The PBOC, The State Banks, and Backdoor Intervention

A post only a true balance of payments geek, a currency trader, or a U.S. Treasury hand can love; as Paul Krugman used to say, wonkish.

China reported that its banking system—technically the state banks and PBOC combined—bought $100 billion in month of December.

That is an insane number. Admittedly, the end of a calendar can make it a bit risky to annualize the monthly number. But it is a big number, and it is consistent with the reports from Bloomberg that the state banks were buying foreign currency to limit the yuan’s appreciation in December.

And if the number is adjusted for forwards, it rises to $120 billion.

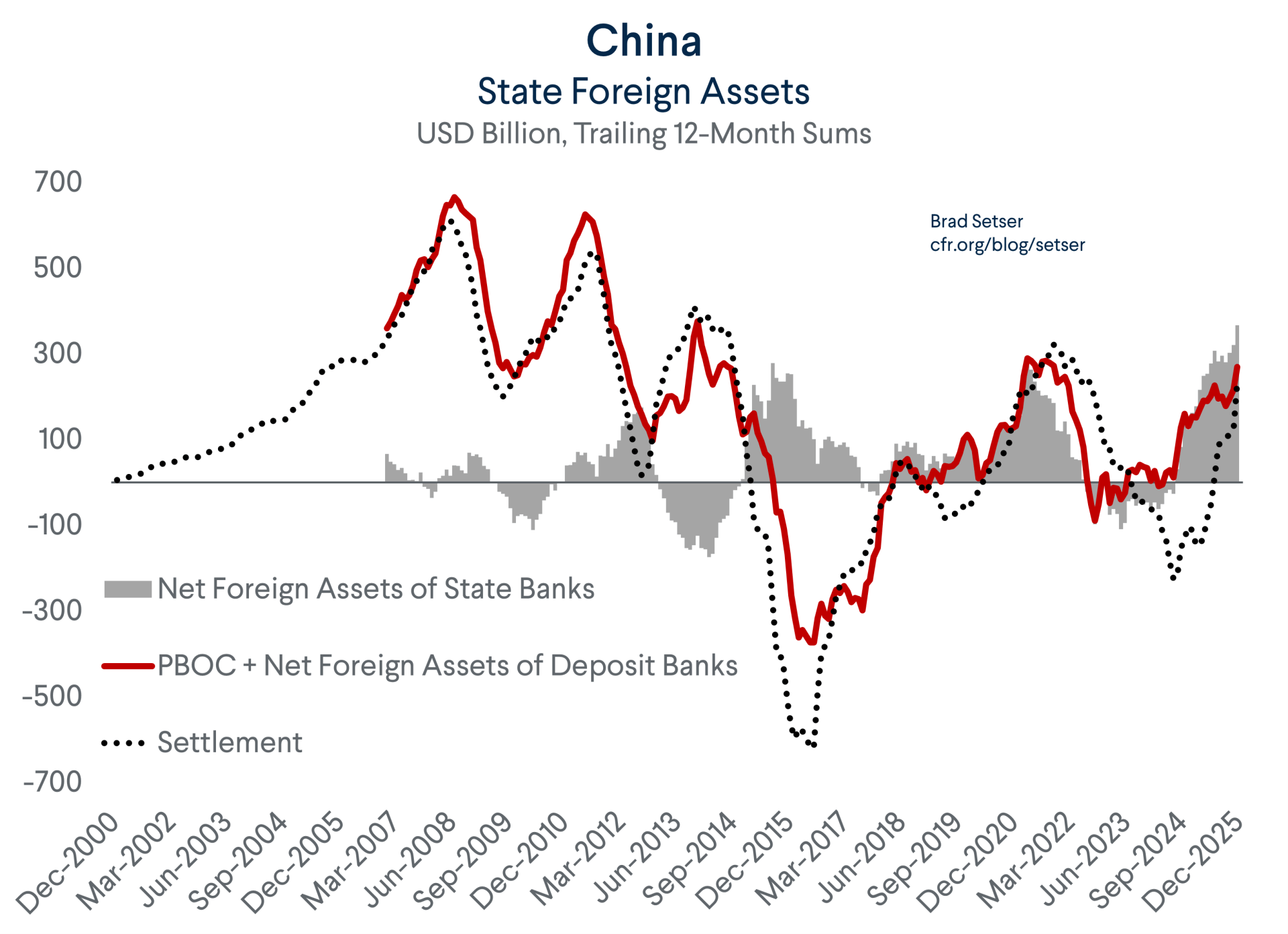

A separate data series showed that China’s state banks added $110 billion to their foreign assets, net of their foreign liabilities, in all currencies (more on that later).

This sure looks to be a surge in intervention even though the foreign currency balance sheet of China’s central bank (the PBOC) was unchanged.

Why am I so confident that settlement is a good proxy for China’s current intervention in the foreign exchange market?

Three reasons:

- The Duck Test

If it walks like duck and quacks like a duck, it’s probably a duck.

State bank dollar buying was all over the financial news in December. Reuters reported it on December 4:

“China’s major state-owned banks bought dollars in the onshore spot market this week and held on to them in an unusually strong effort to rein in yuan strength, according to people with knowledge of the matter. The dollar buying came as the yuan leapt to a 14-month high on Wednesday and extended a trend of state banks leaning against yuan gains in order to smooth its rise.”

Bloomberg too also reported on the dollar-buying on December 4: “Traders say state-owned banks have also been intermittently buying dollars to cool gains.”

And again on December 31 (and several dates in between): “An increase in dollar buying from major Chinese banks and proprietary trading desks caused the onshore yuan to erase its gains in the afternoon, according to traders who asked not to be identified discussing the foreign exchange market publicly.”

This builds on an important story from Bloomberg last October, which highlighted how the increased dollar position of the state banks was impacting the swaps market.

“The lenders have been ramping up their purchases of spot dollars over the past few months and offering large amounts of dollars for yuan in the currency swap market, according to traders who asked not to be identified as they’re not authorized to speak publicly. Although the two positions should ultimately balance each other out, the strategy is seen by traders as a negative for the yuan since it front-loads selling pressure.”

(As an aside, buying dollar spot and selling forward didn’t work—the selling pressure on the dollar built toward year-end, leading to more purchases).

As the news reports make clear, the dollar purchases from the state banks always came when the yuan was trading a bit strong, and thus are consistent with a policy of slowing the yuan’s appreciation.

And while the state banks could have been acting on behalf of the PBOC, the PBOC itself wasn’t seen directly in the market, and its foreign currency balance sheet has been surprisingly stable. That fits with a recent trend; the PBOC’s balances sheet has been quiet—too quiet, in fact; all the activity is with the state banks.

- The History Test

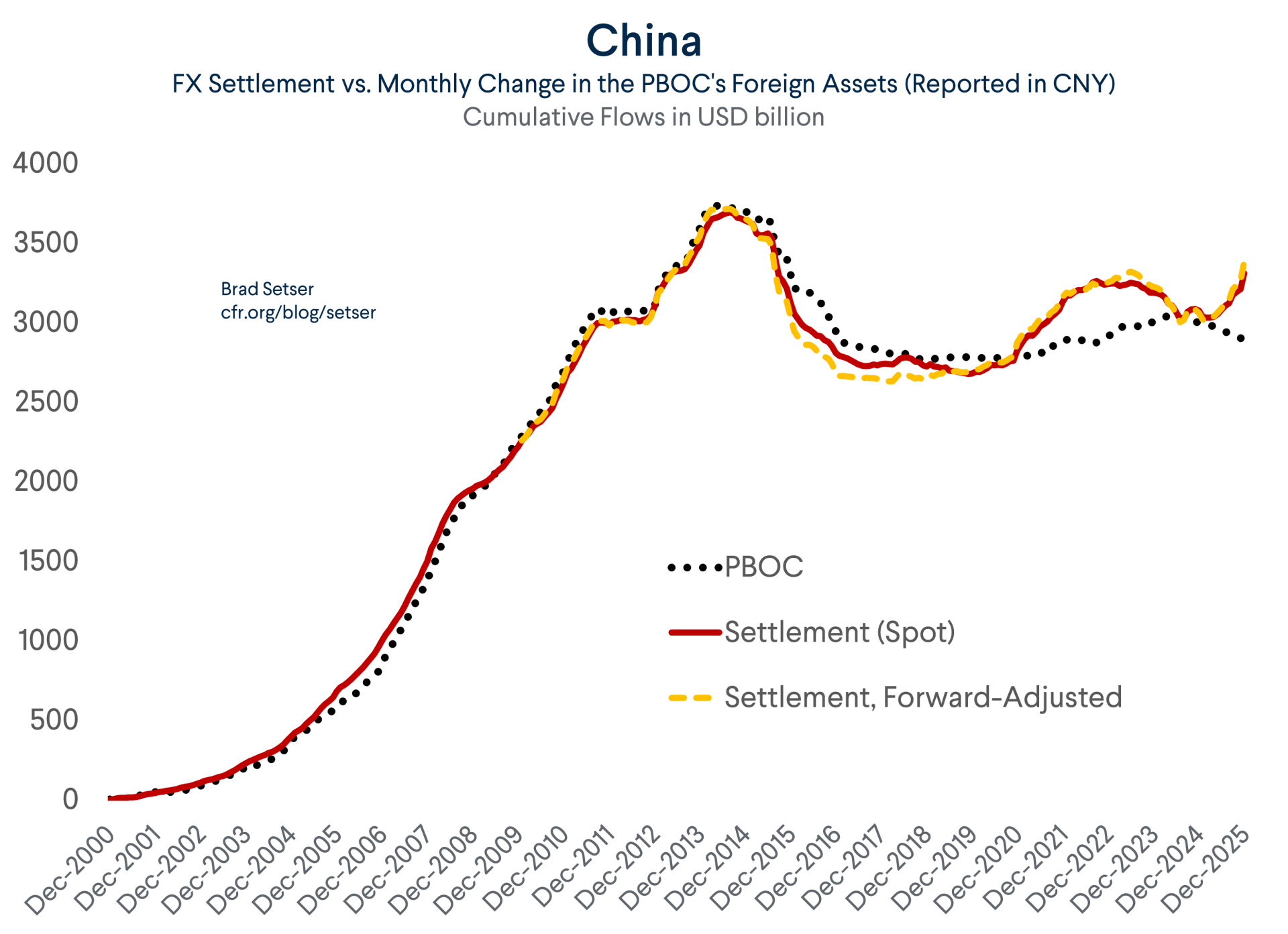

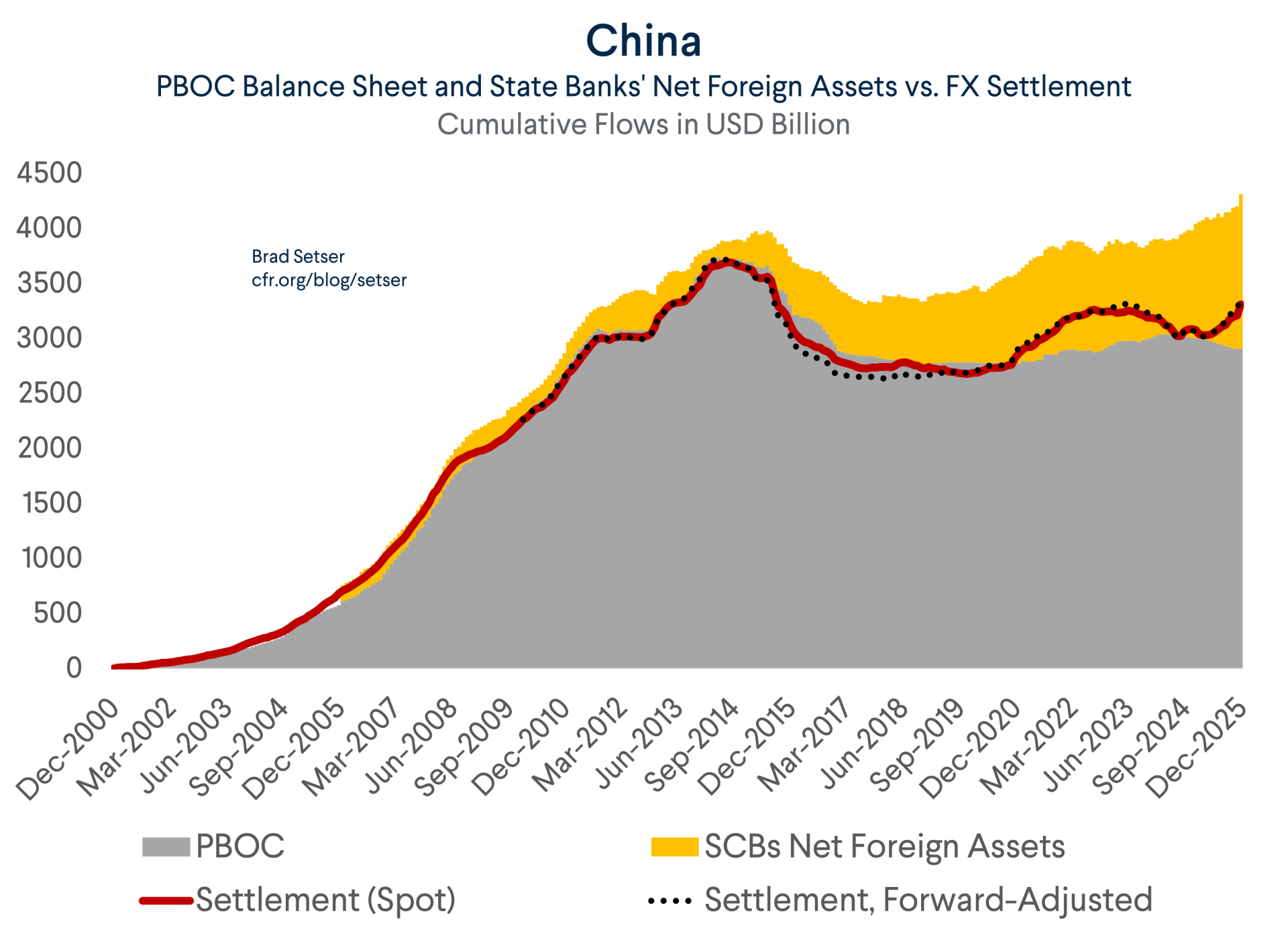

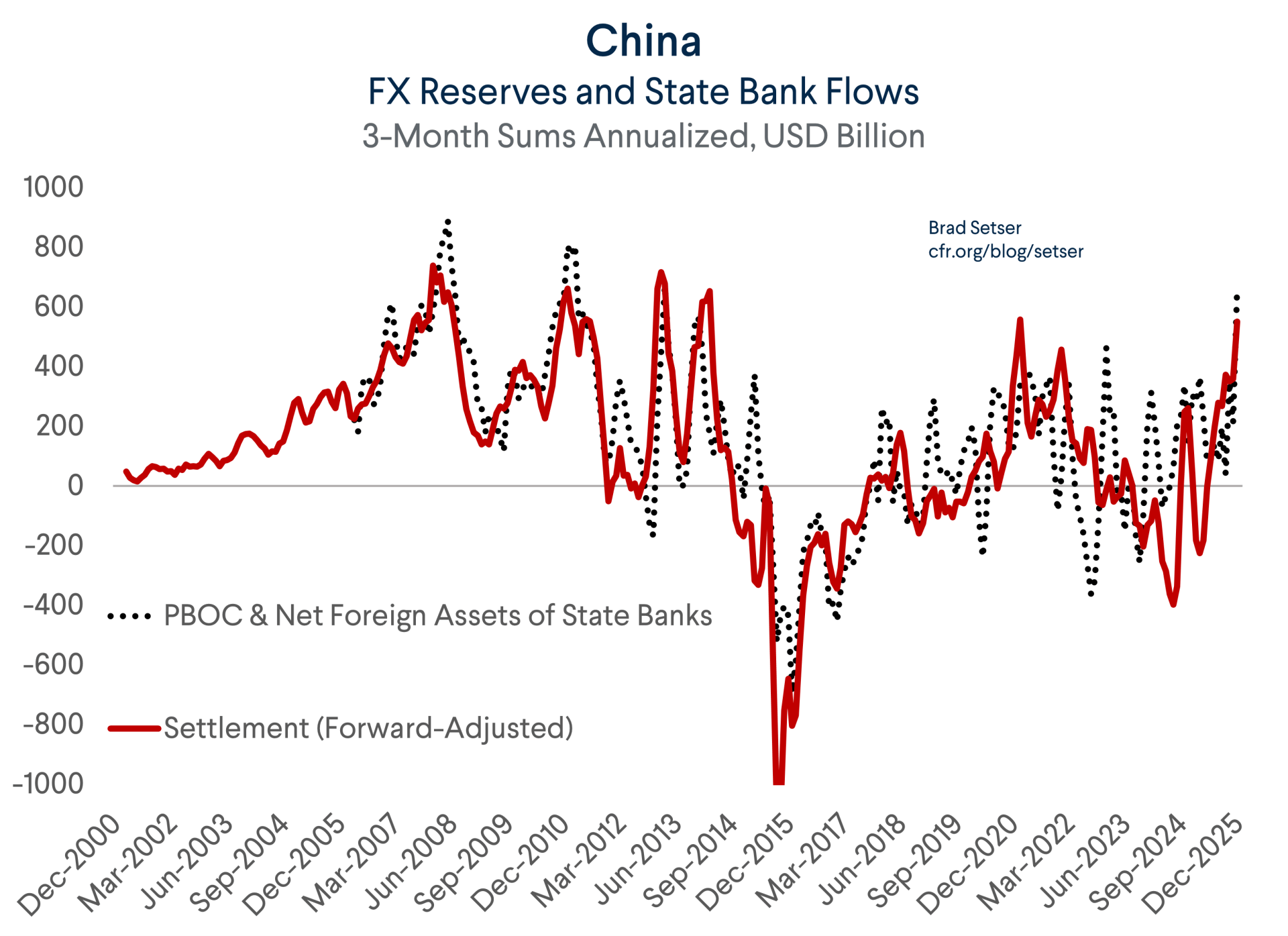

For about twenty years, the data reported in FX settlement was a near-perfect predictor of changes in the PBOC’s foreign currency balance sheet—a data series showing cumulative purchases in settlement and the sum of monthly changes on the PBOC’s balance sheet lines up nearly perfectly between 2000 and early 2020.

And when a close up shows a divergence between settlement and the PBOC’s balance sheet, settlement was generally the more accurate number.

It helps to be, umm, experienced. I am not as distinguished as, well-seasoned as say Mark Sobel, but I am also no longer young --

Go back to 2003. Settlement was bigger than the PBOC’s balance sheet over the year.

That was because the PBOC transferred $45 billion of foreign currency to the Bank of China and China Construction Bank in late 2003 as part of their recapitalization.

In 2005, settlement was again bigger than the rise in the PBOC’s balance sheet.

That turned out to be because the PBOC swapped over $100 billion with the state banks to allow the state banks to experiment with a foreign bond portfolio (it didn’t work out well, as it was largely reversed after 2008). We know this because the PBOC stopped publishing a data series in 2014—“funding of state commercial banks from the purchase and sale of foreign exchange”—and because there was a one-off surge in portfolio debt outflows from state banks (see my 2009 paper with Arpana Pandey).

And in 2007 and 2008, settlement was significantly above the PBOC’s foreign exchange reserves, not its foreign assets. That is because the PBOC requires that the banks hold some of their required reserves (against their CNY deposits) in foreign currency, and those required foreign currency reserves weren’t consolidated into the PBOC’s formal reserves. They show up in a line called “other foreign assets.”

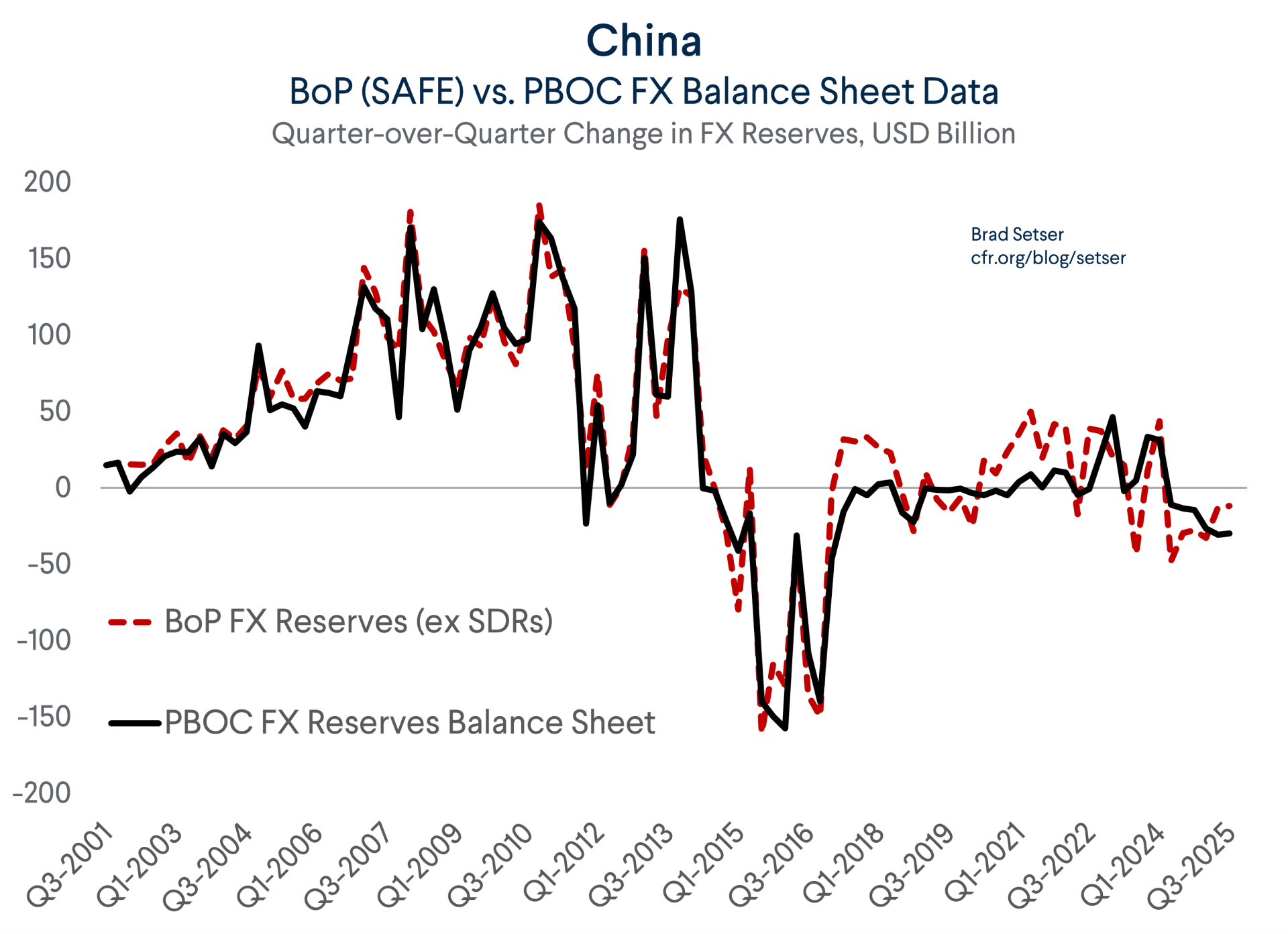

Settlement can also be used to construct a quarterly series that can be correlated with the quarterly increase in FX reserves that China reports as part of its balance of payments. Again, there is a near perfect fit over time. Or rather, there was a near-perfect fit over time until 2018 or so (that will turn out to be important).

Both settlement and the PBOC balance sheet dipped below the cumulative reserve increases reported in the balance of payments between 2016 and 2020.

Then in 2020 and throughout 2021, there was a surge in settlement that didn’t show up in either the PBOC’s balance sheet or the reserves line in the balance of payments.

And the same thing has happened this year.

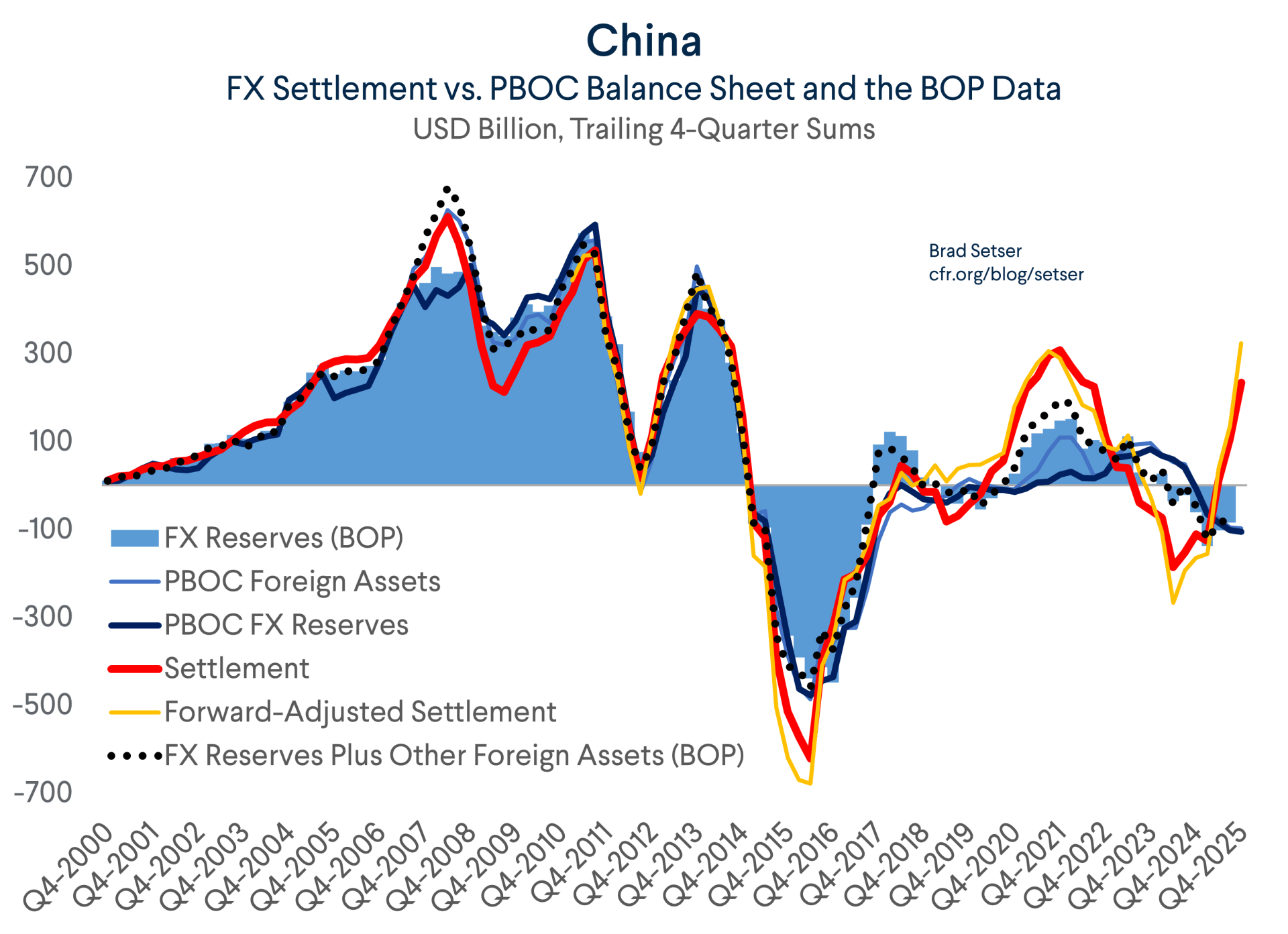

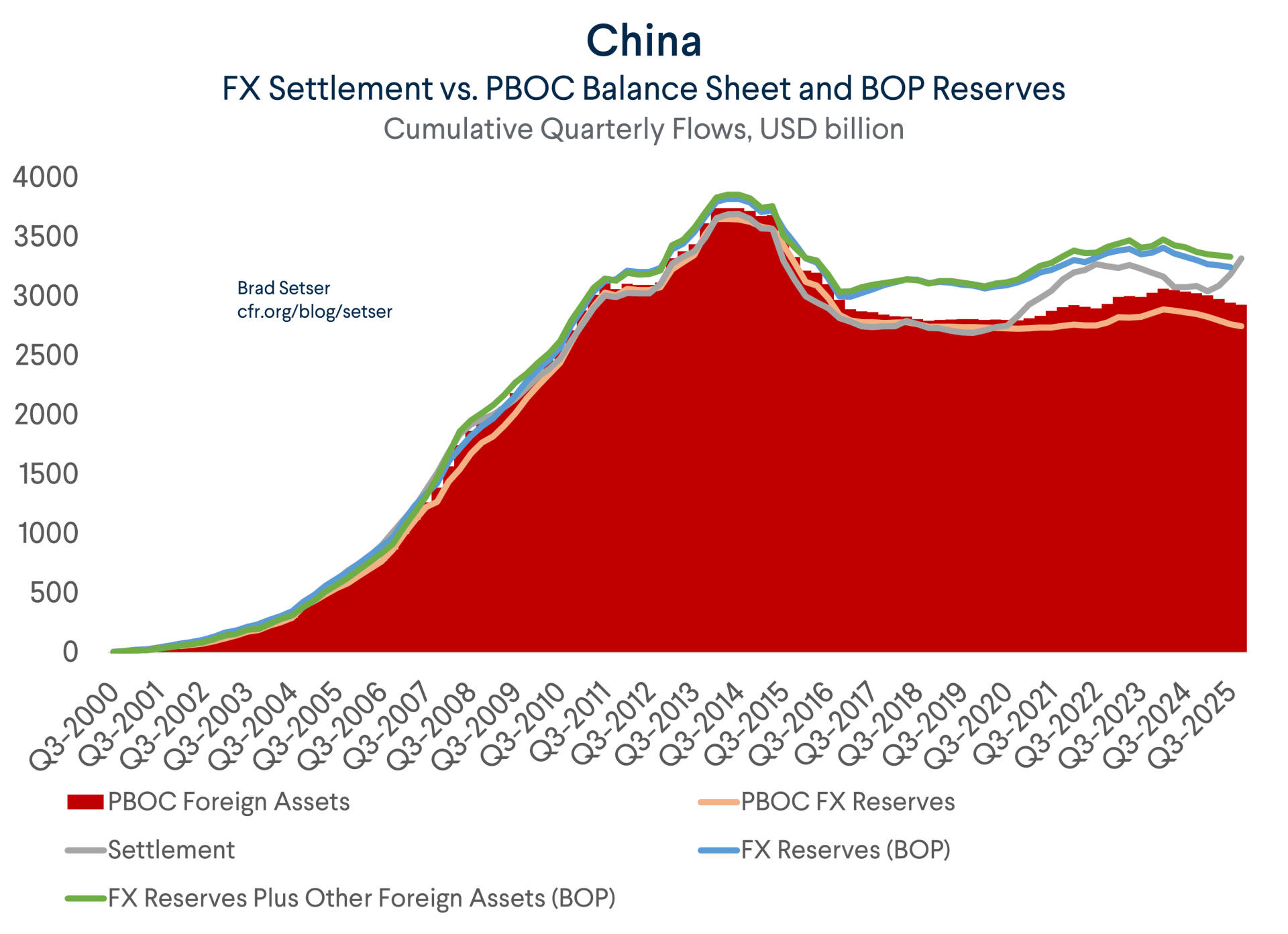

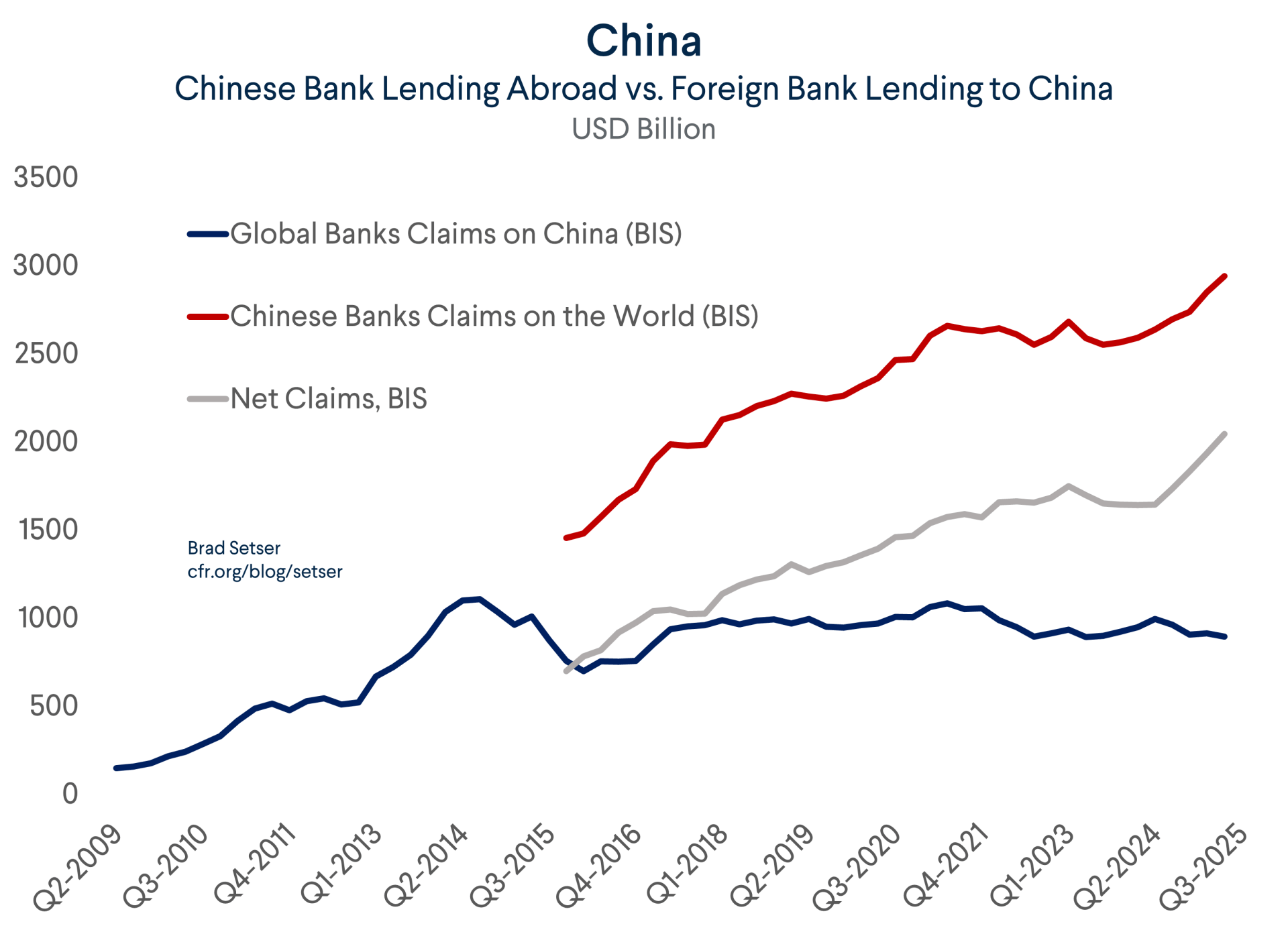

In theory, the difference between settlement and the PBOC’s balance sheet should be the foreign assets (ideally, the foreign assets in foreign currency) of the state commercial banks. Getting that number takes a bit of work though, as the foreign currency balance sheet of the state banks isn’t perfectly split between in China and out of China, the foreign asset data includes foreign assets in Chinese yuan. And any number will be incomplete as neither the state banks balance sheet data nor the foreign assets of the deposit taking banks data seems to include the two big policy banks. (Those policy banks which do appear in the broader balance of payments data as part of “other”, and figure prominently in the amazing work of Brad Parks and the AidData team).

The broad correlation between the sum of the PBOC’s balance sheet changes and the net foreign assets of state banks and fx settlement did hold for quite some time—until roughly 2021, in fact. But that correlation too has become a bit unstable.

Still, it is hard not to read the gap between the foreign assets reported on the PBOC’s balance sheet (measured as a sum of monthly changes) and cumulative fx settlement after 2018 as a measure of backdoor intervention.

That measure soared in 2020 and 2021, when U.S. rates were zero and China’s currency was under pressure to appreciate. It fell in 2022 and 2023, as the Fed raised rates in response to U.S. inflation and the PBOC cut its rates in the face of China’s property market bust.

It jumped again in 2025, particularly after China showed it could absorb Trump’s best tariff punch and Trump decided to back down.

To be clear, settlement is a better measure of backdoor intervention than the state banks’ balance sheet on its own. And the sum of the PBOC balance sheet and the net foreign assets of the state banks exceeds cumulative FX purchases in the settlement data, implying that the state banks have funding sources for their foreign balance sheet beyond the “excess foreign exchange” in the settlement data.

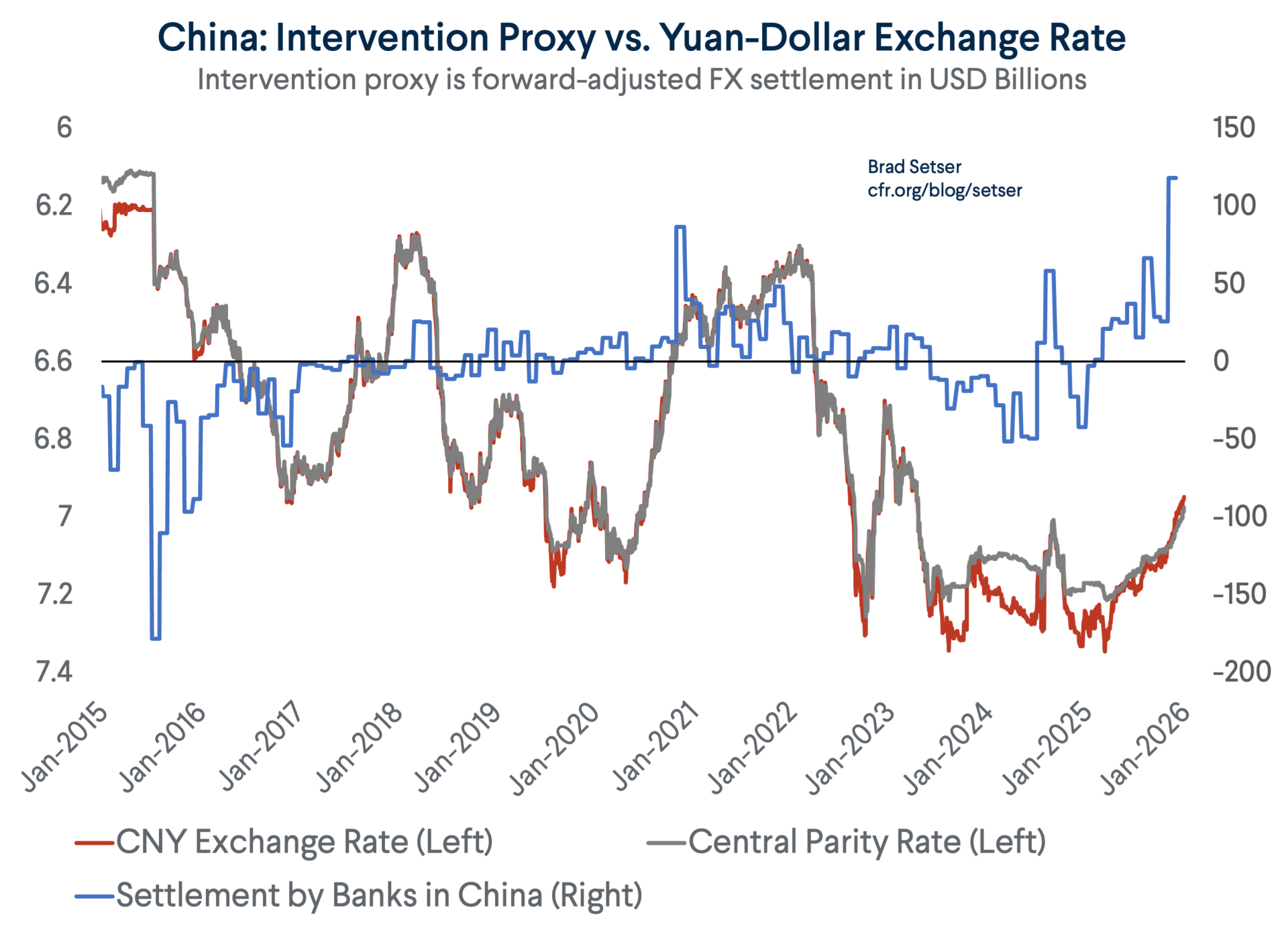

- The “Someone Has to Manage the Daily Trading Band” Test

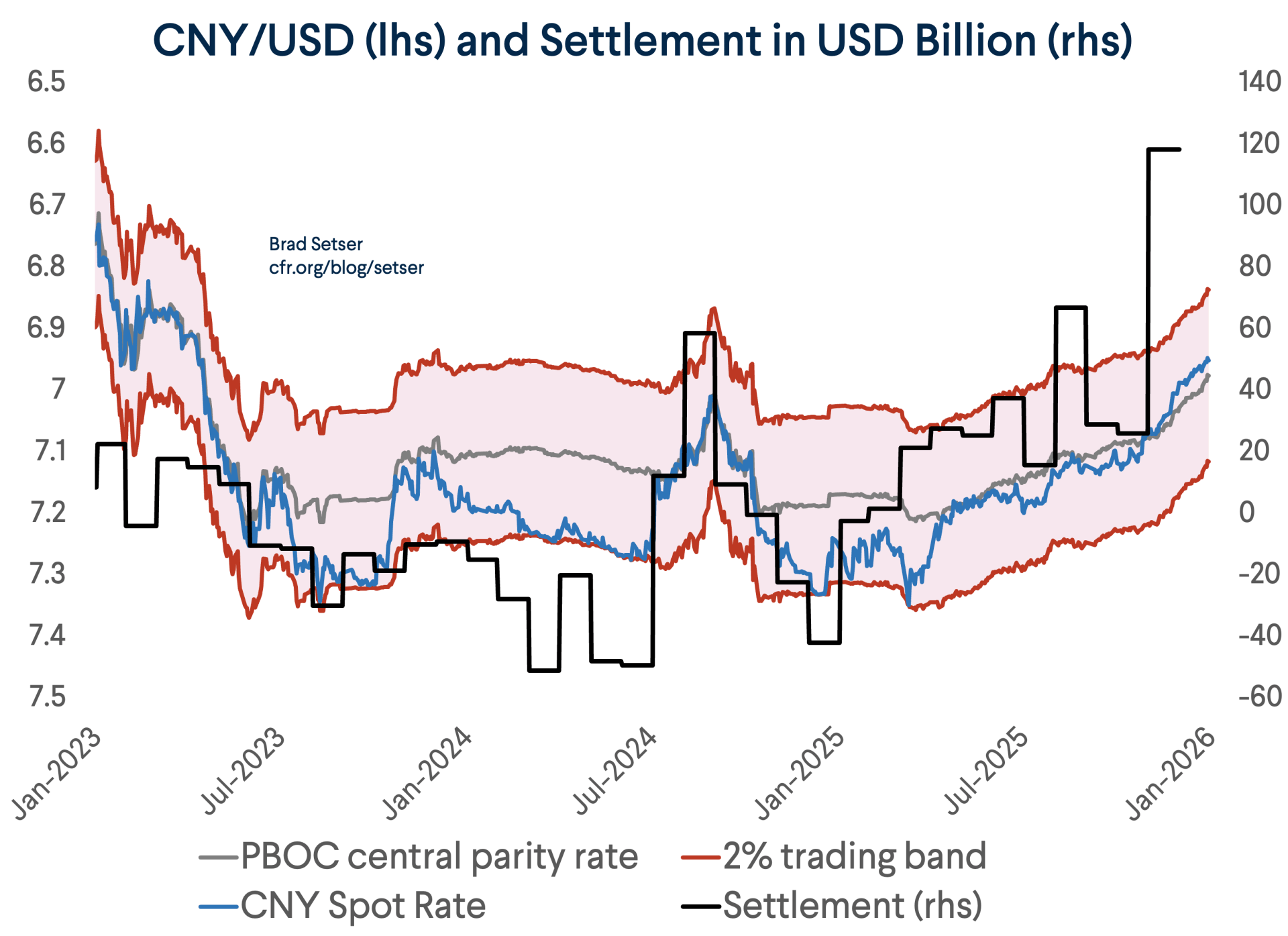

The yuan’s daily trading vs. the dollar is limited: it must stay within two percentage points of the central parity rate (the “fix”).

And the yuan has been much more stable against the dollar than against other currencies over the last five years (China maybe managed vs. the basket for a while, but it moved back to managing for stability against the dollar in a super visible way back in 2023).

That tends to require a bit of intervention.

The PBOC’s balance sheet has either been unchanged or moving in the wrong direction, so the needed intervention isn’t showing up there.

I think a trader at a state financial institution inadvertently revealed the trust back in 2023 to the FT:

“There’s no denying authorities have mobilized invisible foreign reserves from state commercial banks to manage the market,” said a trader at one of China’s largest state-run securities firms. “You can’t really touch the state reserves, which are closely watched.”

In recent months, there is a clear pattern to the FX settlement series, which smart analysts are starting to watch as closely as they used to watch reserves.

When the yuan is either weakening or on the weak side of its band (-2 percent vs. the fix), there are almost always sales in settlement.

And when the yuan is strengthening and either at the fix or stronger than the fix, there are almost aways purchases in settlement.

There is an important though subtle point here. The overall effect of PBOC purchases is to keep the yuan weaker than it otherwise would be. But the PBOC (and now the state banks) always tended to buy more when the yuan was slowly appreciating than when the yuan was super stable.

The PBOC has historically resisted big moves in either direction. And the PBOC did push back against depreciation pressures in 2023 and 2024. And now it is resisting a quick move back up.

And for a country with a large trade surplus, resisting appreciation pressure can require buying a lot of foreign exchange. When the yuan is going down, China’s exporters are willing to hold the dollars from the trade surplus offshore (an estimated $1 trillion now); and when the yuan is going up (it went up 1 percent in both December and January) the exporters all want to convert their dollars from the trade surplus back into yuan.

In this light, there is nothing surprising—given the enormous scale of China’s trade surplus—in the big purchases in the December data. In fact, there have been times in the past—admittedly now the distant past—when purchases exceeded the trade surplus.**

So, there is every reason to think that the surge in settlement is in fact a signal of pressure on China’s current system of exchange rate management—one that shows that Chinese state actors currently have to but a lot of foreign exchange to avoid a much faster pace of appreciation.

Remaining Data Gaps

Any analysis of China is limited by the gaps in China’s data.

I am confident that settlement should be viewed as a measure of direct intervention. But SAFE hasn’t given up all its secrets.

There are several important mysteries (or pure data inconsistencies) that remain.

Let me highlight three:

- The lack of interest income on the PBOC’s balance sheet, and the gap between the PBOC’s balance sheet reserves and balance of payments reserves (I am leaving gold out of this post, the FT covered the issues there better than I could).

Sometimes the most useful information comes from differences in the reports coming out of different parts of China’s state.

In 2022, the Ministry of Finance reported a large payment from the PBOC from accumulated earnings on foreign currency reserves—a payment of close to $160 billion that held the reported budget deficit down (China’s Finance Ministry is very European, it really tries to meet the Maastricht 3 percent criteria):

“China’s central bank [said] it will transfer more than 1 trillion yuan ($158 billion) in profits to the government to help finance fiscal spending. It’s the first time the People’s Bank of China has disclosed this kind of transfer, although it’s required by law to hand over profits to the government every year. The PBOC said in a statement Tuesday the funds will come from income accumulated over the past few years on the nation’s foreign exchange reserve” (emphasis added).

Fair enough.

But there was no corresponding change in the PBOC’s balance sheet reserves. Nothing. Nada. Zilch.

And indeed, the stability of the PBOC’s balance sheet from 2018 to 2023 (no change at all) suggests that the PBOC’s FX reserves number isn’t counting interest income (which apparently wasn’t consistently repatriated and converted into yuan).

The accumulated earnings (now around $100 billion a year if SAFE gets a 3 percent nominal return) need to show up somewhere, or at least one would think.

There are hints that the PBOC keeps in in a separate account. That would be one explanation for the modest but persistent gap between balance of payments reserves and the PBOC’s balance sheet since 2016 (but not before). But China hasn’t provided any real data here and the IMF hasn’t demanded answers.

- The PBOC’s domestic foreign currency assets (entrusted loans, some now converted into equity held by Buttonwood holdings, the Silk Road Fund and other “co-investment funds”)

We know the PBOC has foreign currency claims on domestic financial institutions that are NOT counted in its reserves.

We know this because the PBOC has said that it provides foreign currency financing to domestic financial institutions—so-called entrusted loans.*** And the PBOC has indicated to the IMF (and others) that it of course follows the IMF’s guidance on reserve reporting, and foreign currency claims on domestic financial institutions are of course not counted in its formal reserves.

Caixin first reported about these loans way back in 2010, just as China’s policy banks ramped up their offshore lending.

And the FT (and Reuters) reported that close to $100 billion in entrusted loans were converted into equity as part of the recapitalization of the Export-Import Bank of China and China Development Bank to ensure that they could fund the Belt and Road Initiative (see my blog on how to hide your foreign exchange reserves).

SAFE’s remarkable 2020 annual report provided a ten year progress report on SAFE’s successful effort to diversify the use of China’s foreign currency reserves—and it is very clear from that report that “diversified use” means something entirely different from changing the currency composition of China’s formal reserves.

It confirmed that entrusted loans have been provided to small, medium and large Chinese financial institutions—and that SAFE has contributed to the implementation of Xi Jinping thought through the contribution of foreign currency to institutions like the Silk Road Fund and other co-investment funds.

That’s enough smoke for me to be very confident that the PBOC’s reported foreign exchange reserves aren’t a complete and full accounting of the PBOC’s full foreign currency assets, including its domestic assets—.

Now I don’t have the full accounting here. But there should be little doubt, given that the total foreign asset position of the state commercial banks, the state investment banks and the policy banks is approaching $3 trillion that these big balance sheets provide a lot of scope for the PBOC to hide a lot of assets**

- There is Something a Bit Funky Going on the Deposit Side of the Balance Sheet of China’s State Banks

As noted earlier, change in the net foreign assets of the state banks now isn’t just correlated with the gap between settlement and the change in the PBOC’s balance sheet.

And cumulative settlement is now well below the sum of the changes in the PBOC’s balance sheet and the increase in the state banks’ foreign assets. So, there is something else going on. Part of the difference would logically be the increases in the offshore yuan lending of the state banks.

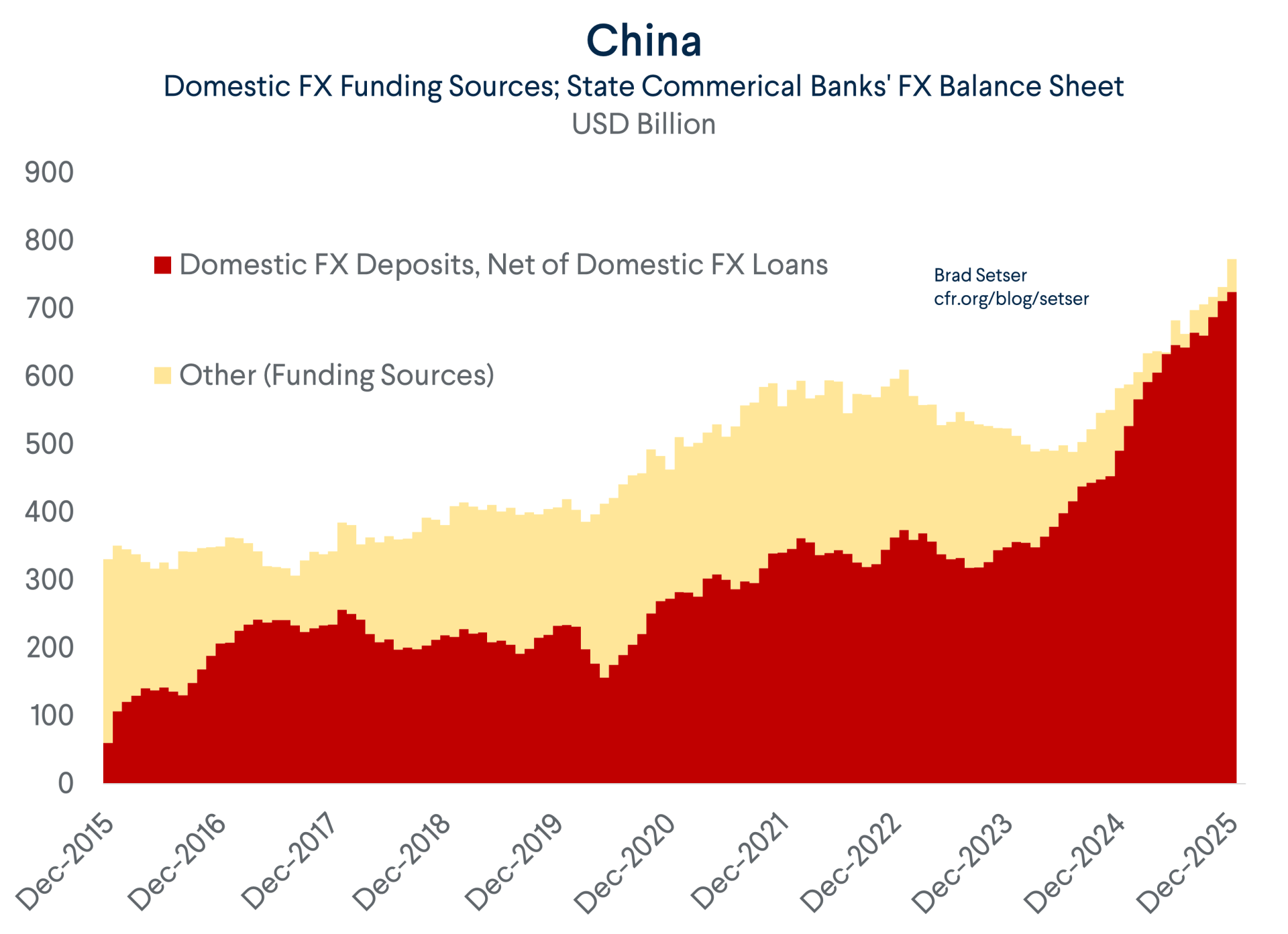

But from a range of data sources, we know that the domestic foreign currency deposits of the Chinese state banks have been growing and that those domestic FX deposits have NOY been offset by domestic FX loans. Rather the offset instead has come from increased holdings of external bonds and rising external FX lending.

That generates a balance of payments outflow. But it technically need not be intervention.

If say PetroChina (or its parent) wants to increase its domestic foreign currency holdings, it could buy foreign currency with yuan, and put the foreign currency on deposit in the Bank of China or ICBC, and the Bank of China or ICBC could then increase its foreign, foreign currency balance sheet. The purchases by PetroChina would be no different than its purchase of foreign currency to pay for the oil it imports; it should offset exporter inflows.

It other words, it shouldn’t register as part of the settlement data.

But there long has been something strange about the onshore foreign currency deposit series.

It simply doesn’t line up as expected with standard economic variables.

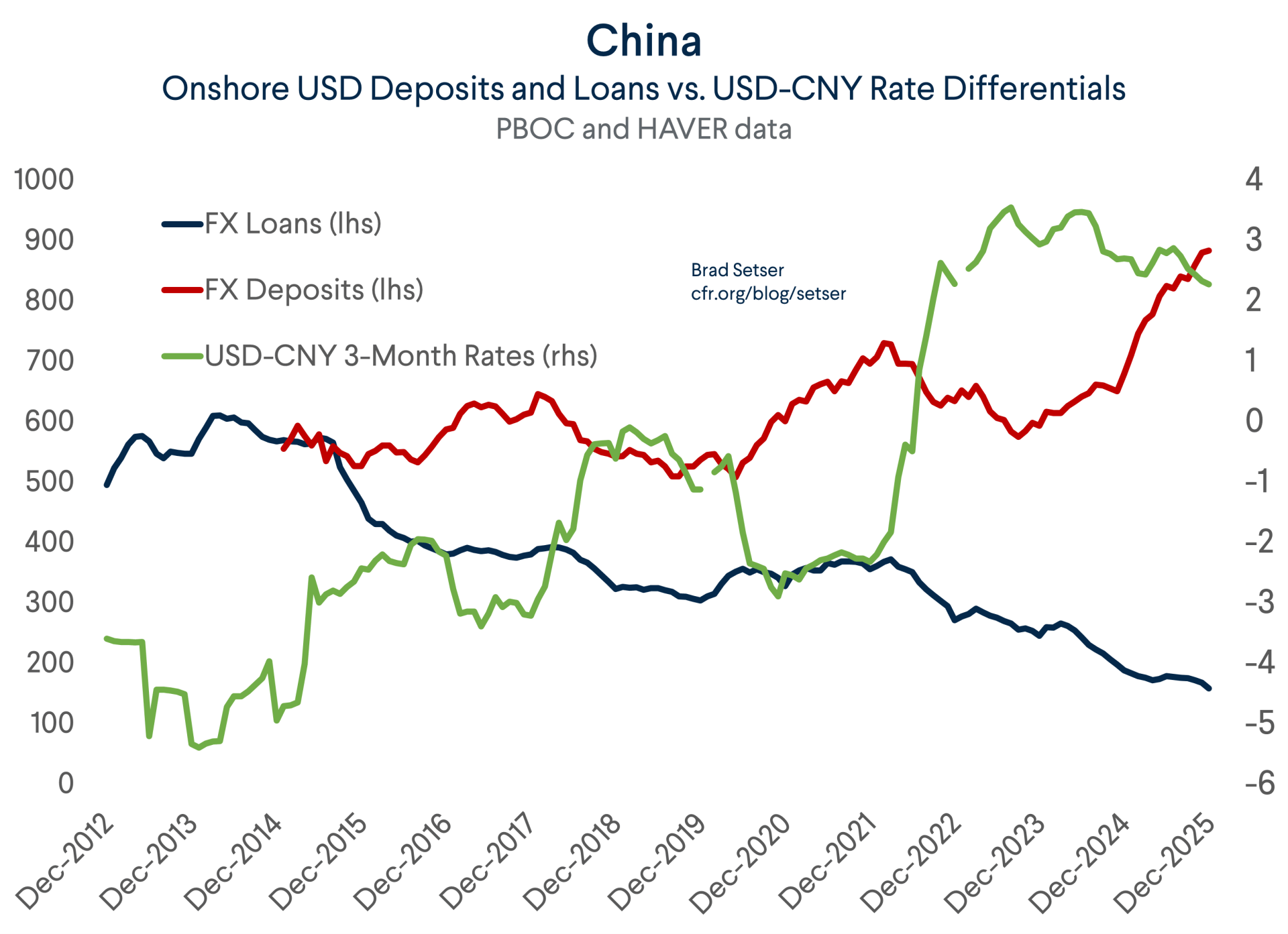

Consider a plot of domestic foreign currency loans and deposits against the difference between U.S. dollar rates and Chinese yuan rates (over three months)—a higher U.S. dollar rate showing up as a more positive number.

Higher U.S. dollar rates than yuan rates led to a decrease in onshore borrowing in dollars—which makes sense, why borrow in dollars rather than in yuan if it is cheaper to borrow in yuan?

But low U.S. dollar rates back in 2020 and 2021 were associated with a rise in domestic FX deposits (why? It should work the other way) and high U.S. dollar rates in 2022 and 2023 were associated with a fall in domestic FX deposits (again, why, folks should be moving into the dollar not away from it).

As the FT reported back in 2023 onshore foreign currency deposits seem to function as “a form of invisible reserves to relieve pressure on the renminbi.”

The state banks’ onshore dollar rates have not necessarily track offshore rates. A common tactic—which actually was first used back in 2011-2012—is setting onshore dollar rates at levels that differ from global dollar rates to help manage the yuan. The FT again, from 2023:

“China’s largest state banks have lowered their dollar deposit rates several times in recent months in line with guidance from central authorities seeking to prevent domestic stockpiling of dollars and ease depreciation pressure on the renminbi, according to bank statements and traders.”

This puzzle though isn’t critical to solve right now. Domestic foreign currency deposit growth slowed in late 2025—Onshore dollar deposits rose $60 billion in in the second half of 2025, well below the $250 billion in foreign exchange purchases reported in the FX settlement number let alone the $320 billion in purchases in forward-adjusted settlement.

Conclusion

Set these mysteries aside—in China, nothing quite lines up perfectly, as the exact management of China’s reserves and the non-reserve foreign assets (entrusted loans, co-investment funds) of the PBOC are treated as state secrets. That is why, in an important policy change, the U.S. Treasury isn’t going to rely exclusively or even primarily on the formal reserves reported by the People’s Bank of China in its assessment of China’s foreign exchange policies. The January 2026 Report state clearly:

“While Treasury has not designated China as a currency manipulator in this Report amid renminbi (RMB) depreciation pressure over the Report period, China stands out among our major trading partners in its relative lack of transparency around its exchange rate policies and practices. This relative lack of transparency will not preclude Treasury from designating China if available evidence suggests that it is intervening through formal or informal channels to resist RMB appreciation in the future”

Unless something changes. China is at risk of being designated if not in the next report (which technically covers calendar 2025) then in the report for the fall of 2026. All the data series showing the offshore activities of China’s state banks currently line—and they all point to a surge in intervention in the fourth quarter, and a nearly unprecedented level of backdoor intervention in December.

China’s $1 trillion plus goods surplus got a lot of attention back in November. The surplus for the full year was actually $1.2 trillion. The annualized paces of backdoor intervention in December also was well over $1 trillion. That won’t need to continue for long to get a little scrutiny.

* Reserve growth in BOP used to match the current account surplus and net FDI flows, or the basic balance, back in the days when China’s financial account was more or less completely closed, and exporters were required to convert foreign currency from exports into yuan at the PBOC.

** An entrusted loan to Exim that funds Exim’s external lending would be a domestic FX non-reserve asset of the PBOC and external asset of China’s banks or part of other loans in the balance of payments).

*** Back when U.S. deposit rates were zero the PBOC didn’t simply want to put its FX on deposit at the CDB to fund the CDB, so SAFE come up with a mechanism that kept its interest income up.