China’s Exorbitant Detriment, Mirror Image of America’s Exorbitant Privilege, Is Costing It Dearly

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Emma SmithAnalyst, Center for Geoeconomic Studies

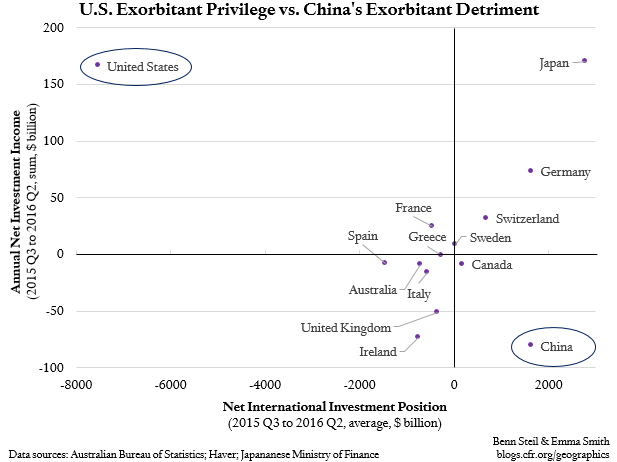

The so-called Exorbitant Privilege of the United States, the power to conjure the world’s primary reserve currency, is reflected in the unique combination of being deeply in debt to the rest of the world (that is, having a massive negative net international investment position, or NIIP) while earning far more income abroad than it pays out in interest (that is, having massive positive annual net investment income, or NII). The U.S. NIIP averaged negative $7.5 trillion over FY15/16, while its NII was positive $167 billion, as shown in the top left of the graphic above. Basically, foreigners are willing to accept a trivial return to hold dollar-denominated assets.

Far less well known is the mirror-image of the Exorbitant Privilege, or what we might call the Exorbitant Detriment. It is, not surprisingly, borne by China. It is, to some extent, the price the country bears as the world’s largest holder of dollar-denominated central bank reserves. Reserves account for half of China’s foreign assets, of which around 40 percent are invested in low-yielding U.S. Treasury securities. But it also reflects the fact that China is lending to the rest of the world at paltry rates. Chinese government institutions lend to Chinese, as well as foreign, firms operating abroad far more cheaply than alternative lenders. This reflects the Chinese government’s efforts both to subsidize its companies and to strengthen economic ties with resource-rich countries in, for example, Africa and Latin America. China’s Exorbitant Detriment is reflected in an NIIP of $1.6 trillion and NII of negative $80 billion in FY15/16.

Can China continue supporting its Exorbitant Detriment indefinitely? Not if it wants to prioritize a halt to reserve sales, which have been necessitated by capital outflows. Negative investment income reduces the current account surplus, and therefore the amount of capital that can leave the country before the central bank has to match outflows with reserve sales. If China’s investment income balance had been zero over FY15/16 it would, all else being equal, have been able to absorb an additional $80 billion of capital outflows before having to sell reserves. This is equivalent to 17 percent of the actual decline in reserves over this period. China’s reserves fell to $3 trillion in December and, as we pointed out in an earlier post, could actually fall to what the IMF reserve-analysis rubric would deem dangerously low levels by summer if outflows continue at the pace seen over the last three months. China can slow this decline by demanding higher returns on its lending abroad, but this will require sacrificing its efforts to subsidize its companies as well as those aimed at putting dollars to the service of geostrategic objectives.