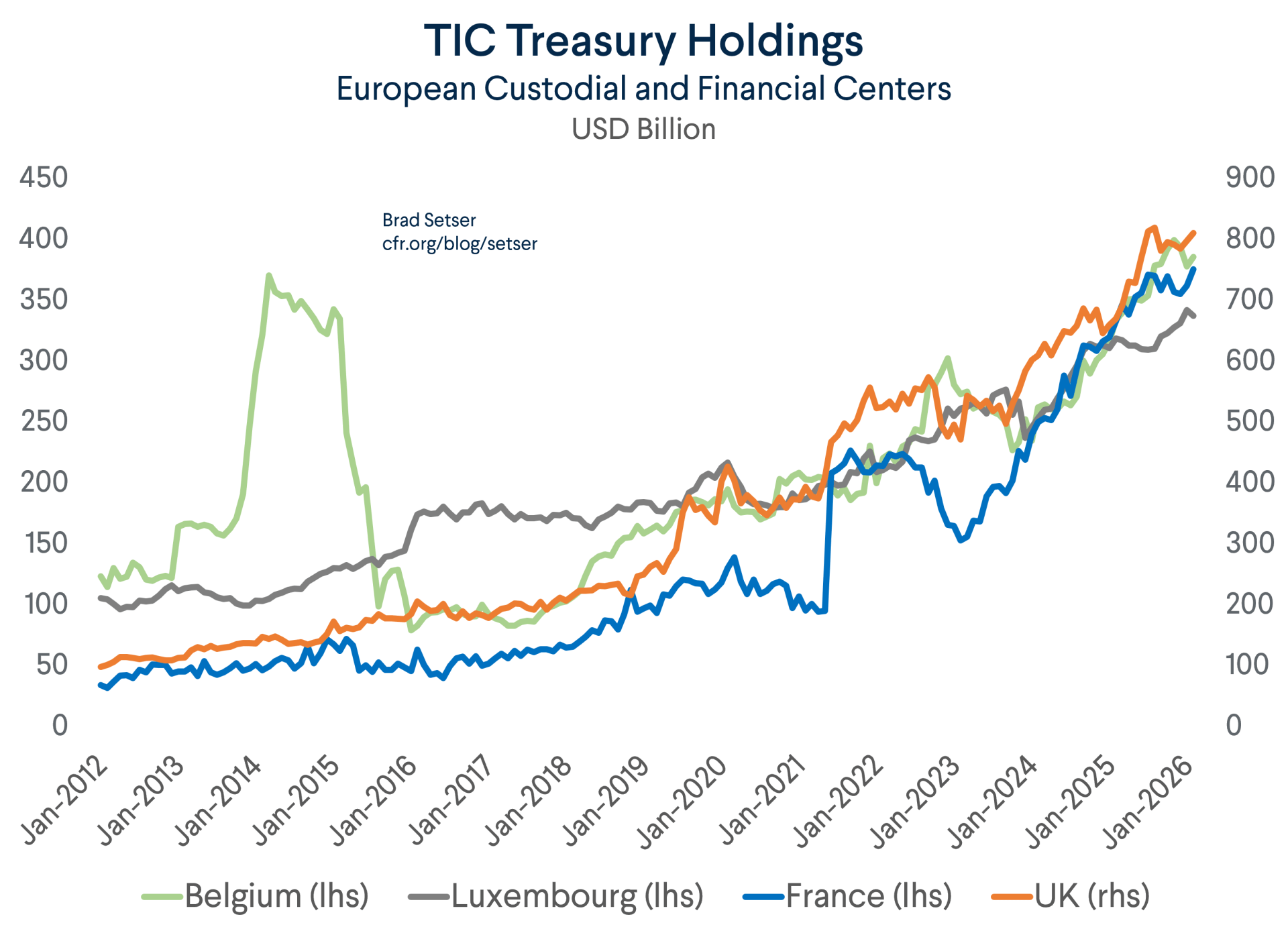

Since 2020 or so, there has been a huge increase in the Treasuries held in custodians in the UK, France, Luxembourg, and Belgium. Ireland of course also holds a lot of Treasuries too, but those are thought to the assets of U.S. firms that use Ireland as a center of tax avoidance.

The rise in the Treasury holdings of a broad set of custodial centers hints that China could now be using a broader set of custodians. It certainly has a reason not to just use Euroclear (Belgium) these days. The freeze on Russia’s reserves not only put Euroclear in the news but it also highlighted a specific risk to holding assets that could be frozen in Euroclear: Euroclear doesn’t pay interest to the owner of a frozen asset after a bond in its custodial account matures; the funds just roll into a zero-interest deposit account.

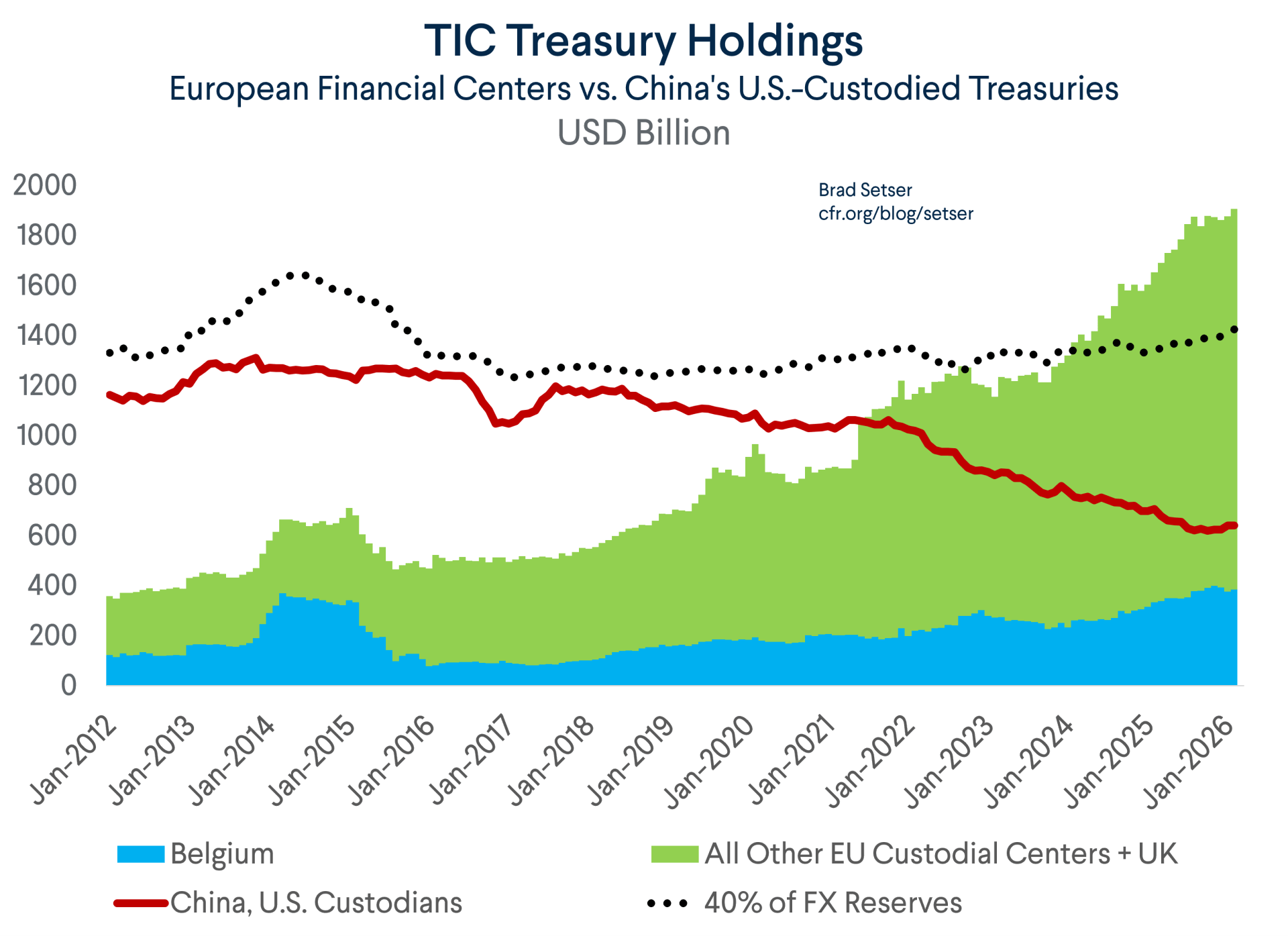

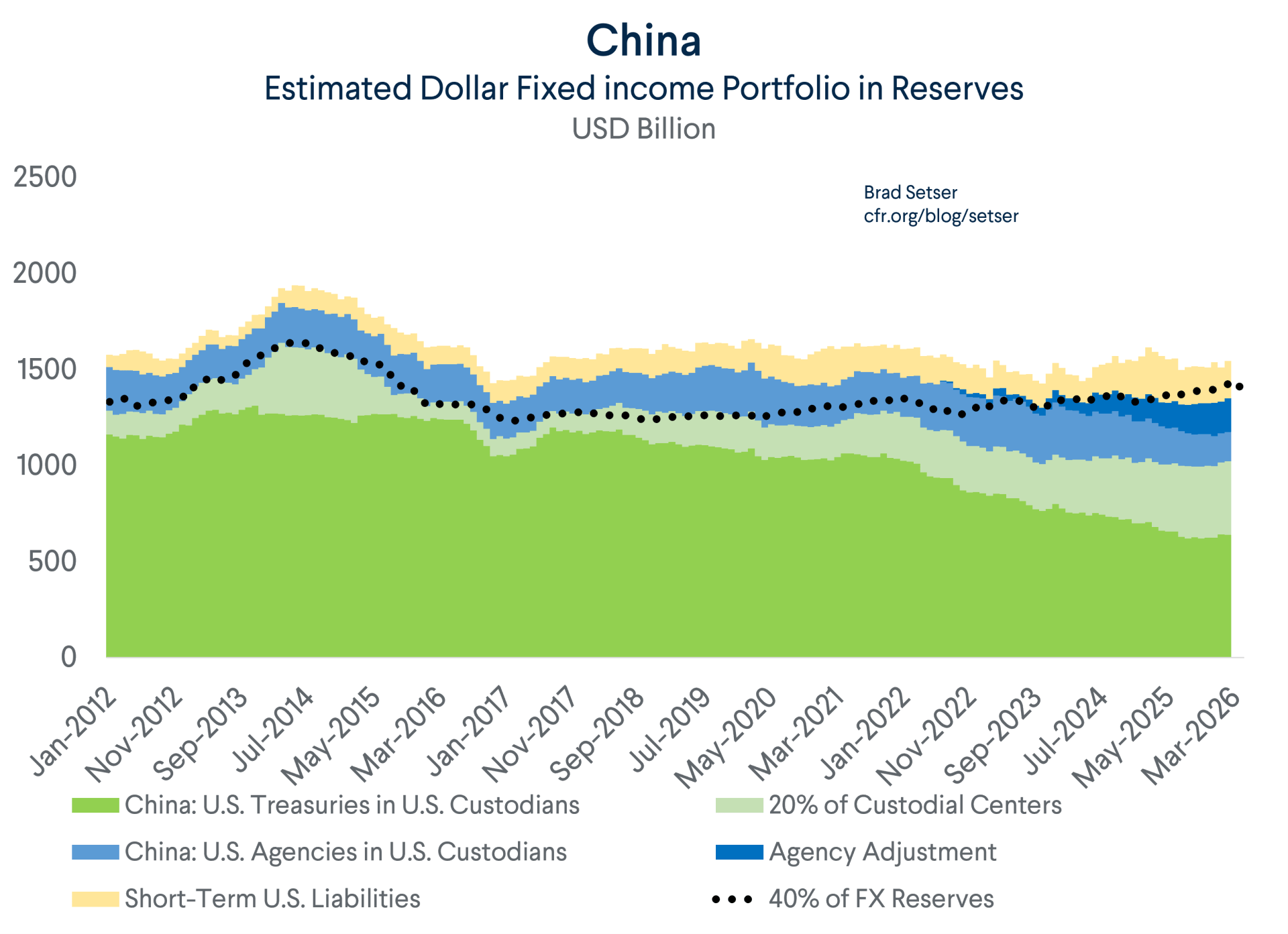

It would be easier to attribute some of the rise in the holdings of these custodial centers to China is China’s reserves were rising and the rise in reserves could be matched to the rise in custodial holdings of a particular center (as with Belgium from 2010 to 2014). But now the match is more complicated as China’s reserves are basically flat (the rising foreign assets of the state banks do not tend to appear cleanly in the U.S. data). In order for the pieces of the puzzle to fit, there should a rise in the holdings of the custodial centers that offsets the gap created by the fall in Treasuries in U.S. custodians relative to China’s reserves.

And since all the custodial centers are now moving together, any one of the centers could be helping to fill that gap.

It turns out that Belgium is around 20 percent of the total Treasuries held in the main European custodial centers other than Ireland (France, the UK and Luxembourg). As a result, changing the custodial center adjustment from “all long-term holdings in Belgium” to 20 percent of the Treasuries held in Belgium, Luxembourg, the UK and France—with the new adjustment starting during the pandemic—doesn’t change China’s total estimated holdings much.

The new methodology though does indicate a lower level of confidence in the adjustment, and thus a higher probability that Treasuries held by non-U.S. custodians for Chinese state investors could be somewhat smaller or higher than this calculation assumes.

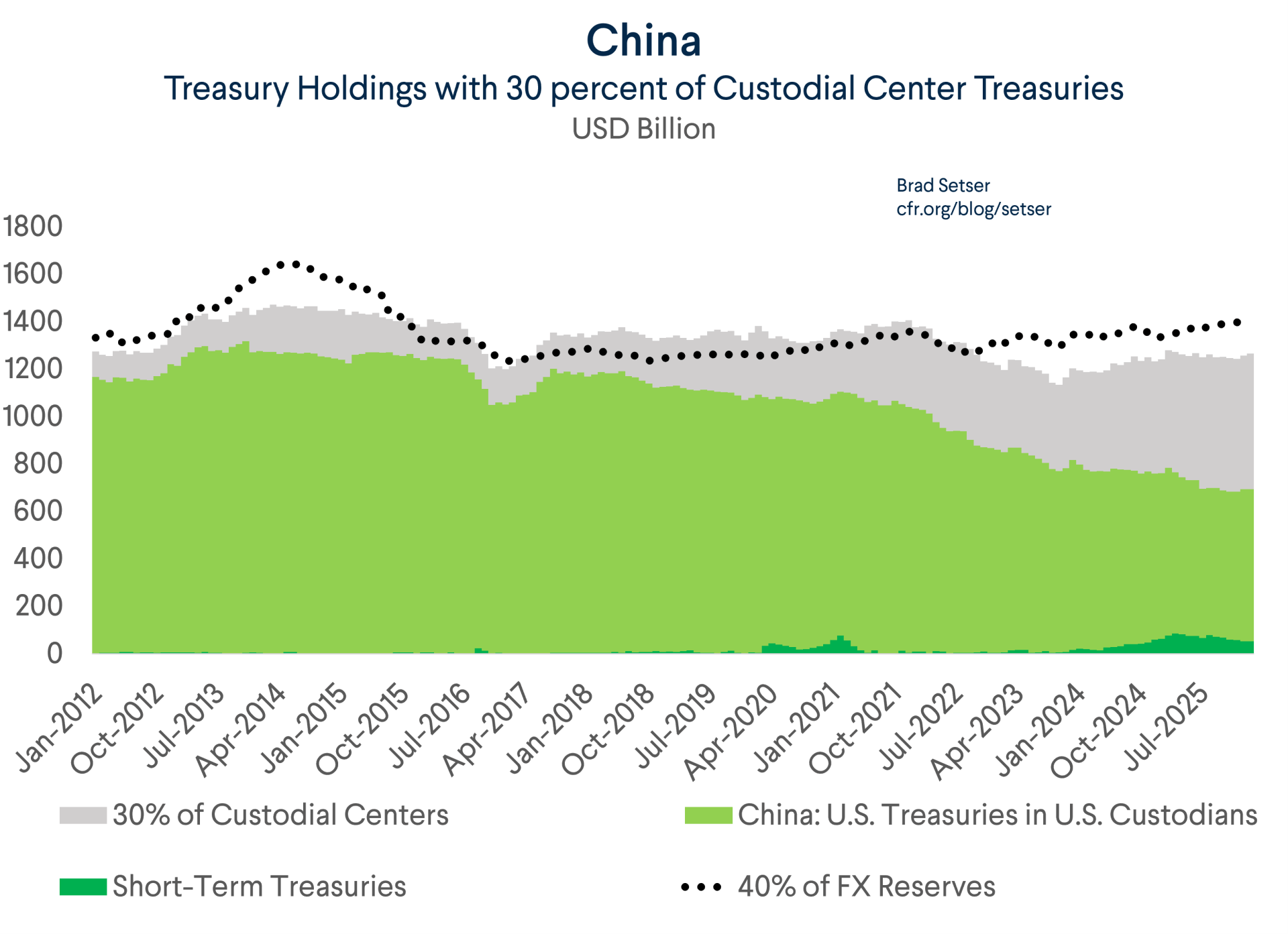

To highlight this point, look at a plot with 30 percent of the holdings in all the custodial centers attributed to China. It looks different than the Belgium-only adjustment I used to use both in the 2010 to 2016 period and now.

As an aside, it wouldn’t matter if the UK were removed from the estimate on the grounds that the UK’s big Treasury holdings reflect basis trades and other relative-value trades by London-based hedge funds and similar financially driven flows. Belgian, Luxembourgeois and French holdings have all moved together.

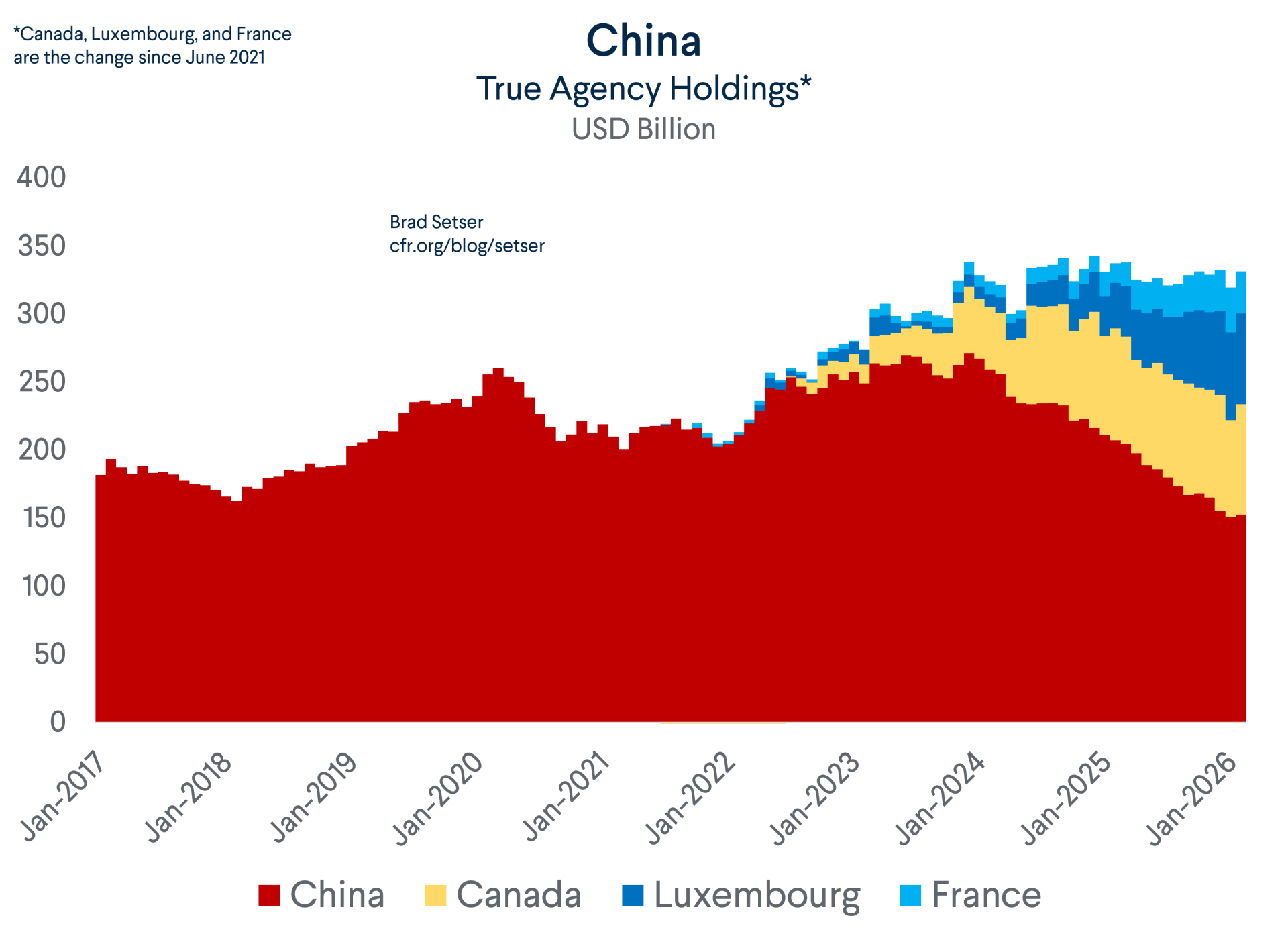

Oh, Canada: China’s Hidden Agency Book

In the past, I didn’t adjust China’s reported holdings of Agencies in my benchmark estimate of China’s U.S. holdings. But though needs to change.

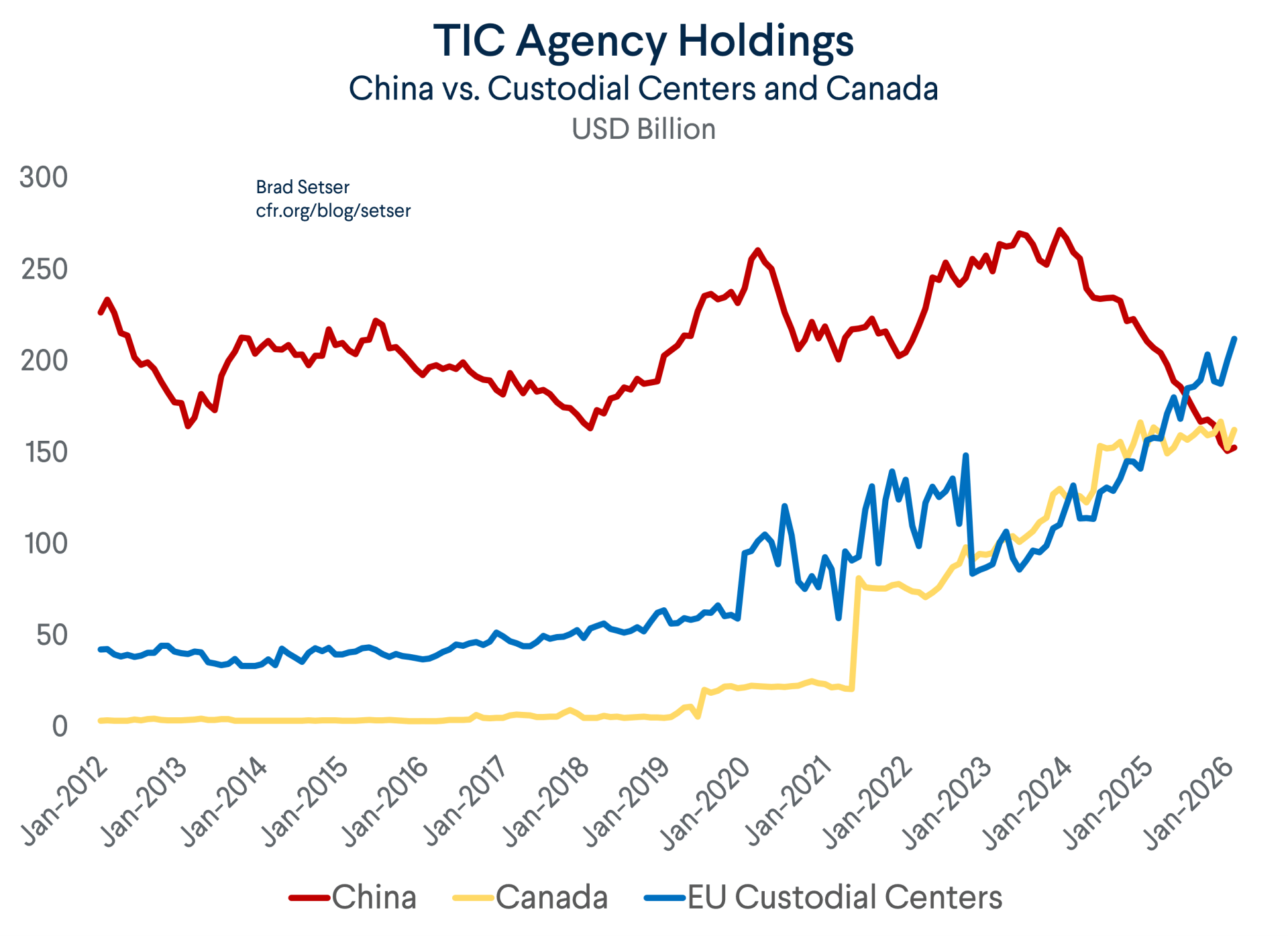

China’s holdings of Agencies in U.S. custodians stopped rising in early 2022 and really started to fall after the end of 2023. They now stands at around $150 billion, down from a recent peak of over $250 billion.

And there have big, and some surprising, changes in the rest of the Agency custodial data since the pandemic.*

For one, Canada—or someone using a Canadian custodian—took a sudden interest in Agencies around 2020. There was a big jump in the June 2021 annual survey, and Canadian holdings continued to rise through 2024.

There were also substantial rises in the Agency holdings of Luxembourg and France in 2024 and 2025, as well as some strange moves in the UK that drove the European data from 2020 to 2022.

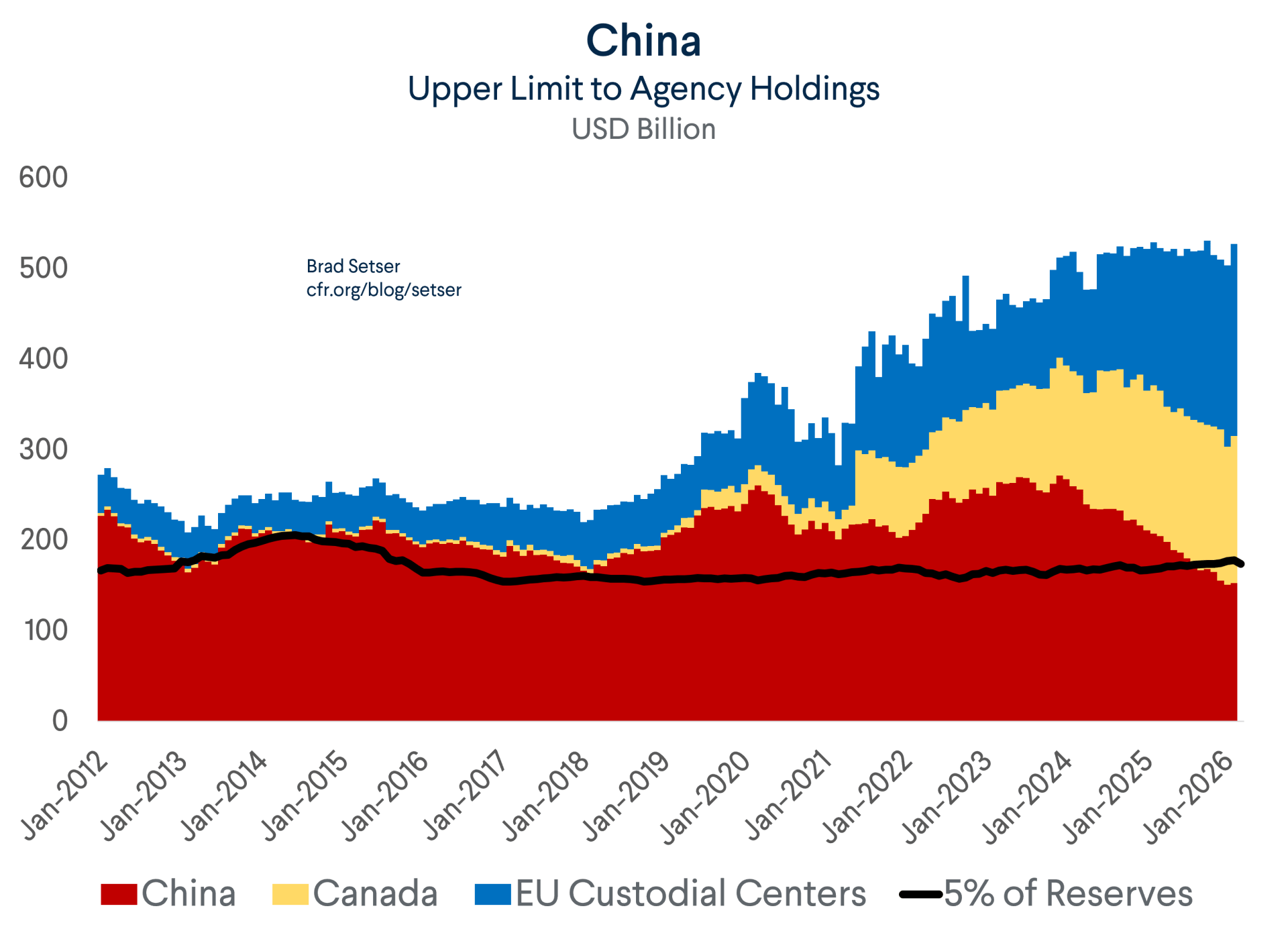

Sum up China’s holdings with the holdings of Canada and the European custodial centers* and an upper-end estimate for China’s true Agency holdings could be as high as $500 billion.

That seems a bit too high. Unless there has been a really big shift out of Treasuries or some other shift in the underlying data, this would imply that China’s dollar share is going up, not down (the other logical possibility is that China’s state banks have started to appear in the data).***

A more modest adjustment just looks at the change in Canadian, Luxembourgeois, and French holdings since 2022 or so. That puts China’s current holdings at around $300 billion.

This is as much an art as a science.

I am focusing on countries whose Agency holdings jumped suspiciously around the time China’s holdings started to fall (just as Belgium’s holdings jumped once the U.S. custodial data got more attention), together with the surprise rise in Canadian holdings over the last five years, and using that jump to make an estimate of what China’s actual portfolio might be. And to make the chart look smooth I left out the big jump in French and Canadian custodial holdings in June 2021. Add those in and China’s holdings jump by around $70 billion, to close to $400 billion.

And full disclosure: I got a tip from a market insider who suggested that the rise in Canada’s holdings was rather suspicious.

The overall result suggests that China has reduced the share of its portfolio in long-term Treasuries, while increasing its bill holdings and maintaining a sizeable Agency portfolio of around 10 percent of total reserves (more than before 2020).

Zooming in on the chart in highlights that the key implication of this upward adjustment to China’s estimated holdings of Agencies is that China’s total U.S. financial holdings remain between 50 and 55 percent of it reserve portfolio.

The error band is conscious; I don’t have a good estimate of the portfolio equity holdings of China’s sovereign wealth fund that are managed in-house and could bleed into the U.S. TIC data, and attributing all the visible equity holdings to SAFE is a stretch.

The bigger story, of course, is that China’s true holdings of U.S. bonds cannot be assessed by just looking at the “China” line in the TIC data. Both the Treasury and the Agency portfolios need to be adjusted for the bonds that China keeps on custody in Canada and in Europe.

That adds to uncertainty around the estimate, as it seems likely that China is now using multiple non-U.S. custodians to mask its true holdings.

But it doesn’t make it any less necessary to try to do an adjustment, and not to take the now predictable falls in the bonds that China holds in U.S. custodians as evidence that China is abandoning the dollar.

* The PBOC balance sheet data suggests only a bit over 10 million fine troy ounces in gold purchases; most of the reported increase in gold holdings is from the rise gold prices. Of course, many suspect that China isn’t disclosing all of the gold now held by the central bank.

** Neither Canada nor Europe (or rather investors using U.S. custodians) have historically been big holders of Agencies. The big buyers abroad were in Japan and Taiwan—and of course China. Korea was a smaller player in the market. Agencies have appealed to both large reserve managers and Asian life insurers looking for a bit more yield than available in either their local bond market or in U.S. Treasuries.

*** The large dollar portfolios of China’s state commercial banks have never appeared cleanly in the U.S. data for a host of reasons—not the least of which is that they don’t have access to the Fed’s custodial facilities. It it possible that some of their $400 billion in foreign securities holdings (per the Chinese banking data) could be bleeding into the custodial data now. But their biggest market impact has been indirect, as a source of funding for global investors, including hedge funds, that buy and hold Treasuries as one leg in a basis or swap-spreads trade. Both trades require holding large quantities of cash bonds, and thus large amounts of funding. And Chinese bank claims on other banks have been rising.