Revisiting the Ides of March, Part I: A Thousand Year Flood

By experts and staff

- Published

- Guest Blogger for Brad Setser

This is a guest blog by Josh Younger, an interest rate strategist at J.P. Morgan. Joshua Younger is employed by the Research Department of J.P. Morgan Chase & Co. All views expressed in this forum are his own and may not align with those of the firm, but they are consistent with all research publications published under the firm brand for which he is listed as an author. This is part one of a three part series.

Brad Setser notes that he believes this work is of great interest to the general public, given the scale of the market disruption in March.

Among other superlatives that can be assigned to the COVID-19 pandemic, the re-pricing of global financial assets to reflect its economic implications was arguably the most rapid and unexpected of the modern era.

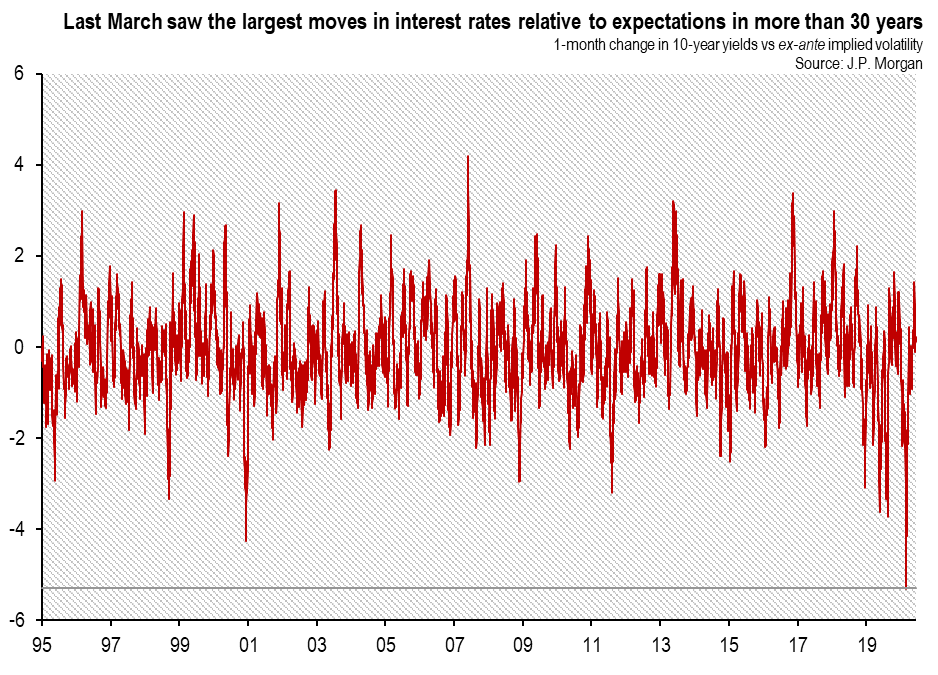

For fixed income markets in particular, these moves were multiples of what the market considered plausible in the months prior. The decline in 10-year Treasury yields over the month ending in mid-March, for example, was nearly six times that implied by the cost of buying protection against those moves in the options market.

By this measure—volatility-adjusted price change—that was the largest re-pricing of any monthly period in at least 30 years (CHART 1). This uniquely fast pace was consistent with the combination of a uniquely fast-moving event—even financial crises cannot approach the exponential growth exhibited by disease epidemics—and much more severe economic consequences—a synchronized global economic shutdown. Financial asset returns are famously fat-tailed, but a surprise of that magnitude should still be exceedingly rare. Even a conservative interpretation of the statistics suggests they should only occur once every thousand years or so.

As a general matter, very large intraday price swings complicate the process of connecting buyers and sellers—market making. This reflects the fact that in many markets, including Treasuries, there is typically a time lag between the acquisition and placement of a security. If prices decline over that period, short though it may be, market makers could be forced to sell for less than what they paid, resulting in a loss.

Traders guard against this risk to some degree by offering bonds for sale (the offer) at a higher price than they can buy them in the market (the bid). In principle they can widen this bid/ask spread to accommodate larger expected short-term price swings. But when volatility is rising, it can be difficult to keep up, and even a few minutes can quickly lead to significant losses. When market making risks becoming a money-losing enterprise, the solution is simple: reduce the size and/or pace of transactions or, in the extreme, simply stop trading all together.

Though this was just as true of the street markets of medieval Paris as it is today, in modern electronic trading it is exacerbated by increased reliance on algorithms. Often referred to collectively as high frequency traders (HFTs), these computerized systems engage in an enormous number of transactions a day but only hold those positions for (ideally) a fraction of a second. That means their ideal environment is one of relatively stable prices and heavy volumes, so they can effectively monetize the bid/ask spread many times over.

These strategies dominate activity across a number of markets, including Treasuries where the top four counterparties are far from household names and make up more than 60 percent of these transactions. HFT-style trading is also not limited to these dedicated outfits (i.e., principal trading firms, or PTFs)—many large bank-affiliated dealers now employ similar strategies for at least part of their market making business.

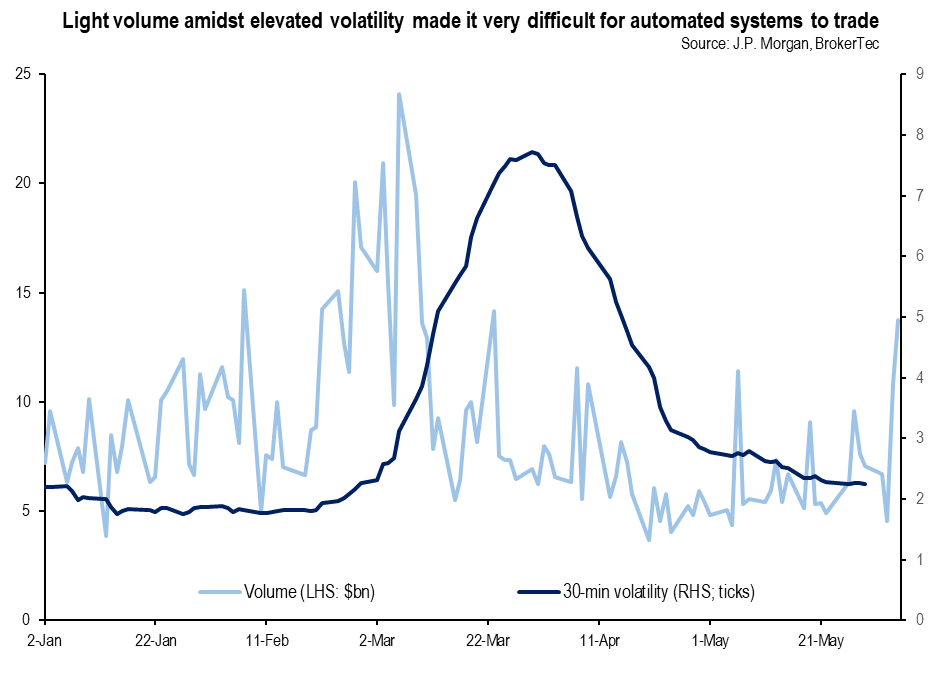

HFT models have been quite successful in the relatively calm waters of the past few years, and they have grown to make up the vast majority of liquidity provided in the Treasury market. That means that ability to buy and sell large volumes at low cost has become increasingly dependent on their involvement. That all came crashing down in March as not only did prices oscillate violently over the course of the trading day, but the level of activity dried up as well (CHART 2).

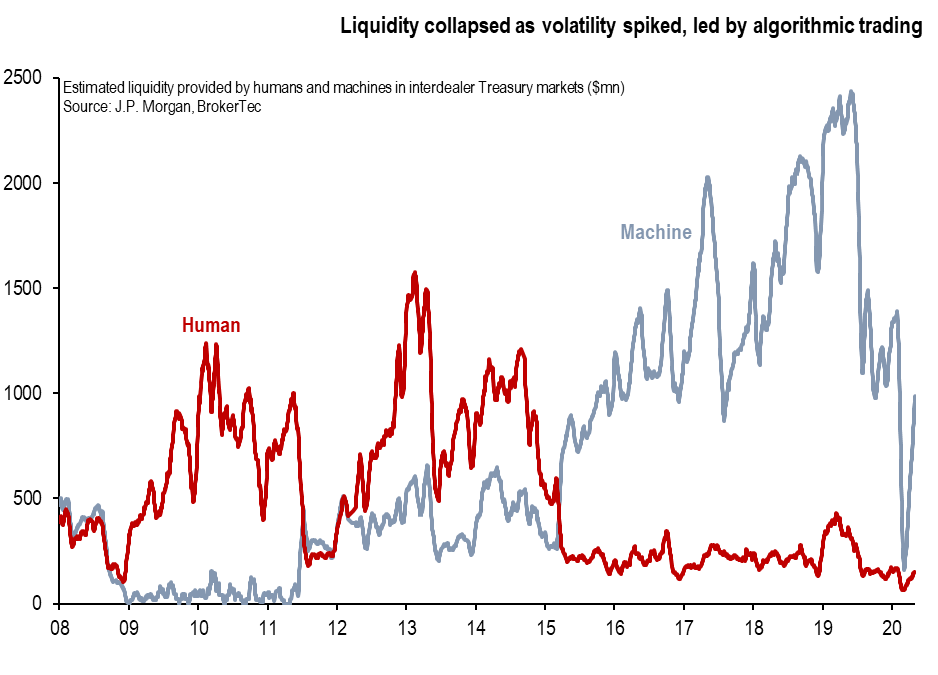

With fewer opportunities to profit from connecting buyers and sellers, and a much greater risk of losing money in the meantime, HFT-style market makers pulled back abruptly and in some cases likely shut down entirely. Thus the liquidity they provided dropped to a tiny fraction of its previous peak over the first couple weeks of March (CHART 3).

When liquidity dries up, activity tends to migrate to the deepest, most actively traded, most transparent, and fungible product. For interest rates, that typically means Treasury futures, which are a contractual agreement to buy or sell a Treasury security on future date.

These instruments have many advantages during periods of stress, not least among them the fact that they are a derivative rather than a ‘cash’ instrument, and that means they effectively offer leverage (aside from the required margin of course). If you need to quickly hedge significant interest rate risk without locking up or borrowing a lot of cash, this is an immensely valuable feature.

When the going gets tough enough, this dynamic can have an impact on the relative pricing of different fixed income products with very similar underlying risk profiles, which we often refer to as liquidity tiering. Futures in particular tend to lead in disorderly market moves—dropping in price more than similar securities when interest rates are rising, and vice versa when they are falling. This is typically quantified by tracking the difference, or basis, between the futures contract price and the bond that is optimal (i.e., cheapest) to deliver into that contract (the cheapest-to-deliver, or CTD). Market convention is to quote the so-called cash/futures basis as the price of the CTD (with some adjustments, which we will not belabor here) minus that of the futures. Therefore, a drop in the value of this measure represents the outperformance of the futures contract.

We are not talking about massive numbers here: among those who traffic in such things, even a 0.5 percent change in the pricing of futures relative to their CTD is considered a very large move indeed! But, as we will see, under the right circumstances even such a small discrepancy can have massive consequences.

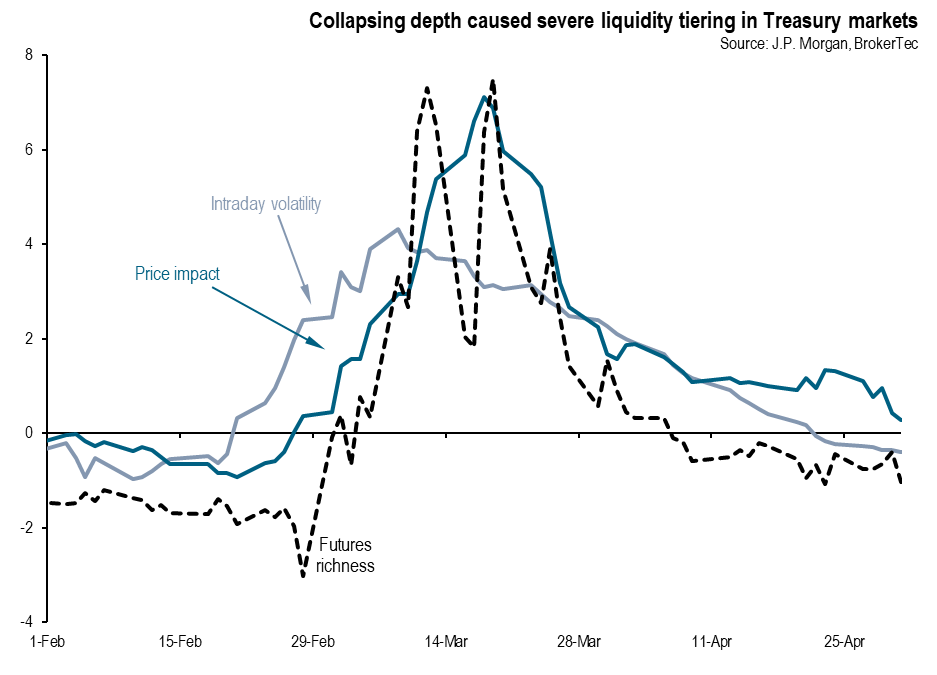

That leaves us with a sequence of events that should look very familiar to any interest rate trader: a spike in volatility led to a collapse in market depth and then a re-pricing of the cash/futures basis (CHART 4)*. Though markets had weathered episodes of severe illiquidity several times since 2008, financial stability was never directly threatened.

This time was different, and anything but familiar. A confluence of events triggered by small shifts in relative pricing of different fixed income instruments ultimately threatened a financial crisis and disorderly deleveraging of the banking system in the middle of a historic shock to the real economy. The key lay in long dormant, highly levered positions held by professional investors but previously dismissed as having little impact on the market (if they were aware of it at all).

* Price impact is a complementary measure of liquidity to market depth, and quantifies the expected change in price for a imbalance of buyers versus sellers. More details on various measures of liquidity are available here.