Beware Friendly Fire in the Currency Wars

By experts and staff

- Published

Experts

![]() By Benn SteilSenior Fellow and Director of International Economics

By Benn SteilSenior Fellow and Director of International Economics

By

- Dinah WalkerAnalyst, Geoeconomics

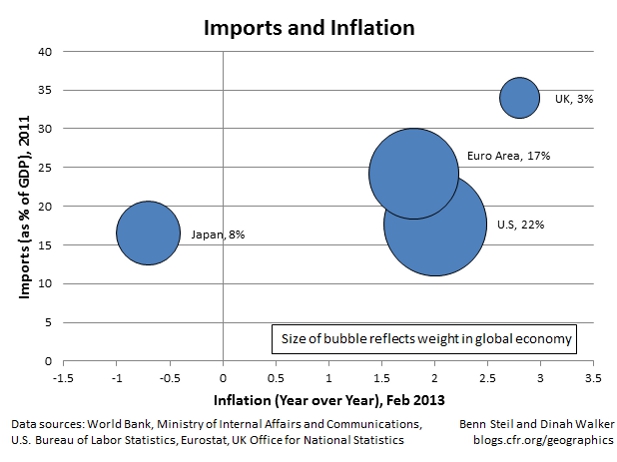

Prominent economic commentators have argued the cases for significantly weaker currencies in each of the world’s major economies – in particular, the United States, the eurozone, Japan, and the UK. As these four economies represent over half of the global economy, it’s clear that they can’t all accomplish this feat. It’s also far from clear that they should all want to.

Take the UK, where the FT’s Martin Wolf has led the charge for “further depreciation of the real exchange rate.” John Maynard Keynes, belying his reputation as a devaluationist, had argued passionately against a weaker pound in 1945 on the basis of terms of trade: that is, the UK would, broadly, have to give up more domestic goods in return for the same quantity of foreign goods. “In [our] circumstances, you can’t imagine anything more foolish,” he said, “than to be trying to sell [our] exports at quite unnecessarily low prices.” Today he might highlight inflation. As shown in today’s Geo-Graphic, currency depreciation is likely to have a much more adverse effect on inflation in the UK than in the United States, the eurozone, or Japan, owing to much higher imports relative to GDP. UK consumer price inflation is already running at a relatively high 2.8%, and the Bank of England’s own analysis suggests that a 20% sterling depreciation risks pushing the price level up 6 percentage points higher than it would otherwise be.