U.S. Trade Deficit Stable in Q1

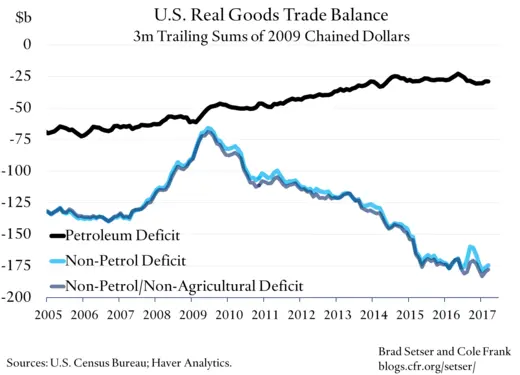

The U.S. trade deficit did not change much in the first quarter. The real (price adjusted) goods deficit that is. Oil prices were a bit higher in q1 than q4 (they are now back below their q4 levels, but that will impact the June and July data)

The quarterly real non-petrol deficit has basically been constant—with a soybean specific story explaining the fall in the Q3 deficit. The non-petrol deficit excluding agriculture hasn’t moved much.

Frankly I am a little surprised. I would have expected the lagged impact of the 2014 rise in the dollar (the broad real dollar is up 18 percent since mid 2014) to still be having a bit of an impact on the 2017 data—and also to see an ongoing drag on exports so long as the dollar stays at its current (appreciated) level.

But that didn’t obviously happen in the first quarter.

Though I would argue that the real trade deficit is slowing getting bigger if you look past the impact of the q3 soybean export surge, albeit at a much slower pace than in 2015.

The relative stability of the trade deficit in early 2016 came from weakness in U.S. real imports. That offset the weakness in US real exports. In the last couple of quarters, the story has changed a bit. Real imports have started to flow, but so too have real exports.

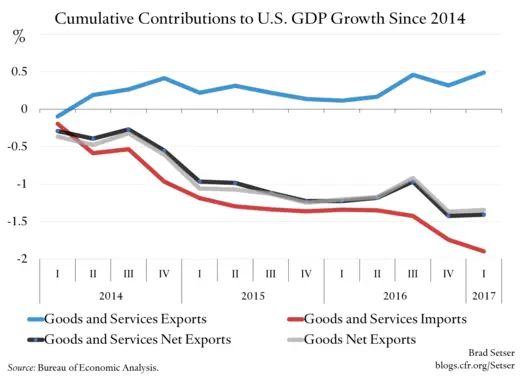

A plot of the cumulative contribution of net exports to U.S. GDP growth since the start of 2014 makes this clear. Net exports over this time have, mechanically, subtracted about 1.5 percent from U.S. growth—with most of the deterioration coming in late 2014 and early 2015, just after the dollar strengthened. There hasn’t been much further deterioration. Net exports knocked about 20 basis points off growth over the course of 2016, and were basically flat.

I am inclined to stick to my original forecast, one based on the expectation that there is still a bit more deterioration in the U.S. trade balance baked in because of the dollar’s past appreciation. I would expect a 18 percent move in the real exchange rate to raise the real trade deficit by a bit more than 2 percent of GDP over three or so years (a standard rule of thumb is that a 10 percent move in the real effective exchange rate changes the non-oil trade balance by between 1 and 1.5 pp of GDP; the Fed’s trade model for example suggests that a 10% exchange rate move knocks 1.5 percent off net exports. That is also the IMF’s central estimate).* I expect the trade deficit to widen a bit in the next few quarters.

But for now the data shows a somewhat smaller expansion of the trade deficit than I would expect given the size of the dollar’s appreciation.

P.S. last year I thought the US real petrol deficit was heading up on a sustained basis. That forecast hinged on an assumption that $45-55 oil would keep U.S. production at best constant. The oil sector has outperformed—with a sizeable increase in drilling coming at a lower price point than I expected. I no longer expect the petrol deficit to rise.

* Bill Cline of the Peterson Institute also projected a deterioration in the non-oil balance of around 2 percent of GDP. See his 2016 policy brief, and in particular figure A3.