Revisiting the Ides of March, Part II: The Going Gets Weird

By experts and staff

- Published

- Guest Blogger for Brad Setser

This is a guest blog by Josh Younger, an interest rate strategist at J.P. Morgan. Joshua Younger is employed by the Research Department of J.P. Morgan Chase & Co. All views expressed in this forum are his own and may not align with those of the firm, but they are consistent with all research publications published under the firm brand for which he is listed as an author. This is part two of a three part series.

In Part I of this series, we described how liquidity collapsed as markets were forced to rapidly come to grips with the economic implications of a global pandemic. That was arguably nothing new, however. Recent memory includes at least a few episodes: the 2008 financial crisis of course, several episodes related to the Euro crisis, the downgrade of the U.S. government’s credit rating, the ‘taper tantrum,’ the devaluation of the Chinese Yuan, Brexit, and the 2016 U.S. Presidential Election, just to name a few.

Things really started to come apart this time around in a relatively obscure corner of financial markets. Hedge funds and other ‘sophisticated’ investors often hold short positions in futures (a contractual agreement to sell those bonds on some future date) against levered positions in the bonds they reference. Liquidity tiering among different fixed income instruments favored futures as the preferred hedging vehicle, leading to a widening price discrepancy between those contracts and the bonds in their deliverable basket.

This had happened before, but there were a few key differences this time around. The net result threatened a new kind of financial crisis—one of collateral quantity rather than quality—which had the potential to be broader then the kind of disorderly systemic delevering policymakers had fought so hard to avoid in 2008.

Why did these positions exist at all? Trading bonds versus futures has been at the core of relative value strategies in fixed income for decades. When prices on the futures are too high compared to the securities one can deliver, for example, there is money to be made in shorting the futures and buying securities—and vice versa when they were too low. This effectively enforces the tight theoretical relationship that should exist between these two connected instruments.

Such trades were generally considered very low risk because losses should be limited; a short futures positions represents a committed buyer, and bonds can simply be delivered at the appointed time. Potential gains are small as well—only a few tenths of a percent.

Thus, cash/futures basis trades tend to be very highly levered (20 or even 50 to 1, or more): securities are purchased using short-term borrowed funds for which they are pledged as collateral (repurchase agreements, or repos; often for no-money-down), and initial margin on the futures leg tends to be small (a few percent of notional, and potentially less if optimized against other positions).

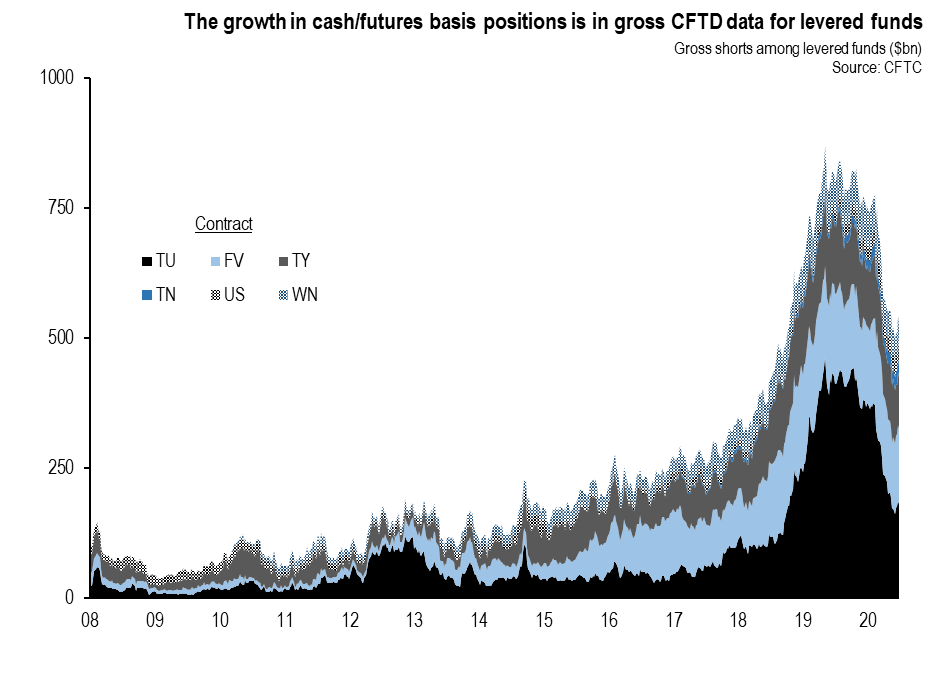

How large are these cash/futures positions? A full accounting is not possible with public data, but the impact can be seen in net positioning reports released by the CFTC. Gross short positions among ‘levered funds’ increased from less than $100bn in early-2010 to a peak of nearly $875bn in mid-2019 and still around $750-800bn to start this year (CHART 1).

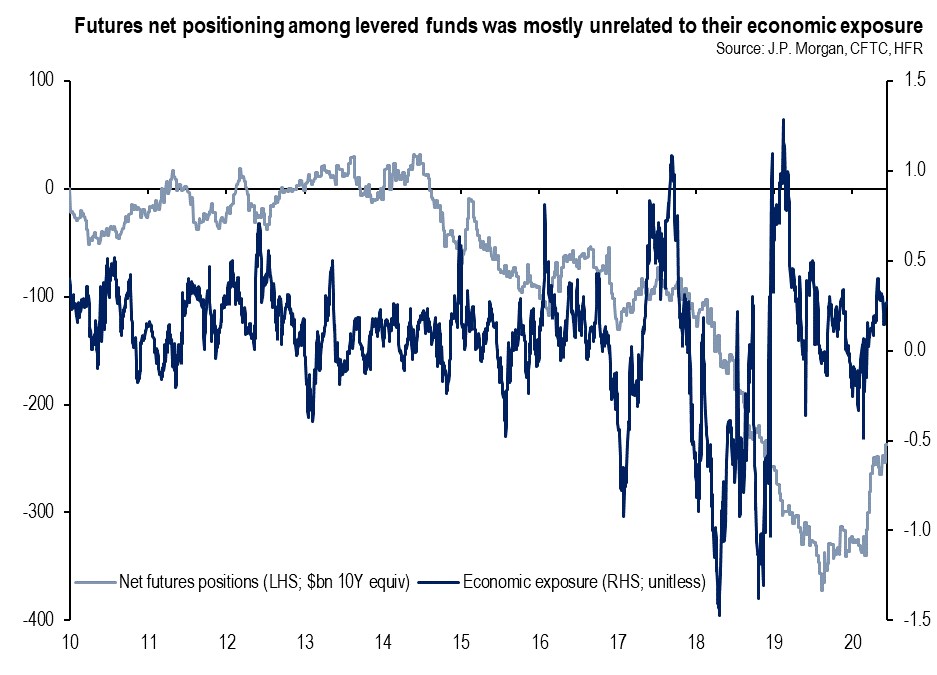

That this was related to basis trading is clear from the decoupling of positioning from economic exposure to moves in interest rates (CHART 2). In other words, hedge funds appeared to be accumulating larger and larger net short positions in futures even as their overall returns reflected a mix of net long and short exposure over time. This suggests another position that is not visible in the futures data—e.g., longs in securities, likely financed with repo.

Why would this position grow so rapidly? If anything relative value opportunities were fewer and further between over the past ten years, in no small part due to the heavy involvement from the Fed.

Rather than economic motivations, it had to do with shifting incentives imposed by new regulations.

After the 2008 crisis, new rules put in place to address Too Big to Fail (TBTF) subsidized the social cost of size and complexity with capital surcharges that were agnostic to risk. Total leverage, for example, was measured capital against all assets, including Treasuries and cash. That made certain types of low-margin/low-risk transactions, like Treasury repo, potentially capital intensive.

Banks responded by planning ahead, often offering repo to clients on a ‘use-it-or-lose-it’ basis. From the client perspective, that incentivized using their allocation without taking much market risk. Basis positions, with their repo-financed bond leg and theoretically limited downside, were ideal placeholders with which to maintain access to leverage in the event it was needed on some future date.

Under normal circumstances, the dislocation in basis pricing that emerged in early March could be assumed to naturally resolve over time. The holders of these levered bond positions still had a committed buyer in the counterparty to their short futures contract.

That is, if they could hold both legs until the delivery period. Hanging on was rapidly becoming far more complicated than anyone anticipated. As the pandemic accelerated and many dealers were forced to transition quickly to work-from-home arrangements, there was a risk that certain types of trades could get lost in the shuffle. Repo is particularly operationally intensive, and had suffered disruptions in the past (for example, September 2001). Hedge funds feared they could be forced out of basis trades early, and at a significant loss. Thus, focus shifted from managing market risk to managing operational risk.

Even if in practice one thought that forced early unwinds were unlikely, the potential for others to come to that conclusion and unwind meant prices could become even more dislocated, and losses much larger. By mid-March, cash/futures basis pricing already implied 10-20 percent losses on some positions, and potentially more depending on the portfolio composition. The way things were going, it could have gotten much worse from there. For placeholders with little economic value, this was concerning to say the least.

A classic run dynamic was taking hold.

A full accounting of what came next is once again not possible with public data, but the evidence is clear. CFTC positioning data shows a roughly $200bn decline in gross short futures positions among levered funds in March and April.

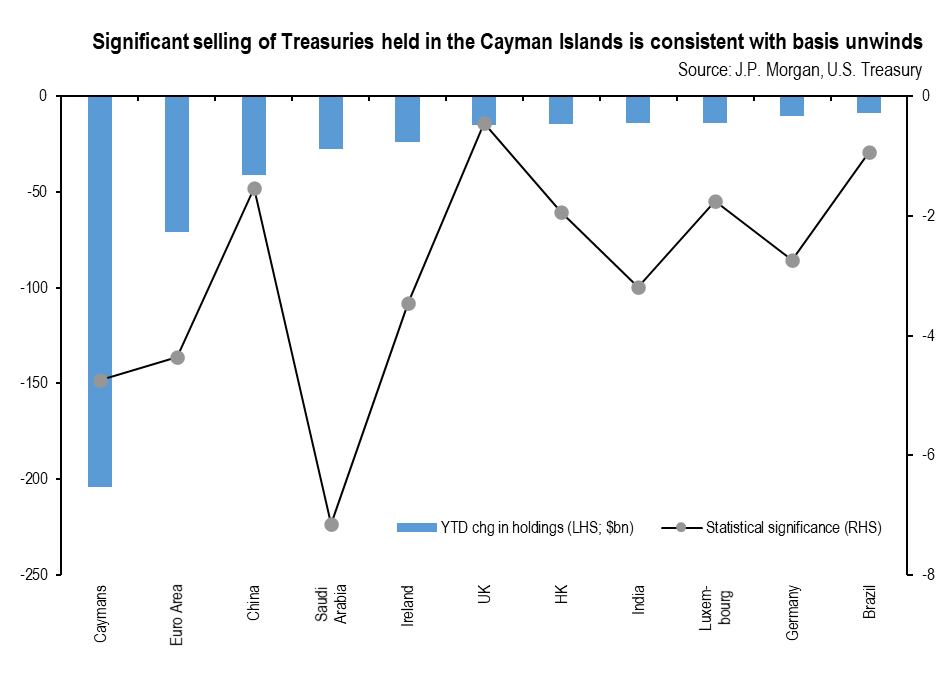

Over the same period, the Cayman Islands (a very common domicile for hedge funds) was a net seller of just over $200bn in Treasury securities YTD—a more than 4-sigma event—despite the fact that prices were rising rapidly (CHART 3).

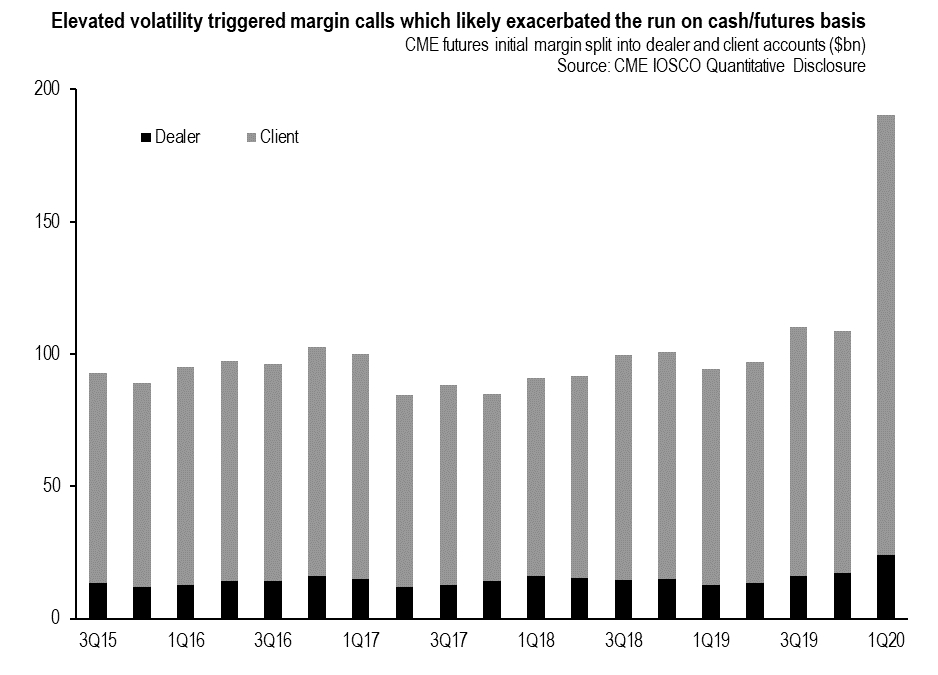

Margin calls likely accelerated this process: in late-March, the Chicago Mercantile Exchange (CME; the clearinghouse for Treasury futures) increased the funds required to maintain existing futures positions, forcing hedge funds and others to come up with as much as $75bn in additional cash in just a couple of days (CHART 4; also discussed here).

Though futures can be collapsed in an unwind—a short paired with a long position in the same contract becomes no position at all—securities always end up on someone’s balance sheet.

In an ideal world, market makers would be pure intermediaries, lining up buyers and sellers in advance. When a match cannot be made quickly, however, the bonds reside on dealer balance sheets. Because most of that activity occurs among bank-affiliated dealers, this inventory is constrained by the same size and complexity regulations as other activities. At a certain point, these increasing capital charges make it more expensive to intermediate subsequent transfers, which is often priced into overall transaction costs.

This materialized in rather dramatic fashion in March.

Though yields were declining, and therefore Treasury prices increasing, that arguably had more to do with a shift in monetary policy expectations (zero or even negative short-term interest rates for an extended period, quantitative easing and even yield curve control) than a fundamental shift in the supply/demand balance among longer-term investors.

In fact, if anything foreign central banks, a key component of demand for Treasury bonds, were significant sellers throughout the decline in yields (as discussed in a recent post by Brad Setser in this blog). Basis trade unwinds added to already heavy inventories, reducing capacity and exponentially increasing the costs of intermediation. The impact was greatest in longer maturity securities: the bid/ask spread (a measure of transaction costs) that dealers charged each other to trade 30-year Treasuries, for example, was 20x larger than typical levels for a few days in March. The shock percolated across the Treasury yield curve such that the relationship between otherwise very similar securities became very volatile and uncertain (CHART 5). As many observed at the time, Treasuries were suddenly trading more like emerging market debt than obligations backed by the full faith and credit of the U.S. government (see a related discussion here).

Large risk transfers have, of course, occurred many times in the past. While they can have a significant impact on prices, they do not typically threaten financial stability. But the scale of the breakdown in market functioning in mid-March was unprecedented, and threatened a new kind of financial crisis—one driven not by the quality of collateral used for short-term lending, like in 2008, but one in which the quantity sloshing around on bank balance sheets risked becoming destabilizing.

Though at first glance the events of March bear little resemblance to the Lehman bankruptcy, the risk they posed were very similar: a disorderly delevering of the banking system, including fire-sales of otherwise high quality assets, in the midst of a historic shock to the real economy.

How could a disruption in the Treasury market expand to envelope the system as a whole? And how did we avoid the most destructive outcomes? We explore that in our third and final installment.