The ECB Fails to Stress Banks Over the One Critical Variable It Controls: Inflation

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Dinah WalkerAnalyst, Geoeconomics

Relentlessly falling inflation is bad news for Eurozone banks. It increases the real (inflation-adjusted) value of borrower debt and the real cost of servicing that debt. It causes loan defaults, and therefore bank loan losses, to rise.

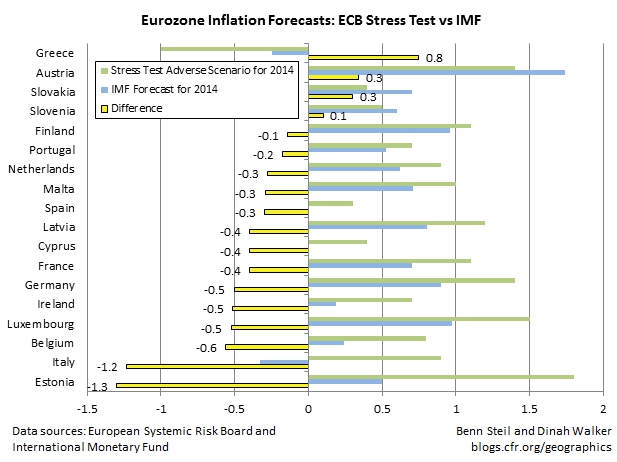

So with Eurozone inflation, currently at a near-record low of 0.4%, clearly at risk of heading into deflationary territory, what did the ECB say was the “adverse scenario” for this year? Inflation of 1% – more than twice its current level. This is indefensible; the ECB’s dire scenario for this year is actually much cheerier than the IMF’s baseline forecast, which pegs inflation at 0.5%. The country-by-country comparison is shown in the graphic above.

Disturbingly, at no point through the end of 2016 is the ECB even willing to contemplate the possibility of inflation being less than it already was in September: 0.3%. This is a serious failure on the part of the central bank, which this month assumes supervisory responsibility for Eurozone banks. It suggests that the ECB is more concerned with the reputational costs of acknowledging the possibility of deflation than with testing accurately the ability of banks to withstand it. As the private sector is not privy to the proprietary bank data that would allow such a proper test, the ECB’s failure to address deflation risks raises the critical unanswerable question of how many of the seven banks that barely passed should actually have failed.

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”