Asia is Adding to its FX Reserves in 2017 (China Included?)

Perceptions often lag economic shifts.

President Trump for example campaigned against China’s currency manipulation at a time when China was selling foreign exchange in the market, and thus didn’t meet the classic definition of manipulation.

And now I think—partly because of the coverage of the Trump Administration’s fight over designating China —there is a general perception that China is still selling significant quantities of foreign exchange to prop up its currency.

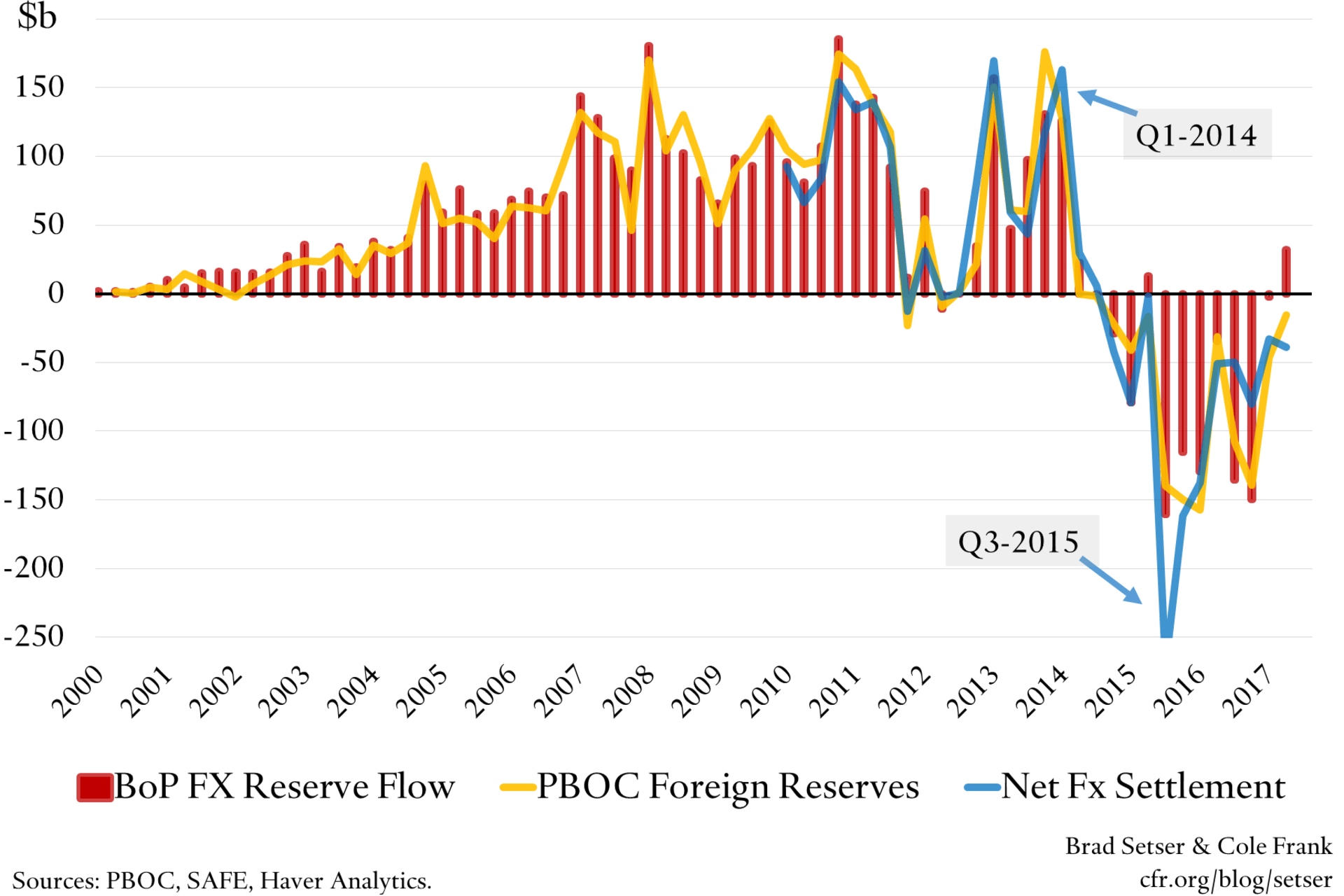

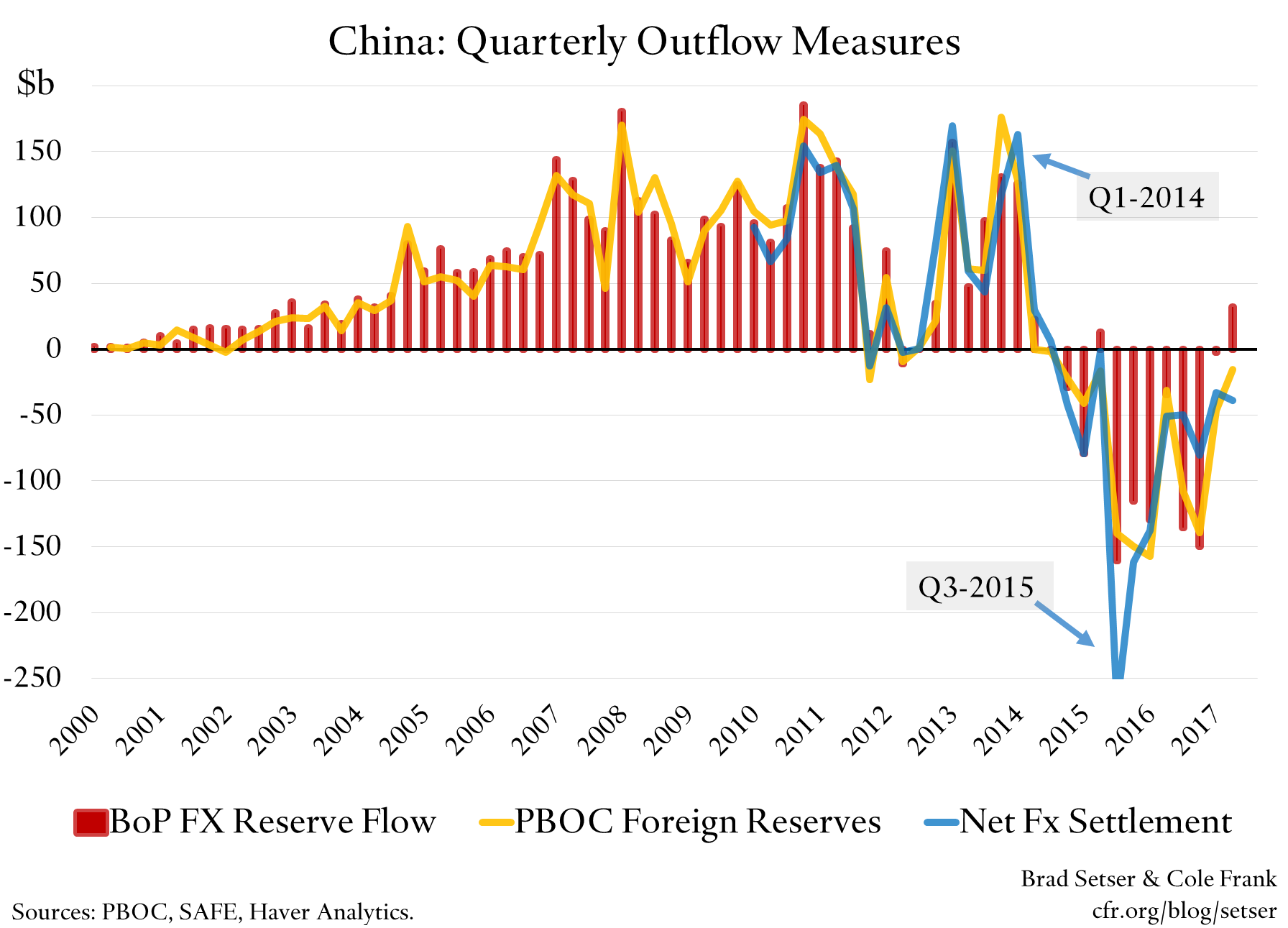

Yet, well, China’s balance of payments shows that China has added—ever so slightly—to its reserves in 2017. Reserves—in the balance of payments (BoP) data—were more or less flat in q1 and up by about $32 billion in q2. Year-to-date, reserves are up $29 billion.

The BoP measure incidentally should include interest income—so a positive BoP number doesn’t necessarily imply actual purchases in the market. That’s the logic the U.S. Treasury uses to take out estimated interest income for its “manipulation” calculations. (The counter argument is that this gives countries a free pass on their past intervention, and that a neutral stance for a country with lots of reserves should include regular fx sales to convert interest payments into local currency to cover the remittance of central bank profits back to the finance ministry, I personally would not give countries a free pass on interest income from past intervention).

But the notion that China is propping up its currency by selling lots of foreign exchange is now a bit dated.

Now for a bunch of throat clearing caveats.

The balance of payments data isn’t the only measure of China’s reserves, and the other measures show modest sales in 2017. There was a roughly $40 billion gap between BoP reserve growth (a flow) and what I think is the best alternative indicator of reserve growth: the sum of monthly changes in the foreign exchange reserves China reports on the PBOC’s yuan balance sheet.

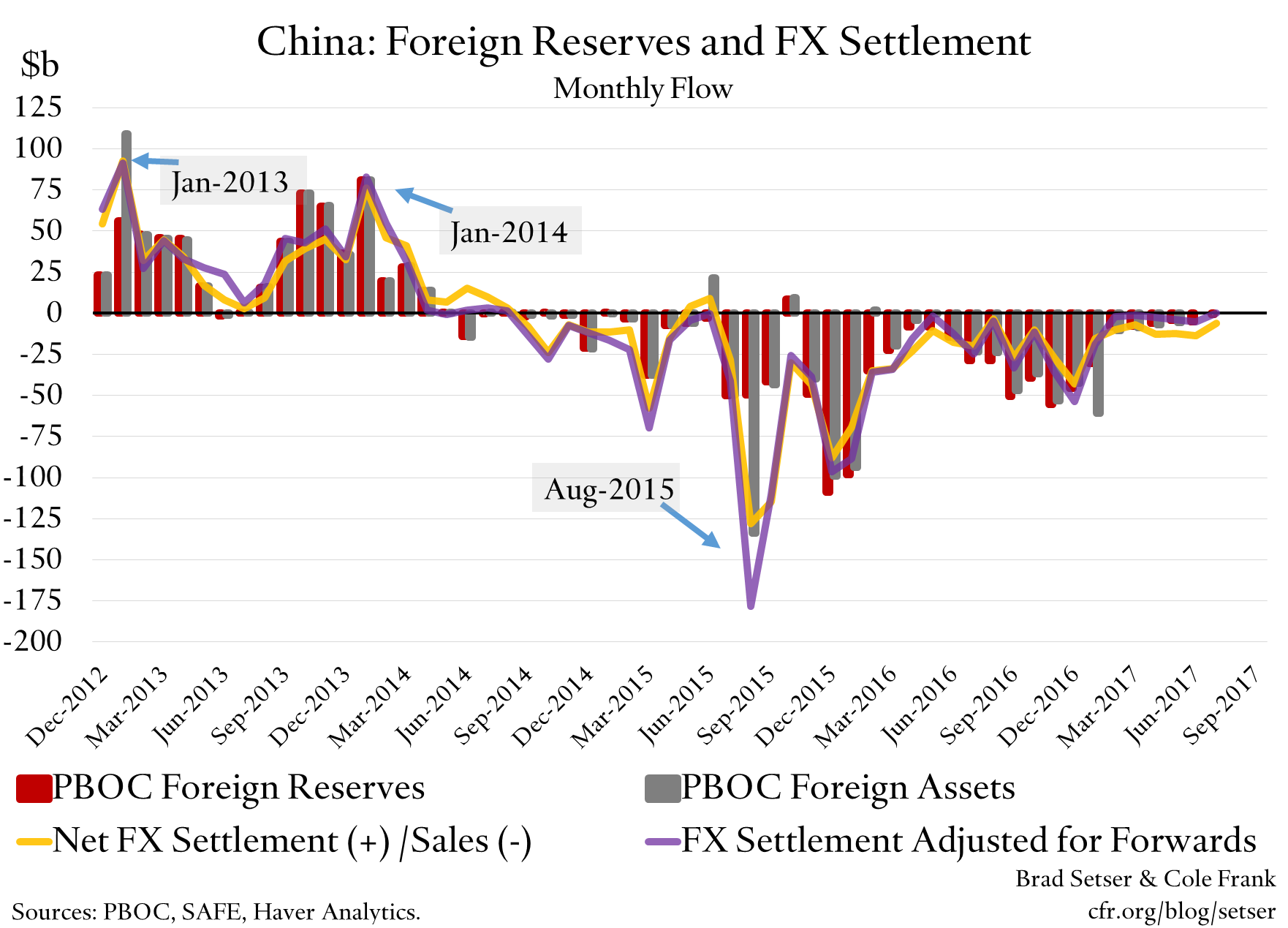

And the measure that I trust the most to capture what China is really doing (fx settlement) still shows (very) modest sales. Settlement includes fx sold by the state banks as well as the PBOC (though historically it tracks reserves reasonably well, as most purchases and sales have been done by the PBOC) so it isn’t quite the same concept as balance of payments reserves.

By the way, the PBOC balance sheet data and the settlement data are both out for July. Both are basically zero. If the q1 and q2 gap with the BoP measure persists in q3, the BoP measure should remain positive.

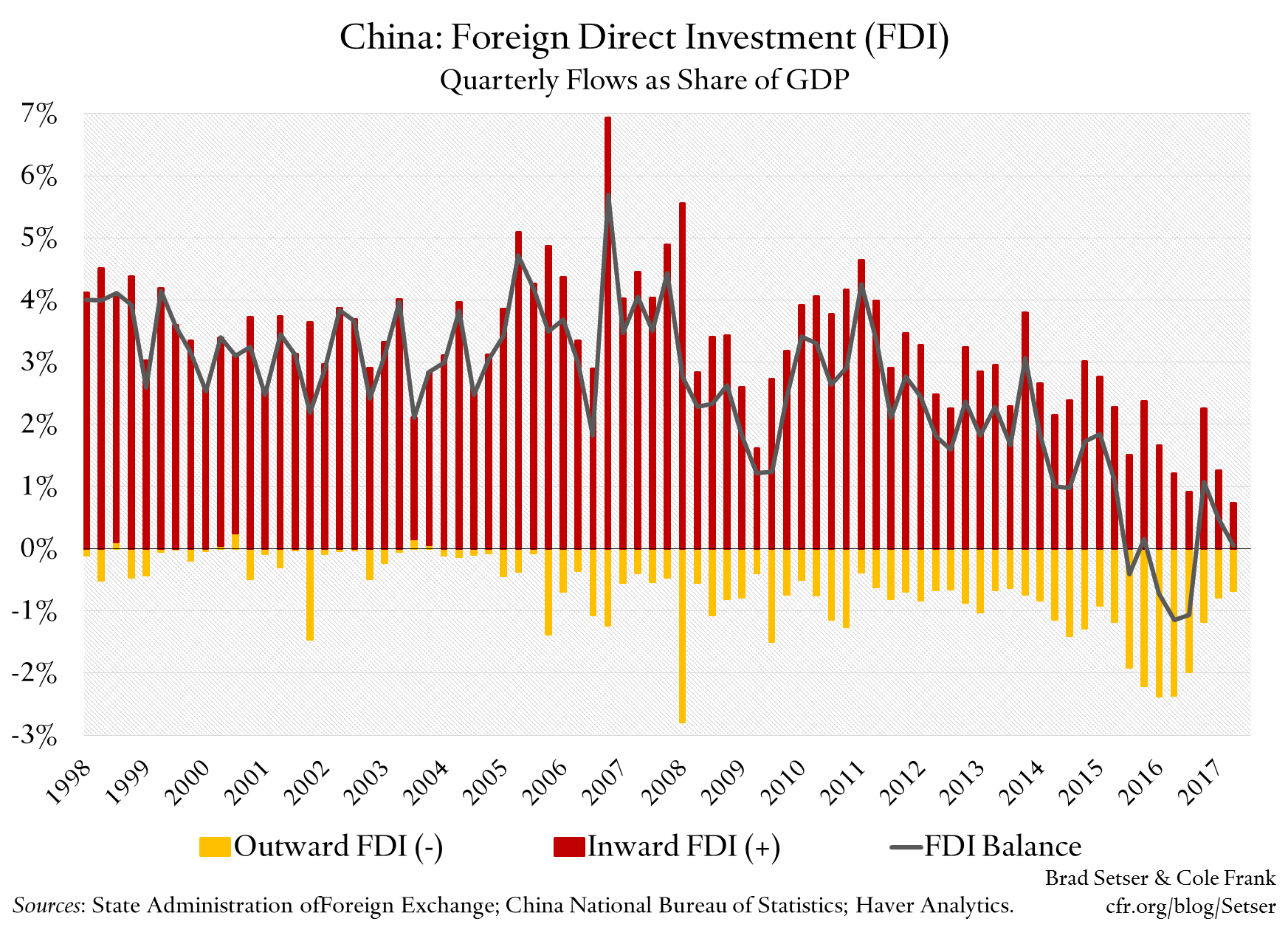

More importantly, there is no doubt that China has tightened its capital controls significantly, and that has helped limit pressure on the currency. You can argue that this is a backdoor form of intervention. Take away the controls and the yuan might depreciate, or China might need to be selling reserves to keep the yuan from depreciating.

One example of how the controls have had an impact: FDI outflows—which jumped when Chinese firms were essentially speculating on a further depreciation—have fallen significantly. We usually don’t think of FDI as “hot money” but the surge in outflows in late 2015 and the first half of 2016 clearly was driven by speculative bets against the yuan (as at the time the government was encouraging firms to go out so this was a permitted channel for outflows, and then things got a little out of hand).

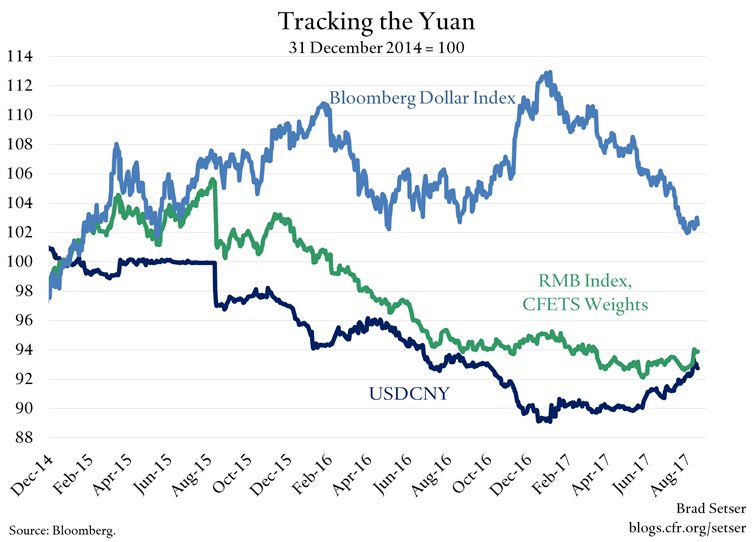

Of course, the controls didn’t work in a vacuum either: China has signaled that it is happy with the current level of the yuan (against a basket) and the dollar’s depreciation this year has made it easier for China to stick to its de facto basket peg, as holding the yuan stable against the basket has meant (modest) appreciation against the dollar. Both the management of the yuan and the controls have helped to stabilize expectations.

Finally the swing in balance of payment reserves into the black in q2 may overstate the real change from q1.

I like to look at broader measures of the state’s foreign assets, to capture the foreign exchange that China salts away (sometimes) in its state banks and in its sovereign wealth fund. In q1, the state banks were adding substantially to their foreign assets. The full balance of payments data isn’t available for q2 so we don’t know for sure what happened then, but the relevant indicators for the state banks suggest a pause in the growth in the external assets of the big state banks. Looking at broad measures of official asset growth, China was already adding to the state’s assets abroad in q1.

(The buildup of external assets in the state banks or the China Investment Corporation essentially substitutes for reserve growth; it is another way of making use of the foreign exchange China still generates from its goods surplus.)

A couple of other points are worth noting–

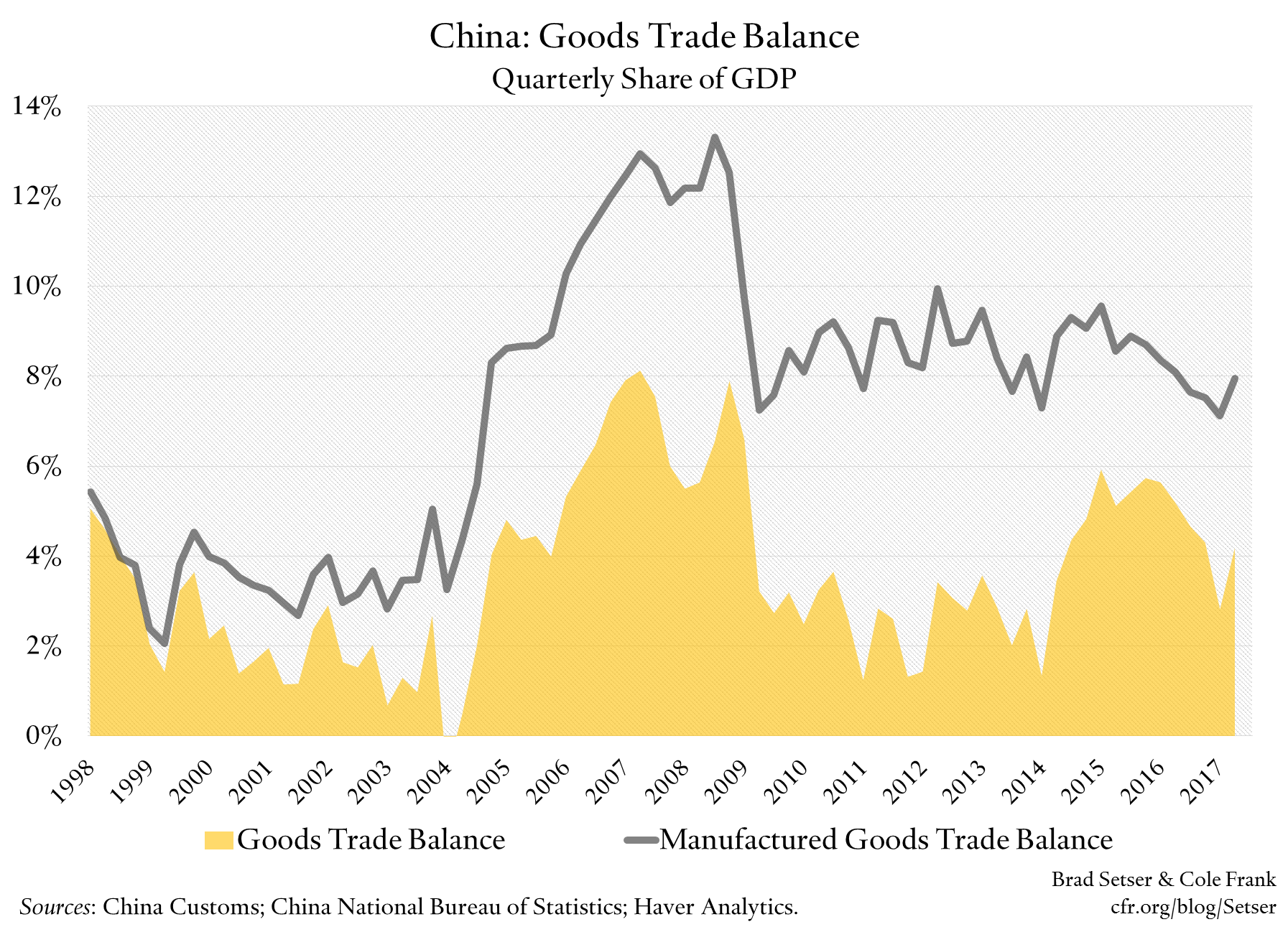

1) China’s goods surplus surged in the second quarter, thanks both to strong export growth and a slowdown in import growth.

The weaker real yuan is having an impact—there isn’t another good explanation for why Chinese year-over-year export volumes were up close to 10 percent in q2. Additionally the policy tightening carried out earlier this year brought import volume growth down. China’s surplus in manufacturing always has been large as a share of its GDP, and it looks to have gone back up in q2 (after falling for a few quarters).

The rise in the goods surplus though was offset (yet again) by a rise in the services deficit. Tourism imports jumped again (relative to q1).

This cuts both ways. There is evidence that at the current exchange rate China’s manufacturing sector remains very competitive, and will take global market share (Chinese export volume growth in q2 likely exceeded global trade growth). But the combination of a large goods surplus and only modest reserve growth implies ongoing (private) capital outflows continue even if the controls have cut off some big sources of pressure.

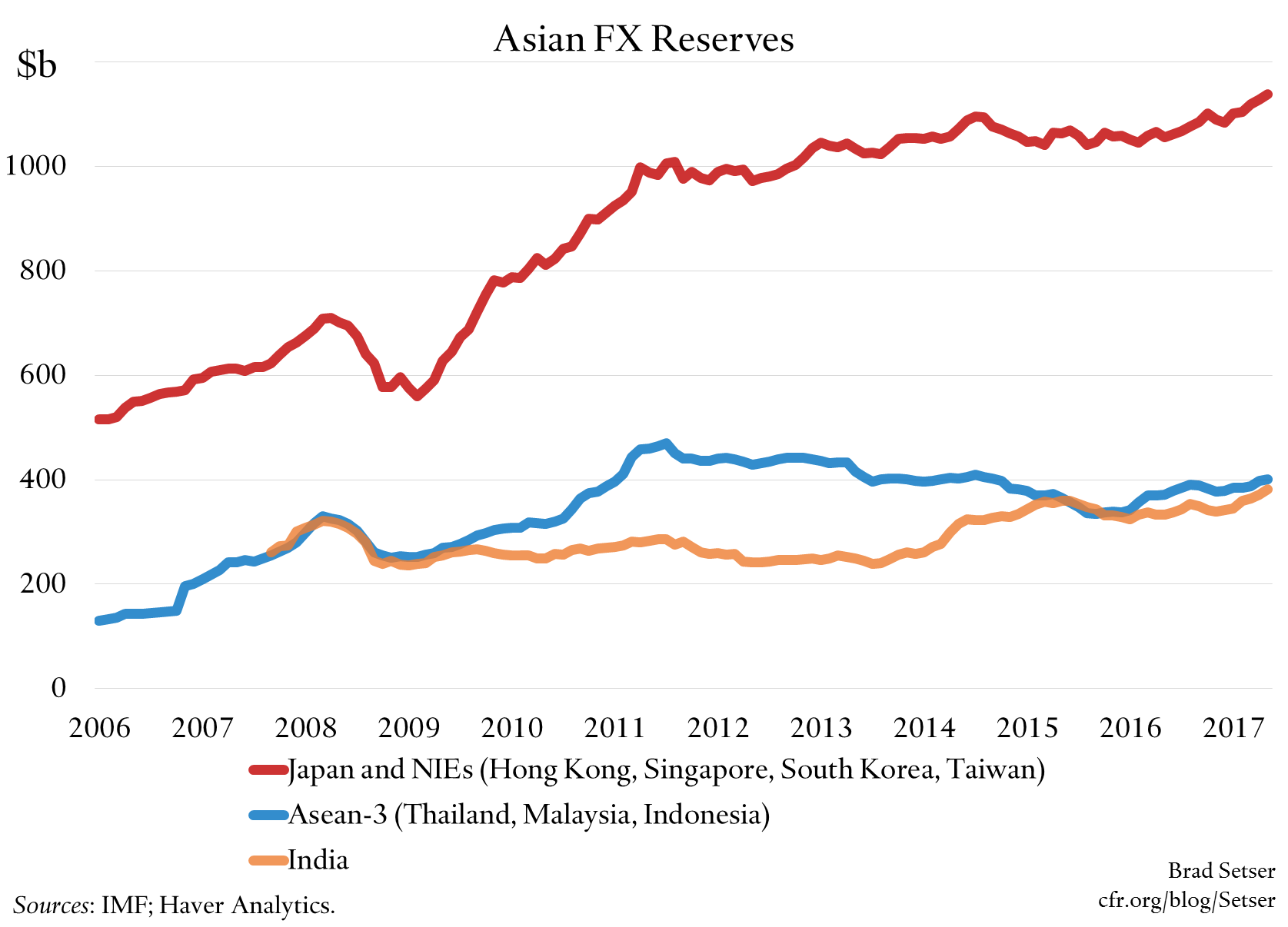

2) China’s return to reserve accumulation is part of a broader trend. Not at the pre-crisis pace, or at the 2010-12 pace, but noticeably. Singapore’s “true” reserve growth is higher than this chart implies too, as there has been a substantial buildup of official deposits offshore through the sovereign wealth fund that has held down reported reserves (see this post). And Singapore isn’t the only country adding to its reserves either. The reserves of most emerging Asian countries (Thailand, India and Indonesia for example) are now rising, and by more than can be explained by valuation gains.*

Reserve accumulation, as the IMF noted its latest external sector report, hasn’t been an important source of balance of payments imbalances in the last couple of years. But there are signs that this could be changing, at least somewhat.

* Korea’s headline reserves haven’t increased by much, but it still appears to be buying foreign exchange at key points in time to prevent the won from strengthening through 1100 against the dollar. For example, it may have intervened on July 27. But recent geopolitical stress and ongoing outflows from the national pension fund have allowed Korea to keep the won within Korea’s de facto target zone without sustained heavy intervention.