Revisiting the Ides of March, Part III: Scary Stories to Tell in the Dark

By experts and staff

- Published

- Guest Blogger for Brad Setser

This is a guest blog by Josh Younger, an interest rate strategist at J.P. Morgan. Joshua Younger is employed by the Research Department of J.P. Morgan Chase & Co. All views expressed in this forum are his own and may not align with those of the firm, but they are consistent with all research publications published under the firm brand for which he is listed as an author. This is the concluding post in a three part series.

By the middle of March, the train is really threatening to jump the track.

As we discussed in Part I, a rapidly shifted fundamental backdrop had precipitated a collapse in market depth and severe liquidity tiering among fixed income products.

In Part II, we described how this combined with operational risk concerns shook loose a $200-300bn, highly levered position that had mostly been accumulated as a placeholder. As dealers were forced to take on more and more inventory, the Treasury market became increasingly incapable of intermediating even modest transactions.

For this last segment, it is important to bear in mind that Treasury cash/futures basis unwinds were arguably the more acutely concerning symptom of a much broader problem.

A sudden and fast-moving economic shock of unknown but clearly massive proportions created a rush to hoard cash to better weather the storm.

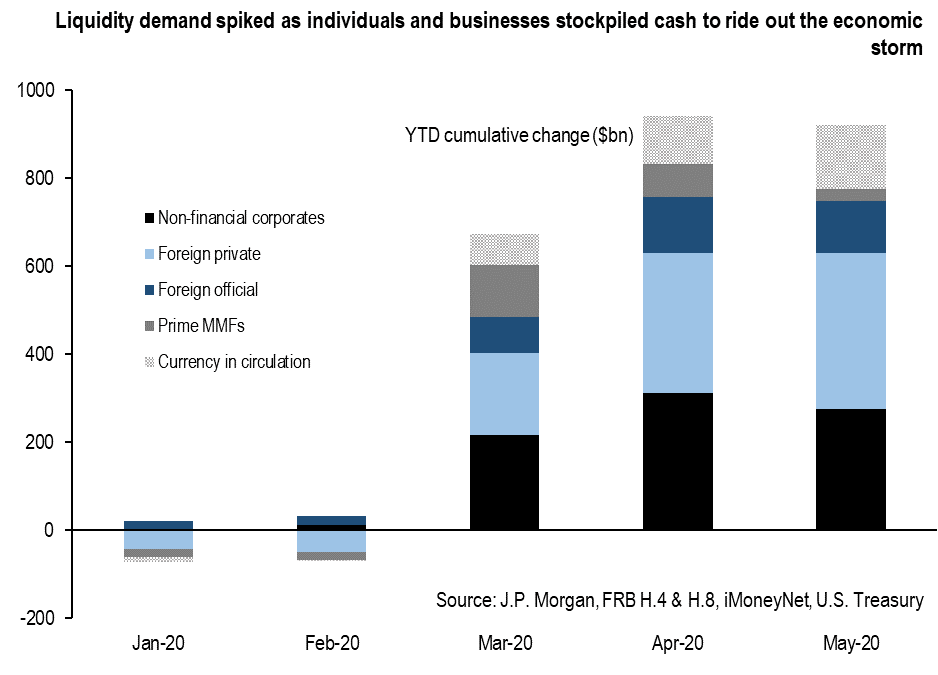

Individuals started to stockpile physical cash: Fed data shows that currency in circulation grew 6 percent in March and April, or roughly six times its longer-term growth rate. But, the actions of large institutions and even governments had much larger consequences. Non-financial corporates, for example, drew more as much as $300bn from their credit facilities at large commercial banks (based on Fed H.8 data) and redeemed more than $130bn of their prime money market fund holdings over the same period (comparable in pace and percentage to the weeks after the Lehman bankruptcy). U.S. Treasury data shows foreign central banks sold $128bn of assets as well, presumably to manage capital outflows and currency effects related to the pandemic.

In all individuals and businesses were demanding $1tn in new cash and equivalents over just a few weeks (CHART 1).

How were banks supposed to supply the liquidity the market was demanding?

This is where two elements of the post-2008 regulatory framework started to conflict with each other, and inhibit the free flow of cash through the financial system.

On the one hand, liquidity regulations, specifically the Liquidity Coverage Ratio (LCR), require banks to hold stocks of high-quality liquid assets (HQLA) that can be monetized quickly and at low cost should the need arise. On the other, capital regulations like the Supplementary Leverage Ratio (SLR) and surcharges on Global Systematically Important Banks (GSIBs), limit the size, complexity, interconnectedness, and cross-jurisdictional exposure of any given institution.

In normal times, these two sets of rules can co-exist quite peacefully with each other. But when the rainy day comes, their interaction can turn toxic.

The central role and large market share held by bank-affiliated securities dealers meant that the banking system itself is largely responsible for the monetization of its own HQLA. In other words, when a bank is facing a spike in liquidity demand—including any of the sources listed above—it is other banks that intermediate asset sales, especially Treasuries, to source the necessary cash. As a result, when leverage and other constraints inhibit their ability to do so, as was certainly the case in March, banks can no longer monetize their HQLA at a reasonable cost—if they can do so at all.

Other problems arise as a result of what happens to that liquidity. Draws on bank revolvers are particularly pernicious. By tapping these facilities, non-financial corporates are creating new assets (loans) and liabilities (wholesale deposits) on bank balance sheets. If the requisite transfers are funded by raising new capital, leverage can remain roughly the same. If banks rely on HQLA which largely remains in the banking system—e.g., reserves at the Fed, which are a closed system, or sales of Treasuries that linger in bank-affiliated dealer inventories, it can exacerbate the leverage problem that generated market dysfunction in the first place: a vicious cycle.

Those new wholesale deposits posed another problem. Because they are being held ‘just in case’ rather than for everyday transactional activity, they are likely to be characterized as ‘non-operational’ for LCR purposes. That category of deposits is considered the highest run risk, and therefore assigned the most demanding coverage requirements. Thus, as liquidity demand spikes, the stock of HQLA banks are required to hold is increasing, not decreasing.

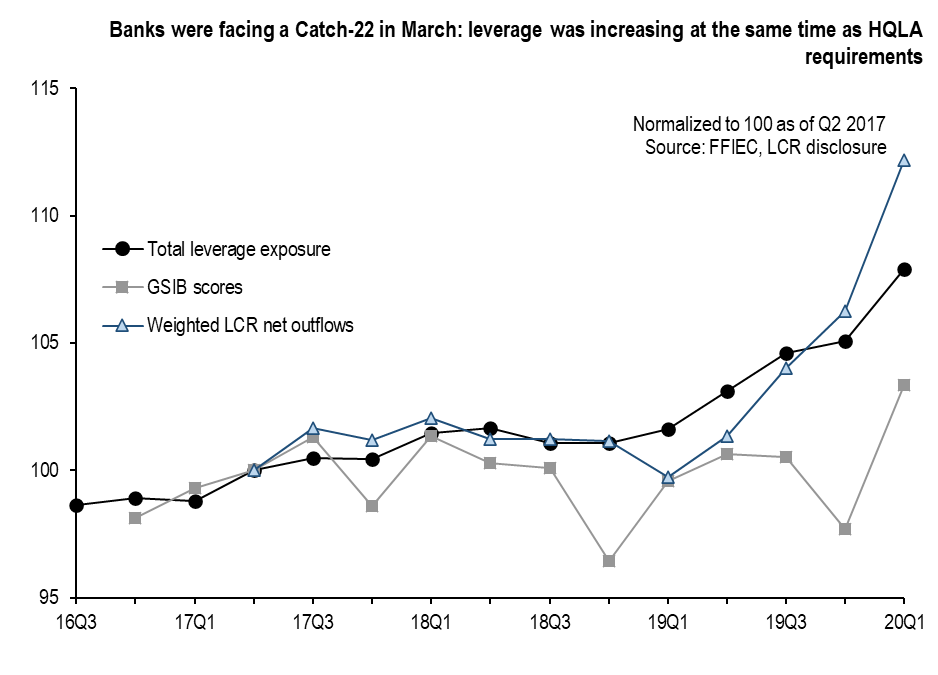

This is clear from 1Q 2020 regulatory disclosures, released a few months after the crisis. Liquidity Coverage Ratio weighted outflows, a measure of the HQLA required to satisfy regulatory minimums, were increasing rapidly at the same time as capital requirements related to total leverage and GSIB surcharges (CHART 2).

When bank leverage is rising in this way, the most effective offset is shedding assets.

Yet that was precisely the risk that regulators wanted to avoid. Disorderly delevering is manageable if it is isolated to a relatively narrow corner of the market (in this case, relative value hedge funds). But the same dynamic taking hold across the banking system was quite another thing.

FRA/OIS and FX swaps, two common barometers of stress in the banking system, were flashing bright red within days (both are measures of how easily banks can raise funds). If things were allowed to continue along this path, fire sales of assets into a severely illiquid market risked a full-fledged panic and financial crisis in the midst of a historic economic shock.

That is where the Fed comes in.

Central banks control the money supply and issue the currency. If nothing else, this gives them the right set of tools to deal with a liquidity squeeze. Simply growing the monetary base could in principle supply the cash that the banking system could not.

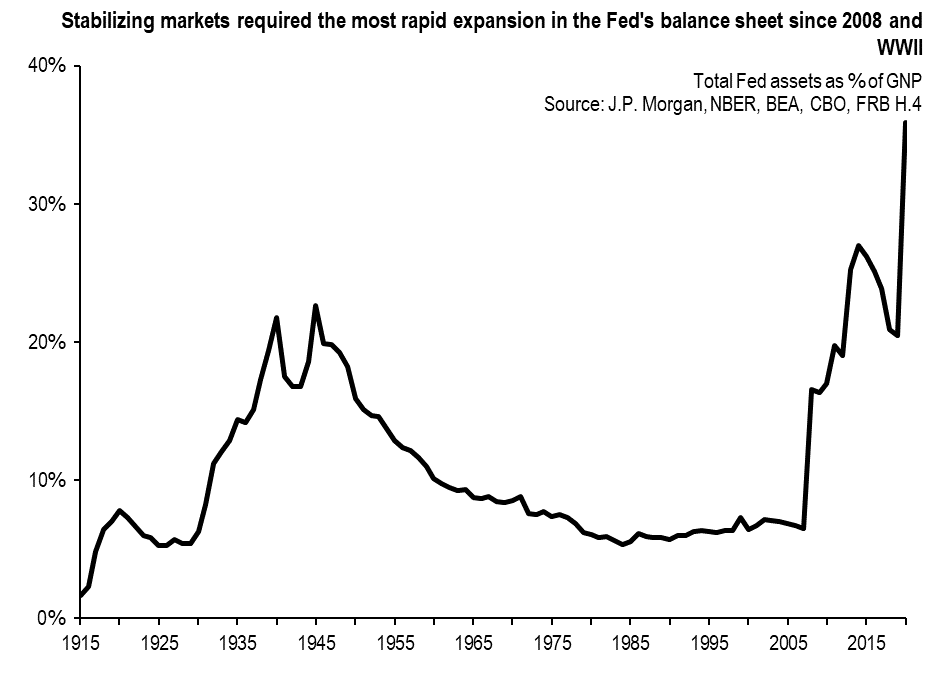

And grow it they did: the emergency cut announced on March 15 was paired with a commitment to purchase $700bn of Treasury and mortgage-backed securities, which was made unlimited shortly thereafter.

After peaking around $75bn per day of Treasury purchases in the second half of March, their asset purchases slowed gradually to the current daily pace of roughly $4bn. The Fed also restarted the FX swap lines, re-introduced several 2008-vintage facilities authorized under Section 13(3) emergency lending powers, and introduced a suite of new facilities under the same authority. At the peak in early-June, the monetary base had increased more than $2.8tn (~13 percent of 1Q GDP) over just three months, the largest such expansion since Second World War (CHART 3).

This intervention worked along a number of dimensions.

Market depth in Treasuries bottomed out and transaction costs normalized as automated systems flicked back on, and futures quickly came back into alignment with their deliverable basket.

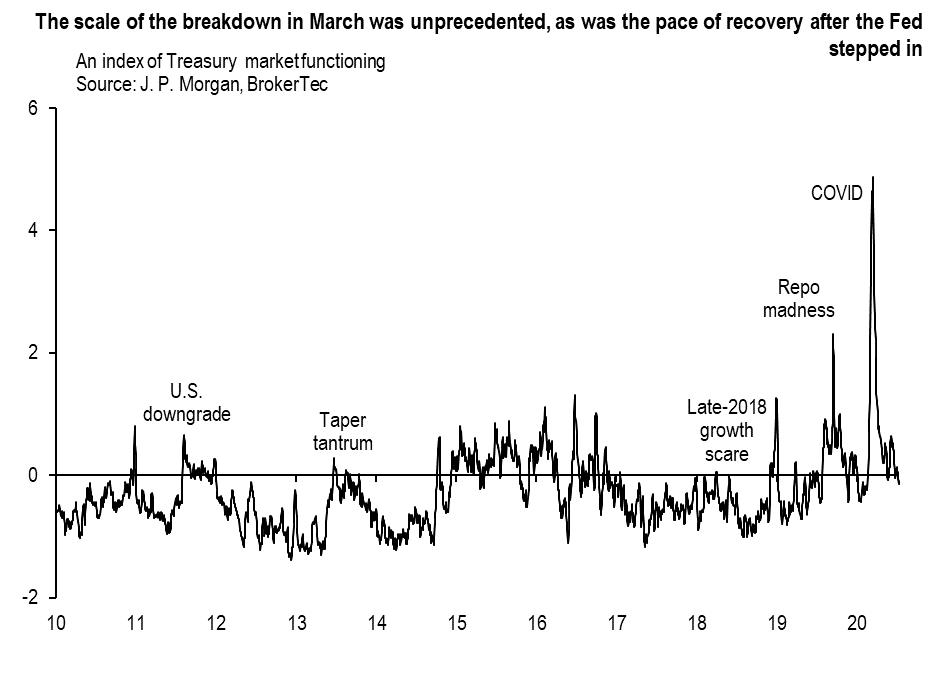

Combining these elements, and some others, shows both how severely market functioning had broken down, and how rapidly it healed in the wake of this historic intervention (CHART 4). FRA/OIS and FX swap pricing also started to return to Earth, thanks in large part to the resuscitated swap lines as well as old (CPFF) and new (MMLF) 13(3) facilities.

What does this tell us about the efficacy of the post-2008 bank regulatory regime?

That suite of rules was arguably successful at transforming a credit crisis, which is quite difficult for central banks to solve, into a liquidity crisis, which is well within their wheelhouse. With market functioning back to something resembling ‘normal,’ and little sign of funding or credit market stress, they appear to have lived up to that assertion. In that sense, this is a success story.

In another, however, we have simply substituted a fast-moving crisis for one which is slower moving. In aggressively expanding the monetary base, the Fed has mechanically increased the size and leverage of the banking system. Nearly $6tn of federal deficits over the next two fiscal years will likely compound the situation. In the 1940s, the last time such a thing happened, it took the banking system decades to delever as the post-War recovery drove renewed demand for private sector credit. With Supplementary Leverage Ratio and GSIB surcharges likely to become increasingly binding constraints on bank activity, the Fed risks simply delaying and spacing out, but not avoiding, asset sales and a sharp curtailment of credit.

That brings us to the present day. There has been some effort to counteract the impact of rising banking system leverage with changes to some regulations. The Fed, FDIC, and OCC in particular have proposed temporarily excluding risk-free assets (cash and Treasuries) from the calculation of total leverage exposure when assessing Supplementary Leverage Ratio compliance.

There are, however, significant gaps in this approach. As proposed, Supplementary Leverage Ratio relief comes with strings attached that may be difficult for many banks to accept. GSIB surcharges, which in practice are a strong constraint on bank behavior, are similarly implicated by a much larger Fed balance sheet but conspicuously absent from the discussion.

Some other proposals, like a clearing mandate for the Treasury market, seek to reduce the intermediation frictions that generated this crisis without wholesale changes to the regulatory framework, but require quite a bit of further study and are unlikely to be a practical solution for some time.

This all means the coming months will likely represent a balancing act, ensuring the safety and soundness of the banking system on the one hand, while seeking to minimize the financial stability risk associated with market dysfunction on the other. The only fundamental change is the Fed’s clear willingness to do what is needed when financial stability is threatened by these dynamics. Though things are calmer now, there is no way to rule out them being called upon to do so again.