ECB Rate Cut a No-Brainer; Also, for Many, a No-Gainer

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Dinah WalkerAnalyst, Geoeconomics

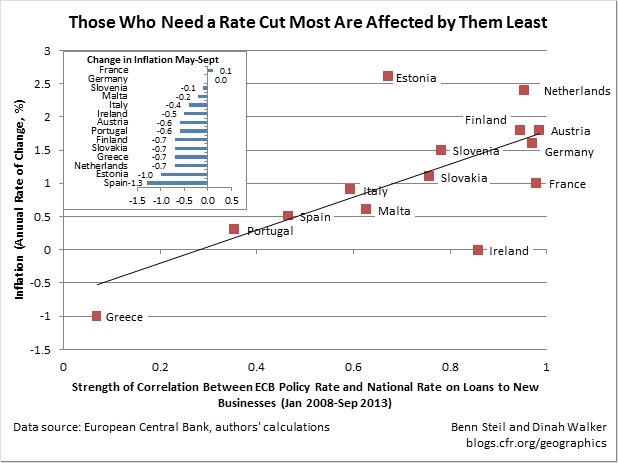

Back in April, we showed that the eurozone countries most in need of lower corporate borrowing rates benefited only marginally from ECB rate cuts. Today’s Geo-Graphic shows that little has changed in this regard; the financial crisis has clearly done serious and lasting damage to the monetary transmission mechanism in Europe – particularly as it affects Greece, Portugal, Spain, and Italy.

In April we also showed that the GDP-weighted inflation rate of the countries where the monetary transmission mechanism was working normally – Austria, Finland, France, Germany, and the Netherlands – was 1.8%, right near the ECB’s target of just-below 2%. Thus, the countries that most needed lower borrowing rates needed much more than an ECB rate cut to boost business lending, whereas those where business lending was responsive to ECB rate cuts were not clearly in need of one – at least according to the ECB’s inflation criterion.

Inflation in the strong countries, however, has declined significantly since then – it now stands at a GDP-weighted 1.5%.

This means that a rate cut at the ECB’s November 7 governing council meeting should be a no-brainer. Sadly, our Geo-Graphic suggests it will also be a no-gainer; the ECB will have to take far more aggressive action to prod business lending in the worst-hit crisis states.

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”