My Latest Take on China’s Foreign Exchange Intervention Proxies

This one is for my currency trading friends…

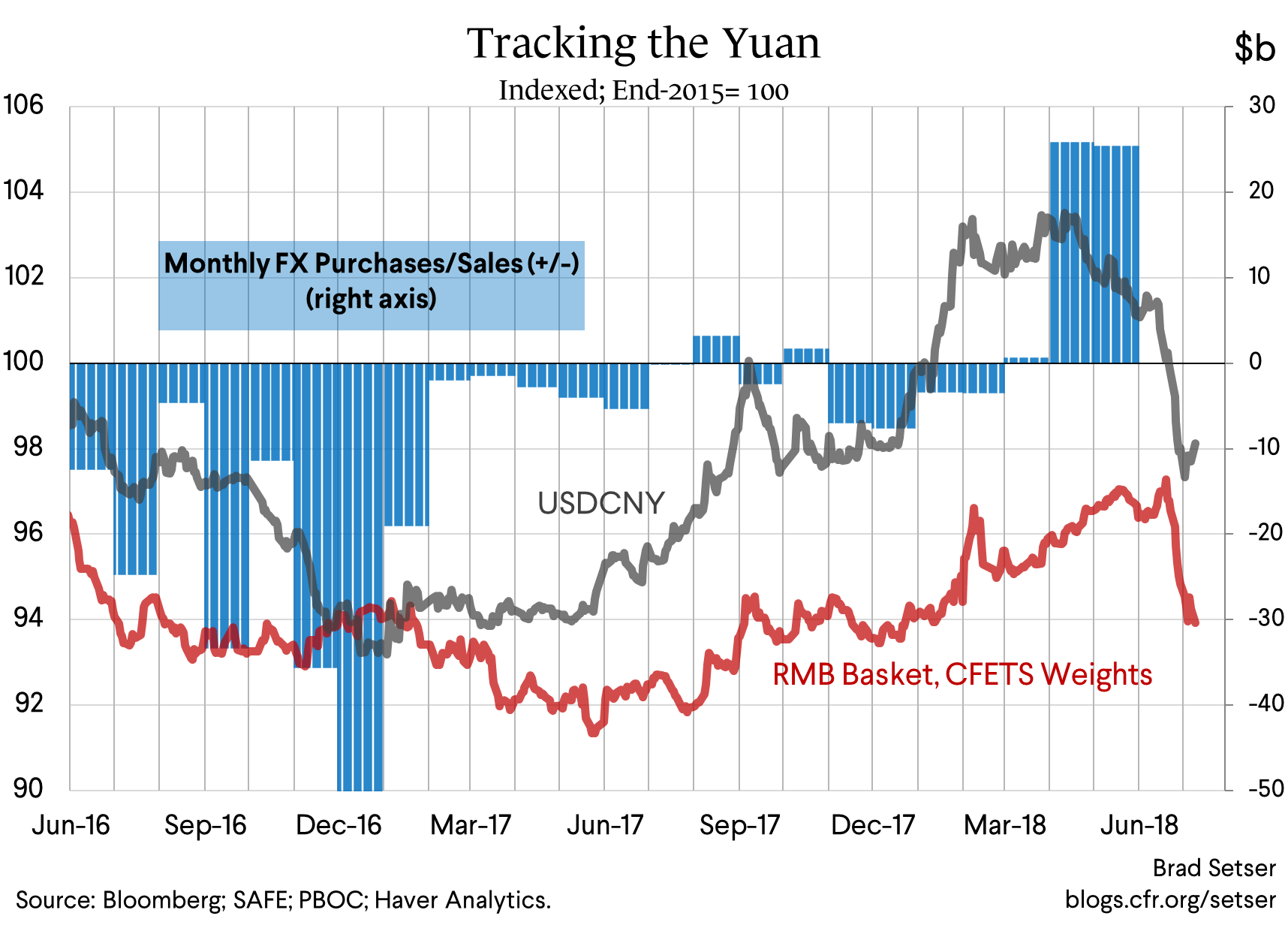

It is too late to be of any practical use now, but I finally think I understand the “signal” sent by the net purchases of foreign exchange by China’s state banks in the foreign exchange settlement data for April and May. Purchases, after adjusting for swings the forward position, topped $20 billion in both months.

“Settlement” is in my experience the best proxy for China’s actual intervention in the market, in part because it doesn’t just include the PBOC. It—like the deeply missed old FX position data—captures the activity of both the PBOC and the state banks. It tends to show a bit more volatility than the direct measure of the PBOC’s own balance sheet.

The net purchases in both April and May surprised me a bit, for two reasons:

- The purchases didn’t come when I expected them. I expected—based on what the rest of Asia was doing, as well as market reports—to see a bit of intervention in January and February.

- The purchases came when the yuan was declining a bit against the dollar. And in the past purchases have been correlated with times when the yuan is rising against the dollar, and sales with times when the yuan is falling against the dollar (in both cases China’s intervention acts to slow or even block any market move, and thus to keep the yuan inside a trading range—maintaining the stability that China’s leaders want).

With the benefit of hindsight, I have a new theory: the purchases likely were a signal that China wasn’t happy with the yuan’s strength against the basket.

That’s why the purchases came when the yuan was creeping up against the basket – e.g. the yuan wasn’t falling fast enough against the dollar to prevent a general appreciation against China’s trading partners at a time when the dollar was rising.

If this theory is correct, the rise in state bank purchases in April and May effectively meant there was an open door for the yuan to fall (versus the basket) but not for the yuan to rise (against the basket).

The implication of course is that China is now managing the yuan inside (undisclosed, and possibly variable) band around the basket.

The strength of the May settlement data also might explain the surprise rise in headline reserves in June. The rise in headline reserves suggests, given the impact of currency moves on the valuation of China’s euros and yen, that China might have been buying foreign exchange early in June (remeber that the yuan was strong against the basket in early June). That at least is one hypothesis. The other is that the change in headline reserves is now almost pure noise most of the time.*

Before the yuan started to depreciate in the middle of June, all the standard measures of China’s reserve growth had actually swung into neutral or positive territory on a trailing 12month or trailing four quarter basis, with the balance of payments data showing the strongest growth of any measure.**

All this obviously is based on what now is very lagged data. It reflects a world when the yuan was drifting up against the basket, not a world where the yuan is falling fairly quickly against both the dollar and the basket.

And while it tells us that China may have found the yuan’s strength against the CFETs basket earlier this year a bit uncomfortable, the real question now is whether the yuan has moved back to level that China is willing to defend.

China pretty clearly intervened to block further depreciation last Tuesday, when it stepped in at around 6.7 against the dollar (keeping the CFETS basket at around 95, and thus preventing any significant depreciation against the basket for the year). We don’t yet know whether that is a signal that China is now happy with the level of the yuan, or whether it is just a signal that China was unhappy with the pace of the recent move.

The frustrating thing, from my point of view, is that China’s reported intervention (dollar sales) took place very early in the month. Which means that there won’t be good data on what China actually did in the market until late August. It also was early in the quarter, which highlights the problem with the Treasury’s (rumored) quarterly with a quarter lag standard in the side deal with Korea on currency. And if Korea followed China’s lead in routing intervention through state banks, it might not even show up at all.

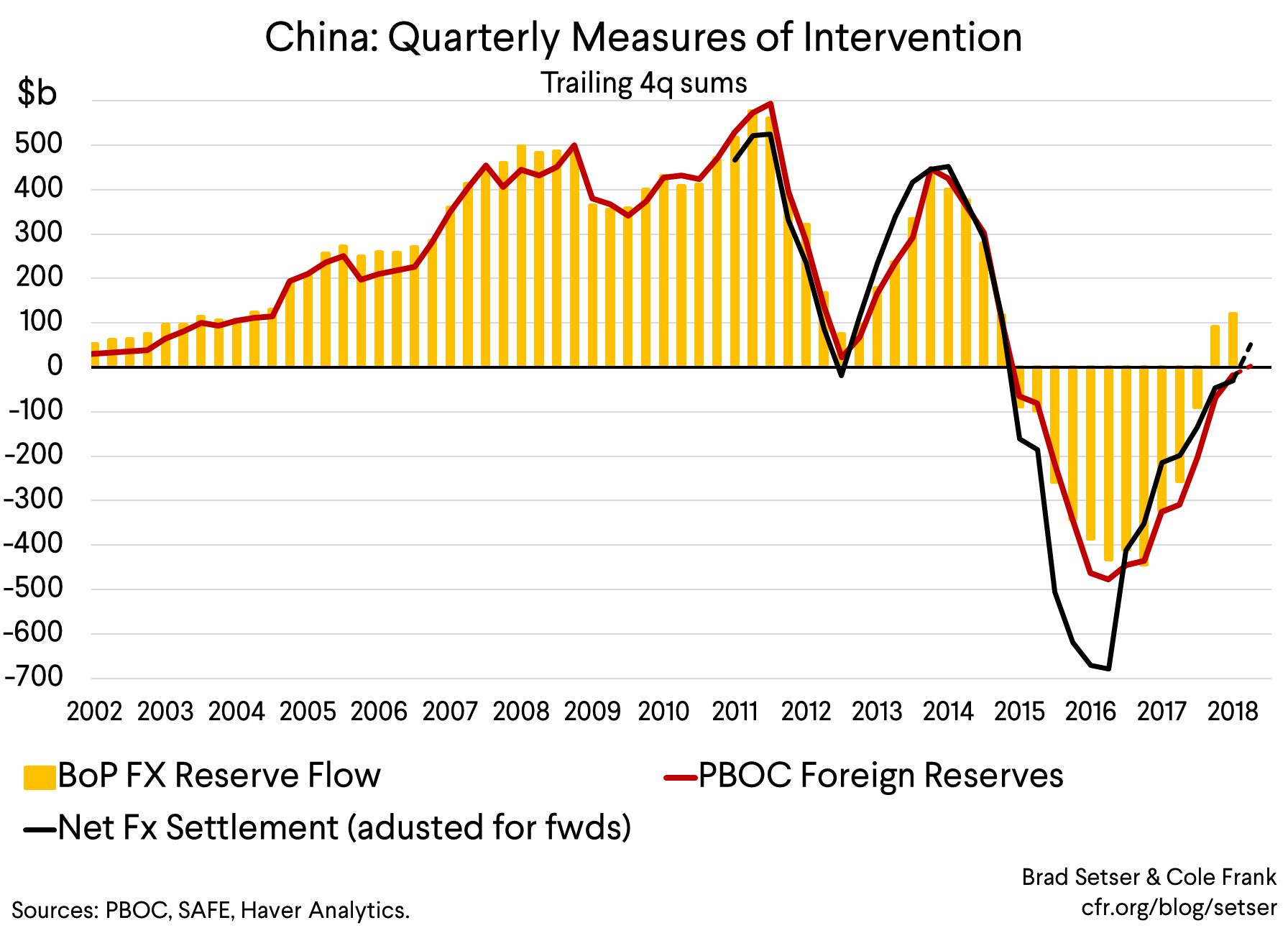

In aggregate China’s intervention over the last fifteen years has tended to keep China’s currency weaker than it would otherwise be. China didn’t accumulate over $3 trillion in reserves by accident.

And there is a common view that in order to push the yuan down, China needs to buy more dollars (and sell yuan), and if China wants the yuan to strengthen, it would need to sell dollars (and buy yuan).

But in practice that isn’t how China’s currency management has tended to work. China tends to buy foreign exchange when the yuan is appreciating, whether from the pressure generated by a large (goods) trade surplus or from the pressure created by capital inlfows. Appreciation creates expectations of appreciation, and pulls capital into China. So China has tended to intervene more when its currency is appreciating than when the yuan is stable, as intervention is needed to control the pace of appreciation. And the same process works in reverse. Reserve sales have tended to occur during periods of depreciation, with the sale of foreign exchange acting to limit the pace of depreciation.

Intervention thus is—together with the daily fix (the mid-point in the yuan’s daily trading band) —the tool China uses to signal where it wants its currency to be. Controlling the pace of appreciation and depreciation through intervention is a big part of how China keeps its currency “basically stable at a reasonable and balanced level.”

China has in the past also encouraged the state banks to lend abroad and to purchase foreign debt during periods of appreciation to reduce the amount that the PBOC needs to buy—and, at other times, it has limited the amount the PBOC needs to sell by restricting the abiltiy of Chinese residents to move funds out of the country. China manages capital flows as well as the level of its currency.

But it is a lot easier to manage capital flows efficiently if pressure on the currency isn’t one-sided.

The challenge China faces now—if it wants to avoid further depreciation, which it may not want to do amid an escalating trade war — is making sure that the renminbi’s recent depreciation is not viewed as a signal that China’s currency is now a one way bet down. Interest rate differentials between the U.S. and China have fallen, so managing expectations of the currency’s direction of movement in a sense has become more critical. Fortunately, with $3.1 trillion in formal reserves and more funds squirreled away at the CIC and in the state banks, China isn’t short on ammunition .... ***

----

*/ The standard valuation adjustment relies on a lot of assumptions about the composition of China’s portfolio and the timing of when it books mark-to-market gains on its bond portfolio. The intervention proxies (the change in the foreign assets reported on the PBOC’s balance sheet, the “settlement” data) are in my view more reliable. They just aren’t yet available for June.

**/ Balance of payments reserve growth has been consistently higher than the rise in reserves implied by changes in the PBOC balance sheet over the last year, for reasons I don’t fully understand.

***/ $3 trillion is a psychologically significant number for China’s reserves, but not an economically significant one (as the IMF recognized in last year’s article IV). China’s reserves more than cover its total external debt, and far exceed its short-term external debt. And with reinforced capital controls, China doesn’t need reserves to back a large share of M2. Turkey and Argentina are legitimately short on reserves, China isn’t.