Which Countries Stand to Lose Big from a Greek Default?

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Dinah WalkerAnalyst, Geoeconomics

The IMF has turned up the heat on Greece’s Eurozone neighbors, calling on them to write off “significant amounts” of Greek sovereign debt. Writing off debt, however, doesn’t make the pain disappear—it transfers it to the creditors.

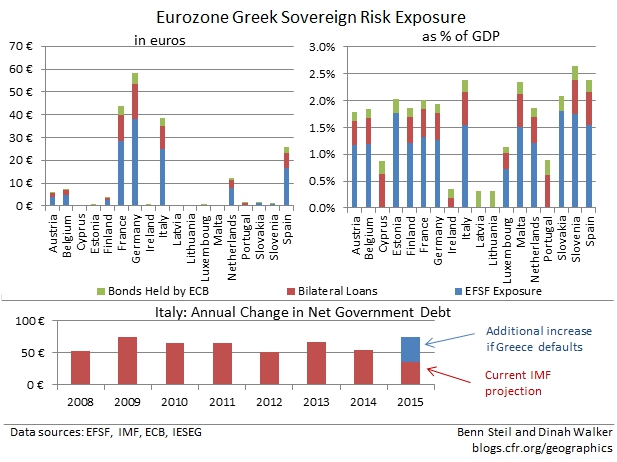

No doubt, Greece’s sovereign creditors, which now own 2/3 of Greece’s €324 billion debt, are in a much stronger position to bear that pain than Greece is. Nevertheless, we are talking real money here—2% of GDP for these creditors.

Germany, naturally, would bear the largest potential loss—€58 billion, or 1.9% of GDP. But as a percentage of GDP, little Slovenia has the most at risk—2.6%.

The most worrying case among the creditors, though, is heavily indebted Italy, which would bear up to €39 billion in losses, or 2.4% of GDP. Italy’s debt dynamics are ugly as is—the FT’s Wolfgang Münchau called them “unsustainable” last September, and not much has improved since then. The IMF expects only 0.5% growth in Italy this year.

As shown in the bottom figure above, Italy’s IMF-projected new net debt for this year would more than double, from €35 billion to €74 billion, on a full Greek default—its highest annual net-debt increase since 2009. With a Greek exit from the Eurozone, Italy will have the currency union’s second highest net debt to GDP ratio, at 114%—just behind Portugal’s 119%.

With the Bank of Italy buying up Italian debt under the ECB’s new quantitative easing program, the markets may decide to accept this with equanimity. Yet assuming that a Greek default is accompanied by Grexit, this can’t be taken for granted. Risk-shifting only works as long as the shiftees have the ability and willingness to bear it, and a Greek default will, around the Eurozone, undermine both.

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”