China’s Bizarre May Intervention Numbers

With the Osaka Xi-Trump summit producing an indefinite “truce” that halts further escalation (at least for now), there is every reason to expect the yuan to remain stable. The intervention proxies (surprisingly) didn’t show much activity in May, at the peak of the recent trade tension.

Sometimes an important (or so you think) indicator doesn’t match your expectations.

That was the case for me with China’s May proxies for its intervention in the foreign exchange market.

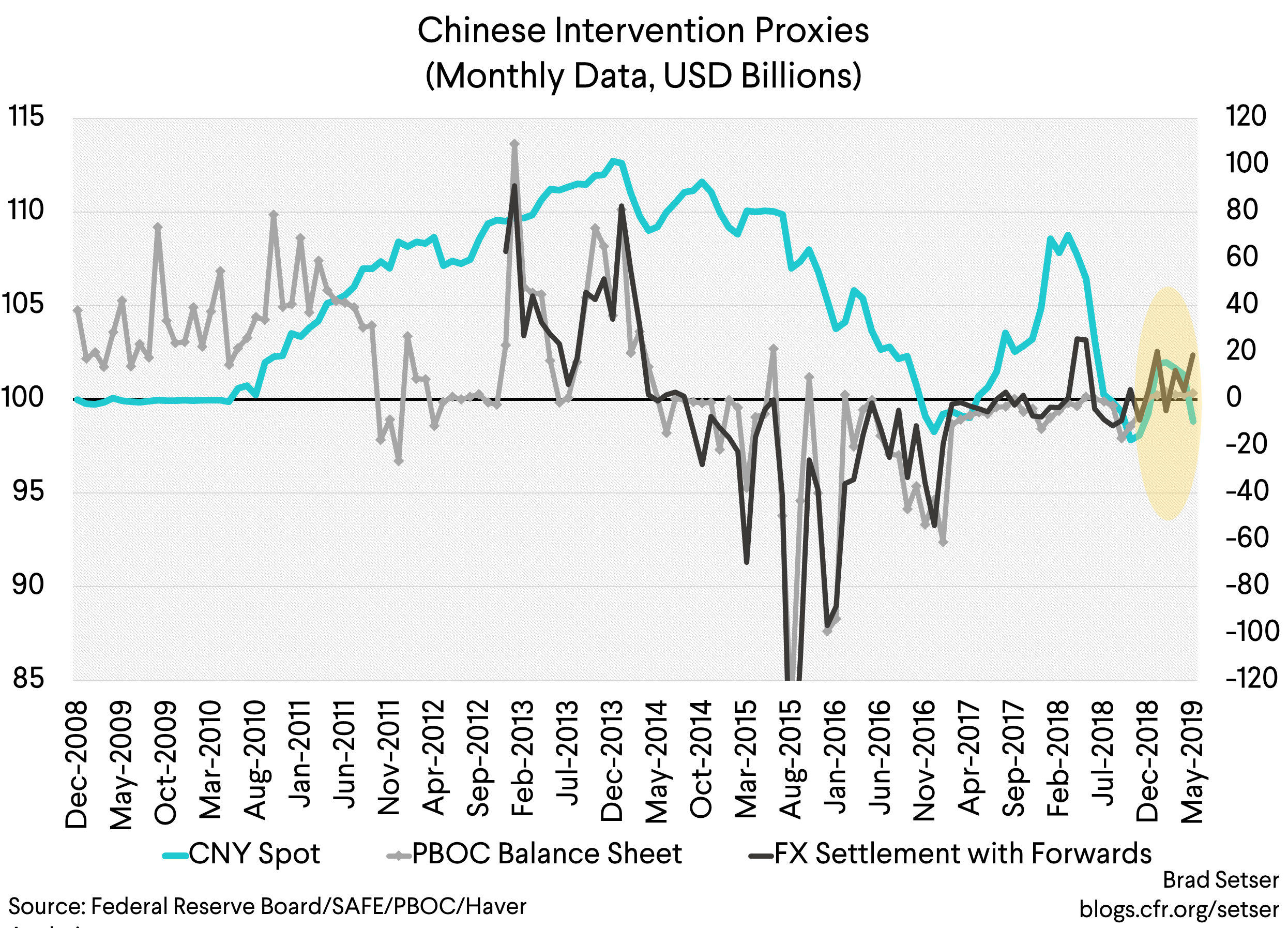

The PBOC balance sheet indicator was flat. That wasn’t really a surprise though. It has been flat for most of the past 24 months. Yi Gang (the governor of China’s central bank) has indicated that China isn’t intervening significantly—a comment that needs to be taken with a grain of salt, but one that also suggested the most obvious indicator of direct central bank intervention wasn’t going to register much.

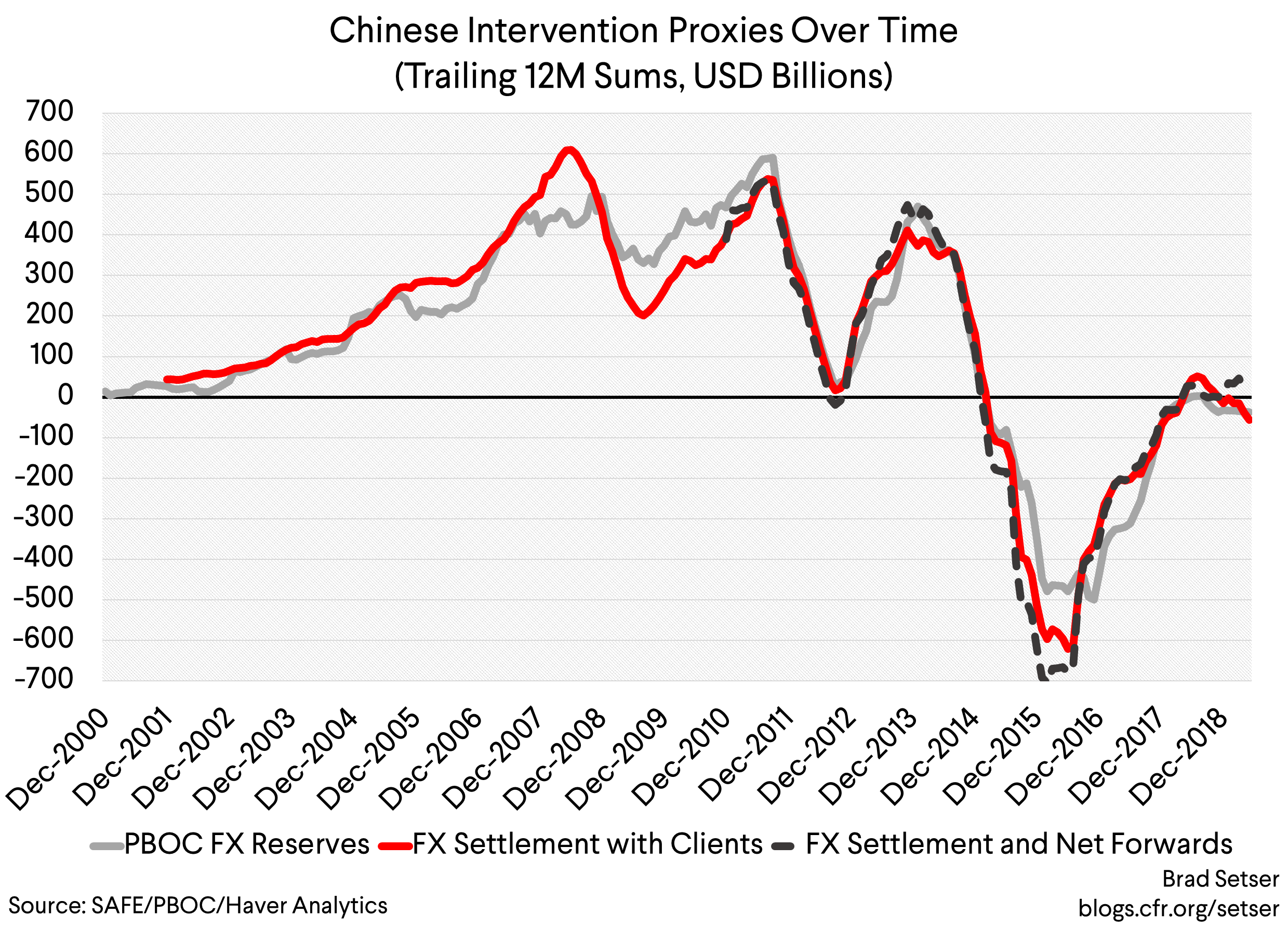

But China has at times used its state banks to disguise its intervention. The FX settlement numbers have historically captured much of that activity—back in the first decade of the 2000s, the pace of intervention implied by the FX settlement data was significantly larger than the pace of intervention implied by the PBOC’s balance sheet (see 04-05, and then 07-08 in the chart below). That of course was a time when China was really hiding its true intervention. FX settlement also showed a bigger swing in 2015, around the August devaluation.

FX settlement of course is one of those “only in China numbers” that stems from the enforcement of China’s system of capital controls. It captures the net balance of the PBOC and the big state banks in foreign exchange transactions.

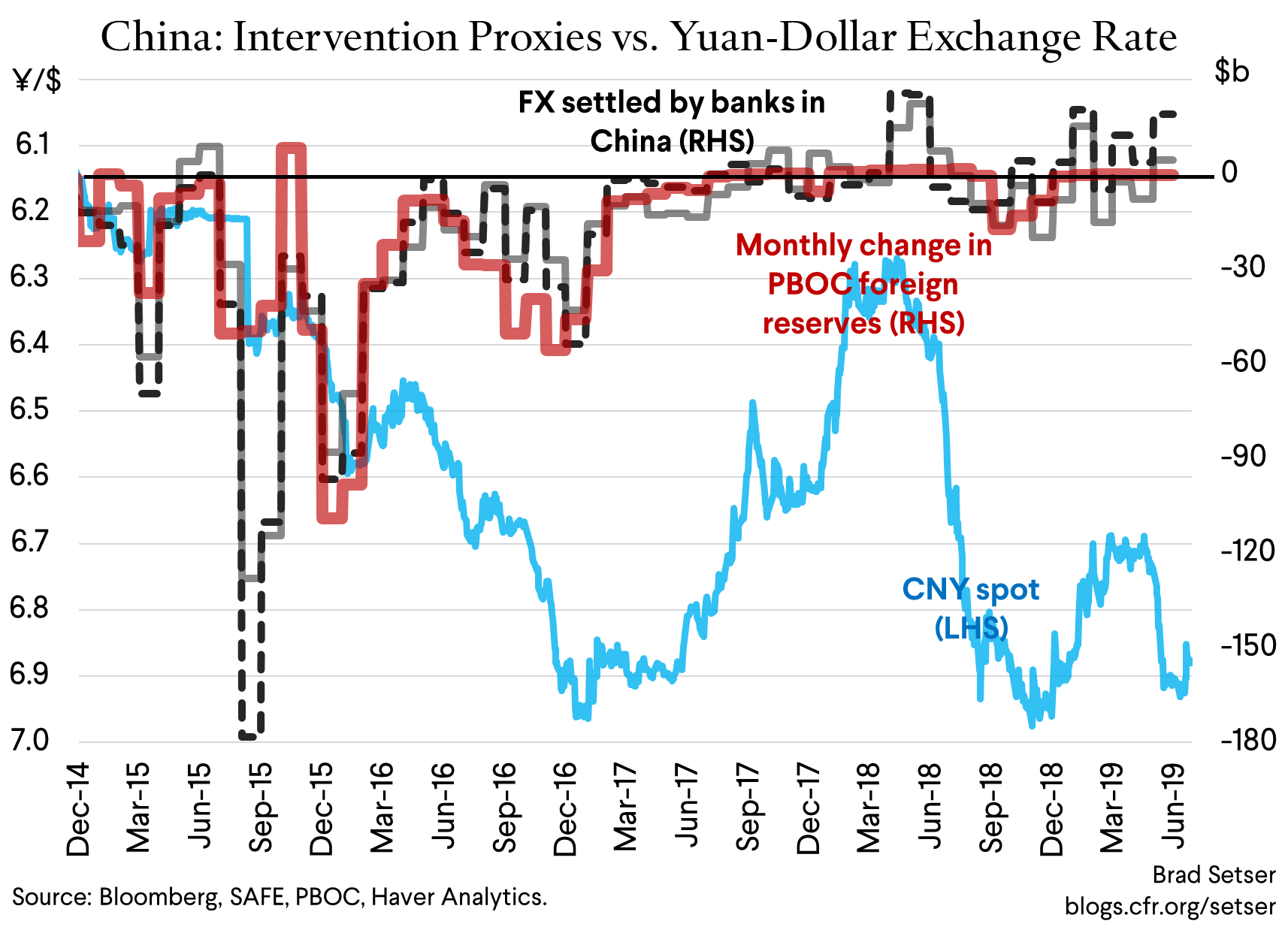

To be sure, the “equilibrium” level of intervention by China has gone down since 2014. Errors and omissions (capital flight) and the tourism deficit are now almost equal to the goods surplus. China doesn’t have a sustained need to build up foreign assets on the central bank’s balance sheet any more, particularly in a world where the net foreign asset position of the state banks continues to grow (all the Belt and Road lending perhaps). But even as the equilibrium level of intervention has gone down, the correlation between moves in the yuan and the need to intervene has remained. When the yuan is rising, China typically needs to buy dollars to keep it from rising too much (that’s the reason for the positive settlement numbers in the spring of 2018, and again in January, when there were hopes of a trade deal to soothe the stock market). And in the past, when the yuan is falling, China has needed to sell dollars to keep the yuan from falling too fast. There were—for example—sales last summer, after the yuan started to depreciate as the United States ratcheted up trade tension.

Based on all this, I expected China’s state banks to have sold dollars in May. The yuan was depreciating, and there were concerns that Trump’s tariff escalation could prompt a larger move.

But, instead, according to the settlement data (and especially the settlement data adjusted for forwards) China’s state banks were buying dollars.

That’s a puzzle.

Now the easy thing to do when data doesn’t match your priors is to dismiss the number.

And it is totally possible that the settlement data is now being massaged in some way.

But in the past I have argued that settlement is the best single indicator. So it is a little hard to abandon it…

There are a couple of potential explanations for the positive settlement number:

One is that, in anticipation of outflows, China really ratcheted up enforcement of its controls. Importers and others who wanted foreign exchange couldn’t buy it easily. Demand for foreign currency (at the current price) was effectively rationed.

Another is that in between China’s $40 billion May trade surplus, bond index inclusion, and reserve diversification (not just out of the dollar—those wanting to hold something other than dollars and get a positive interest rate have limited choices these days) there was a bit of foreign exchange coming into China in May.

All in all, though, it does suggest that China is firmly in control of its financial account (and its exchange rate). A move now—particularly if there is a tariff truce in Osaka—would be China’s choice, not that of the “market” (recognizing that this is a market that is still managed in a host of ways).

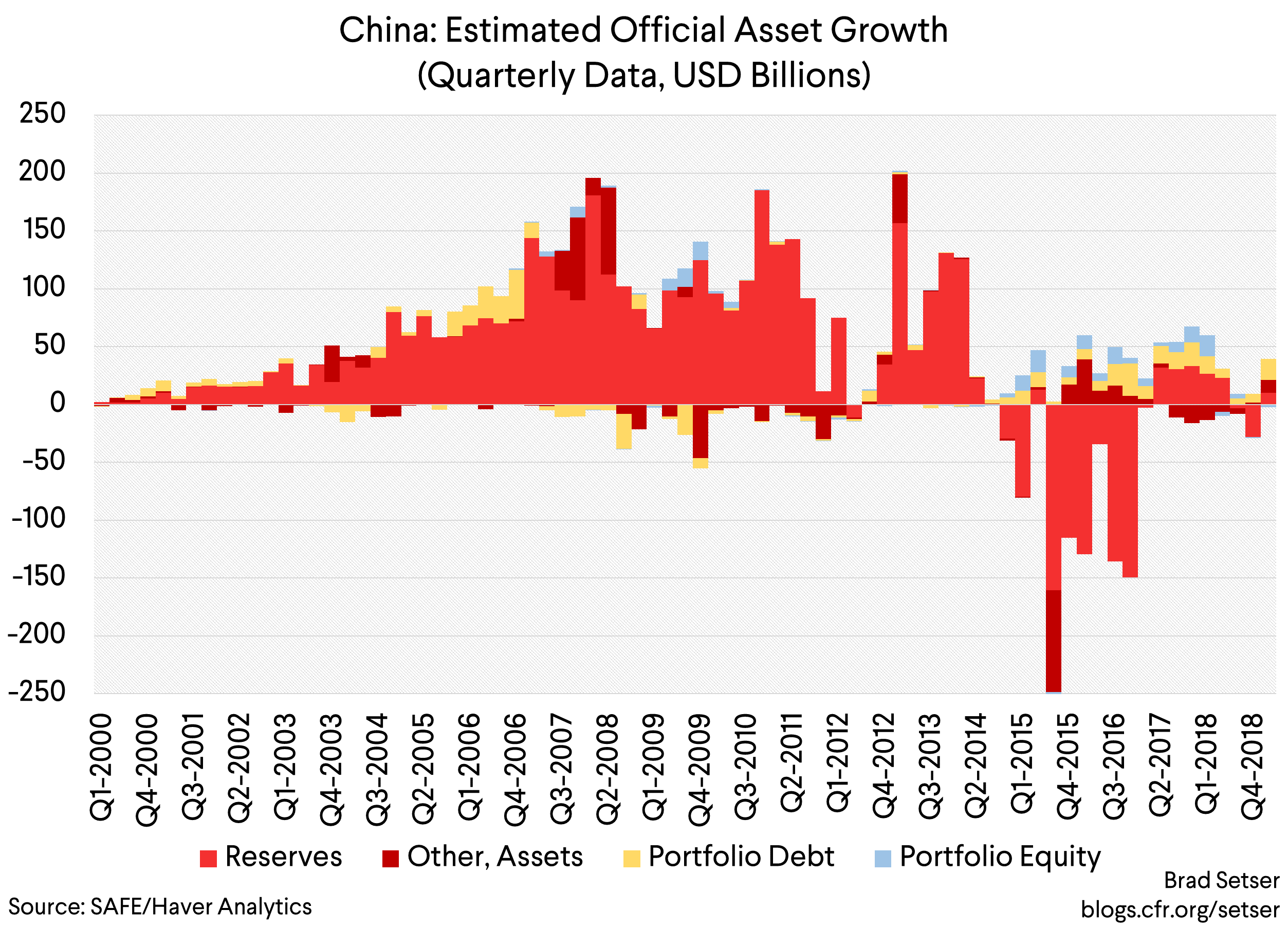

That’s clear if you go back and look at the data for the first quarter in China’s detailed balance of payments. Q1 remember was a period of relative calm: the yuan was stable, and the United States and China appeared to be heading toward some kind of trade deal after the Buenos Aires summit. Reserves—and the most obvious hidden reserves, the foreign exchange that the banks hold as part of their reserve requirement—rose a bit in Q1.* And the state banks were adding to their foreign bond portfolio. Total foreign asset accumulation by China, Inc was huge by the standards of the past, but so long as China’s assets are rising not falling, it is hard to tell a story where China is under real pressure.

Q2 may be a bit different—the formal data won’t be out for another three months, and it may show some hidden sources of pressure. But if the trade truce holds for the duration of the third quarter, I don’t see any force strong enough to push the yuan off the course set by the People’s Bank of China.

* For the past couple of years, the balance of payments measure of reserves has been just a bit stronger than the change in the PBOC’s reported “foreign exchange reserves” on their balance sheet would imply it should be. The precise reason for this discrepancy isn’t clear. It is possible that the PBOC balance sheet measure excludes interest income on China’s existing reserves. The gap between these two measures isn’t big, but it has been persistent.