Time for the IMF to Stop Blaming the Victim

The IMF standard analysis of imbalances puts too much blame on Europe and way too little on China.

The IMF’s standard analysis of global imbalances puts equal emphasis on the United States (too little saving), Europe (too little investment), and East Asia (too much saving).

That analysis is now dated.

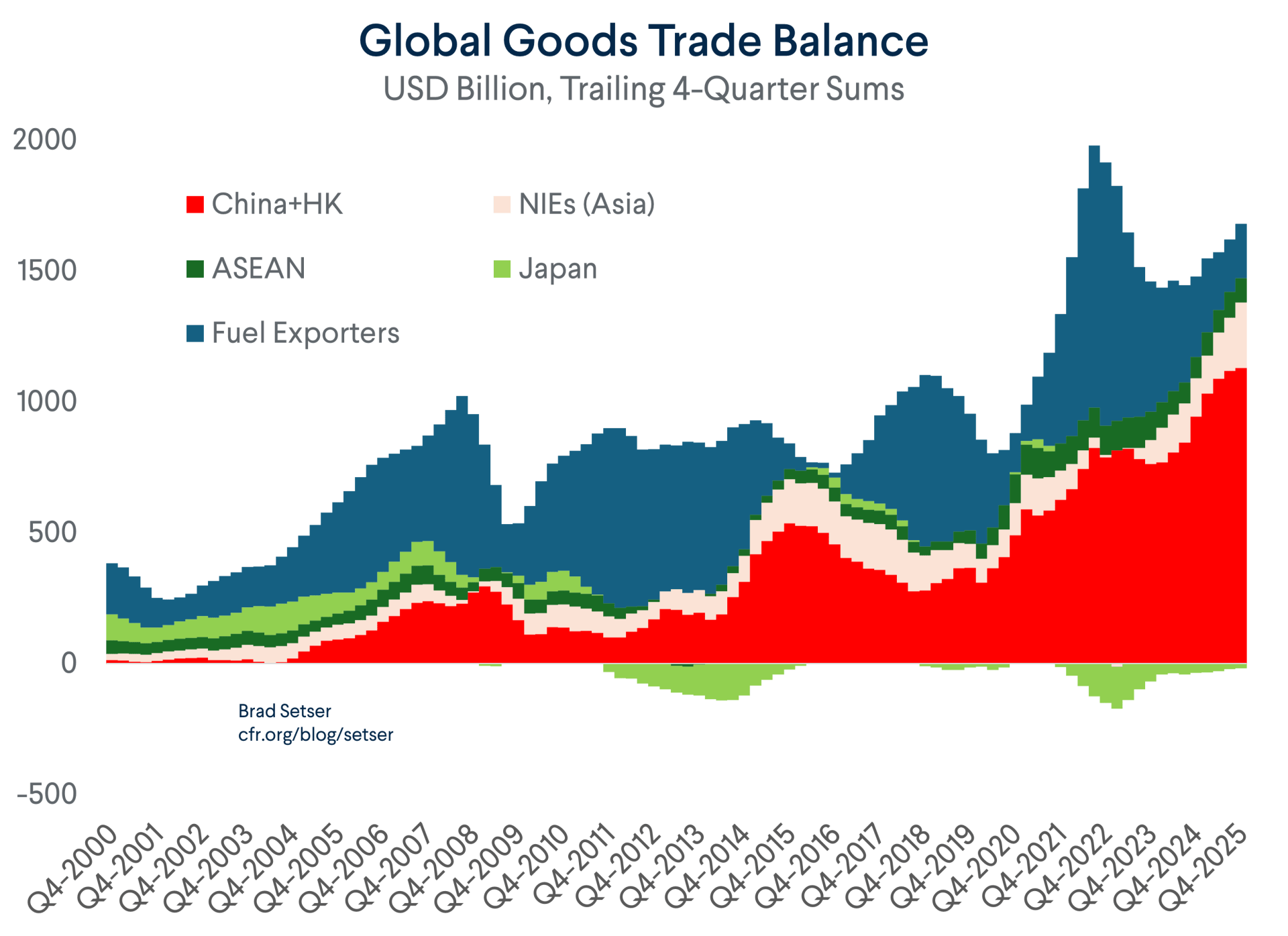

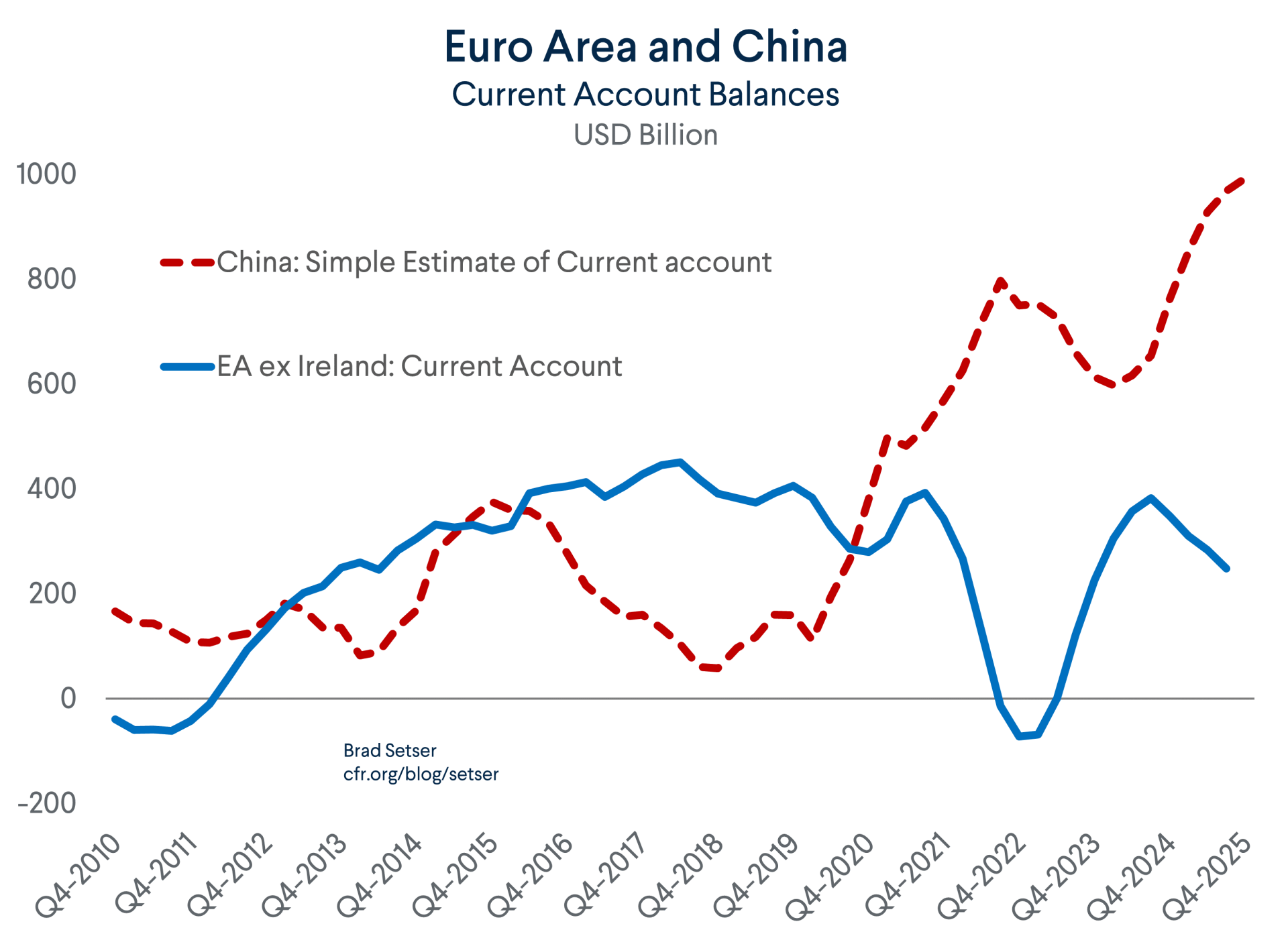

East Asia’s surplus (correctly measured) has soared—and while it will dip with the new oil shock, that dip will be temporary if the oil shock isn’t sustained.

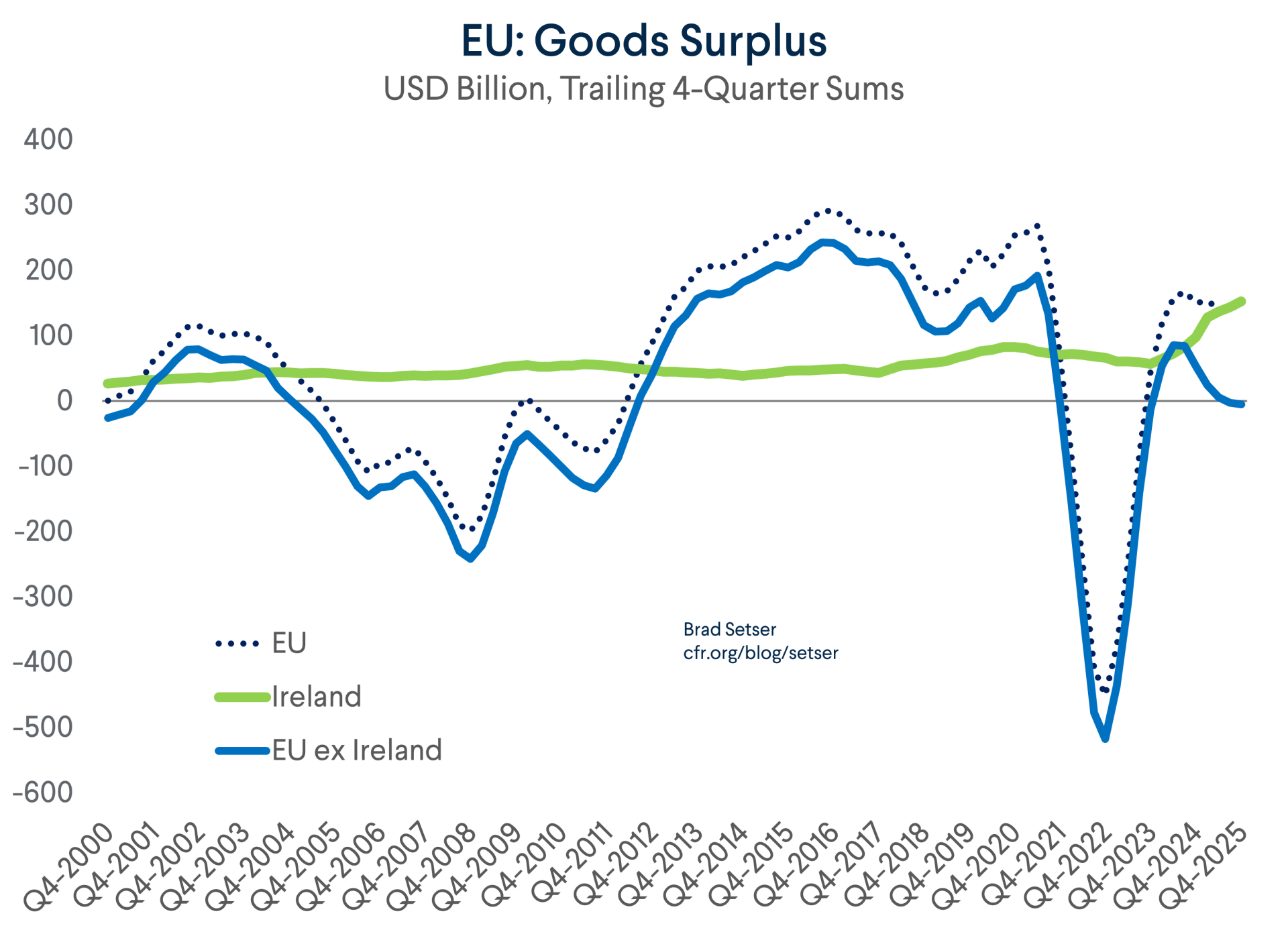

Europe’s surplus (correctly measured) has almost disappeared, even before the oil shock.

Europe may well need reforms to reduce internal barriers to commerce and increase investment, but the China shock (together with the Russian energy shock) has already wiped out the underlying goods surplus (setting aside US firms avoiding US corporate income tax through their Irish operations).

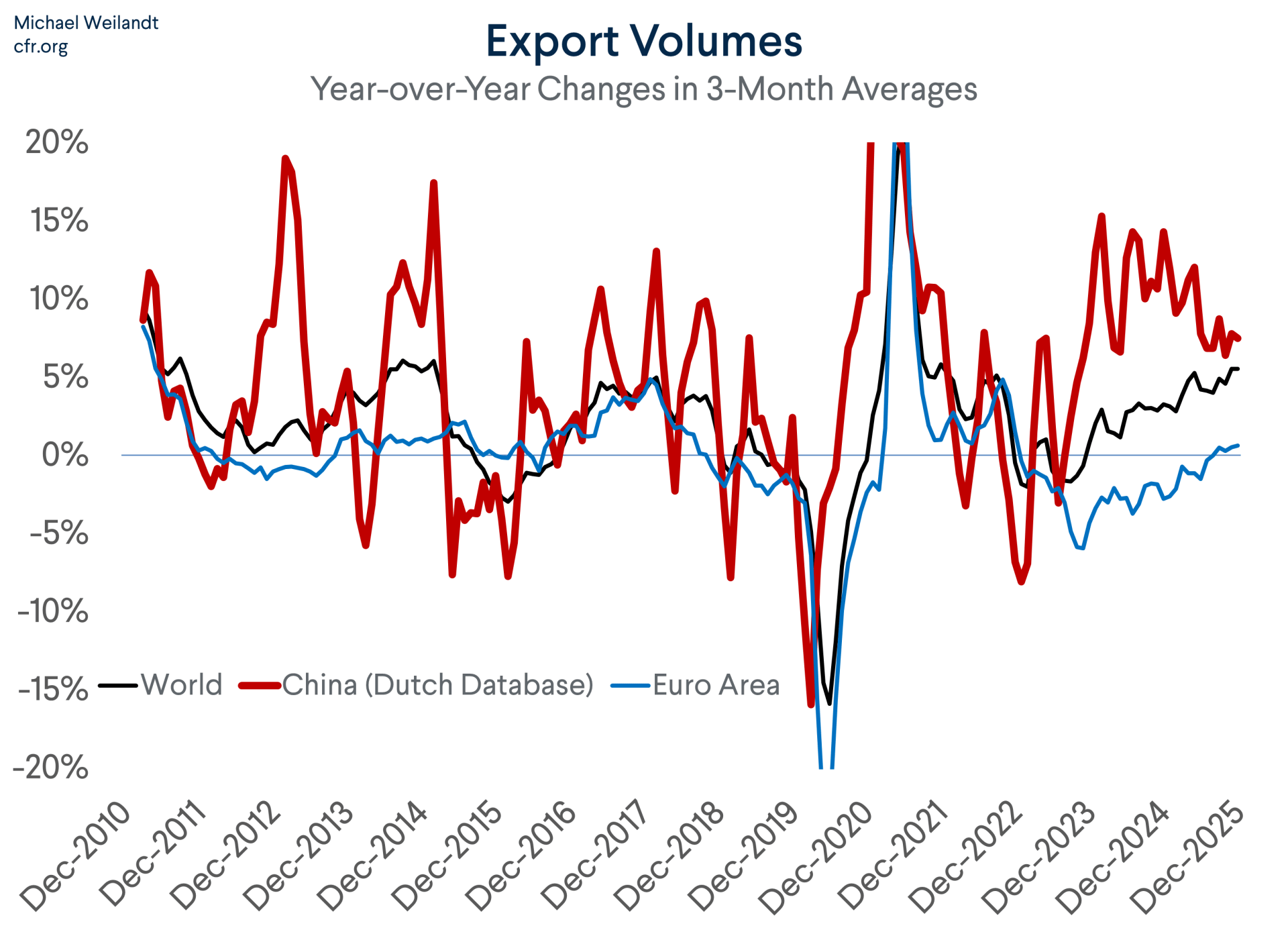

The IMF’s overly balanced analysis ignores an uncomfortable fact that is clear in the numbers: China’s recent export success has come at Europe’s expense.

That is clear from the Dutch Centraal Planbureau data on global trade volumes.

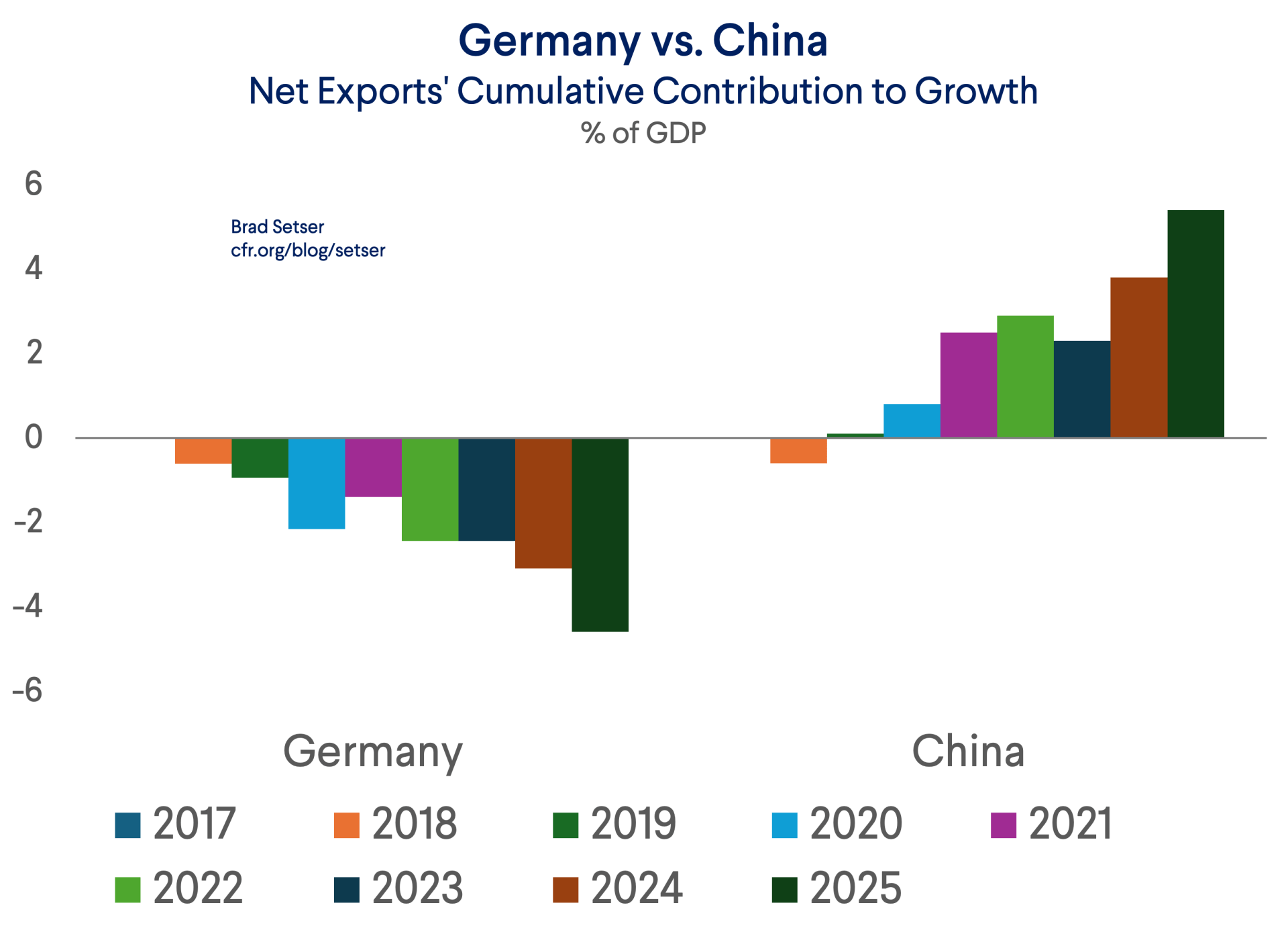

It is also clear in this striking chart—one that the IMF might well want to ponder. It shows the contribution of net exports to China’s growth over the last 6 years (the period after the pandemic). And it shows the drag from net exports on Germany’s growth.

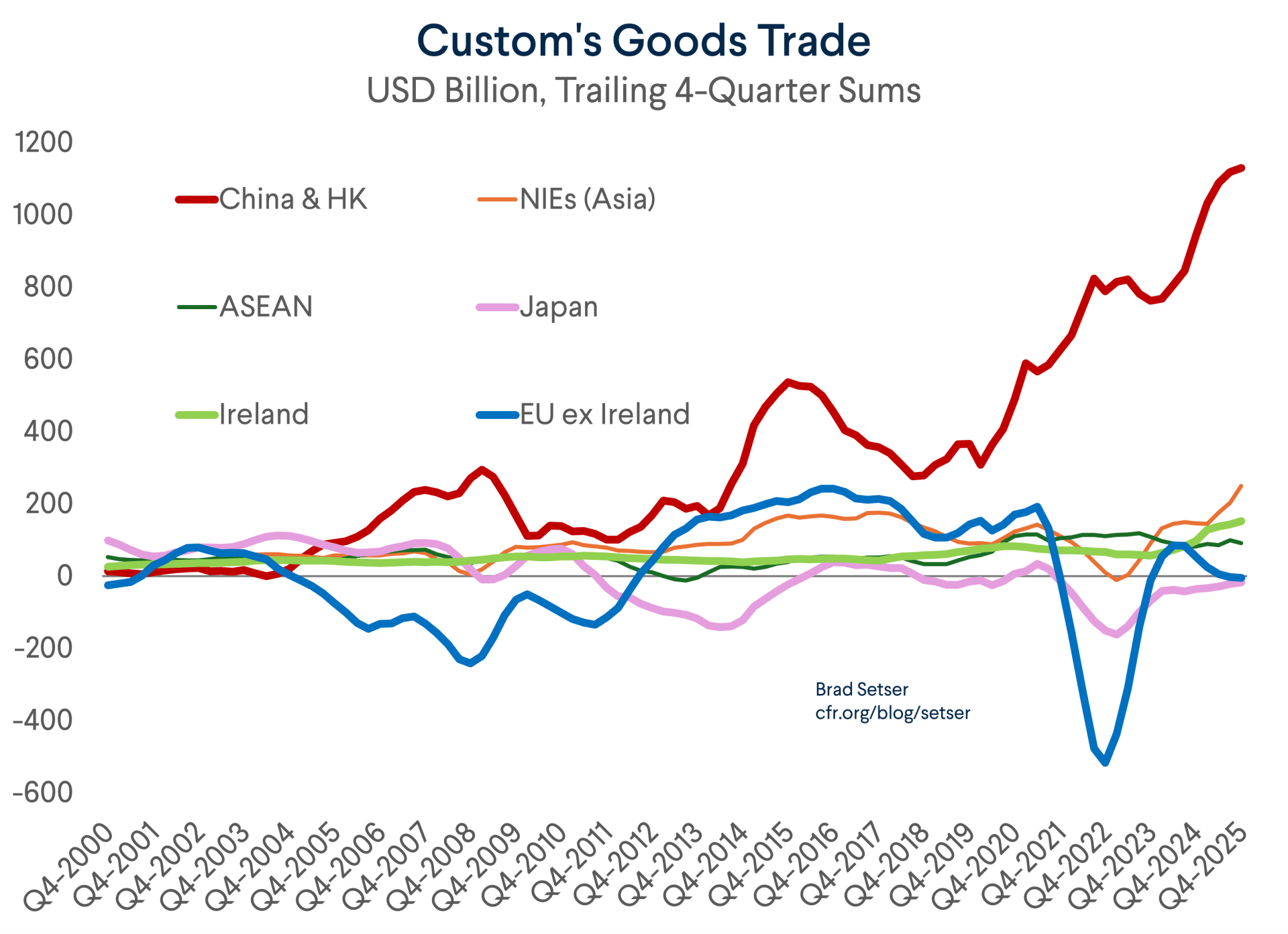

There is no doubt that Germany and its neighbors in central Europe have been hit harder than most other major European economies by the second China shock.

Germany exported more to China in the past (2.5 percent of German GDP, once upon a time), which made it more vulnerable to being squeezed out of the Chinese market.

Germany, Czechia, Slovakia, and Hungary specialized in the production of internal combustion engine cars, and thus were more exposed to China’s remarkable emergence as the biggest auto exporter the world has ever known.

A quick aside: China’s net passenger car exports are likely to top 10 million cars this year—out of a global market excluding China of 60-65 million cars). That is Japan or Germany on steroids.*

But Germany isn’t alone. All European countries that aren’t home to chip making equipment giant ASML have also seen their exports to China fall. And that is a big reason why overall exports have been weak.

This hasn’t jumped out in the numbers the IMF uses in its standard assessment of global imbalances for a few reasons.

The simplest is that the IMF tends to work off lagged data—its latest formal assessment uses numbers from 2024.

Since then, China’s reported surplus has soared and Europe’s reported surplus has shrunk. When the IMF formally updates its assessment of imbalances in the External Sector Report that is due in summer of 2026 (after France’s summit) it will find that China’s excess surplus has increased and Europe’s excess surplus has largely disappeared.**

But lags aren’t a sufficient explanation.

The IMF should have seen the shift in the global surplus toward China and East Asia several years ago. It should have registered Europe’s external weakness a few years back as well.

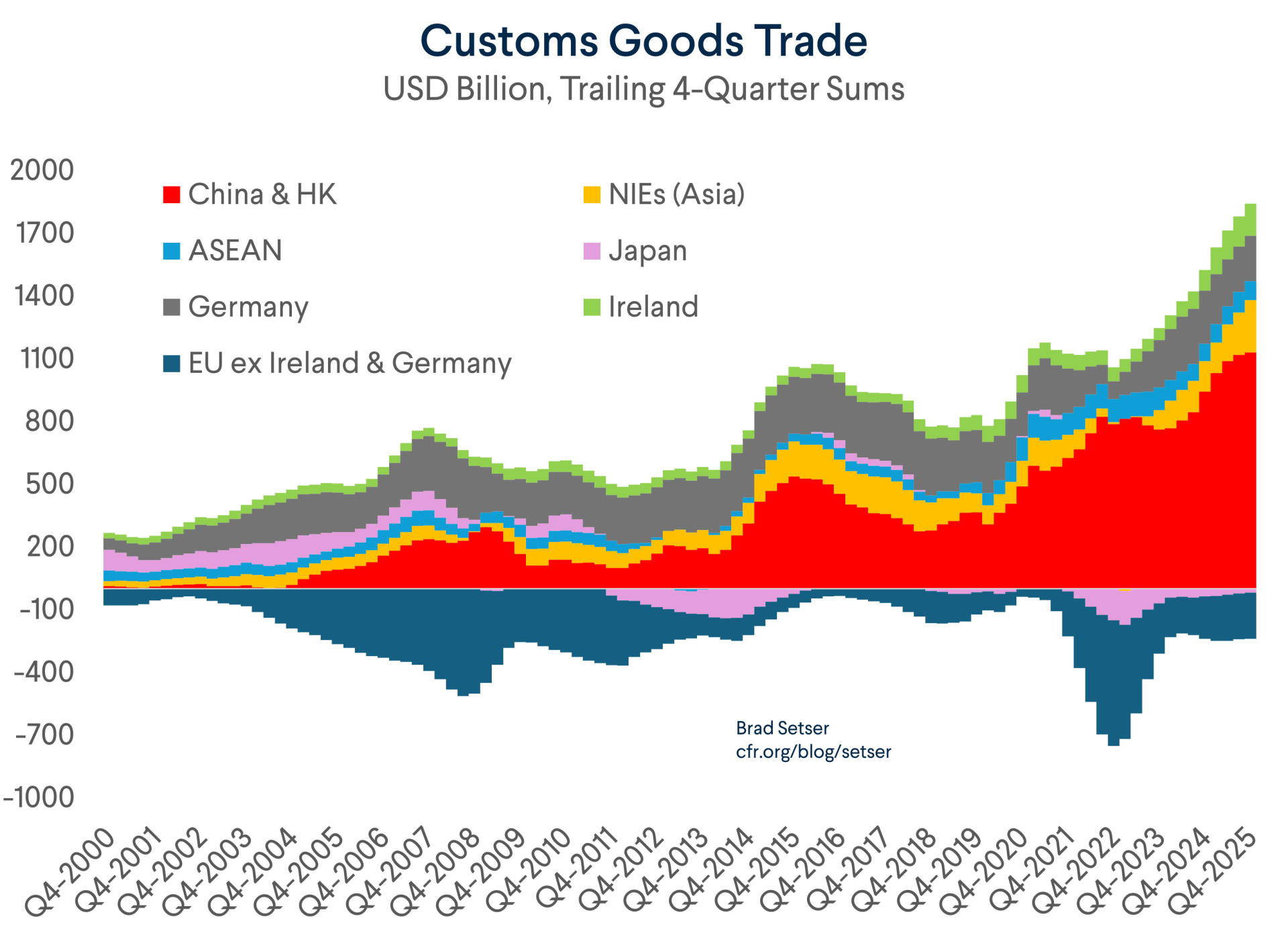

But it did not, for three reasons. The first is that the IMF doesn’t correct the European data for the distortions created by the United States tax beachhead in the euro area: Ireland.

Now there is an argument that, in theory, the tax shenanigans of U.S. multinationals have no impact on Ireland’s reported current account. American pharmaceutical companies inflate the customs goods balance. Apple’s merchanting inflates the balance of payments goods surplus. Microsoft adds to IT service exports. Google and Facebook inflate advertising service exports. But there are offsets. Google makes large royalty payments back to HQ. And the profits that accrue to Apple, Microsoft, Lilly, Pfizer, and Merck’s Irish subsidiaries register as a debit in the income balance. But in practice Ireland reports a current account of 15 percent of its (inflated) GDP—and that surplus isn’t really relevant for assessing much of anything about the broader euro area.

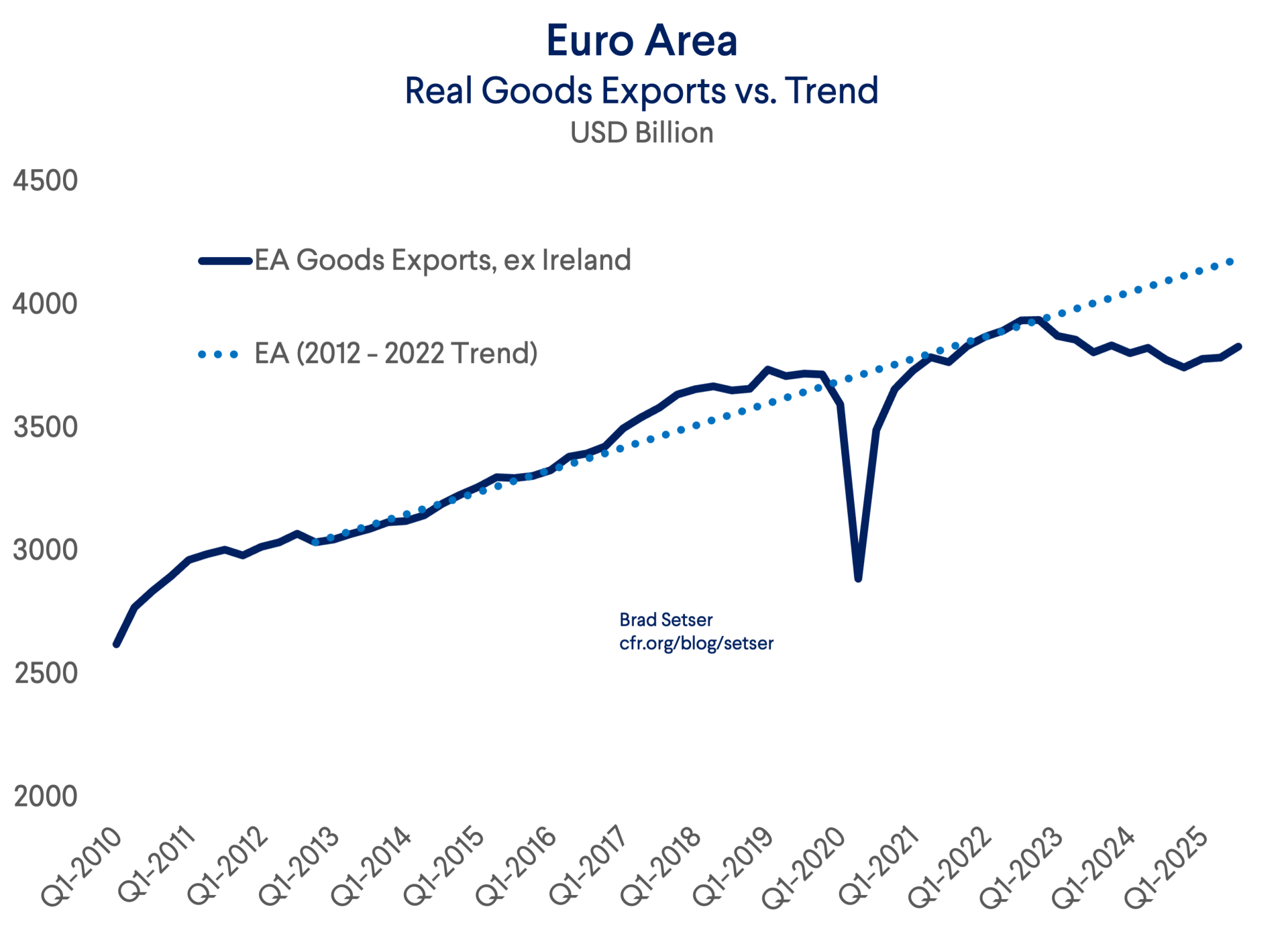

Ireland’s large pharmaceutical exports also have masked the impact of the China shock on Europe’s goods balance.

Looking at the customs data is now considered a bit, well, old fashioned, in most economic circles.***

But the old fashioned customs balance has one underrated virtue: it is counted accurately, and since the import and exporter data generally matches, it is largely immune from statistical manipulation.

Netting out Ireland’s rapidly growing customs surplus (from transfer price-inflated pharmaceutical exports) of the euro area produces a striking result: the euro area’s goods trade is already in balance.

Germany’s shrinking surplus is offset by deficits elsewhere.

That is the second reason why the IMF has missed the impact of the China shock on Europe. It ignored the Ireland-adjusted customs data and focused only on the current account balance.

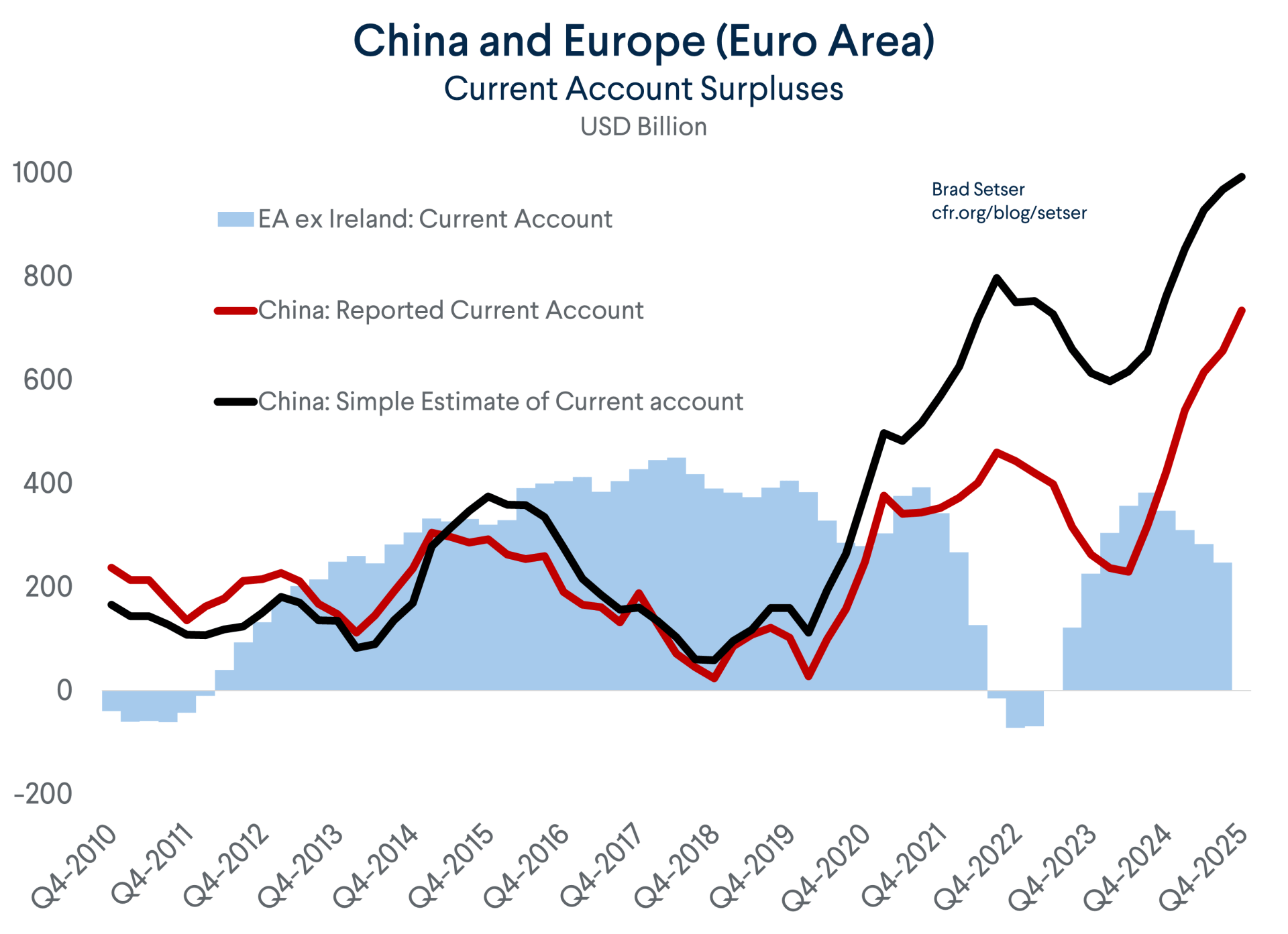

Europe’s current account balance has been supported by higher interest receipts on its large claims on the United States (there is a contrast here with China, of course).

And that gets to the third reason why the IMF largely missed the second China shock: it relied too heavily on the numbers that China reports about its current account surplus.

The IMF has belatedly recognized that China’s reported income deficit doesn’t make any sense. The net international investment position is increasingly positive, and there is no longer a gap between Chinese equity investment abroad and foreign equity investment in China.

Yet China’s income deficit now is bigger than it was six years ago, for reasons that no one can figure out.****

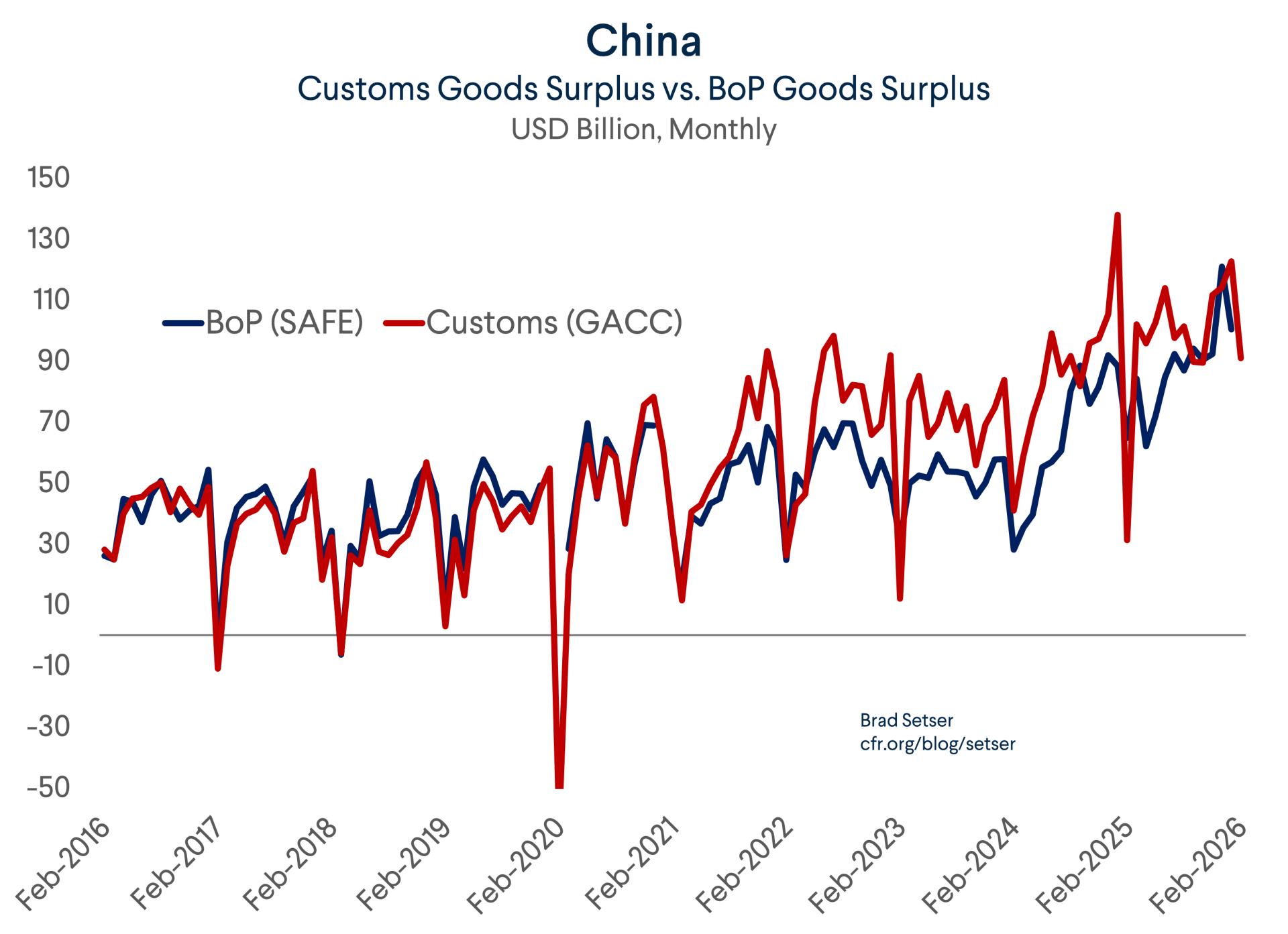

But the misreported income deficit isn’t the only problem with China’s balance of payments data. The downward adjustment in the goods balance (relative to the customs balance) is also problematic.

Now it is true that the reported current account surplus has surged—up from a (wildly too small) $200 billion in the four quarters through Q2 2024 to $730 billion in 2025.

But the downward adjustment to the underlying customs surplus (after adjusting for service imports) is still substantial, and it is a big reason why the current account surplus is “only” $730 billion when the customs goods surplus is $1.2 trillion.

The reported surplus in goods trade on a balance of payments basis is about $200 billion smaller than it would have been had China not changed its methodology for calculating the goods balance in the balance of payments back in 2022—that’s down from a peak of around $300 billion, but still substantial.

What’s more, the adjustment has become almost random (ok, not quite random—it shrinks when the banks are adding to their foreign assets, as China seems to adjust the adjustment to limit reported errors).

It disappeared for example in Q4 2025, though it seems to have crept back in January.

Bottom line: if the IMF looked at the customs data as well as the balance of payments data, it would have realized much earlier that the “surplus” side of the global balance of payments is now concentrated not in Europe, but in the manufacturing exporters of East Asia.

For better or for worse, the second China shock has solved the European surplus—and decimated German industry. Live by exports die by exports. Time for the IMF to mark its worldview to trade reality.

* There are far too many poorly argued comparisons in the U.S. about how the Chinese automotive investment in the U.S. could replicate the impact of Japanese automotive investment in the U.S., thereby raising U.S. production and output and generally raising quality across the industry. Replicating the full impact of the Japanese transplants, however, is impossible for one simple reason: the Japanese transplants largely displaced existing imports Japan, and there aren’t any current auto imports from China to displace.

Since China doesn’t export finished cars to the U.S. (setting one Buick model aside), new factories assembling Chinese designed cars from mostly Chinese made parts will displace U.S. parts production and reduce American/North American value-added in the auto sector in the first instance. There will be a positive effect from increased competition for consumers, and there is an argument that Chinese transplant will lead Chinese automotive manufacturing innovations may diffuse more rapidly.

But, in the first instance, Chinese marks would, on net, displace U.S. production. I agree with Jake Sullivan—the low hanging fruit here is from Chinese investment in the battery sector, not BYD or Xioami production of their EV designs (using their EV chips and Chinese supply chains) out of kits coming from China.

** To its credit, the IMF already updated its assessment of China’s undervaluation. If the actual end-2025 Chinese surplus is substituted in for the IMF’s estimate of the 2025 surplus, the 16 percent undervaluation becomes a 19 percent undervaluation.

*** Customs trade is influenced by tax, but much less than services trade, which is something that those who insist at looking at the goods and services balance to get an accurate measure of trade tend to either do not know or conveniently forget.

**** China has promised to break out FDI income from the rest of the income balance in 2026, so the underlying problems in the data should be easier to see going forward.