China’s “Fake” De-Dollarization

China didn’t truly de-dollarize—it just shifted its dollar holdings from official reserves at SAFE to less transparent state entities like banks and investment funds.

Back in 2005, China held 79 percent of its growing reserve portfolio in dollars.

In 2024, China disclosed that by 2019 only 55 percent of its now stagnant reserves were in dollars.

That is the last disclosed data point, but careful analysis of the U.S. Treasury’s data essentially rules out a significant rise in the dollar share of China’s formal reserves. The U.S. data is consistent with either a bit of a fall or very aggressive use of non-U.S. custodians over the last five years.

So, China has de-dollarized? Not exactly.

The big fall in the dollar share of China reserves (from 79 to 59 percent) occurred between 2005 and 2012 (though China only disclosed the 2015 number) and during that period China’s toal reserves went from $800 to close to well over $3 trillion and its actual dollars continued to rise.

Reserves rose from 2012 to 2014 before falling sharply in 2015 and 2016. But reserves now have been stuck at just over $3 trillion for the last 8 years. Subsequent fluctuations in the dollar share of reserves haven’t been all that material to the global flow of funds; a change of a hundred billion or so over spread over a multi-year period should not move markets much.

More importantly, China has played a bit of a game. It reduced the dollar share of its formal reserves.

But it then stopped adding to its formal reserves.

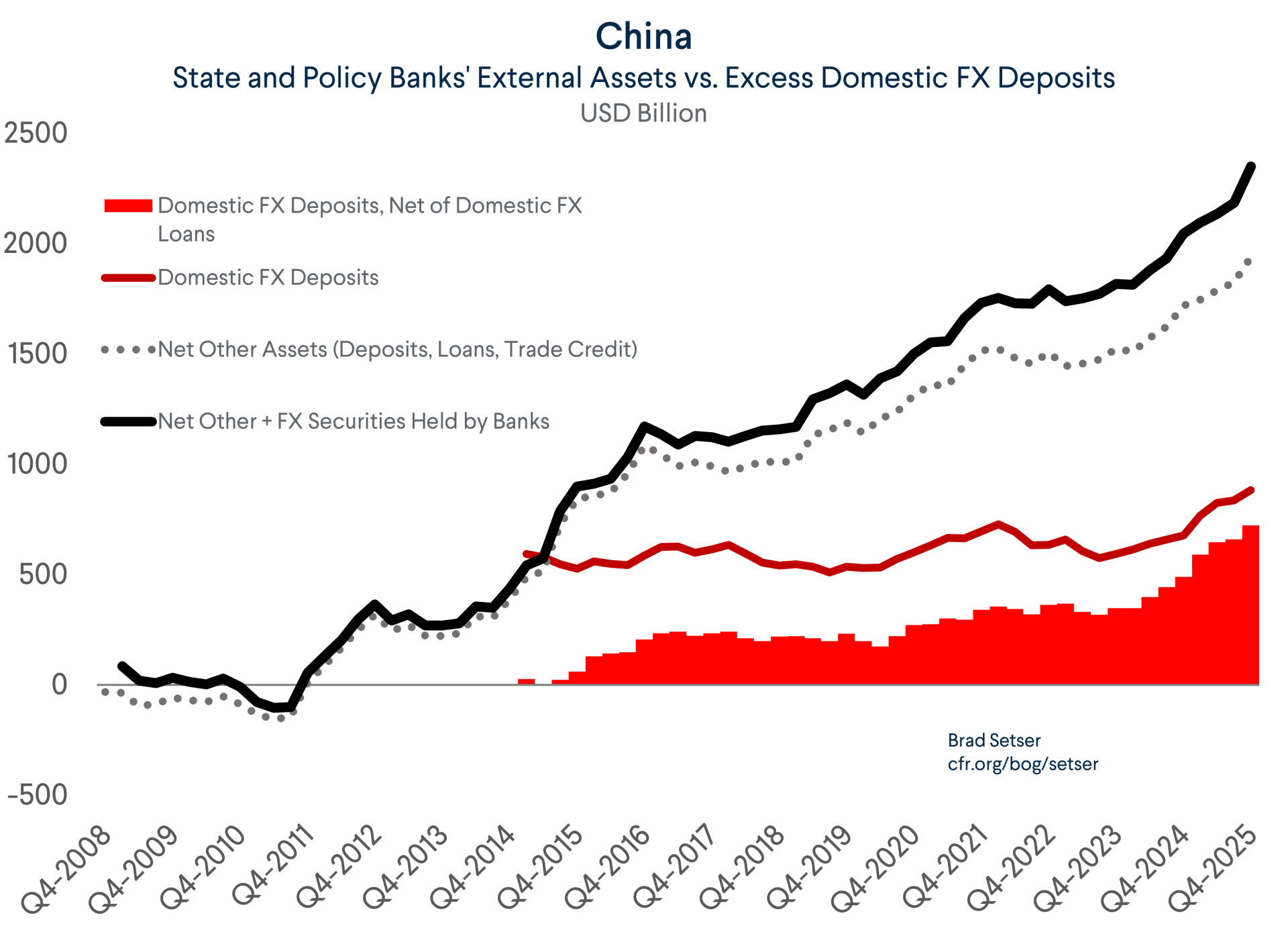

All incremental growth in the foreign assets of China, Inc. has come from the increase in foreign lending of the policy banks (domestically funded), the increase in the foreign and foreign currency assets of the state commercial banks (also mostly domestically funded) and increases in the assets of various state investment funds (the State Administration of Foreign Exchange’s Buttonwood Investments vehicle has put dollars into a set of funds that support the Belt and Road and Chinese firms “going out”).

Now, China doesn’t disclose full data about the currency composition of the broader Chinese state. In fact, there is essentially no useful public information about the country or currency composition of the obviously substantial foreign assets of China’s policy banks.*

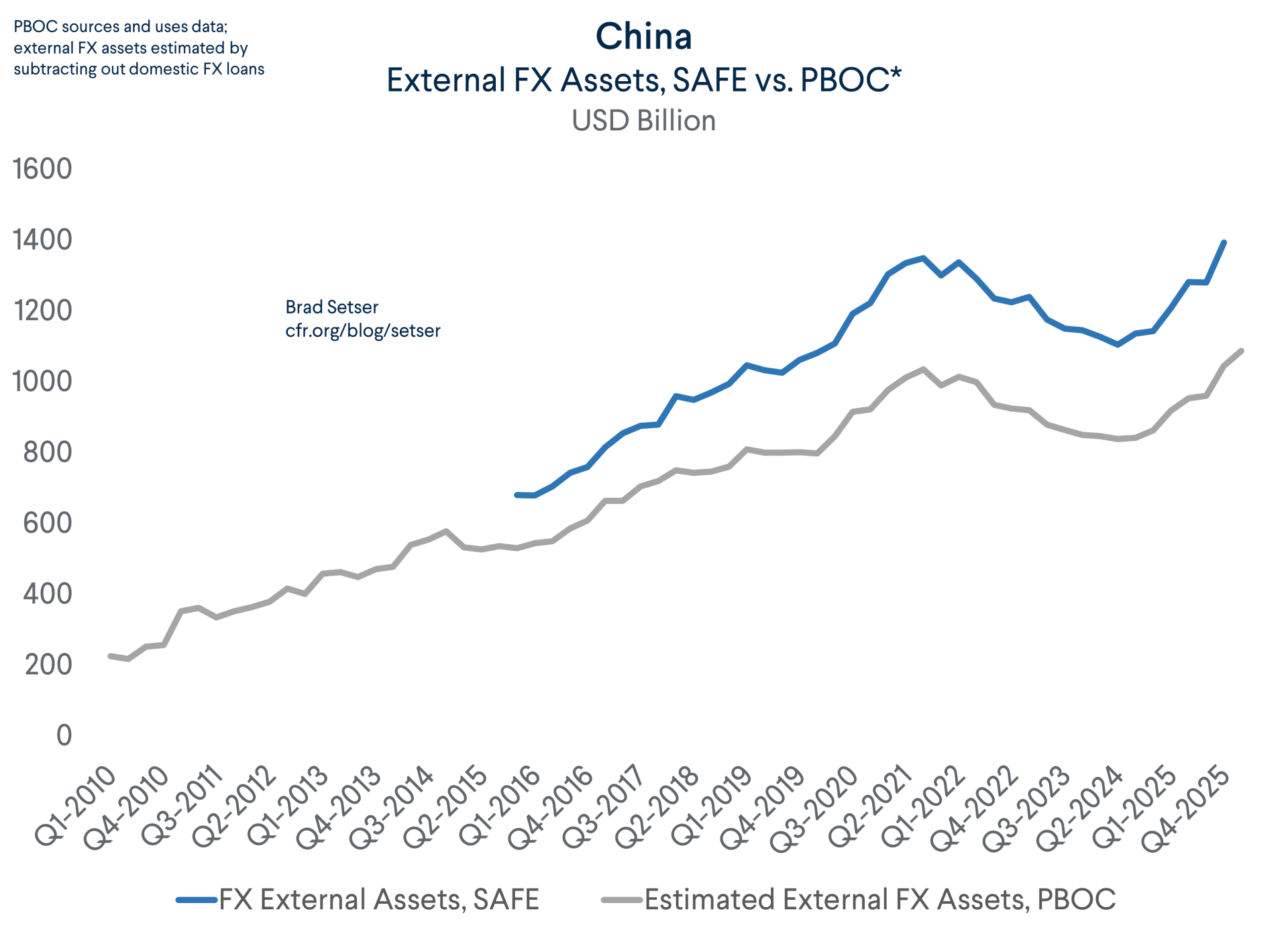

Moreover, the data on the foreign assets of the deposit-taking state commercial banks isn’t presented in the cleanest matter. One dataset includes yuan-denominated foreign assets, another includes foreign currency-denominated domestic assets, and the quarterly data set that provides a breakdown of foreign currency and yuan-denominated external assets doesn’t line up with the monthly data.**

But all the available data indicates that, until recently, the bulk of the policy banks’ lending was in dollars. That has certainly been true in the various “restructuring” cases (Zambia, Sri Lanka, Ecuador, and Angola had dollar exposure—not yuan or euro exposure—to China’s policy banks). The recent restructuring of a few loans to Kenya into yuan is welcome, but not enough to really change the overall numbers.

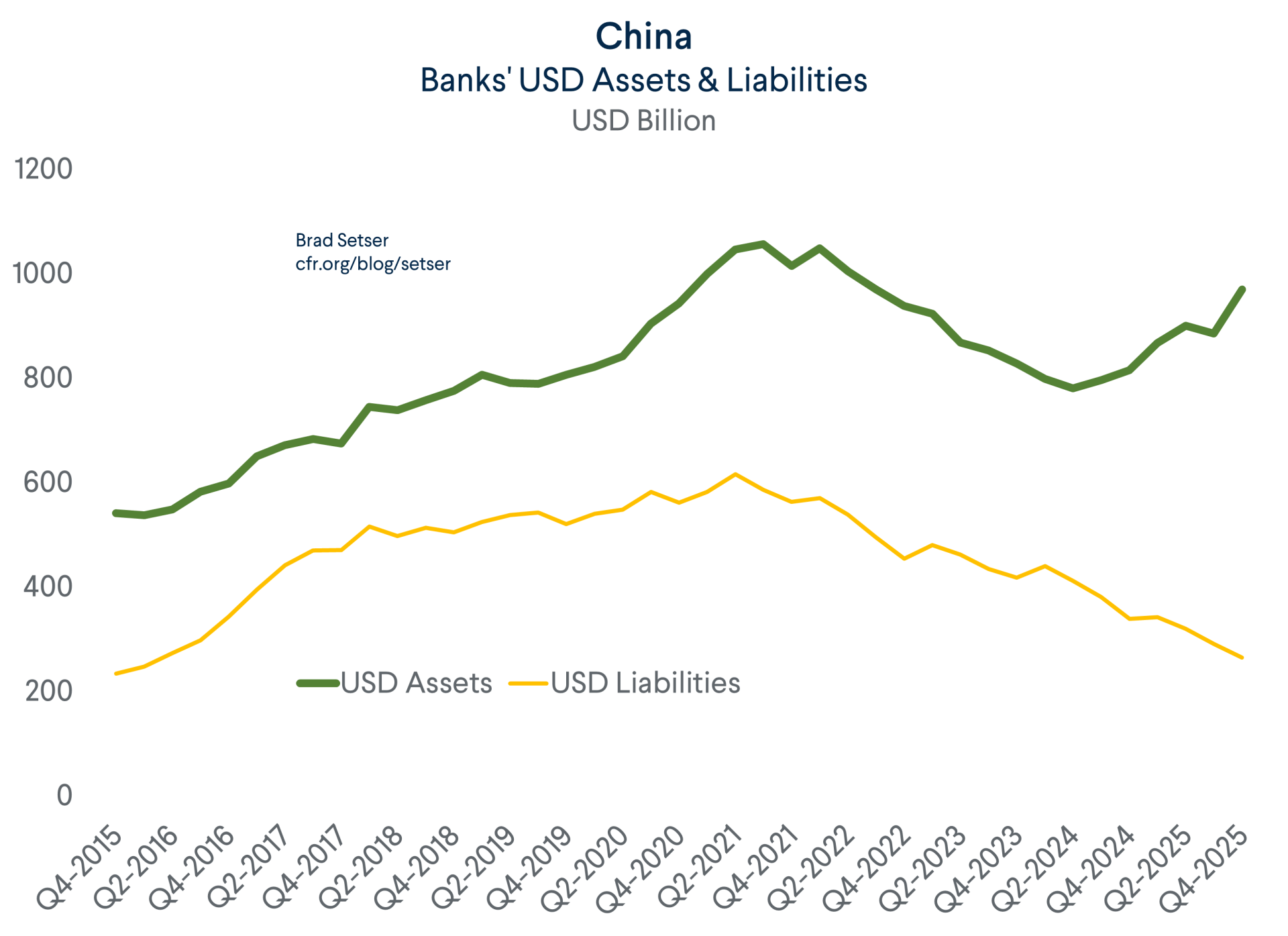

SAFE’s published data suggests that the state commercial banks have roughly 70 percent of their foreign currency assets in dollars (well above SAFE’s dollar share). But that probably understates the state banks’ impact on their dollar market. The state banks’ euro, yen, and other non-dollar foreign currency assets are matched by external euro, yen, and other non-dollar foreign currency denominated liabilities. So, the state banks in aggregate look to be borrowing euros and other currencies to invest in euros and other currencies abroad.

Conversely, dollar assets abroad have been rising even as the banks‘ external dollar borrowing has fallen.

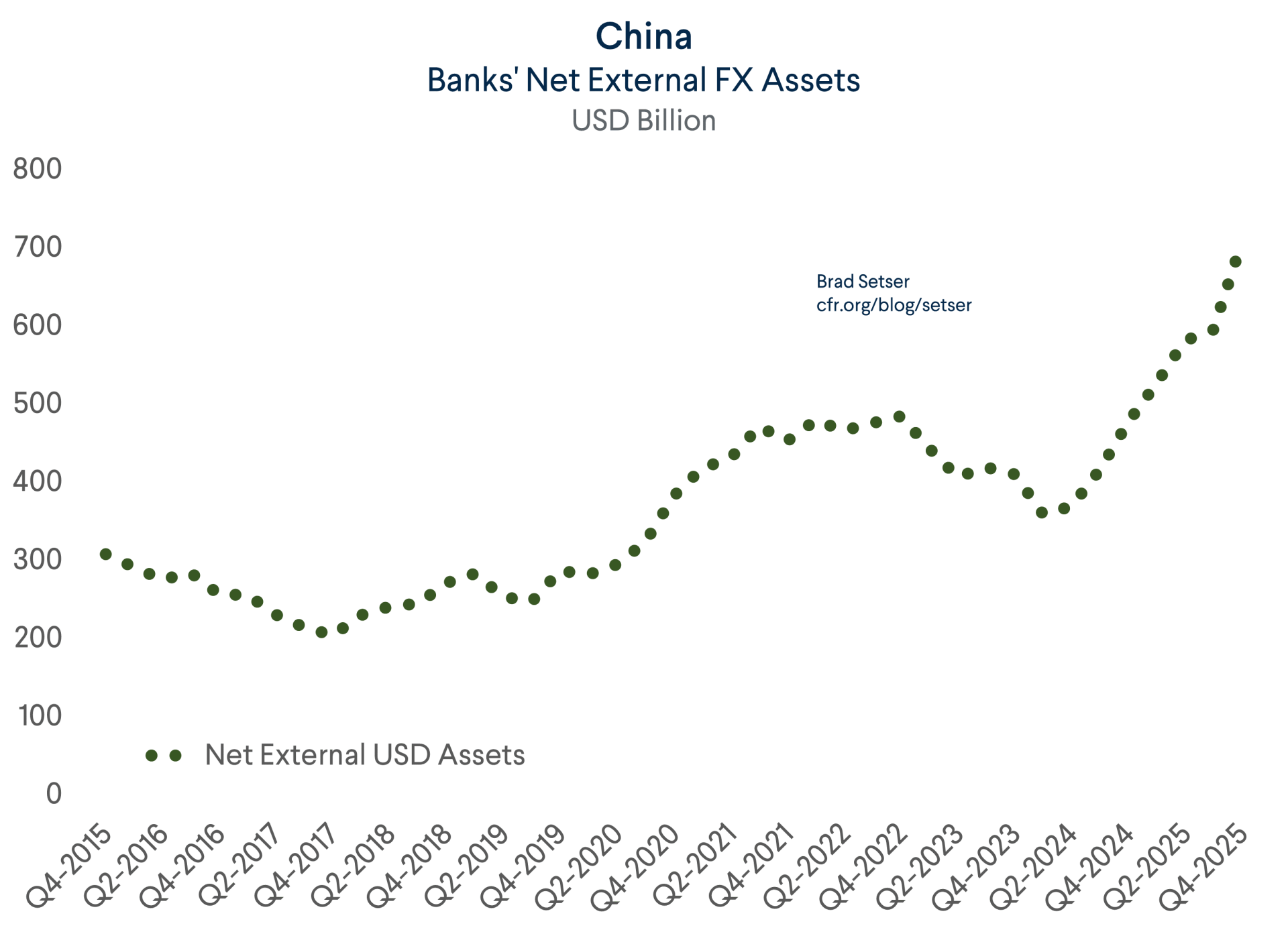

The back door “intervention” consistent external portfolio (i.e. the state banks’ foreign assets that are somehow funded internally) is all in dollars.*** And the net external dollar position was above $700 billion at the end of last year and rising fast (it should be higher when the end Q1 data is released; the banking data shows a $50 billion rise in foreign currency external assets).

A bit of ballpark math is now needed.

55 percent of China’s $3.3 trillion in reserves is roughly $1.8 trillion. That is a reasonable estimate of SAFE’s dollar holdings (which include a decent chunk of U.S. equities; it isn’t all in fixed income).

SAFE’s quarterly data shows state commercial banks had $1 trillion in dollar assets (versus $300 billion in dollar liabilities abroad) at the end of Q4, and probably more like $1.1 trillion in dollar assets now.

The policy banks have an undisclosed foreign portfolio. But AIDdata estimated that they could hold close to $1 trillion in claims on the world—and most of those seem to be in dollars.

And, of course, the bulk of the China Investment Corporation’s (CIC) private equity investments will be dollar-based. That suggests that the bulk of the CIC’s $450 billion in foreign assets are dollars.****

Sum it up, and China, Inc. could hold more dollars off SAFE’s balance sheet than on SAFE’s balance sheet.

Nice little trick.

It seems to have fooled most of the internet.

* The IMF hasn’t wanted to press about how the policy banks raise funds for external lending, it seems; it hasn’t been the subject of any IMF research even though it would seem to be critical for the IMF’s understanding a number of policy issues. Tooze argues that the IMF opts to avoid some controversial topics with China; this may be one of them.

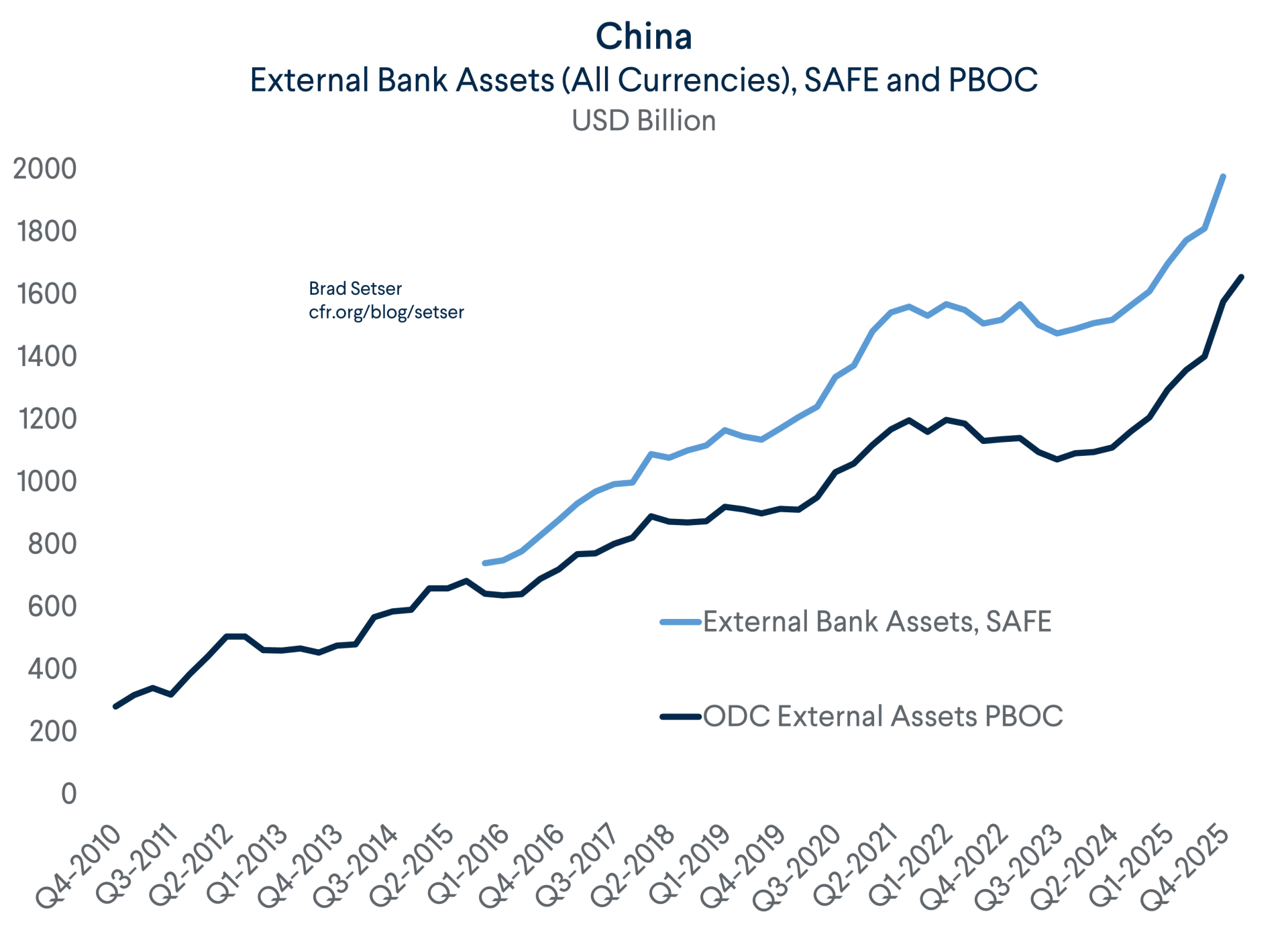

** SAFE’s data set on the external assets and liabilities of the state banks shows more assets and liabilities than the central’s bank data set on the foreign assets of the state commercial banks (other depository corporations). The difference, however, is bigger on the liability side (in yuan) than on the asset side. The SAFE series shows more foreign assets than the PBOC series, but the changes now line.

Same if the numbers on foreign currency assets are compared to the relevant PBOC data set.

*** Foreign assets that are funded out of deposits need not be intervention, though China is now somewhat unique in that its domestic FX deposits are overwhelmingly backed by external FX assets. The stock of available deposits falls far short of measures of the banks’ total foreign assets. That includes the policy banks, so there is more going on than simple intermediation. And the deposit series is itself a little strange; it rose strongly from 2019 to 2021 even though CNY interest rates exceeded dollar interest rates, and fell in 2022 and 2023 even as the Fed raised rates and the PBOC cut rates. It looks a lot more like a data series influenced by backdoor intervention than a series driven by organic demand for dollars. See this blog for more.

**** It is less clear with SAFE’s investment vehicles; they initially were funded out of dollars, but now likely have equity stakes in various Chinese investments around the world.