Petrodollars: Myth and Reality

Global dollar liquidity is driven far more by Asian manufacturing surpluses than by oil exporters stashing dollars away offshore. The glory days of the petrodollar are over.

The foundation of the dollar’s global role, it is sometimes argued, rests on the willingness of the Gulf countries (but not Russia) to price their oil in dollars.

But it was never quite clear why oil pricing mattered quite as much as some claim.

To be sure, there are network effects around dollar pricing. But it isn’t hard to pay for oil in a global currency like the euro, even if the underlying contract is priced in dollars. There is a deep and liquid market for converting euros into dollars, and a firm aiming to lock in the euro price of oil 3 months forward can buy oil forward in dollars and dollars forward with euros, thereby locking in a euro price.

Dollar settlement is a problem for countries that are sanctioned by the U.S. and the EU and for frontier economies that cannot settle their oil bill in local currency, but it hasn’t required most European oil importers to build up big stocks of dollar reserves just to pay for oil.

What has mattered at times is how the big oil exporters manage their surplus funds when there is a surge in the global price of oil.

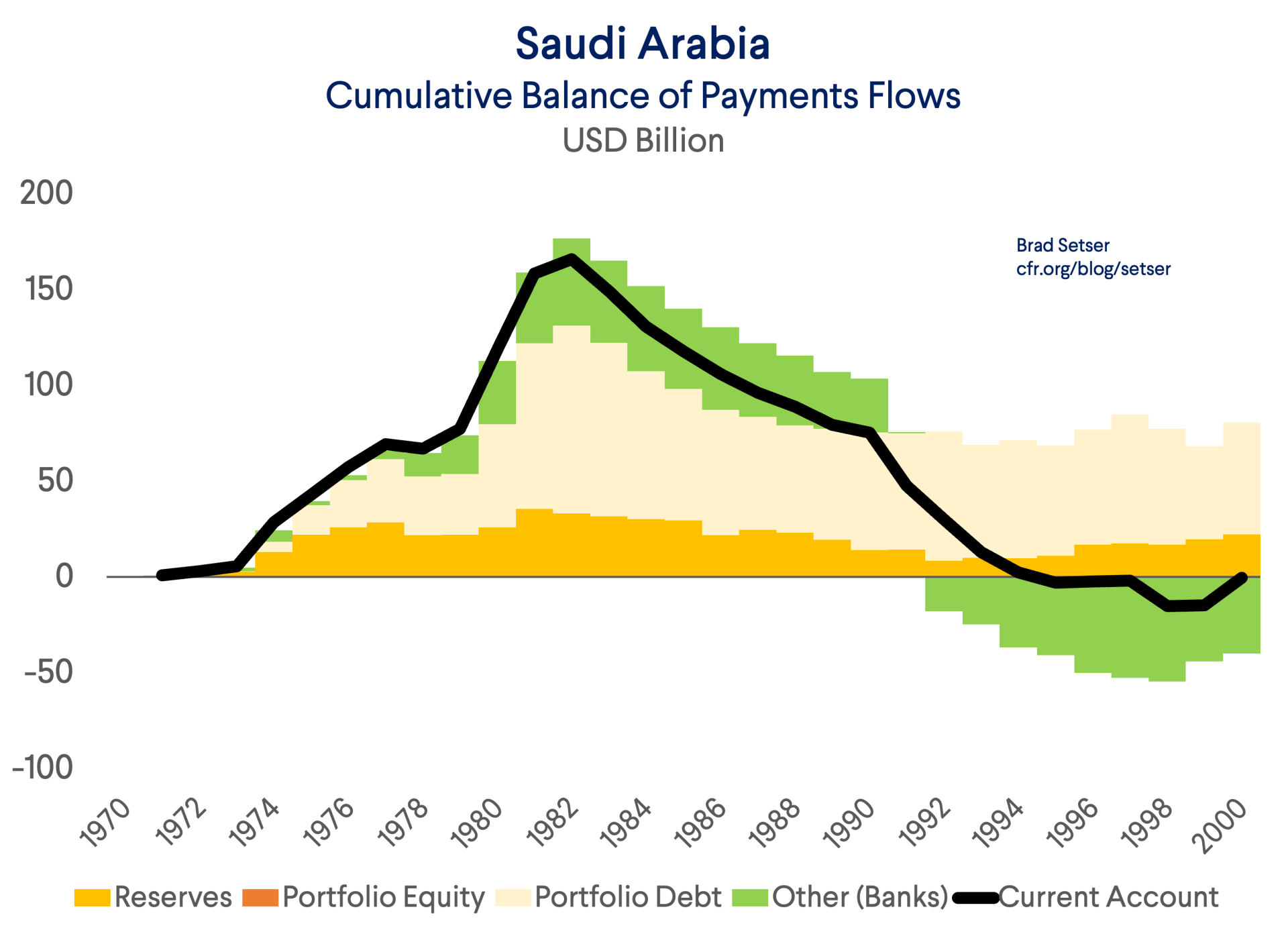

Petrodollars emerged back in the 1970s, when the oil exporters of Gulf—flush with oil proceeds after the price of oil tripled in the early 70s—placed their dollar proceeds on deposit in the big international banks and (secretly) bought Treasury bonds. Those dollars were in turn lent out, often to Latin American economies. Petrodollar recycling through U.S. banks became big business.

This set the foundation for the debt troubles of several Latin American economies once dollar interest rates soared and the payments on their floating rate dollar loans became untenable.

Over time, the dollars that the oil exporters held in the global banks fluctuated. In the early 1980s, the Saudis had to severely reduce their oil production to keep prices up. During the years after 1981, the Saudis ran current account deficits, financed by drawing down on surpluses accumulated in the 1970s.

And many of the wealthiest oil exporters in the Gulf set up investment funds—now called sovereign wealth funds that took their surplus dollars out of the global banking system and put them into global equity markets.

What we know is that by 2000—after the Asian financial crisis pulled global oil prices down—the cumulative Saudi current account since 1970 was in balance. Surpluses early on were offset by later deficits. Bank flows (imperfectly measured) turned negative in 1990, during the first Gulf war.

The Russians were obviously out of cash too, and famously defaulted in 1998.

The only real surpluses were in the smaller Gulf kingdoms that were never paragons of financial transparency—partly because the line between royal funds and sovereign funds was long blurred.

Yet the myths around petrodollars persisted long after they had lost most of their substance: the 1970s deal between Saudi Arabia and the United States to price oil in dollars never dictated the accumulation of dollar reserves in East Asia, and it should be clear by now that the U.S. commitment to defend the Saudis is based on much more than dollar pricing of oil.

The second era of “petrodollars” started with the surge in oil prices that accompanied China’s fast growth across most emerging economies in the years before the global financial crisis.

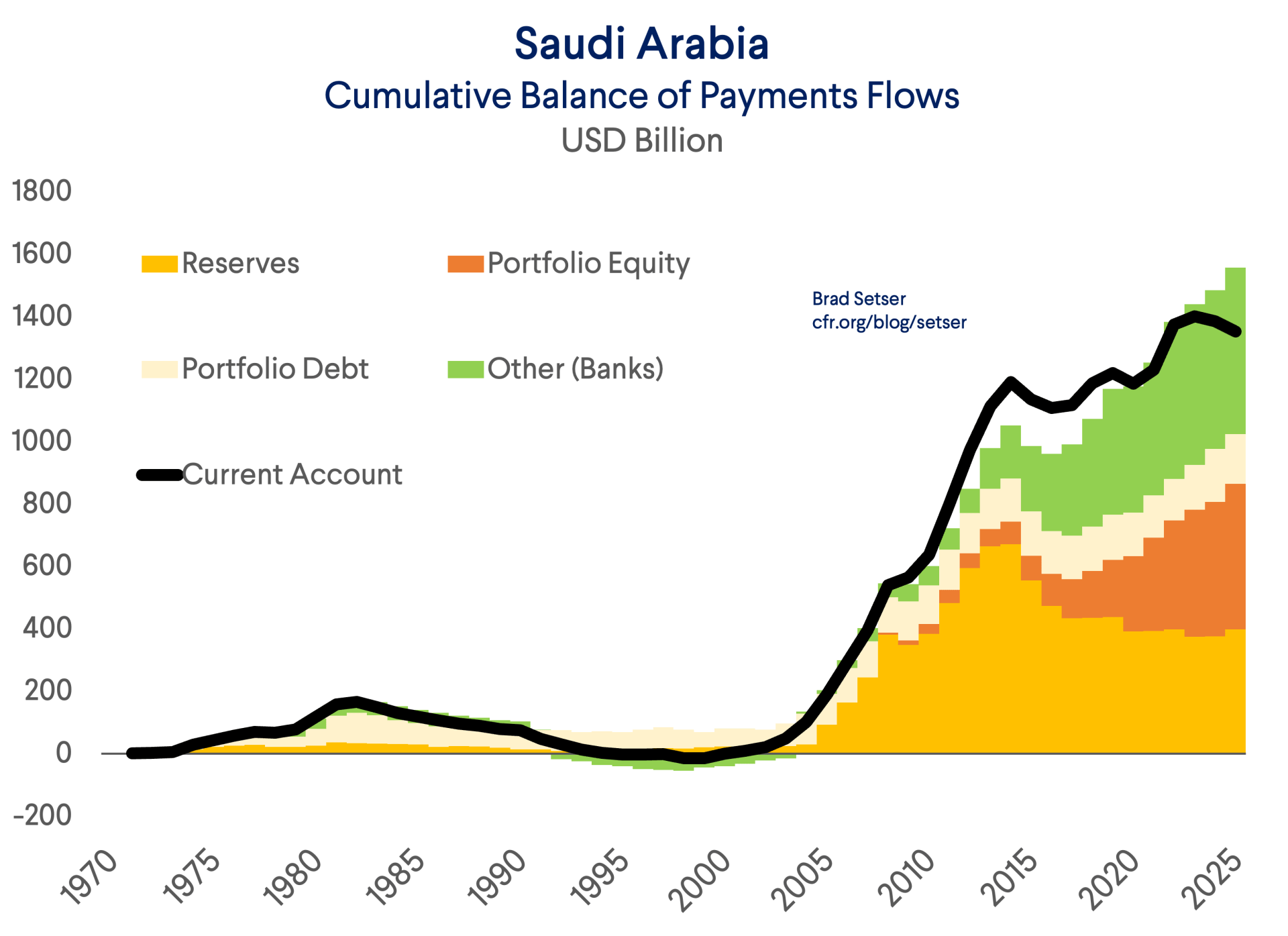

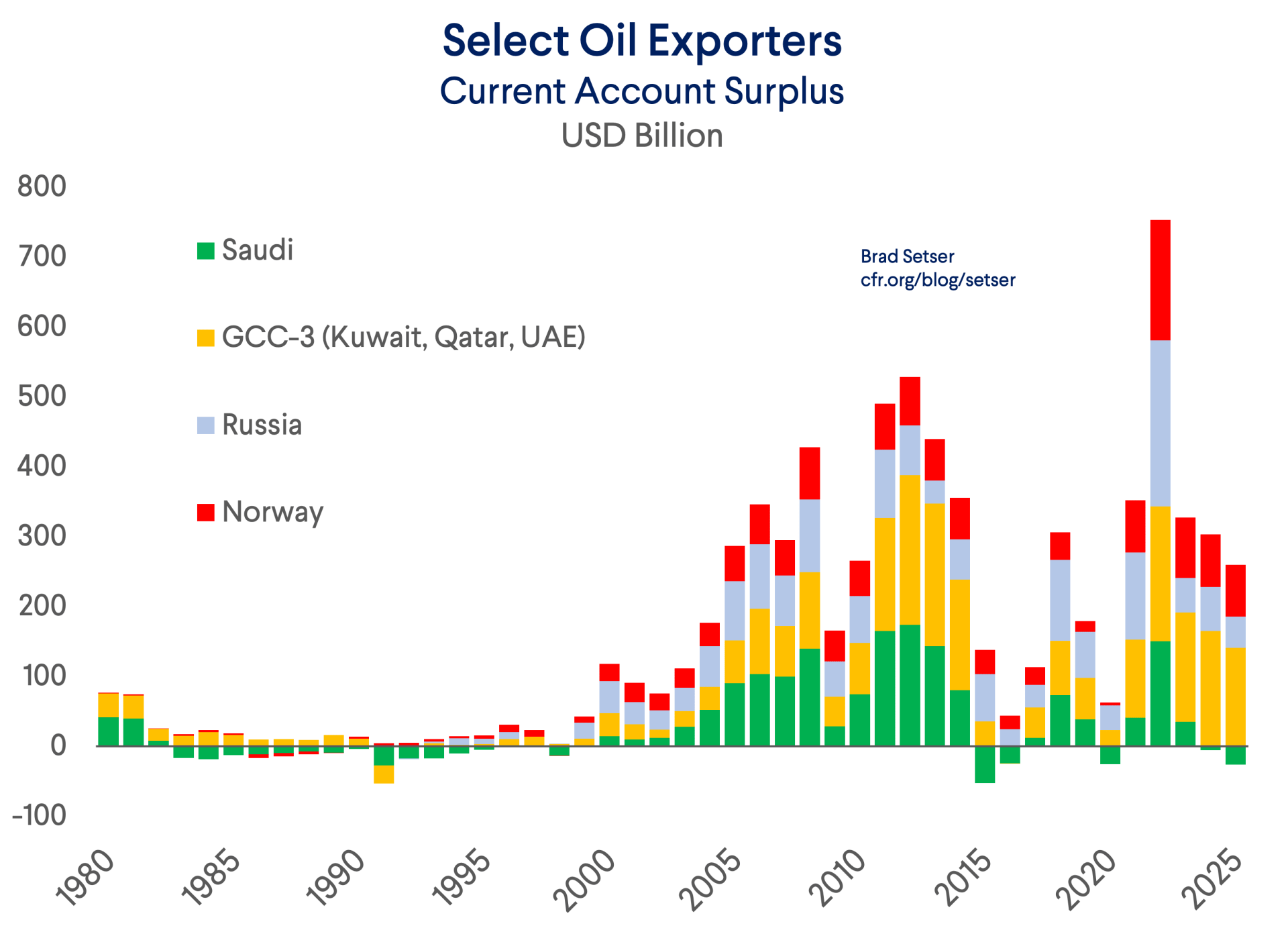

Oil exporters who had adjusted to sustained $20 a barrel oil racked up enormous surpluses as oil soared to over $100—with the Saudis serving as the best example. The cumulative Saudi surplus between 2005 and 2015 topped $1 trillion.

Not all those dollars flowed through the global banking system, but a lot did (look at dollar deposits from central banks in the global banking system over this period; they rose from $260 billion at the end of 2002 to close to $800 billion at the end of 2007 before plummeting during the crisis).

There was plenty of money flowing into classic reserve assets (Treasury and Agency bonds), as well as classic sovereign wealth fund assets (equities and private equity).

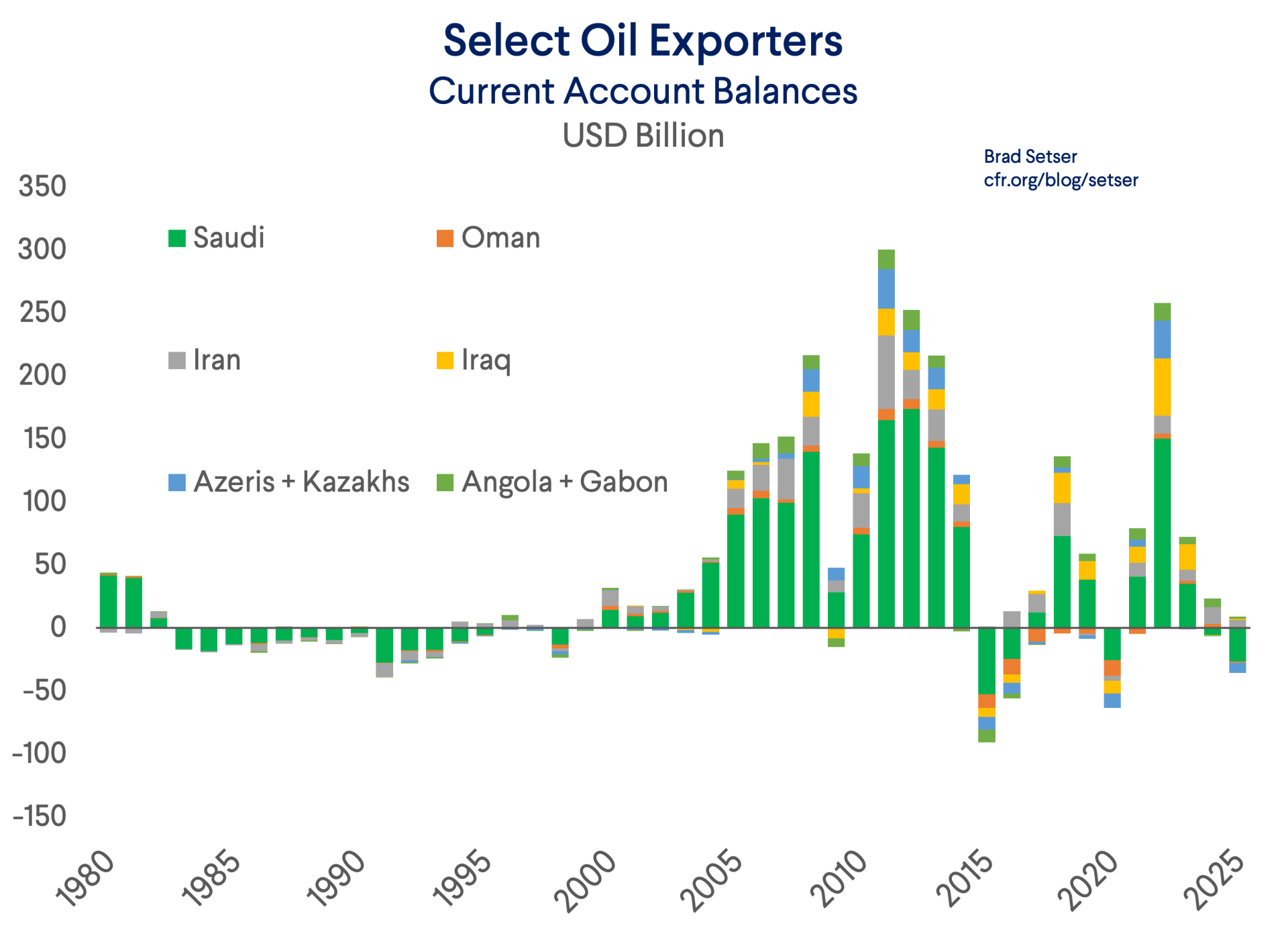

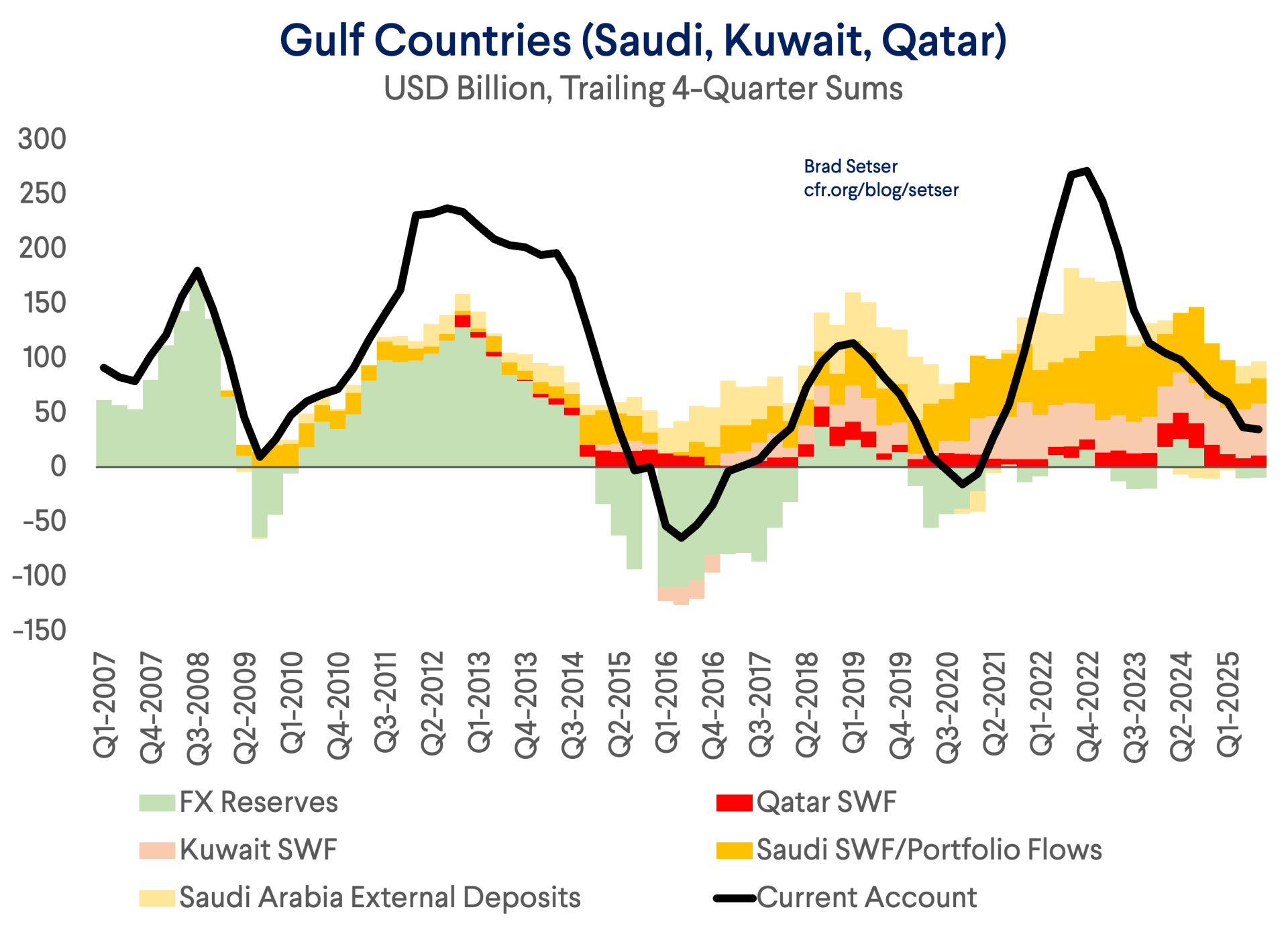

While transparent economic data has never been a forte of the GCC countries, over time some of the oil exporters started reporting quarterly balance of payments data that makes it possible to track a decent portion of the core flow out of the GCC into global markets.

The Saudis started reporting quarterly data in 2009, followed by Qatar in 2011, and Kuwait in 2012.The main exception is the UAE, which barely even produces any annual balance of payments data anymore.

The Russian data also used to be good, but sanctions have since gotten in the way.

And are a few other big oil and gas surplus countries with excellent data, with Norway being the most significant.

As a result, we more or less knew three things going into the current oil shock:

First, the Saudis, along with most other oil exporting economies, weren’t running current account surpluses going into the latest oil shock. The Saudis actually have run deficits in 2024 and 2025.

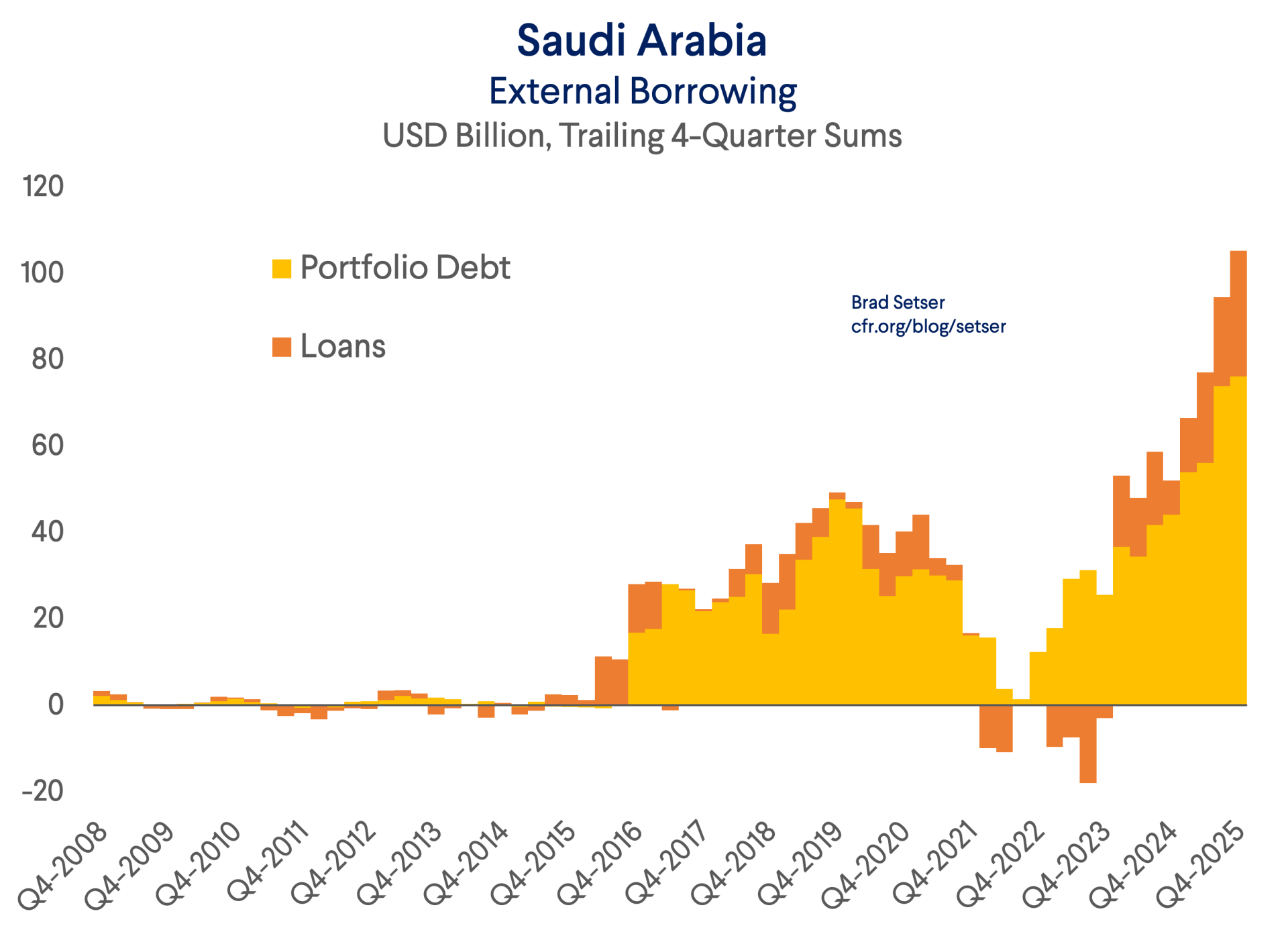

The Saudis were thus a net drain on the liquidity of the global banking system; Aramco, the Public Investment Fund (PIF) and the Kingdom itself have been significant issuers of international bonds. Those funds covered domestic investments and the Crown Prince’s desire to build a sovereign fund with a global equity portfolio that matched those of his neighbors.

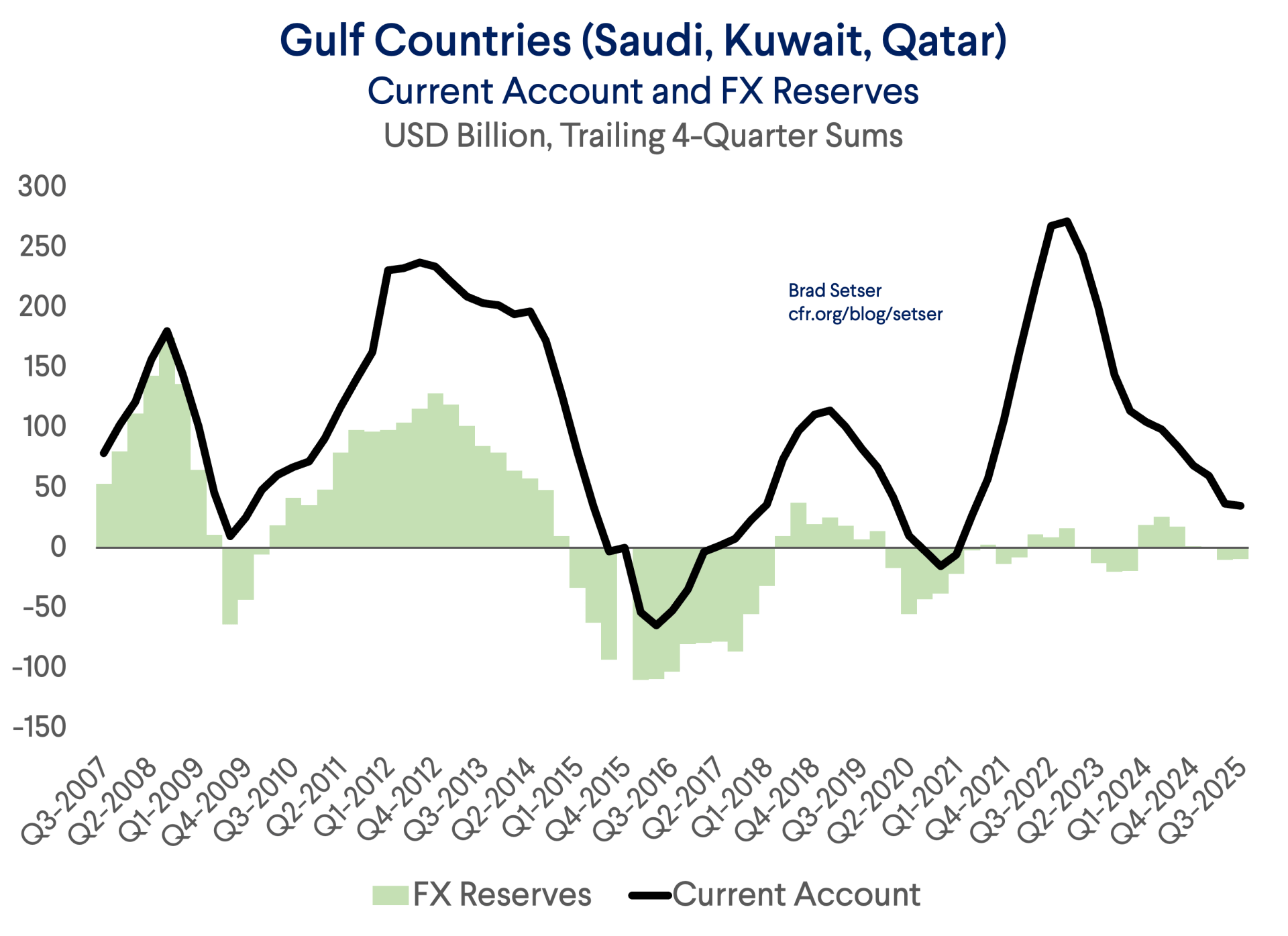

Second, the remaining oil surplus was concentrated in a small set of countries with tiny populations relative to their oil and gas endowments and wasn’t being accumulated in the form of central bank reserves—in that sense, the world of classic “petrodollars” had come to an end.**

The GCC countries and Norway do still have a significant surplus, but that oil surplus had fallen to around $200 billion dollars or so in 2025 ($35 billion in Kuwait and the UAE, $25 billion in Qatar, and around $50 in Norway; the Saudi deficit $33 billion.

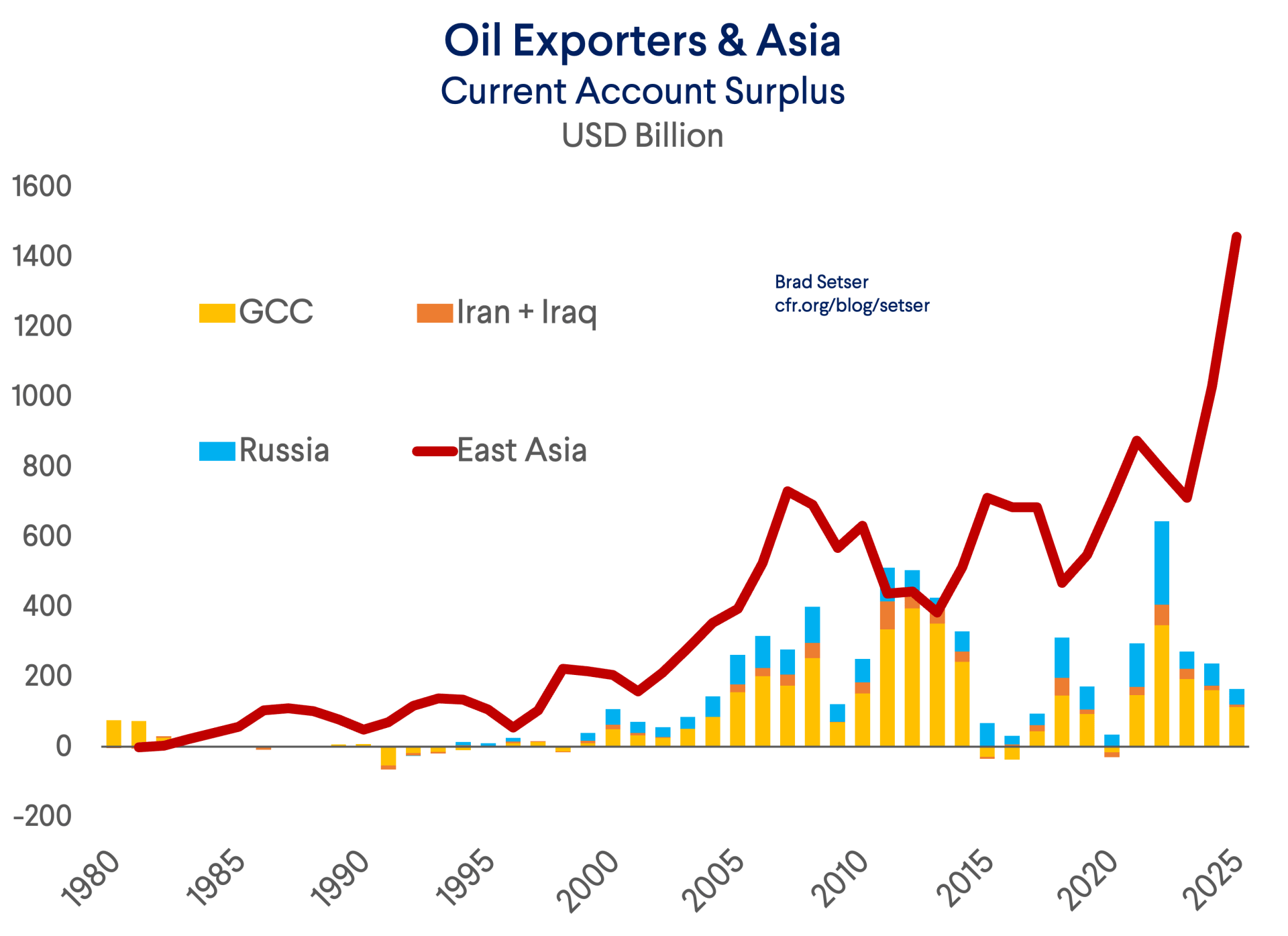

That is tiny relative to the $1.5 trillion surplus of “manufacturing Asia”—the buildup of dollars in the Chinese state banks and the buildup of offshore dollars in Hong Kong and Singapore from Chinese exporters drove the Eurodollar market.

Third, there are notable differences in how the remaining oil surplus is invested.

It isn’t going into classic reserves and traditional reserve assets.***

And there are important differences among the countries with big sovereign wealth funds.

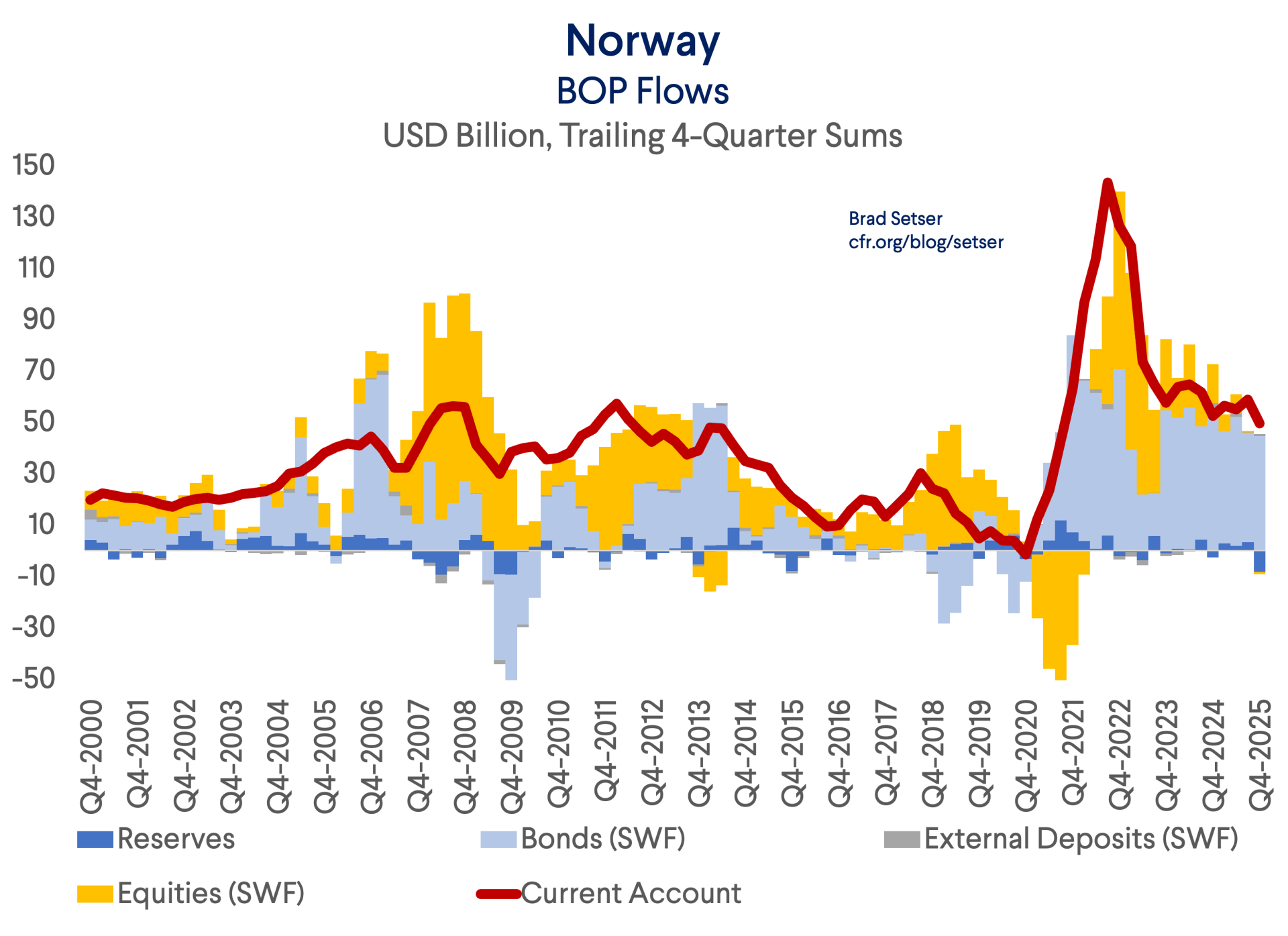

Norway has been the portfolio balancer par excellence—buying bonds rather than equities to keep the bond share of its portfolio up.

Kuwait also looks to have stepped up its bond purchases in 2025. Meanwhile Qatar, and presumably the Emirates, were still buying equities and funding a range of new ventures. Abu Dhabi’s old school, professionally managed sovereign fund (Abu Dhabi Investment Authority, or ADIA) has lost out to flashier royal ventures. And the Saudis were still buying equities, just with borrowed funds.

Tracking these flows isn’t easy—and the Emirates remains a black box.

But there is enough real data for me to refute the modern financial fairy tale that there is a big float of petrodollars sustains the dollar system.* This is fun to believe, but not really based in reality.

Prior to the confrontation with Iran and the de facto interruption of the flow of oil and gas through the strait of Hormuz, there was almost no flow from the oil exporters into liquid dollar assets. Well, ok, apart from the predictable Norwegian flow in U.S. bonds; but the only real way to get a globally significant flow into U.S. assets is to treat “petro-equities” as “petrodollars,” even though equity investments generally have more equity market risk than currency risk.

Alex Etra of Exante Data has found that 80 percent of the PIF’s reported external assets are dollar denominated, and it wouldn’t be a surprise if the UAE’s much larger overall portfolio was also dollar heavy.

Obviously, all of this is backward looking. Oil isn’t at $60 anymore. Spot oil for immediate delivery traded for well over $130 a barrel on the second weekend of April. Landlocked U.S. oil for June delivery is in the 90s. Seaborne sweet light in the North Atlantic (Brent) for May or June is still around $100 a barrel.

But even with the current uncertainty over the future path of oil, there are some basic analytic points that can help anchor informed analysis.

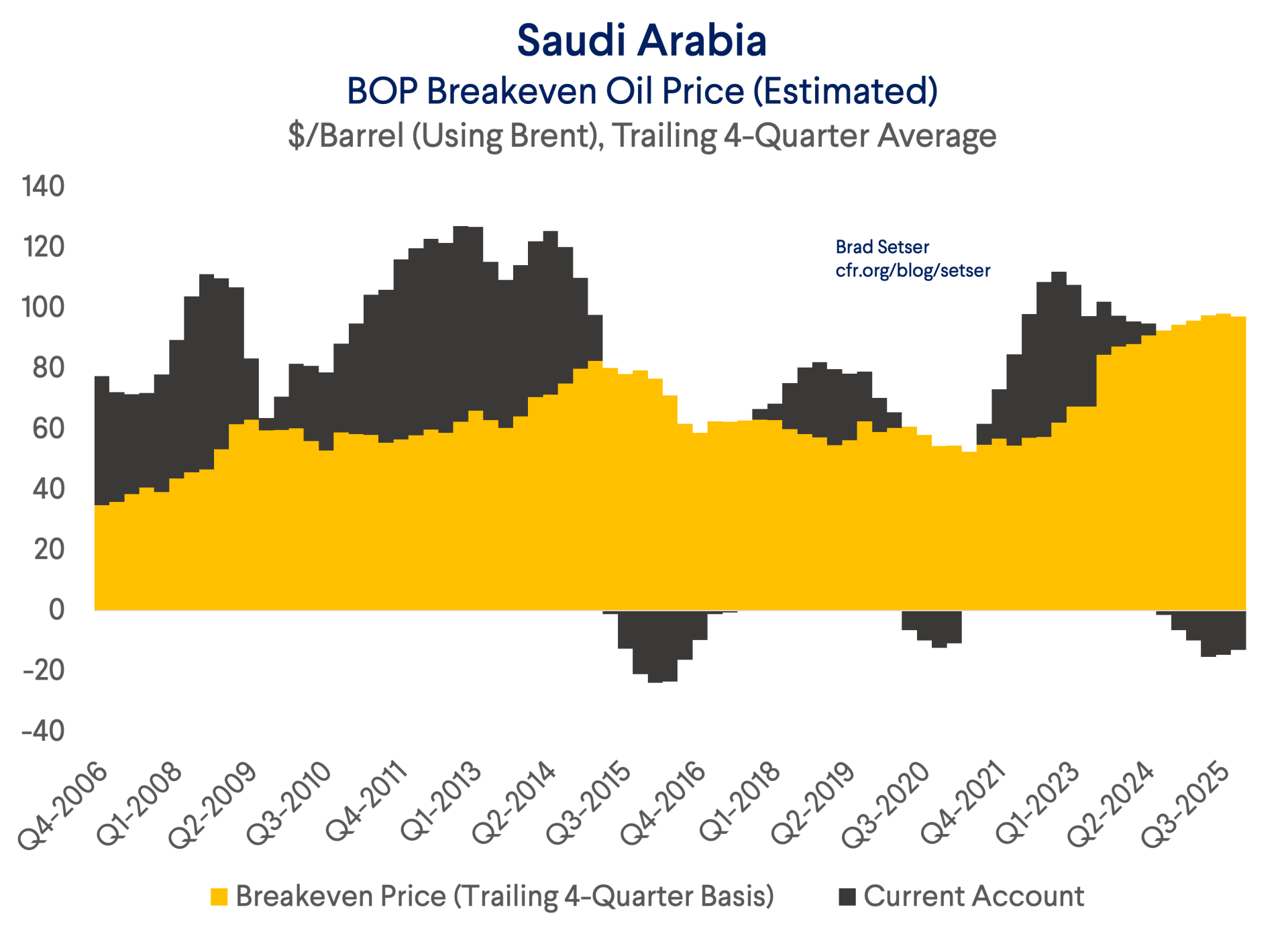

The Saudis aren’t going to generate a big surplus to reinforce the postulated petrodollar system with oil at around $100—not when their balance of payments breakeven (on around 7 million barrels a day of exports) is over $90 a barrel.

But if the benchmark price of oil converges to around $100 for an extended period of time, a bit of Asia’s massive current account surplus will flow to those oil exporters able to supply the global market while flows through the Strait are limited. For reference, the average price of Brent in 2025 was just under $70 a barrel.

A $10 barrel increase in the price of oil raises the import bill of Europe and the oil importers of South and East Asia by about $160 billion. According to the Energy Institute data, Europe imports 12 mbd, and South and East Asia something like 30 mbd, so the bulk of the impact is felt in Asia.

East Asia in aggregate imports around 20 million barrels day (China 12 mbd, Japan a bit over 3 mbd, Korea a bit under 3 mbd, Taiwan less than a million barrels a day), so every $10 a barrel raises East Asia’s import bill by $70-80 billion over the course of a year.

But East Asia can afford a big shock. A sustained $50 a barrel shock (oil at $120 a barrel) would reduce East Asia’s current account surplus by $350 billion (more, if counting gas), leaving the combined surplus of Korea, Taiwan, Japan, and China well above $1 trillion.

South Asia imports less in aggregate but faces a more significant payments squeeze. Pakistan and Bangladesh are relatively poor and can be priced out of global markets—a particularly cruel form of demand destruction.

On the surplus side, this shock is unique as that the usual sources of petrodollars—the Gulf Monarchies—aren’t among the beneficiaries. Rather, the contrary. Iraq, Kuwait, and Qatar aren’t exporting much at all. Volumes from the Emirates are way down. Saudi exports have been sustained by the East-West pipeline but aren’t equal to their January or February levels.

The clear winners are the traditional oil exporters outside the Gulf: the Norwegians, the Kazakhs and Azeris, and the Russians. The exporters of the new world as well, the Canadians first and foremost, but also Brazil, Colombia, Ecuador, Venezuela and now Guyana.

The oil exporters of Alberta and the oil producers in parts of the U.S. will be flush, but they tend to keep their funds in the onshore market. So, there may not be the usual flood of offshore petrodollars (though Russia may want to do more with oil surplus than increase its holdings of low-yielding yuan), at least not in the usual sense of the term, but big North American oil will be flush with onshore dollars.

That is the key point, in a sense.

There is too much talk about Kissinger’s 1974 deal with the Saudis, and perhaps Treasury Secretary Simon’s deal. That deal wasn’t for all time.

The Saudi surplus from ‘73 and ‘79 had disappeared by the late 80s and early 90s, but at the time, few talked about the end of the petrodollar system.

It is time to update a lot of priors. The U.S. is now a net oil exporter, not an importer, and has no direct need for Saudi supply. The Saudis today are borrowers rather than lenders, big issuers of dollar-denominated bonds not buyers of Treasuries. The Gulf monarchies are more equity investors than “bankers” to the world.

And even with oil above $100, the big sources of offshore dollar liquidity (dollars in banks, available to be lent out) are the Asian manufacturing exporters, not the Gulf monarchies.

* The UAE’s reserves are up, but that stemmed from pre-Iran “excursion” financial flows; the CBUAE is the federal central bank and it doesn’t manage the budget reserves of any individual emirate to my knowledge.

** A fairy tale that is also widely believed in the national security community, which has convinced itself that dollar “dominance” is critical to U.S. global power without carefully defining what is meant by dollar “dominance.” As an example, does the impact of the dollar’s reserve currency status hinge on the actual flow of dollar reserves, or the dollar’s share of a static stock of reserves?

*** To be clear, unless the U.S. walls itself off, stops exporting, allows efficient internal transport of Gulf Coast and Texan oil to the West and East Coast, and changes its stock of refiners to use light rather than heavy oil, the U.S. does rely on Saudi and GCC oil to keep the global price of oil and thus the domestic price of oil stable. And of course, the U.S. public remains incredibly sensitive to swings in the price of oil.