Scaling China’s Hidden Intervention In the Foreign Exchange Market

Is China’s actual intervention even larger than I thought?

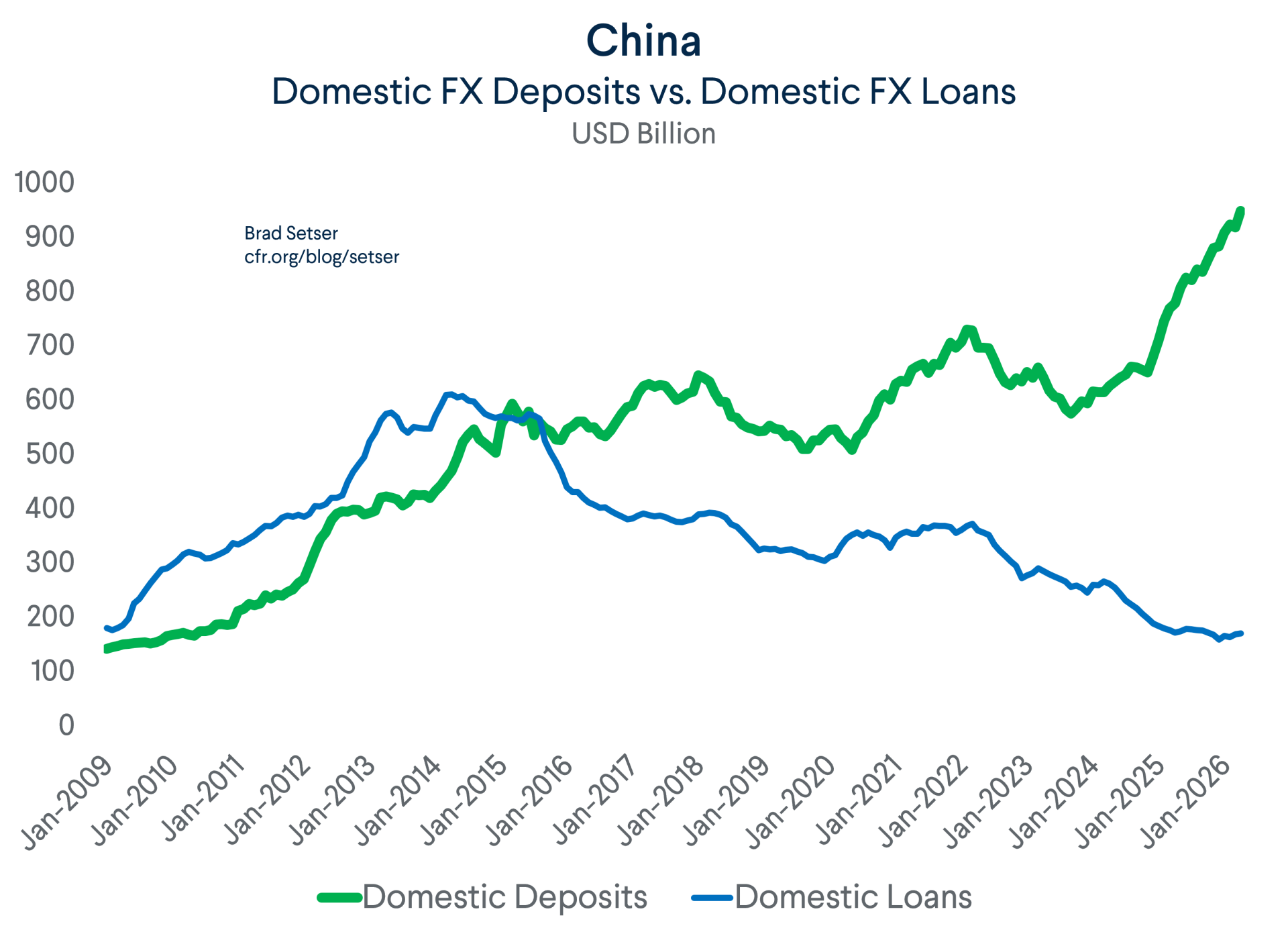

China’s central bank (the PBOC) has been arguing—in conversations with some think tanks—that the rise in the foreign assets of China’s state commercial banks just reflects investments financed by a rise in domestic foreign currency deposits. Since the state banks are just putting foreign currency raised domestically to use globally, the rise in the state banks foreign assets doesn’t reflect backdoor intervention to support the yuan.

Fair enough.

That is the best possible argument available to the PBOC at a time when the foreign assets of China’s state banks have surged.

Of course, there is also reason to be suspicious.

The state banks have in the past been used to disguise PBOC intervention, as the PBOC provided the state banks with some of the foreign exchange it bought to manage, and thus moved the foreign exchange out of reported reserves.*

This certainly happened in 2005 and 2006, when the PBOC used swaps to transfer dollars over to the state banks (the state banks invested the funds in foreign bonds, and registered as a portfolio debt outflow). It happened again in the 2007 and 2008, which the state commercial banks were required to hold a portion of their required reserves in foreign currency. This registered as other foreign assets on the PBOC’s balance sheet, and as an “other, other” outflow in the balance of payments.* By contrast, countries like Turkey and Argentina report the foreign exchange that domestic banks hold at the central bank as part of their required domestic reserves, and as part of the central banks’ foreign exchange reserves.

But these examples are from the past, and they didn’t coincide with a rise in the state commercial banks’ domestic foreign currency deposits.

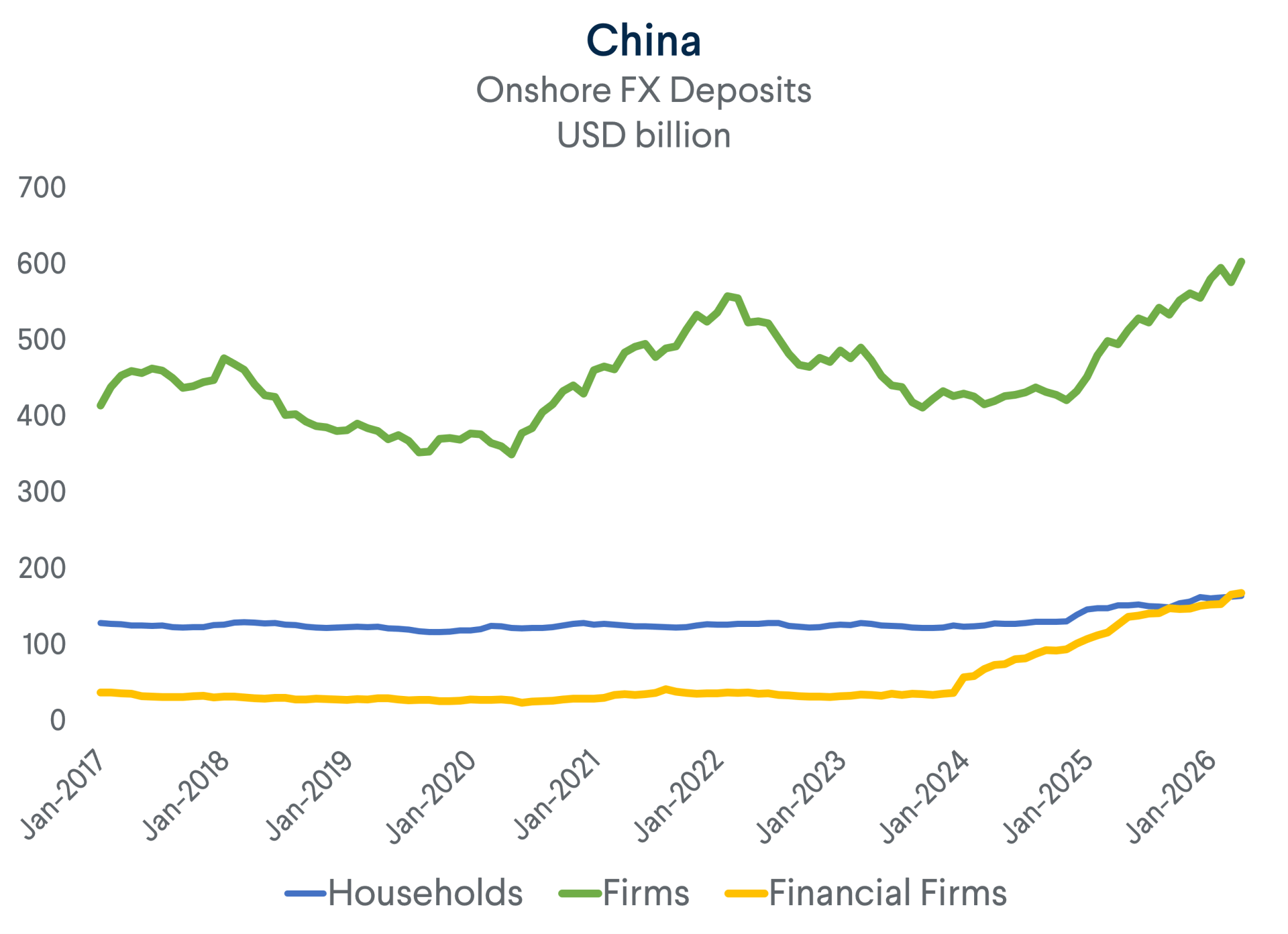

At the same time, the fact that reported foreign currency deposits are rising should not get the PBOC off the hook.

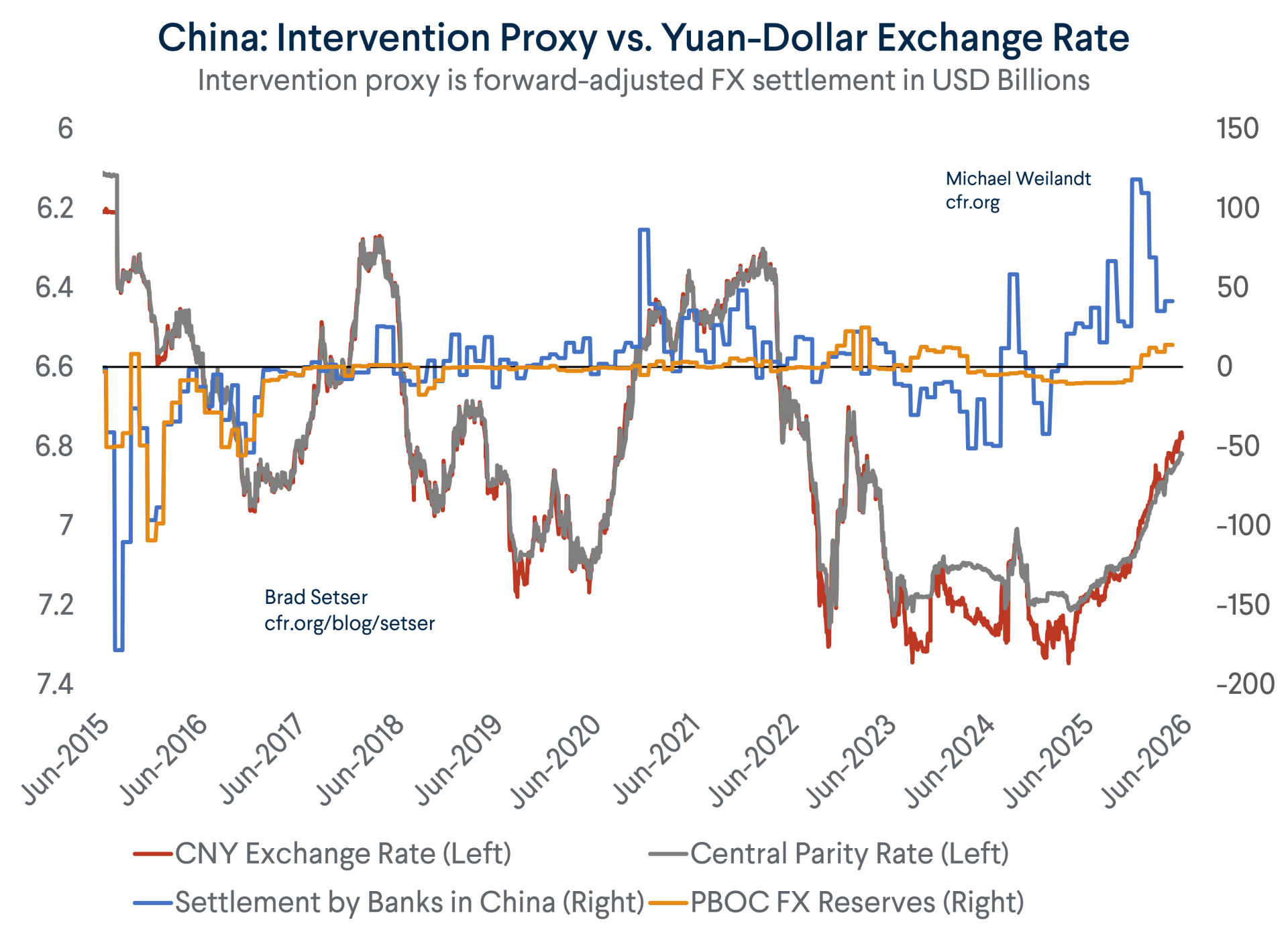

The RMB is obviously managed; its moves are driven by the PBOC’s daily fix, and it has far less volatility than a freely floating currency.

The deposit line item itself could reflect backdoor management (the FT back in 2023 called the banks’ domestic FX deposits hidden reserves).

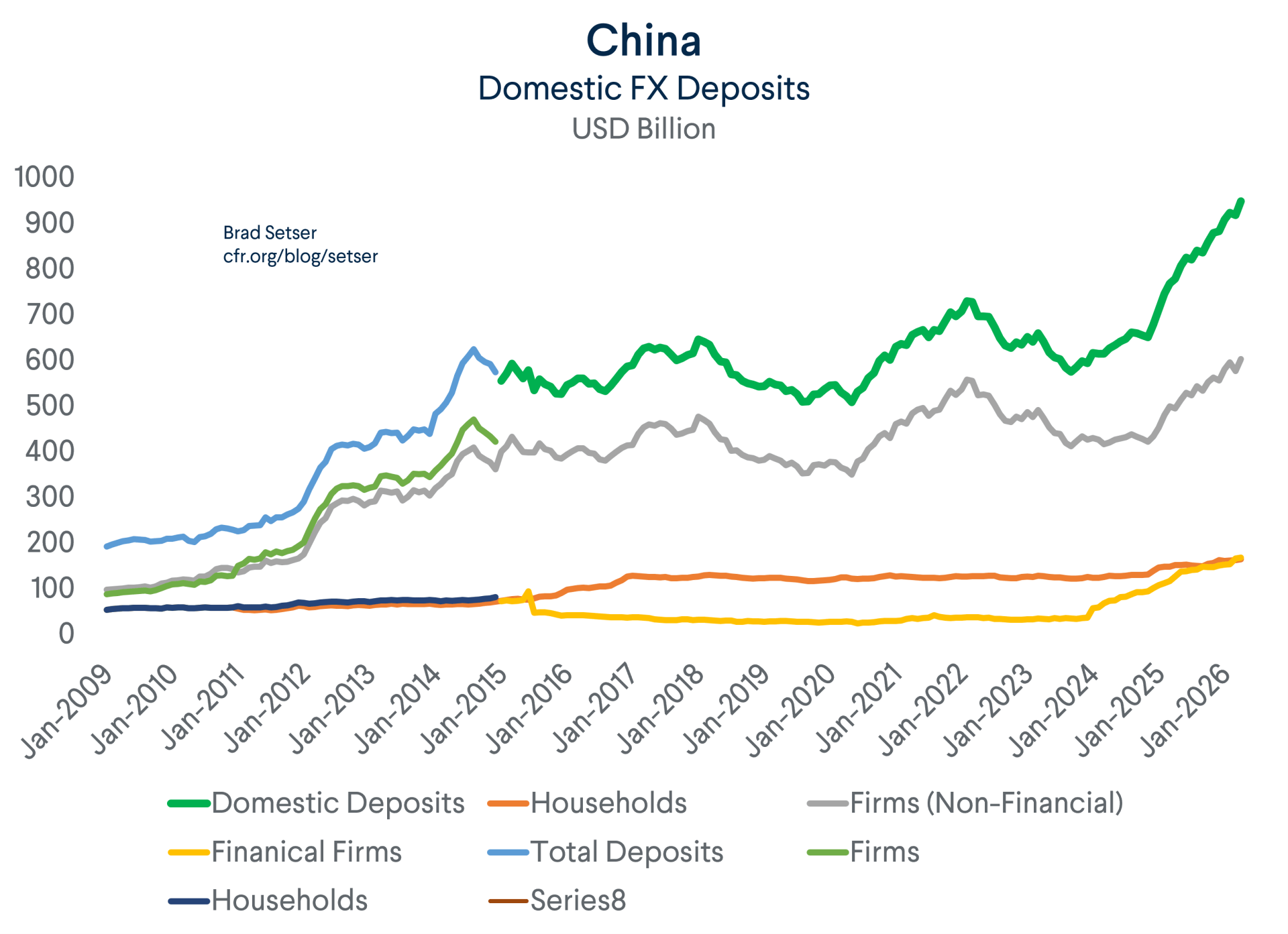

And the deposit series itself has long been a bit suspicious.

There was a surge in 2012 for example, which came out of nowhere and coincided with the absence of any PBOC reserve growth (during a U.S. election year where Governor Romney was making China’s currency an election issue). It turned out that the rise in deposits was driven by unusually high dollar interest rates, which pulled dollars into the state banking system. In 2013, after the U.S. election, the PBOC returned to more normal reserve accumulation.

And there was another surge in foreign currency deposits in 2020 and 2021.

That too is a bit suspicious.

The Fed ad cut U.S. interest rates in the pandemic, and thus the apparent incentive to hold dollars wasn’t there. Chinese policy rates were in fact above U.S. rates, so there wasn’t any obvious incentive for Chinese firms to place a lot of dollars in the state banking system.

Foreign currency deposits then fell when the Fed raised rates to contain the post-pandemic surge in inflation in 2022 and 2023. I repeat: deposits fell as the Fed raised rates, and China was, at the time, cutting yuan rates to prop up its domestic economy after the property bubble burst.

Basically, dollar deposits moved in the opposite direction of interest rate differentials (and CNY/USD) from 2020 to 2023. By contrast, they moved in the way one would expect central bank reserves would move if the central bank was managing its currency to dampen volatility.

The recent runup in foreign currency deposits is also a bit difficult to explain with economic variables.

U.S. rates remain higher than Chinese rates, true. But during the period of dollar deposit growth, the yuan has appreciated modestly against the dollar, so a yuan-based investor would have been better off just holding yuan and profiting from the yuan’s appreciation.

All that is to say: the FX deposit series behaves suspiciously like a backdoor intervention series (rising when the yuan is under pressure to appreciate, falling when there is depreciation pressure) rather than as a real indicator of onshore dollar demand.

Moreover, the recent rise in foreign currency deposits is coming from inside the financial sector, which only adds to my suspicions.

But suppose that the PBOC is right, and that the buildup of domestic dollar deposits isn’t funded out of backdoor intervention.

The PBOC still needs to explain what is happening with the dollars bought by the state banks (and/or the PBOC) in the FX settlement series.

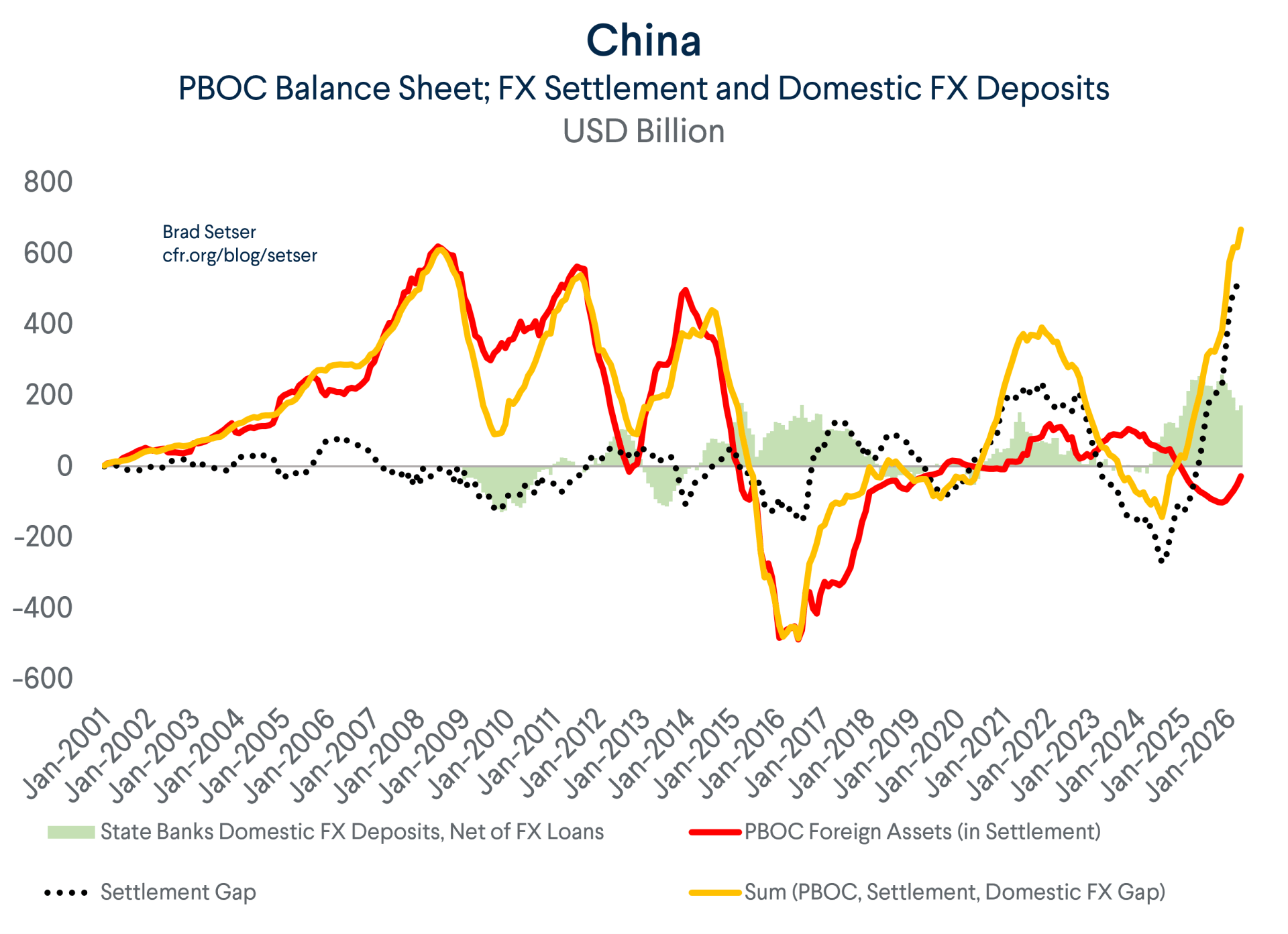

Remember that settlement is a series that shows net purchases of foreign exchange for yuan.

That is to say that an exporter bringing a dollar onshore and putting it on deposit in the state commercial banks would not register in the settlement data. And an exporter that sold dollars for yuan and put the yuan on deposit in the banks would appear in settlement.

As a result, the settlement data should be added to the flow generated by the state banks investing domestic dollar deposits abroad (at least so long as the foreign exchange from settlement isn’t itself the source of the dollar deposits).

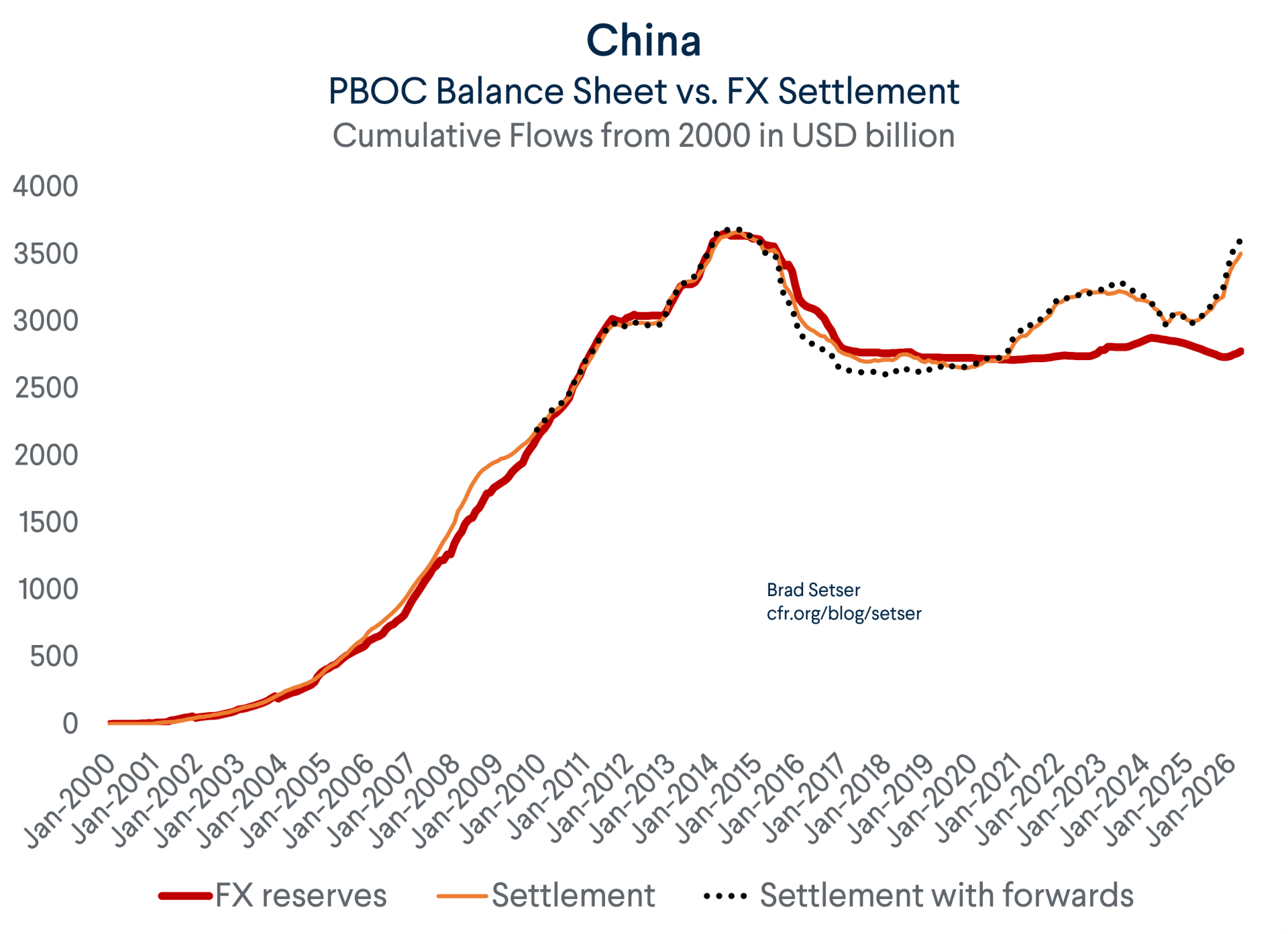

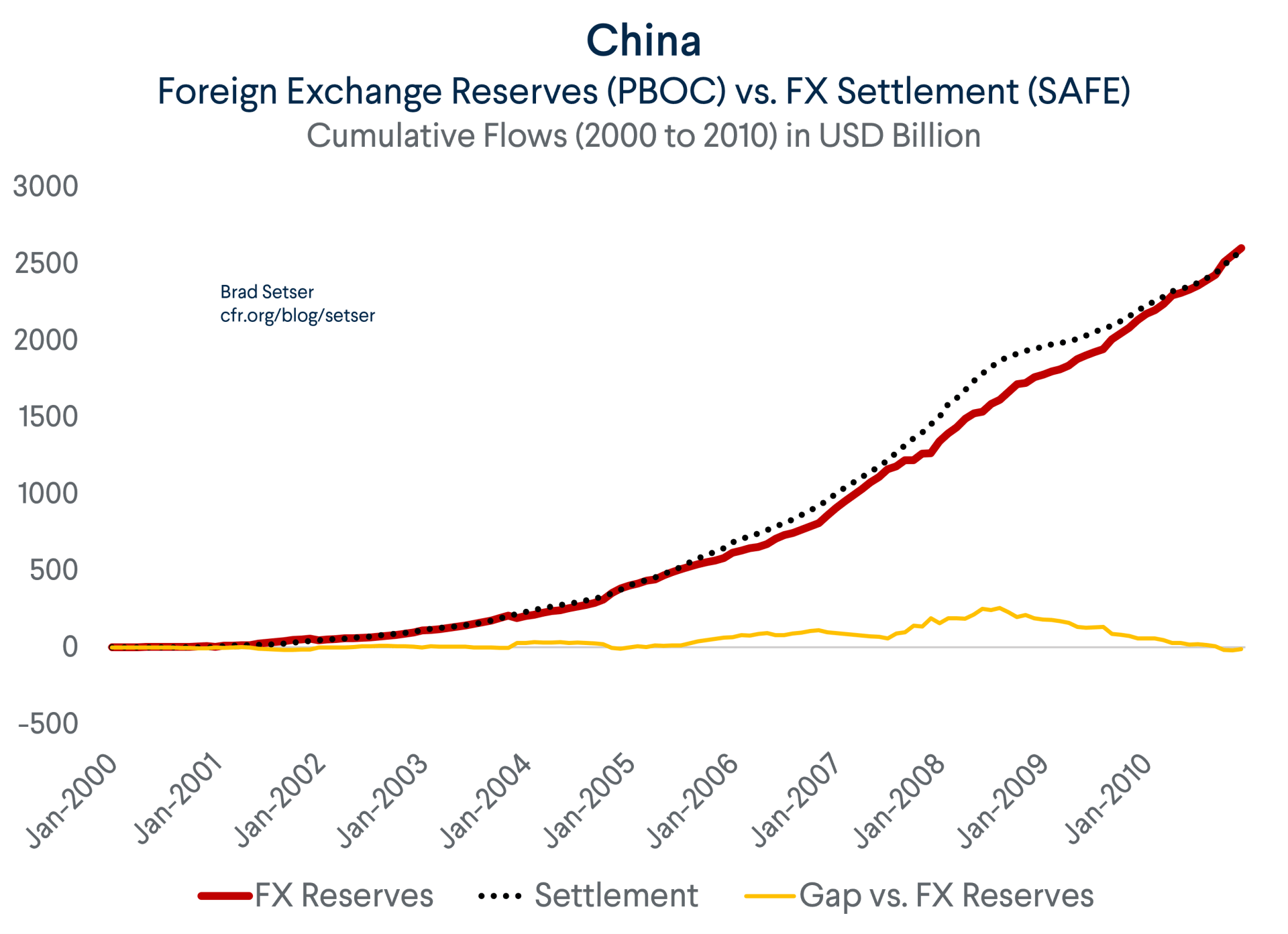

Historically, the foreign exchange bought in settlement more or less all ended up on the PBOC’s balance sheet. That makes sense, because settlement implies taking an open position (holding foreign currency assets abroad against domestic currency liabilities) and the risk of losses in the event of an appreciation. It is an intervention variable after all.

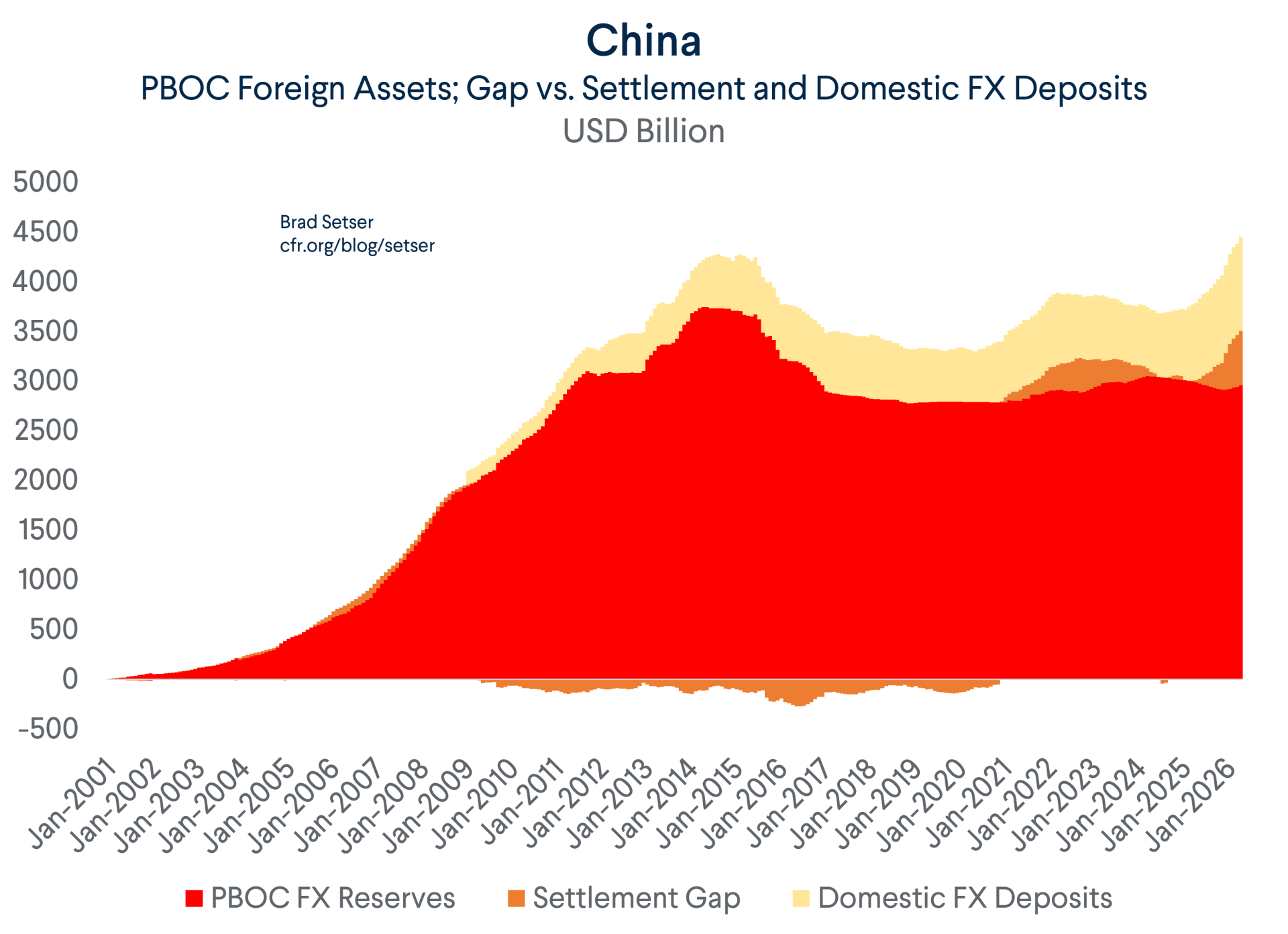

In the past, a gap between foreign exchange settlement and the foreign exchange reserves reported on the PBOC’s balance sheet generally meant that the PBOC had found a way to transfer some of the foreign exchange it bought to the state commercial banks. That was certainly the case from 2006 to the middle of 2008, as the PBOC swapped its dollars for yuan and effectively lent its dollars out to the state banks to manage (as discussed previously).

But in recent years, for reasons that China has never transparently explained and that the IMF hasn’t bothered to investigate, the settlement series has diverged from the PBOC’s balance sheet.

My suspicion was that the “settlement gap”—the gap between the foreign exchange bought in the settlement series and the foreign exchange that shows up on the PBOC’s balance sheet—was discretely being transferred to the state banks (or the state banks were buying the foreign exchange and discretely hedging the risk with the PBOC). That would help explain the rapid growth in the foreign assets and the foreign currency assets of the state banking system.**

But let’s assume that the PBOC isn’t transferring ANY foreign exchange to the state banks to manage and the growth in the state banks external foreign exchange assets is all organic. That means that the settlement gap isn’t contributing to the rise in the external foreign currency assets of the state banks. The extra foreign exchange bought in settlement thus has to be going somewhere else. That implies that the true scale of foreign currency now flowing through China’s state institutions is even bigger than I realized.

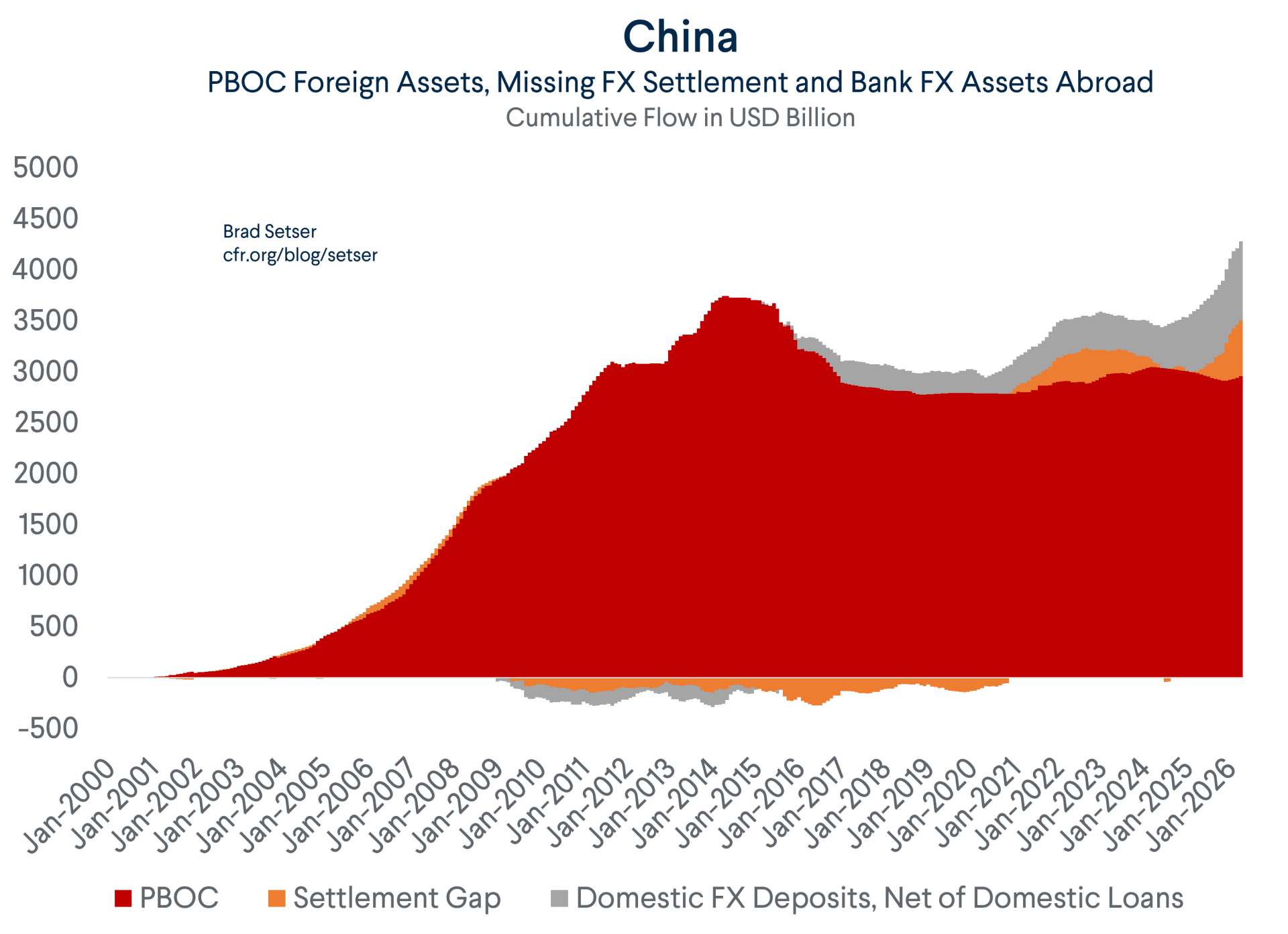

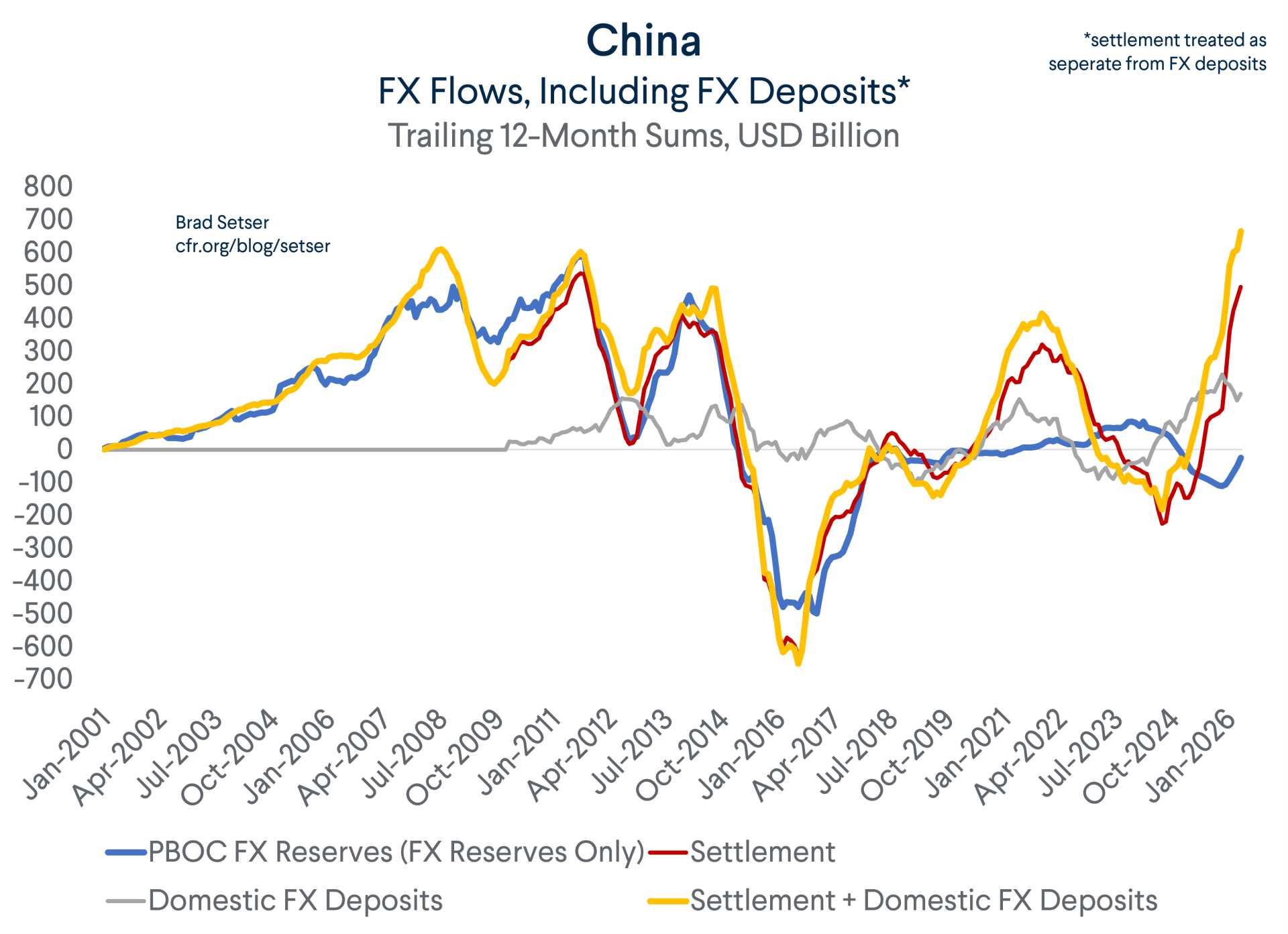

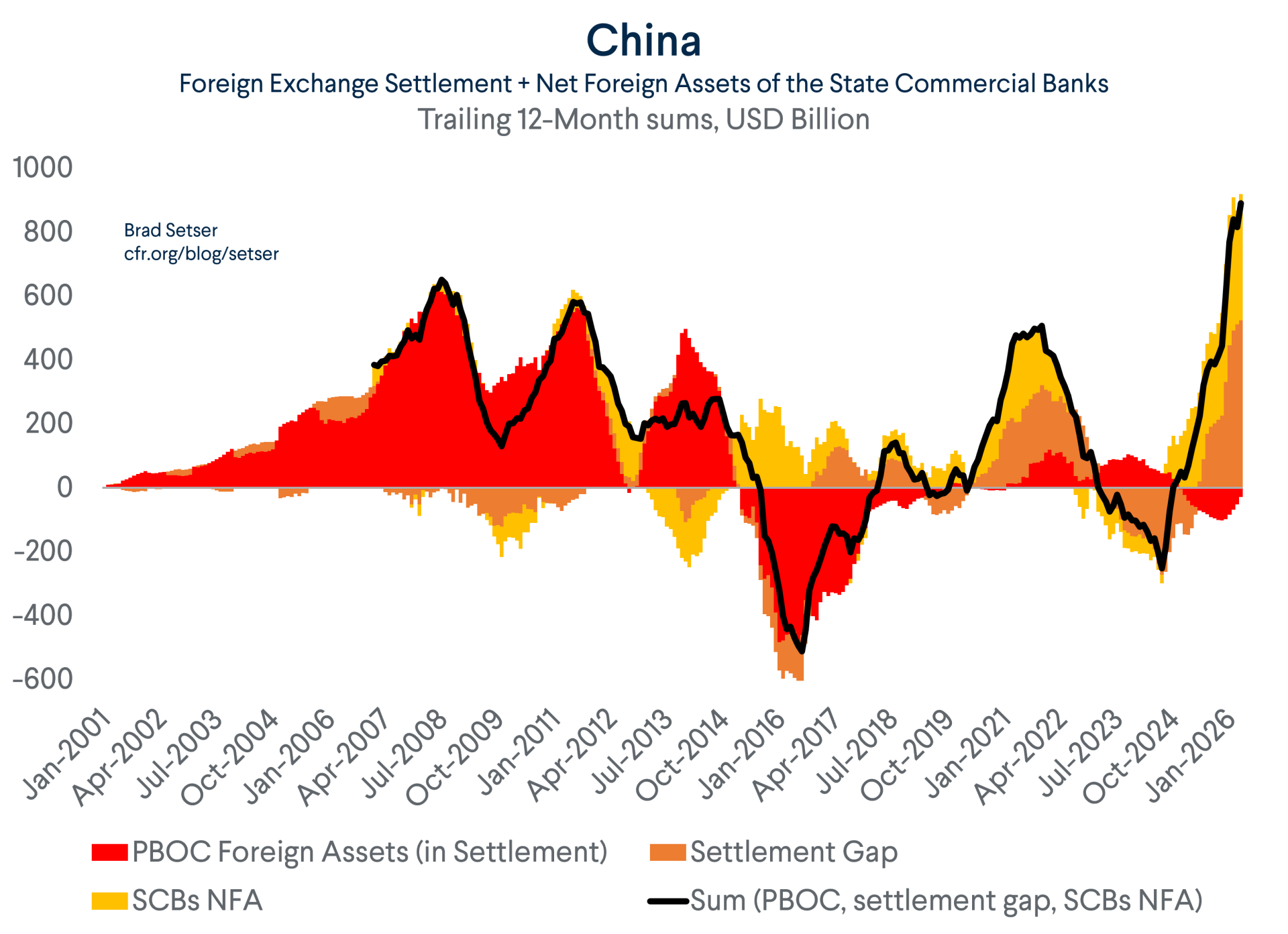

Basically, the best current measure of state foreign currency flows would be the sum of foreign currency deposits invested abroad (proxied by domestic FX deposits net of domestic FX loans) and the foreign currency actually bought by state in the settlement series (split into settlement that appears on the PBOC’s balance sheet and settlement that doesn’t appear at the PBOC– the settlement gap).

One implication is that the total amount of foreign currency intermediated by the Chinese state rose to around $700 billion to their foreign assets over the last 12 months. Note that I am netting domestic fx loans against deposits to get a measure of external foreign currency assets funded domestically.***

Another implication is that the banks and the PBOC added substantially more foreign currency assets to their balance sheet in 2020 and 2021 than would be the case if FX settlement was supporting the expansion of the foreign currency assets of the state commercial banks (see the graph above).

Since the deposit series doesn’t look like it maps to economic variables like rate differentials or path of the yuan against the dollar in any predictable way, deposit growth too could be viewed as a form of indirect intervention—one that helps take pressure off the more direct intervention in settlement.****

That would explain why the two series have been correlated—both are ways of absorbing appreciation pressure without (at least right now) putting foreign exchange directly on the PBOC’s balance sheet.

I am not entirely sure that this is the right interpretation.

In the past, settlement that did not find its way onto the balance sheet did find its way over to the balance sheet of the state banks, which implies that the series are not additive.

But it is a potentially plausible assumption, and one that is consistent with the PBOC’s claims about the state commercial banks.

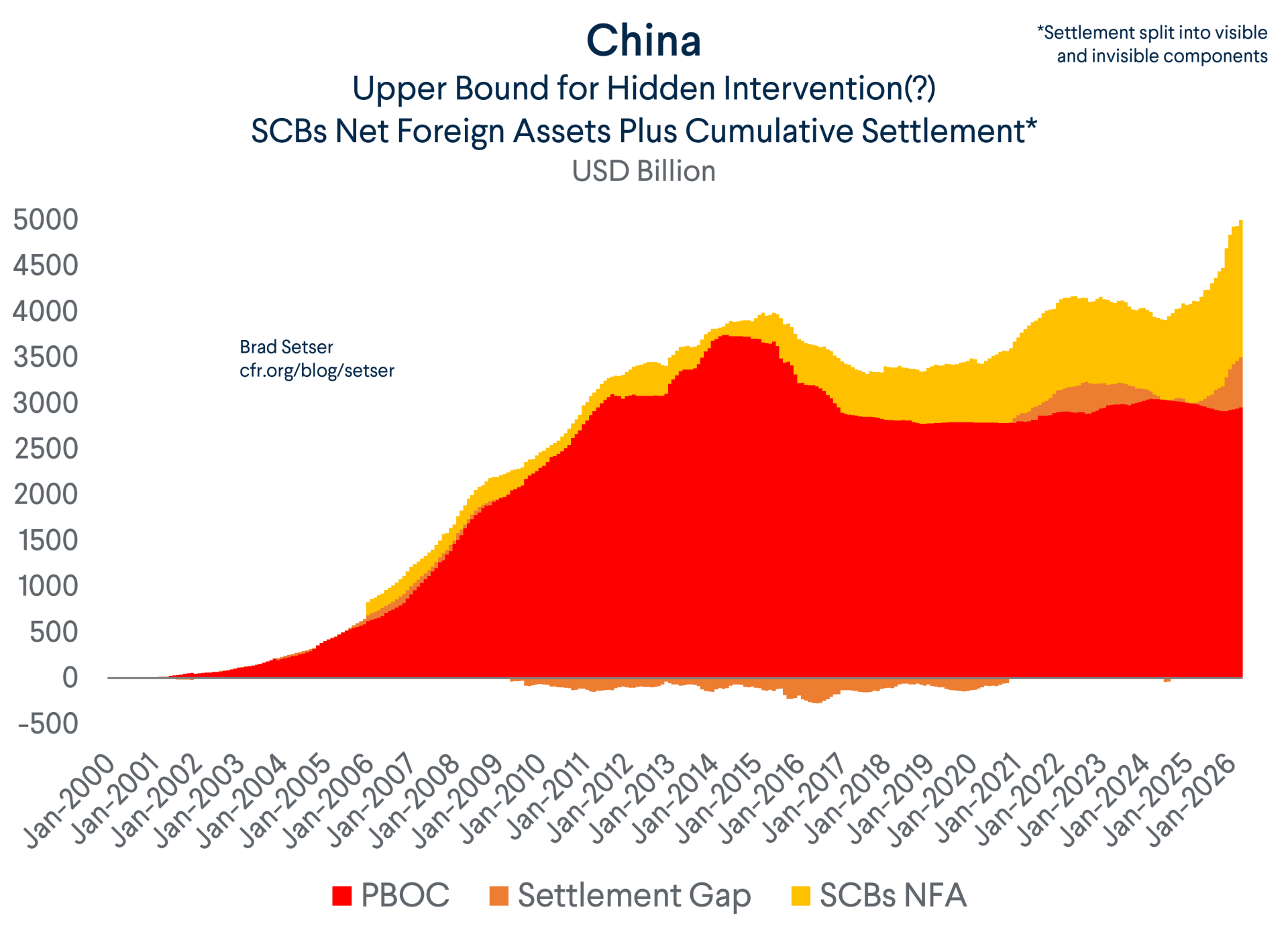

I could make an even stronger assumption and include settlement on top of the growth in the entire stock of external state commercial bank assets. That includes some external RMB loans (and purchases of RMB denominated securities) financed by domestic FX deposits – as the state banks now may be meeting foreign demand to borrow in cheap RMB out of their domestic balance sheet.*****

That implies even more flows have been funneled through the Chinese state in the last 12 months.

To be sure, such an assumption was wrong in the past. Settlement was equal to the total flow through the PBOC and the state commercial banks prior to the global crisis, as the PBOC moved fx and fx risk over to the state banks to limit visible reserve growth.

But things have changed, and adding settlement to the flows through the state banks doesn’t violate any balance of payments checks.

Bottom line: the PBOC has a lot of explaining to do. If settlement isn’t funding the growth in the state banks’ foreign assets, there is more overall foreign asset growth in the state financial system than I realized.

And yes, all this is rather advanced stuff. One implication of the PBOC’s argument that deposit growth is unrelated to settlement is that a lot of foreign exchange must be going to institutions that don’t register in the state commercial banks series; be it the policy banks, one of the state investment banks, or one of China’s many sovereign investment and co-investment funds.******

I don’t have full confidence in any of the adjustments right now.******* But all the indicators point to very large flows through the Chinese state financial system and underlying pressure for the yuan to appreciate.

*

** I covered this in detail in a previous blog.

***

**** Settlement mapped to FX reserves on the PBOC balance sheet before 2016, and the PBOC balance sheet metric seems to exclude interest income. So, the settlement gap is relative to the PBOC balance sheet, not relative to reserves in the balance of payments. Interest income retained by the PBOC would be another pool of additional assets available to fund investment abroad (for example, gold purchases) “inside” the system.

***** State bank outflows register in “other” (which is basically the banking system, IMF nomenclature here is confusing) in the balance of payments data.

****** The policy banks don’t appear in the PBOC banking data. Nor do the investment banks. Nor do the various sovereign funds. So, there are lots of options.

******* The SAFE data on external bank liabilities and assets by currency implies that the state banks on net actually use offshore RMB deposits to fund domestic lending, but the SAFE data here is at odds with the PBOC data (which shows much smaller external liabilities). As usual with China, nothing quite adds up.