A Quick Word on the (Lack of) Revenue From the Senate’s Proposed International Tax Reform

The Joint Committee on Tax has scored the Senate’s proposed international tax reform.

I haven’t seen any reporting indicating that the conference committee has significantly changed these provisions—though it seems like the conference committee will get rid of the alternative minimum tax for corporations that the Senate introduced at the last minute.

And the JCT score of the Senate bill is kind of interesting—as it shows how the Senate effectively chose not to broaden the U.S. tax base in a way that will raise significant future revenues from the globally untaxed profits U.S. firms now stash abroad.

The JCT indicates that the international side of the reform should generate $260 billion of revenue over ten years.

But that is purely a function of the $290 billion in revenue expected from the taxation of “legacy” tax-deferred profits (the infamous cash stash U.S. firms have kept abroad while waiting for a tax holiday).

The other reforms on net cost $30 billion.

In some sense that is a function of moving toward a territorial system where income “earned” abroad can be returned to the U.S. without incurring an additional tax liability.

The quotes around “earned” are intentional. A lot of tax planning goes into moving profits abroad—it isn’t clear if the American tax residents of Bermuda, Ireland, and similar locations really are earning large sums abroad, or just attributing large sums to their offshore arms.

But it is also a function of the choices made to limit the potential base erosion.

There seem to be real provisions to limit profit stripping out of the U.S. operations of foreign firms operating in the U.S.—those provisions are expected to net almost $150 billion over ten years.*

But, well, the provisions designed to tax the often largely untaxed profits U.S. firms now report abroad seem thin.

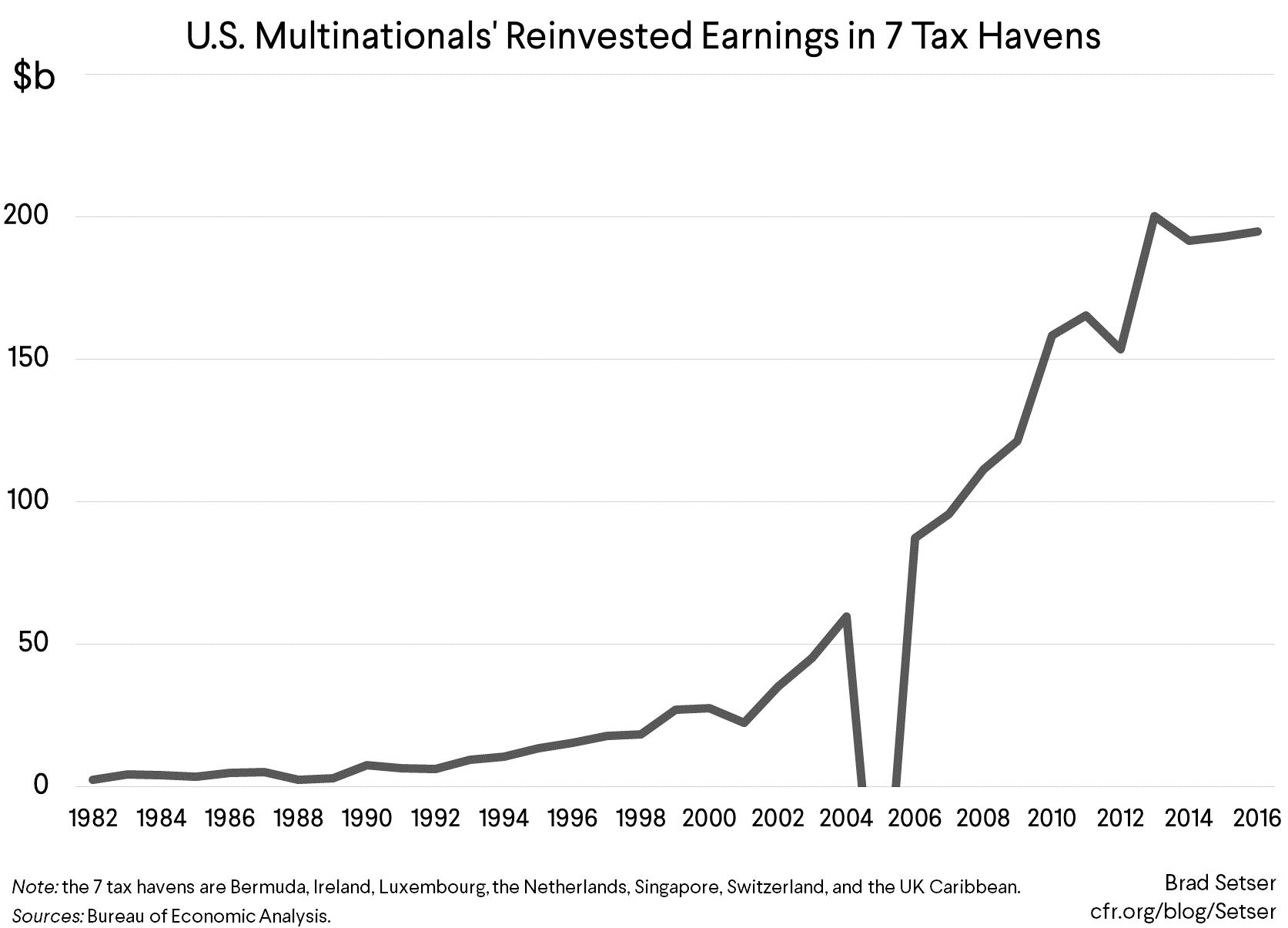

U.S. firms abroad now report $200 billion in “reinvested” (so not repatriated and not currently taxed) profits in the seven main tax havens, or almost exactly a percentage point of GDP. That is just the funds in the main tax havens—which I am taking as a proxy for the offshore earnings of U.S. firms that right now no one globally is really taxing.

If that share stays constant as a share of GDP, the annual flow of such profits over the next ten years should average about $250 billion.

A 20 percent tax (imposed on a firm’s global profit, with no deferral) thus should collect about $500 billion over ten years (e.g. an average of about $50 billion a year), minus any taxes actually paid abroad. And even a 10 percent tax should net about $250 billion.

The proposed 10 percent global minimum on intangible income though collects $135 billion (per the JCT) —partially because of the deduction for foreign taxes actually paid, and in part because firms get an automatic deduction equal to a 10 percent assumed return on any actual assets abroad, and in part because of the way the tax is calculated.

That’s leaving a lot of money on the table compared to a reform that really sought to broaden the base, which has clearly been eroded by tax shifting.

And a large part of the gains from a global minimum are offset by the special low tax on export earnings from intangible income retained by a U.S. firm. The 12.5 percent rate (counting the ability to move intangible assets that now held abroad back to the U.S. without a tax penalty) is estimated to cost about $100 billion over ten years.

In other words, the tax reform doesn’t seem to generate any significant future revenue out of U.S firms that have gamed the current system by shifting profits to low tax jurisdictions abroad.

And of course the new rules themselves can be gamed. As a prominent group of tax experts have noted, the 10 percent rate abroad creates incentives to shift assets offshore and the 12.5 percent rate on the export of intangibles creates incentives to export more (and then find ways to sell the goods back to the U.S).

As a result, I would not be surprised if the Senate’s proposed international reforms—if they are adopted by the conference and approved by both houses—actually end up reducing the amount of “international” tax revenue the U.S. generates going forward.

I have read that the tax reform doesn’t deliver much of an additional benefit to large global multinationals. That’s only true because global multinationals already have found so many ways to reduce their tax. The proposed reform doesn’t really widen the tax base to cover profits that have been shifted to tax havens in any real way.

One final, small point: the FT’s estimate of the gains to Apple from the tax reform seems to be too low. The FT’s calculation only captured the gains on Apple’s legacy profits (the $250 billion in cash Apple has “offshore,” which can be returned at a 14.5 percent rate rather than a 35 percent rate). It didn’t try to estimate Apple’s future tax savings, and those will also be significant.

Right now roughly two thirds of Apple’s profit is reportedly earned offshore (the New York Times indicates that 70 percent of Apple’s profit comes from its international side). So Apple’s offshore (e.g. tax deferred under current U.S. law) profit is likely close to $40 billion. Apple reports that it pays about $2 billion in foreign tax right now—so something close to a 5 percent rate on its roughly $40 billion in offshore profit.

Going forward, those earnings will either be taxed at somewhat under 10 percent (the global minimum on intangibles is 10, but Apple does have some tangible assets abroad) or at 12.5 percent (if Apple reorganizes itself as a U.S. exporter of intangible design and software and phases out its offshore subsidiaries). Either rate would be well below the 35 percent rate (minus deductions of taxes actually paid abroad) that theoretically should be paid under the current law—in fact both are below the 14.5 percent rate on legacy (e.g. tax deferred) profits in the Senate bill. **

And Apple here really is a metaphor for all the big technology and pharmaceutical companies with large offshore earnings in low tax jurisdictions, and large offshore cash holdings.

* The new base erosion taxes on foreign multinationals operating in the U.S. (which report very few profits in the U.S. currently thanks to their own tax gaming) helps offset the revenue lost from the shift to territoriality—e.g. the $215 billion in lost revenue from the “participation exemption” on U.S. firms foreign income in the JCT’s score.

** Of course Apple doesn’t pay the 35 percent rate as offshore profits can be tax deferred. If the Senate bill becomes law, its de facto tax rate on its past profits will be 14.5 percent--and Apple’s going forward rate on the same offshore income streams will be even lower.