By experts and staff

- Published

Experts

![]() By Benn SteilSenior Fellow and Director of International Economics

By Benn SteilSenior Fellow and Director of International Economics

By

- Benjamin Della RoccaAnalyst, Center for Geoeconomic Studies

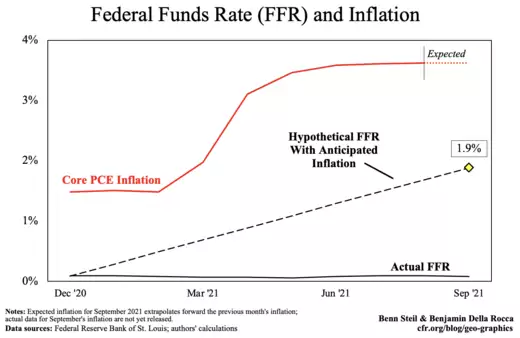

Last week we learned that August core PCE inflation, the Fed’s preferred inflation measure, hit 3.6 percent for the third consecutive month. Yet as the evidence mounts that current inflation is not merely “transitory,” and the Fed raises its inflation forecasts in consequence, the Fed’s guidance as to when it will raise its policy rate above 0-0.25%, where it has been stuck since March 2020, has barely budged.

As we explained recently in the Wall Street Journal, past Fed behavior—as exemplified by a close correlation between the Fed’s inflation forecasts and its rate guidance—suggests that its policy rate should already be at 1.9%. So why is the Fed still signaling near-zero rates well into 2022?

Observations of past and present Fed officials, whom we quoted in our piece, suggest the answer.

Whereas Fed officials cannot make their inflation forecasts come true, they can make their rate forecasts come true—since they themselves control those rates. It is therefore increasingly clear that Fed officials are trying to maintain “credibility” by doing what they predicted they would do—even though current inflation data no longer validate those predictions. Such behavior is, however, a recipe for bad long-run macroeconomic outcomes—meaning lower future growth and higher unemployment.