Beijing and Shanghai Overbuild Suggests Growth Hit by 2019

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Benjamin Della RoccaAnalyst, Center for Geoeconomic Studies

“Houses are built to be inhabited,” scolded Chinese leader Xi Jinping at last October’s 19th Party Congress, and “not for speculation.”

After a year’s worth of mortgage-rate hikes and new home sale restrictions backing his words, speculation does seem to have lost steam. Since autumn 2016, housing price growth has slowed nationally, hitting zero last year in Beijing and Shanghai—historically China’s frothiest markets. But might prices actually start falling soon? And if they do, what would that mean for the economy broadly?

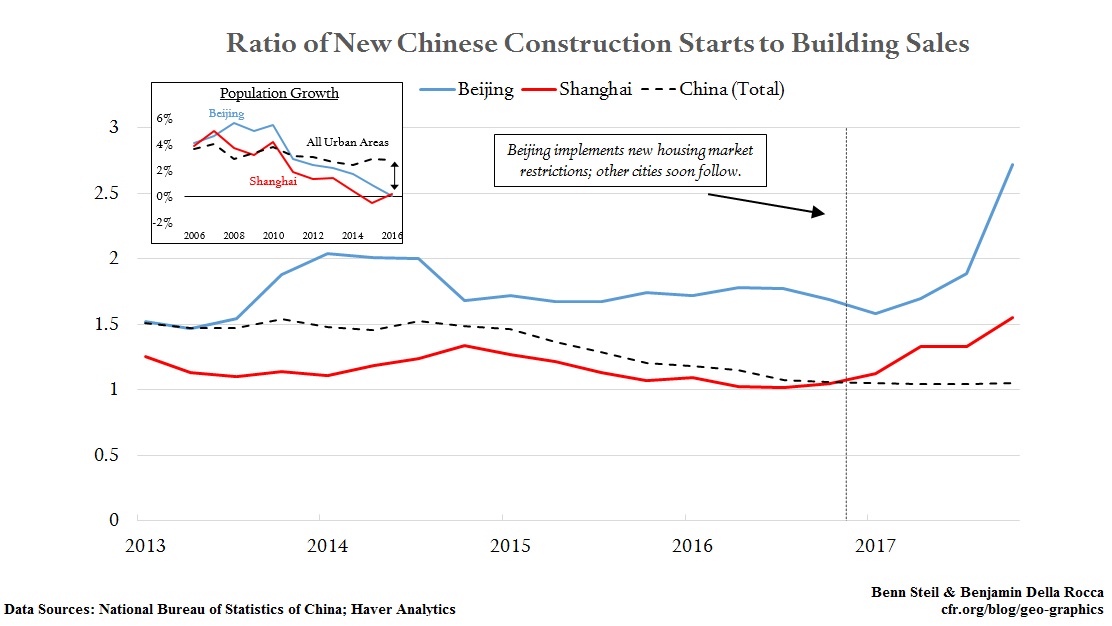

Despite falling sales, Beijing and Shanghai continue to build at roughly the same pace we’ve seen since 2014—over 50 million square meters per year in total. The result is that the ratio of new construction starts to building sales has soared—as our main graphic above shows. Unless this reverses soon, the law of supply and demand would seem to dictate price falls.

Of course, China famously “overbuilt” in the past, only to see massive influxes of rural migrants absorb the excess supply. Couldn’t the same now happen in Beijing and Shanghai? We think not. Population growth in these two megacities has hovered near zero in recent years, following efforts to curb population growth in each.

What might falling house prices mean for the broader Chinese economy? Home values affect consumer spending, and therefore GDP growth, by way of the so-called wealth effect—that is, consumers tend to change spending habits as their assets rise or fall in value. In the United States, according to one Federal Reserve study, for every $100 decline in housing-market net worth consumption tends to drop by $2.50-5.00. If this relationship were to hold for China, where homes represent a far greater portion of household income, we calculate that a modest 10 percent fall in Beijing and Shanghai home prices would knock over half a percent off GDP.

The IMF expects Chinese growth to fall from 6.8 percent in 2017 to 6.4 percent in 2019, although house price declines do not appear to be part of their equation. Our analysis suggests that, all else being equal, something below six percent is more likely—with the drag persisting into 2020 and possibly beyond.