By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Benjamin Della RoccaAnalyst, Center for Geoeconomic Studies

Since the summer, Chinese real-estate behemoth Evergrande has been buckling under outstanding debts worth some $300 billion. Chinese authorities have consistently chalked up its plight to managerial failure. “Evergrande’s risks,” China’s central bank scolded this month, “are mainly due to its own poor management and blind expansion.” But, as we explained recently in Foreign Affairs, Evergrande’s collapse is the logical consequence of Beijing’s chosen strategy for economic development.

The Chinese Communist Party grounds its legitimacy in maintaining high economic growth. To deliver on its growth targets, it has for decades stoked real-estate speculation and unproductive corporate borrowing. The result is continuously rising levels of leverage across China’s economy.

Beijing knows its trajectory is ultimately unsustainable. But history suggests it won’t change course anytime soon.

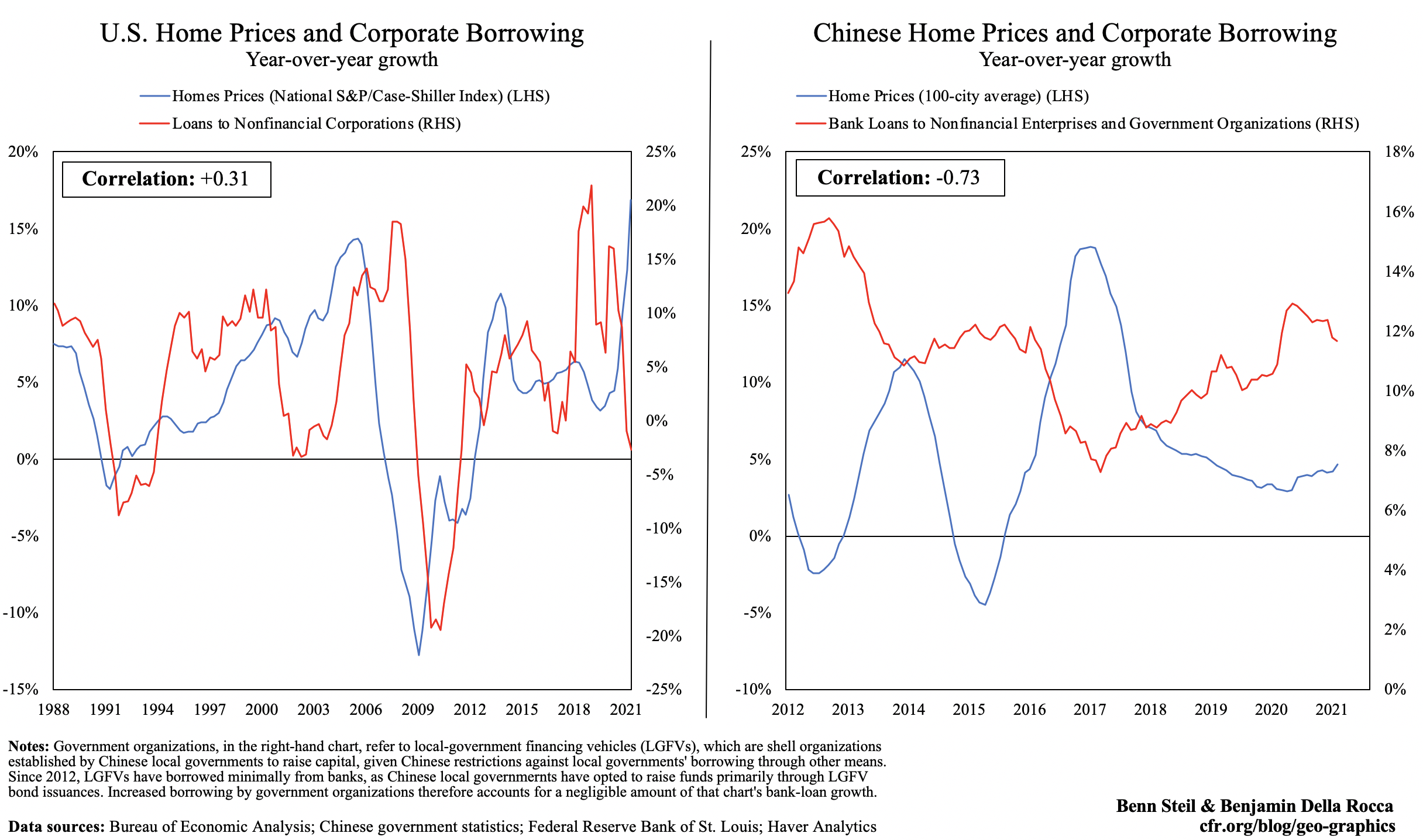

The left-hand chart in the graphic above shows corporate leverage and home prices in the United States—a market economy. These metrics typically move in tandem. When the economy is strong, corporate borrowing and home buying rise; they then fall when the economy flags. But the opposite is true in China. Since Xi Jinping took power in 2012, as the right-hand chart shows, Chinese corporate leverage and home prices have correlated negatively. The reason? Despite ever-rising imbalances in real-estate and corporate-credit markets, Beijing knows that a downturn in either would jeopardize short-term growth. So as policymakers curb property speculation, they funnel risky loans to corporations to keep growth up. Later, as default risks rise, they do the reverse.

This pattern suggests that Chinese authorities, even after Evergrande, will continue siphoning credit to property developers and state-owned enterprises that use loans unproductively.

And, indeed, Beijing is now compensating for the Evergrande growth hit by allowing real-estate developers to borrow directly in the bond markets, while Chinese local governments are subsidizing home buying.

Plus ça change, plus c’est la même chose. Or at least that is what we will witness until rising defaults and falling productivity fatally undermine Xi’s political credibility.