Shadow FX Intervention in Taiwan: Solving a 100+ billion dollar enigma (Part 2)

Large-scale purchases of foreign bonds have become the central flow sustaining Taiwan’s massive current account surplus and keeping the Taiwan dollar weak. The size of this flow raises the question of who supplies Taiwan’s lifers with FX hedges.

By experts and staff

- Published

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow- Guest Blogger for Brad Setser

This is the second post in a series* on Taiwan’s life insurers and their private & sovereign FX hedging counterparties. It’s the product of a collaboration with S.T.W**, a market participant and friend of the blog. Printable versions of entries in this series will be available in pdf format on his site (Concentrated Ambiguity).

Part Two: Perennial Trade Surpluses, Debt Outflows, & the Rise of the Life Insurers

This blog seeks to provide the clearest possible understanding of financial flows between Taiwan and the rest of the world. It will commence by examining Taiwan’s enduring Current Account surpluses, their reflection as debt outflows in the Financial Account, as well as the key role of the life insurance industry, acting as the primary intermediator for Taiwan’s savings.

A. Perennial Trade Surpluses

With the progression of globalization during the past 30 years, Taiwan first carved out and then cemented its place as the backbone of the Information and Communication Technology (ICT) value chain in Northeast Asia. It is home to numerous giants in electronic and semiconductor-related industries, has the highest share globally of ICT value-added as a share of total GDP (15% vs. a global average of 1.4%)[1] and delivers chips and other hardware to practically all nations assembling these components into final products.

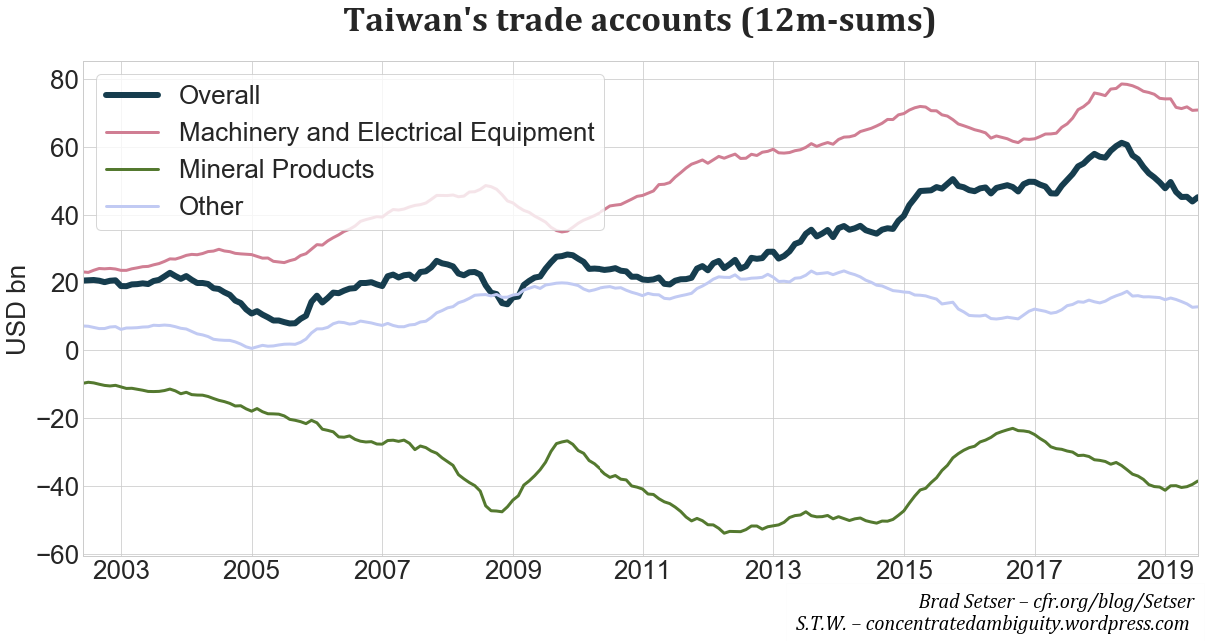

Taiwan’s strength in the ICT trade is clearly visible in its trade accounts, with a trade surplus in this category easily averaging north of 10% of GDP for the past 20 years.

Due to a lack of domestic natural resources, Taiwan is dependent on foreign oil, gas and other minerals, a fact also clearly visible in its trade statistics and the prime detractor of the large ICT-related surplus. All other product categories exhibit low relative volatility (compared to the two aforementioned ones) and, when all combined, result in a small but steady trade surplus in the ‘other’ category.

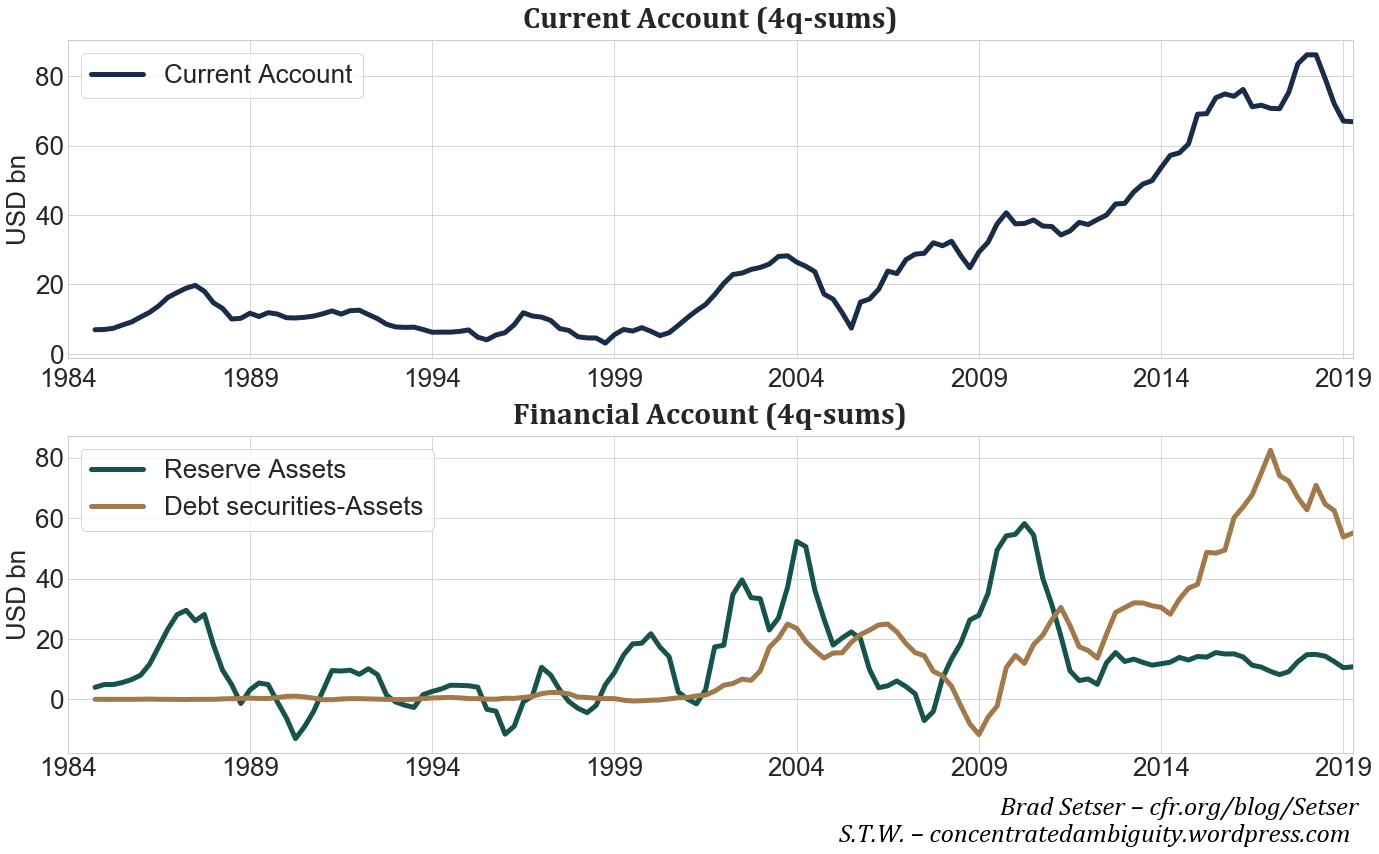

The quarterly released Balance of Payments (BoP) statistics (upper panel, Fig. 2) conform to the dynamics shown by the monthly trade figures, highlighting Current Account surpluses on the order of ~USD 70bn, or well over 10% of Taiwan’s GDP, during the past four years.

B. Slowing FX Reserve Accumulation & Private Debt Outflows

Surpluses on the Current Account have to axiomatically be accompanied by an increase in net claims on the Rest of the World. This manifests itself as Financial Account outflows in Balance of Payments accounts.

As with the trade statistics before, the Financial Account consists of dozens of line items, yet the key drivers can be summarized by two series alone: the accumulation of FX reserves by the CBC and the purchases of overseas debt by the private sector, both shown in the lower panel of Fig. 2. FX reserve accumulation was the predominant mechanism for recycling Taiwan’s current account surplus until 2003 and was briefly resurrected in the immediate aftermath of the financial crisis in 2008. But formal reserve accumulation has since settled down to a much lower and less volatile level of around USD 10bn per annum.

Private acquisitions of foreign debt grew in the mid-2000s, but these flows partly reversed during the global financial crisis. They subsequently picked up notably, replacing FX reserve accumulation as the main Current Account recycling mechanism and virtually matched the increase in the Current Account surplus after 2014.

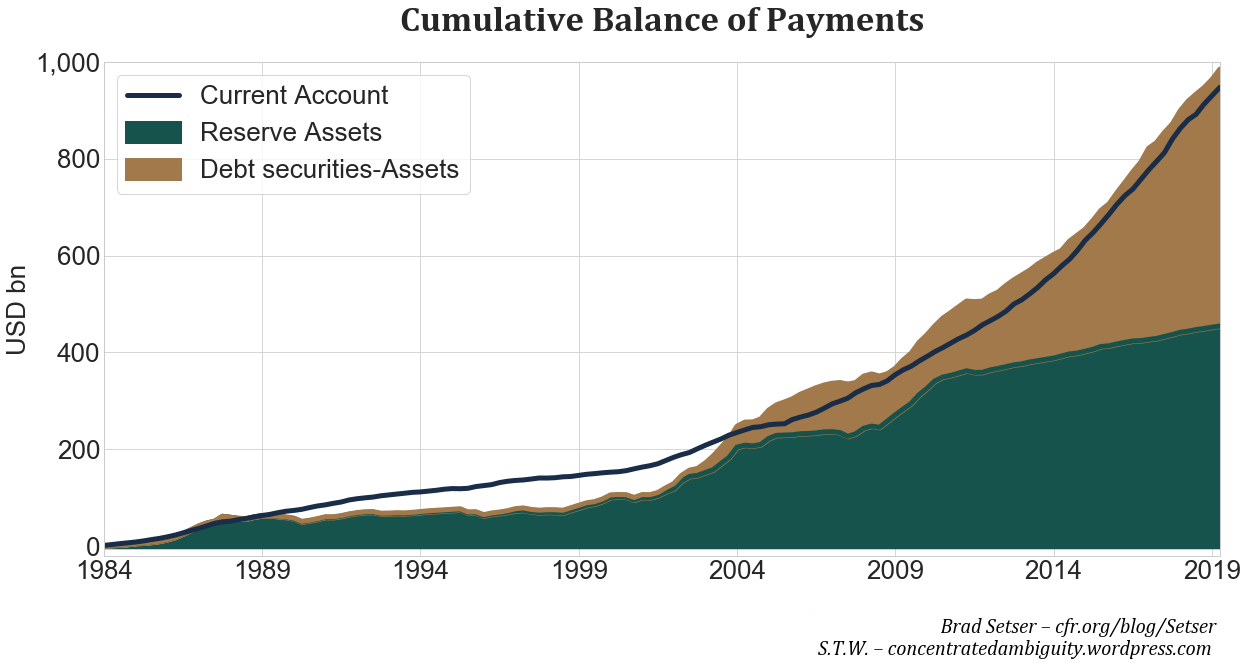

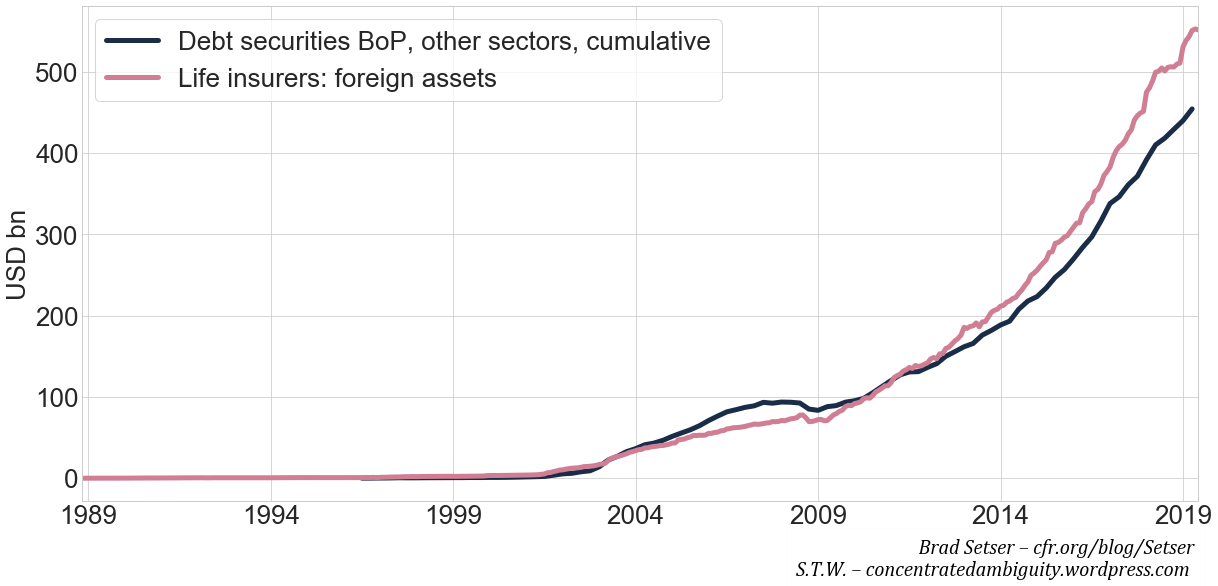

Fig. 3 shows the same information, this time as cumulative sums starting in 1984. Especially in recent years, the explanatory power of the two discussed categories is very high, almost exactly matching the cumulative Current Account surpluses of USD 900bn. This cumulative sum is roughly equally split between FX reserves on the CBC’s balance sheet and holdings of foreign debt by Taiwan’s private sector.

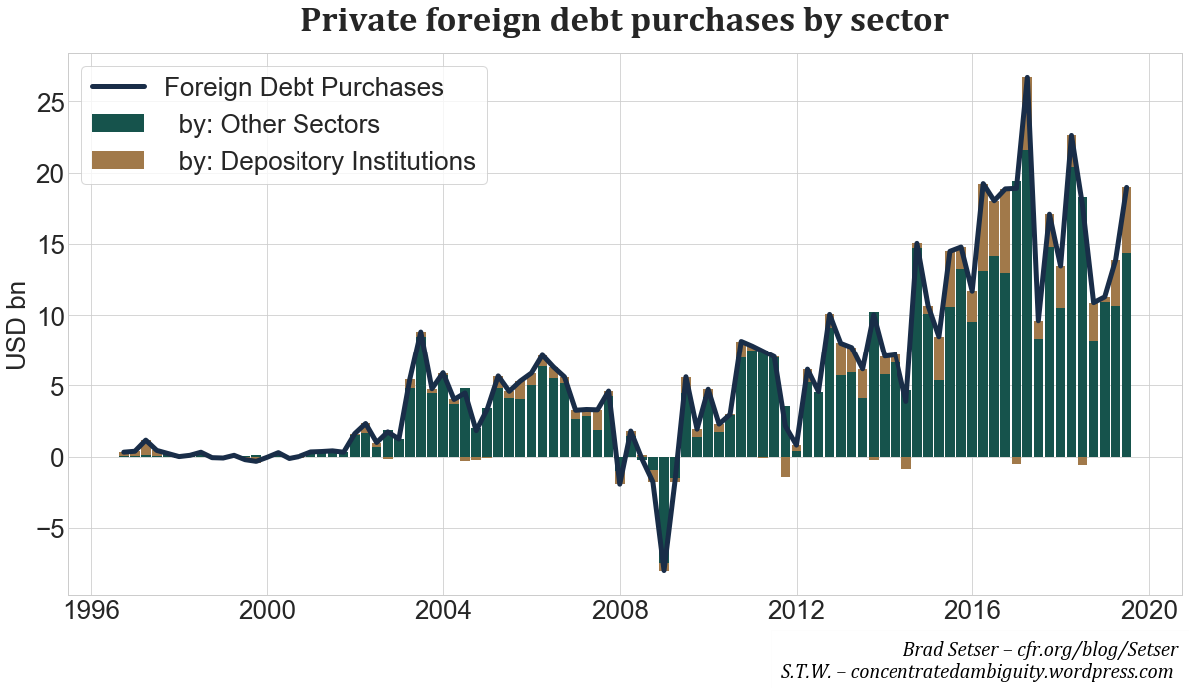

Digging deeper into the BoP statistics (Fig. 4) shows that while Depository Institutions (i.e. banks) do contribute to purchases of foreign bonds, the overwhelming share is purchased by the ’Other Sector’ category, which typically houses a country’s insurance sector, mutual funds & other financial institutions aside from banks. As evidenced in Fig. 5, in Taiwan’s case, the life insurance sector is the key purchaser of foreign fixed income assets[2] and thus also the linchpin of the Current Account recycling mechanism.

C. The Rise of the Life Insurers

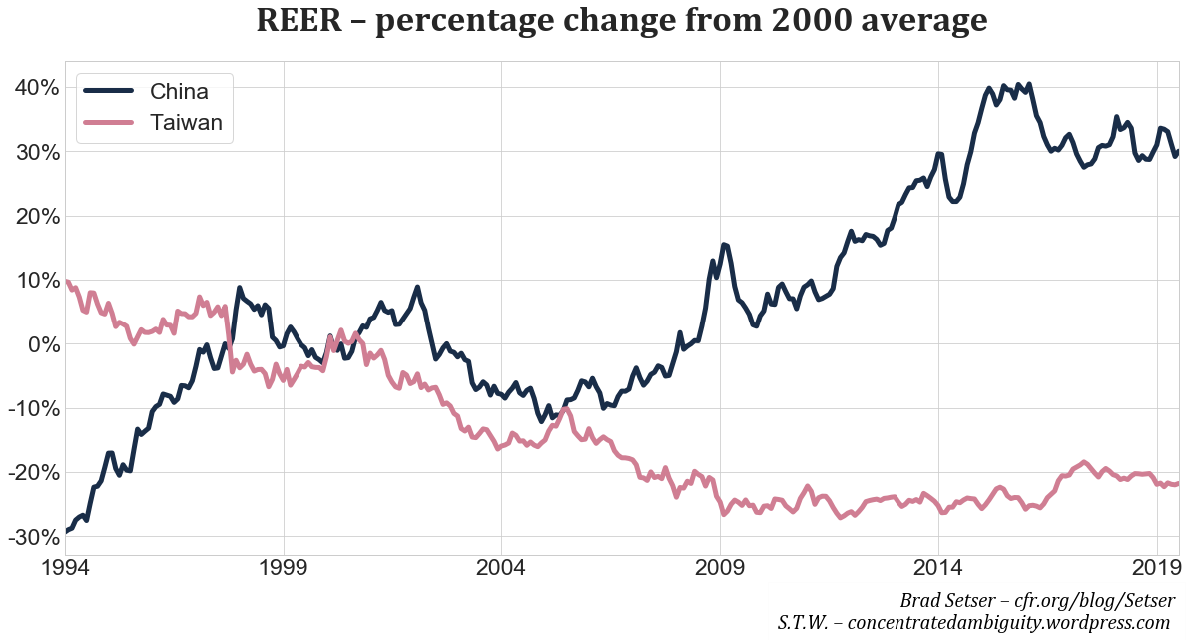

Taiwan’s economy’s high savings rate of 35% of GDP, reflects a relatively limited social safety net for workers in the private sector, comparatively conservative fiscal policies, as well as Taiwan’s aging population. High savings, paired with modest rates of domestic investment, naturally gives rise to the need to invest surplus savings abroad. Taiwan’s ability to sustain a large current account surplus has been aided by relatively low domestic interest rates, as well as regular interventions by the central bank in spot FX markets. Whereas CNY has appreciated substantially since 2009, TWD has not. In fact, in real effective terms, Taiwan’s exchange rate has depreciated by about 20 percent over the last twenty years. Other Asian countries also tend to have excess savings, but the size of its surplus makes Taiwan an outlier even in its region.[7]

Taiwan is not included in the IMF’s annual External Sector Report. Two private sector evaluations—by William R. Cline[4] of PIIE and by Robin Brooks of the Institute of International Finance[5]—of TWD’s valuation with similar modeling setups as the IMF, put its current undervaluation against USD at approximately 20%, with even higher historical values[6].

Countries subscribing to a mercantilist growth model—i.e. sacrificing current consumption in order to generate trade surpluses—ultimately face the unenviable task of having to direct large funds into overseas markets.

Taiwan’s aging population, the ultimate benefactor of perennial trade surpluses, faces an imperfect climate allocating capital safely in domestic markets for eventual retirements. A domestic government bond market exists, its size at USD 190bn (combined with a lack of new net issuance due to a comparatively hawkish fiscal stance) is however far too small to allow the deployment of larger capital bases at reasonable rates of return. The domestic corporate bond market is even smaller at USD 60bn and equally characterized by only subdued growth. The USD 300bn capitalization of the domestic stock market is notable, but the lack of diversification across sectors and its high beta to global growth relegates it however in attractiveness for safety-oriented savers. Lastly, real estate is priced very competitively at an average price to income ratio of 9.

All factors combined leave overseas markets as the only viable alternative to absorb large quantities of funds. Since households are far from optimally equipped to manage large foreign fixed income portfolios, they transfer this task to the life insurance industry, which then takes on the challenge to allocate money overseas—and is tempted, no doubt, by the opportunity apparently created when international interest rates exceed local ones, conjuring the illusion of easily arbitragable profits[7].

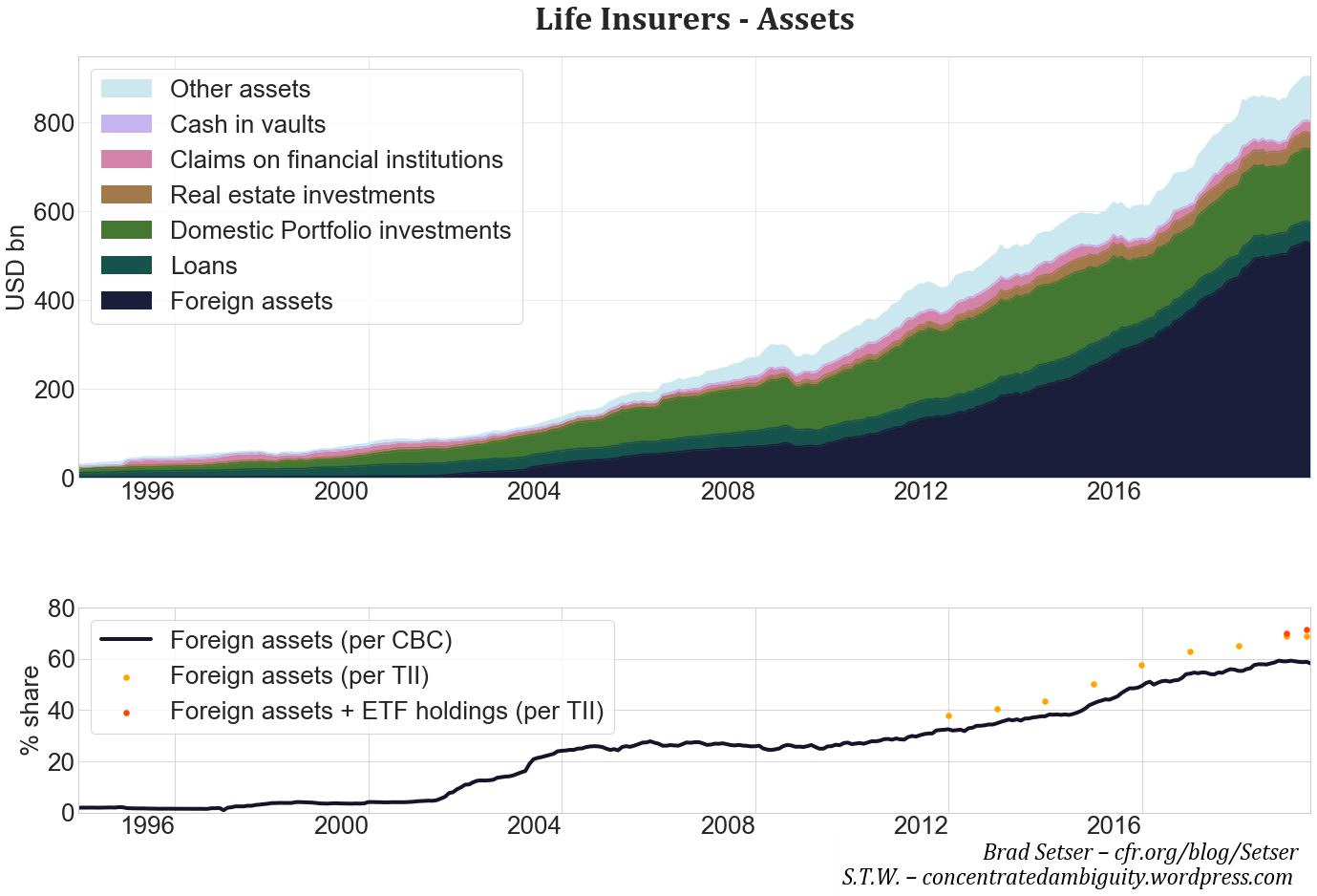

The CBC provides an elementary dataset on the balance sheet of Taiwan’s life insurers, which helps to emphasize the growth the industry has experienced this cycle. Assets have more than quadrupled since 2009, crossing the USD 900bn mark in the spring of 2019. The accumulation of foreign debt accounts for over 75% of the overall asset increase, with holdings of domestic portfolio investments basically unchanged. As a result, the foreign asset share has increased from the low 20s up to 60% today. A similar dataset, assembled by the Taiwan Insurance Institute, puts the this share even higher, at ∼70%.

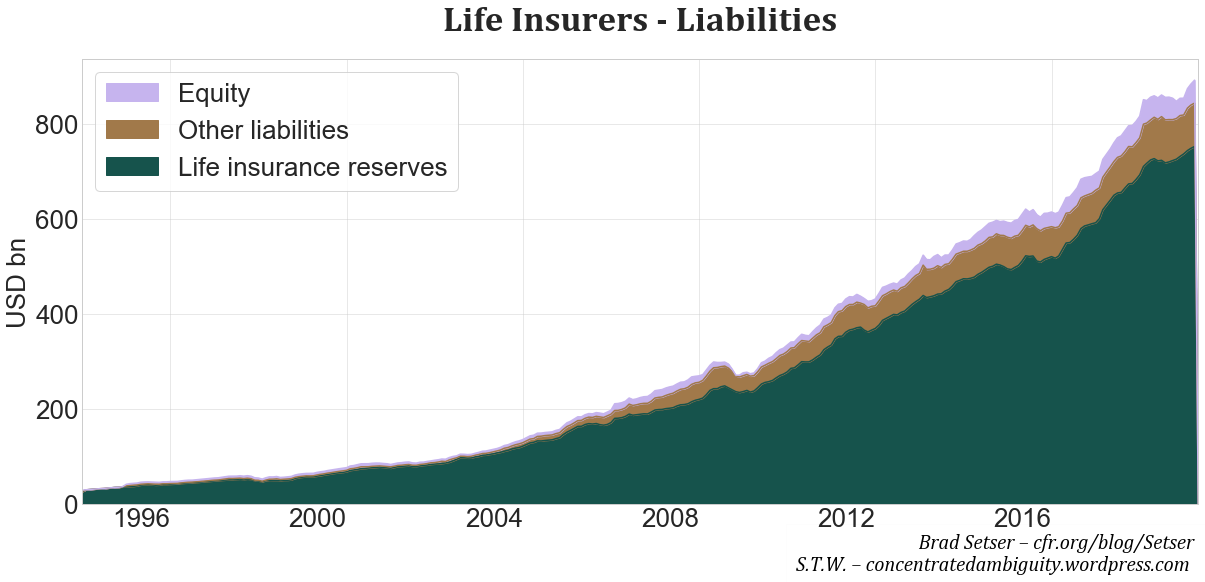

The liability side of the balance sheet is less exciting: Insurance reserves expectedly explain the greatest share; equity accounts for around 5% of assets in recent years, resulting in a leverage ratio of ∼20.

In order to later dissect the entirety of the CBC’s actions, it is unfortunately necessary to dive deeper into insurers’ management of their overseas debt holdings, the associated regulations and ultimately their approach to FX risk-taking. To this end, the following three sources will be merged to create the broadest possible understanding:

- the already utilized CBC dataset,

- information provided by the Taiwan Insurance Institute,

- financial statements, investor documents and conference calls of the insurers. The majority of Taiwan’s insurers are owned by larger financial holding companies, of which a hand full are publicly traded, releasing the above information. These account for between 60 and 70% of total industry assets. Triangulation, aided by anecdotal help for the privately held institutions, makes it possible to form a good perspective of how the entire industry is behaving.

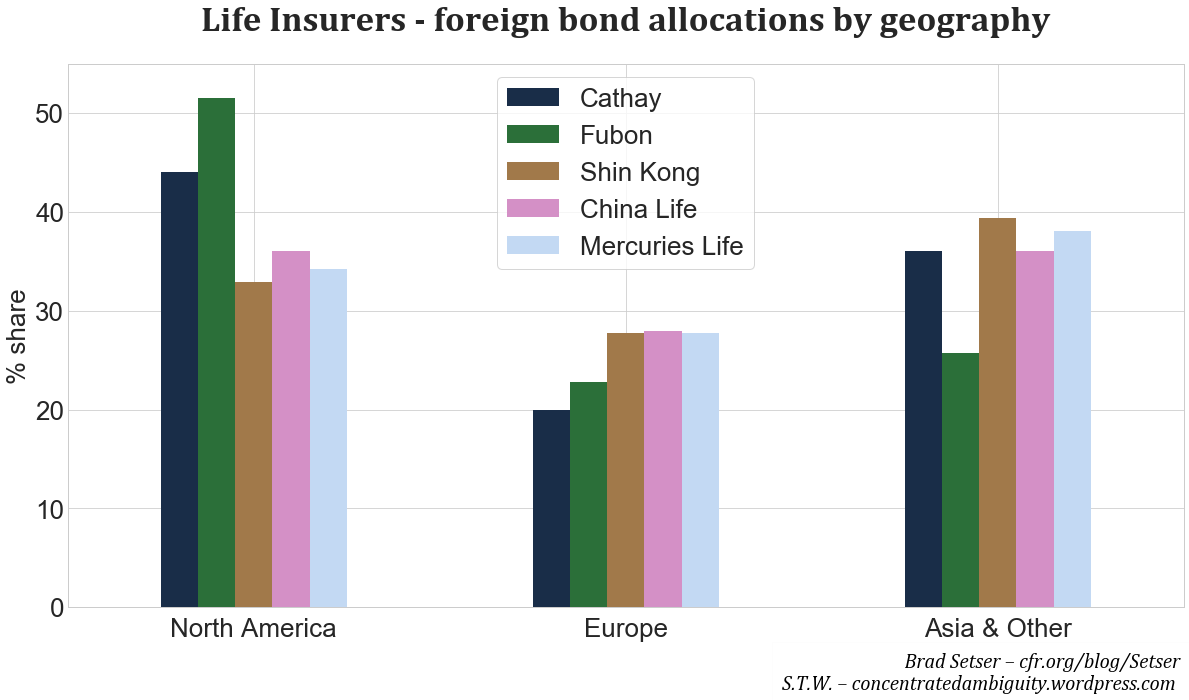

One fact that becomes clear relatively quickly is the high degree of similarity in the insurers’ business models. North American issuers continue to be the largest target of lifers’ overseas bond buying, followed closely by allocations to the burgeoning Asian dollar bond market. Europe’s average share has decreased over the years, to 25% today.

The geographic dispersion of the insurers’ bond portfolios though is a misleading picture of the insurers’ currency risk assumed: US dollar denominated bonds account on average for 95% of the insurers’ foreign bond portfolios[8]. Like life insurers elsewhere, Taiwan’s firms acquire bonds of long duration, trying to match the long-dated nature of policy claims; the average duration of the overseas bond section exceeds 10 years for all reporting companies. In the international context, Taiwan’s lifers show a clear preference for non-sovereign debt, with corporate exposures of up to 80% not unusual, as well as large exposures to Agency debt securities.

Overseas investments by Taiwan’s insurers requires prior regulatory approval[9], which has strongly influenced the shape of preferred vehicles selected to access foreign debt over time. While the exact foreign investment quotas are set discretionarily based on company specific details, 45% of assets has for a long time been the acknowledged limit set by Taiwan’s Financial Supervisory Commission (FSC). With most insurers converging to this limit during 2016, loopholes (more or less deliberately) left open by regulators have been employed ever since to further increase the foreign debt share.

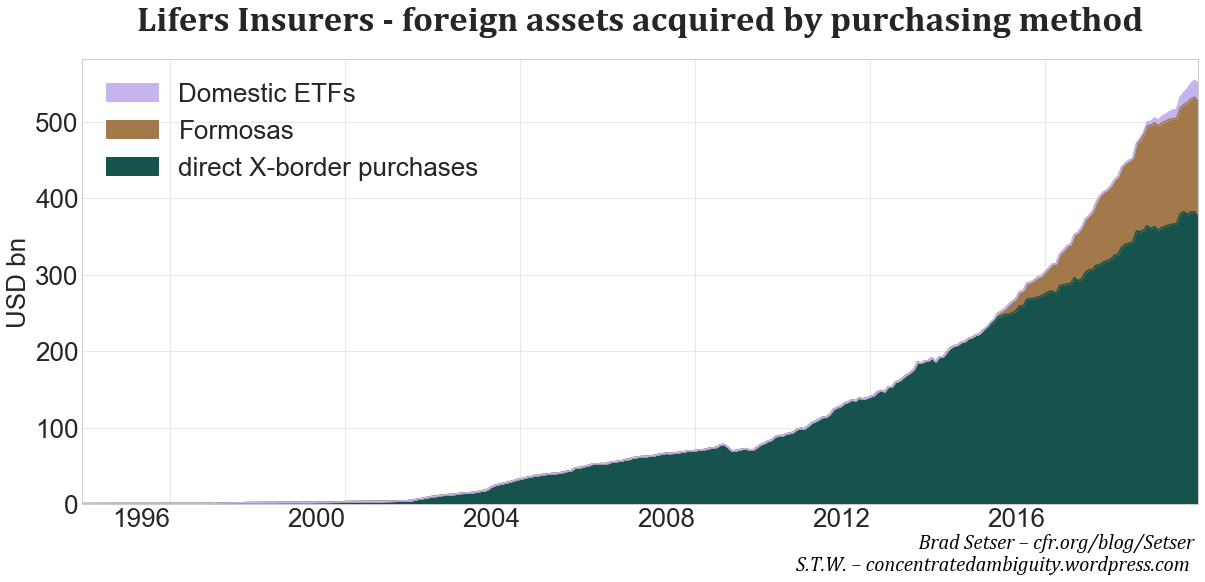

Formosa bonds, i.e. bonds denominated in foreign currencies issued by international firms, but listed on the Taipei Exchange, marked the first opportunity to further increase overseas allocations. Such securities are classified as domestic products by the FSC, regardless of their otherwise very different appearance. As a result, many of the prime IG issuers from the US and Europe flocked to Taiwan during 2016-2018 to accommodate lifers’ thirst for long-dated and high-yielding assets. Such issues (typically featured a relatively short call period) were the main channel for insurers to access foreign bonds during this period, the size of the USD-denominated Formosa market grew from zero to about USD 150bn (of which lifers hold more than 90%), before new regulations[10] were introduced during 2018. These, among other things, imposed an indirect cap on Formosa holdings by limiting the combined share of a) ’genuine’ foreign bond holdings plus b) Formosa holdings to 145% of an insurer’s overseas investment quota. This results in a new overall cap of 65% for foreign assets.

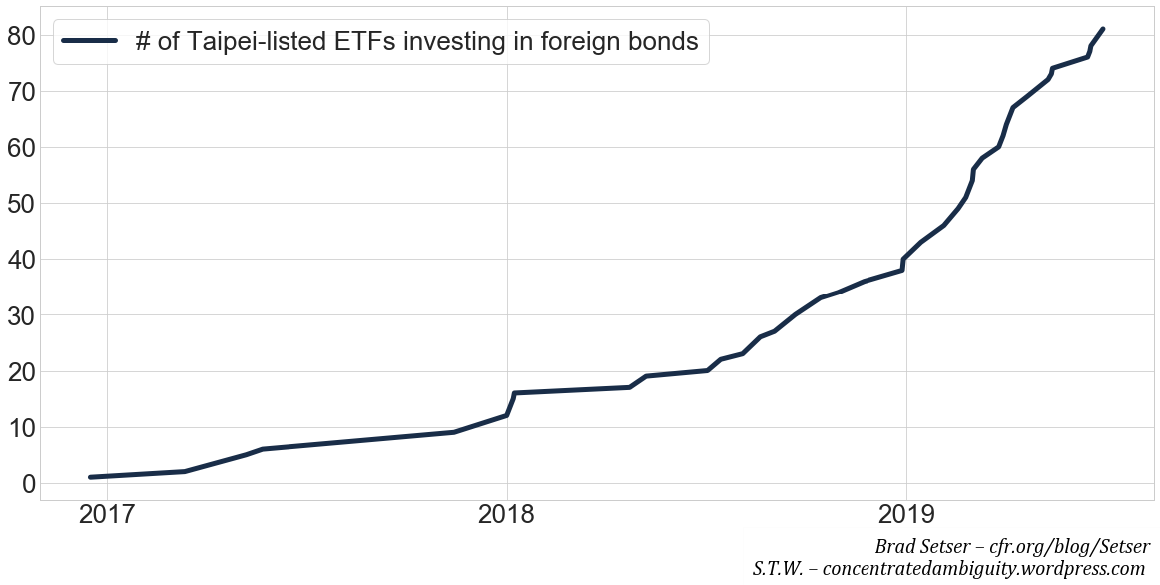

During 2018, with the regulatory changes in the air, a better vehicle had to be developed...and was found in the form of locally listed, TWD-denominated bond ETFs, which then in turn acquire foreign debt securities. In contrast to Formosa bonds, these are not only listed in Taiwan, but also are denominated in the home currency. Of course, since the assets underlying the ETFs are foreign currency-denominated and FX risk is not hedged by ETFs directly, currency movements are simply transmitted to the TWD-listed price. This leaves insurers with the same FX exposure as when overseas bonds are purchased directly. Everyone in Taiwan is aware of the trick and for the time being its tolerated by regulators. ETFs have been the primary vehicle for insurers to acquire overseas debt since mid-2018, the value of purchased foreign bond ETFs currently stands at USD 25bn and led to a boom in new listings of such products, the number of which now approaches 80. Squaring the circle, many life insurers acquire ETFs not from an outside issuer, but from the ETF desk in the equity division of the bank subsidiary part of the same holding company as the insurer itself.

Lastly, the immensely important subject of FX risk management involved in managing foreign bond portfolios has to be addressed. Regular life insurance policies, which in Taiwan constitute the preferred saving vehicle of households, are overwhelmingly denominated in the policy holder’s home currency, so that at the conclusion of the contract, funds can be used by policy holders to acquire goods and services in the domestic economy. Life insurers with substantial holdings of USD-denominated debt have to carefully manage FX mismatches and have three tools at their disposal to do so:

- FX policies: Insurers can offer foreign currency denominated policies, which either partially or fully transfer the FX risk to policy holders. This is usually a cheap way of reducing FX imbalances, but is constrained by the buyer’s willingness to assume the FX risk instead. The TWDs relative stability vs. USD certainly helps selling this case to prospective clients.

- FX hedges: Insurers can hedge the FX risk by acquiring TWD in the FX forward or futures market. Alternatively, they can enter into FX swap or Cross-Currency Swap contracts, which correspond to collateralized borrowings. In either case, the FX risk is laid off to the market, but the pricing of the hedges (manifesting itself as a negative X-CCY basis[11]) depends on market conditions and is costlier than FX policies.

- Open FX position[12]: Insurers can also keep the FX risk on their own balance sheets. This option is constrained by the insurers’ high leverage, limiting the ability to absorb large FX swings, high risk-based capital charges for open FX exposures and the regulatory mandated requirement to build up a precautionary FX reserve account.

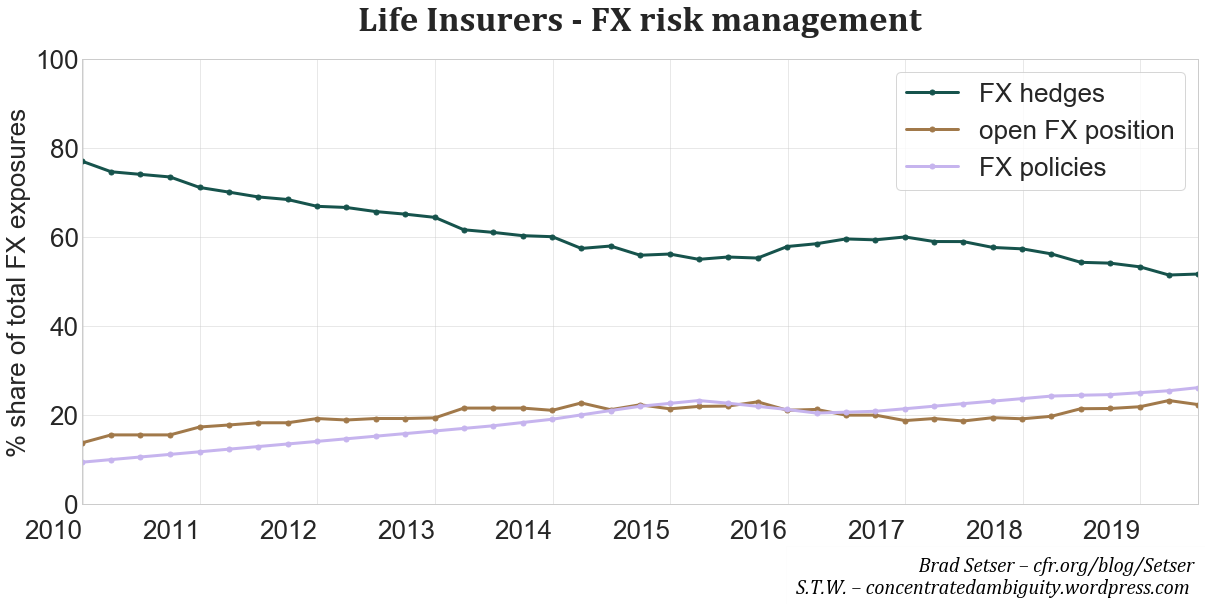

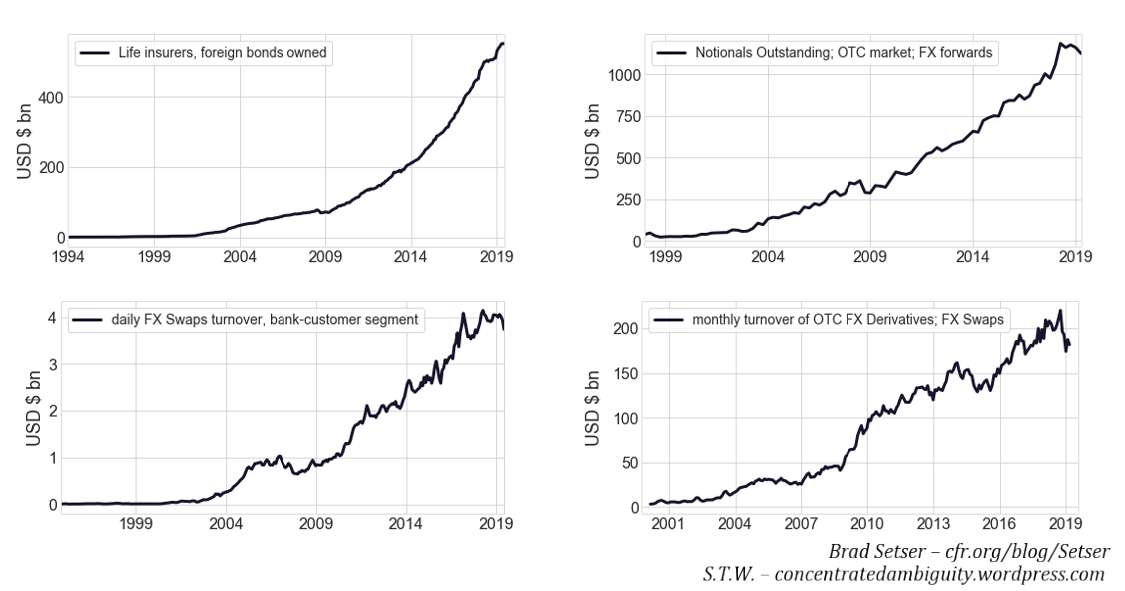

Insurers, as shown in Fig. 12, rely on all tools in managing their FX risk, the relative importance changing however over time. The share of classic FX hedges has declined from 80 to 60%, yet with the stupendous rise in the value of foreign bond holdings, the demand for FX hedges nevertheless increased steeply. This is clearly visible in various metrics of the onshore FX derivative market illustrated in Fig. 13.

FX risk taking by insurers themselves, as well as their clients via FX policies, have both increased relative to the start of the decade. The growth in sales of FX policies was steady, currently releasing insurers of 25% of their overall FX risk taken; insurers own relative FX positions were more volatile and pro-cyclical, growing larger during the USD appreciation until 2016, followed by a swift reversal as a result of FX losses due to TWD strength. Since 2018, with acquisitions of FX-unhedged foreign bond ETFs, insurers open FX position has started rising again, today matching the 2015 heights at about 23%.

D. Sizing the Lifers FX Hedges: Two Sources

Since lifers’ FX hedges will play a crucial role in this story, it is worth openly discussing the difficulties in pinning down their exact size.

One way to attain an estimate of the size of the life insurance sector’s FX hedges is by applying the percent share in Fig. 12 to the CBC released series of insurers’ foreign assets. While the calculation per se is sound, there exists some uncertainty created by the limited numbers of insurers reporting during the early years of this decade, as well as the privately held nature of some. Extrapolations based on the limited sample may not exactly represent the FX management across all insurers. On the positive side, insurers’ disclosures include all FX-hedges, independent of whether they were executed domestically or offshore via non-deliverable forwards (NDFs).

A second method to derive an estimate is to rely on a regular footnote in the aggregate life insurance statistics released by the CBC, stating the size of FX hedges established. Available at a monthly periodicity, this source includes all life insurers but has two disadvantages. Historical footnotes are not part of the CBC’s statistical database, so that quite some extrapolation is required to use the small number of historical values obtained. Furthermore, it is unclear whether hedges in offshore markets are taken into account by the CBC.

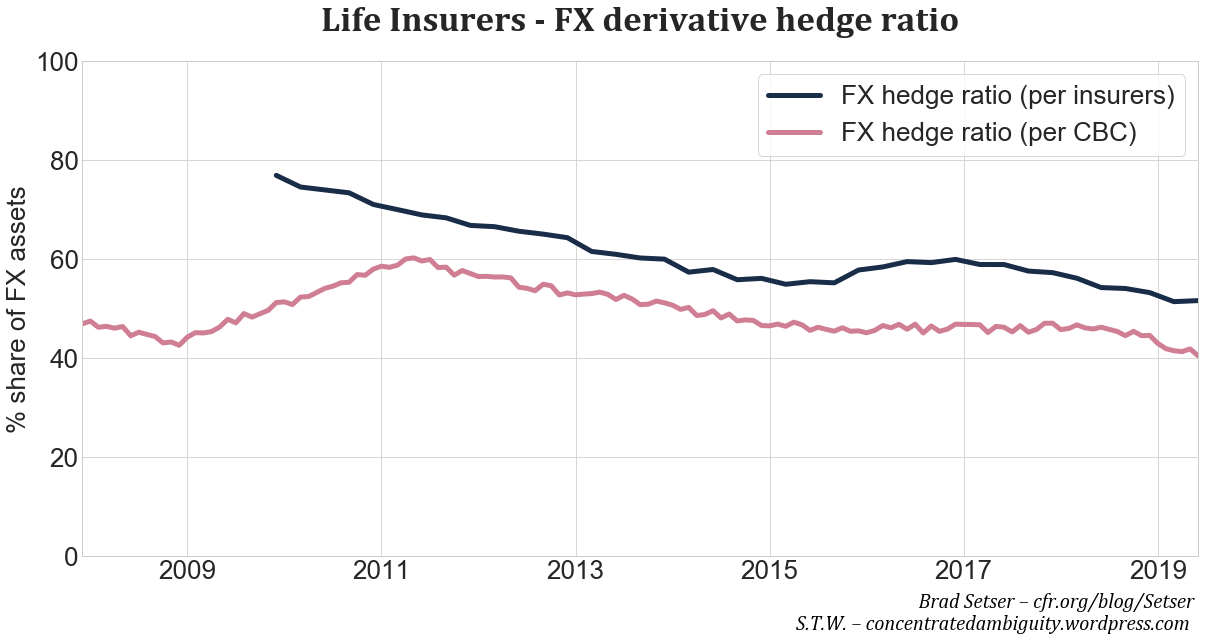

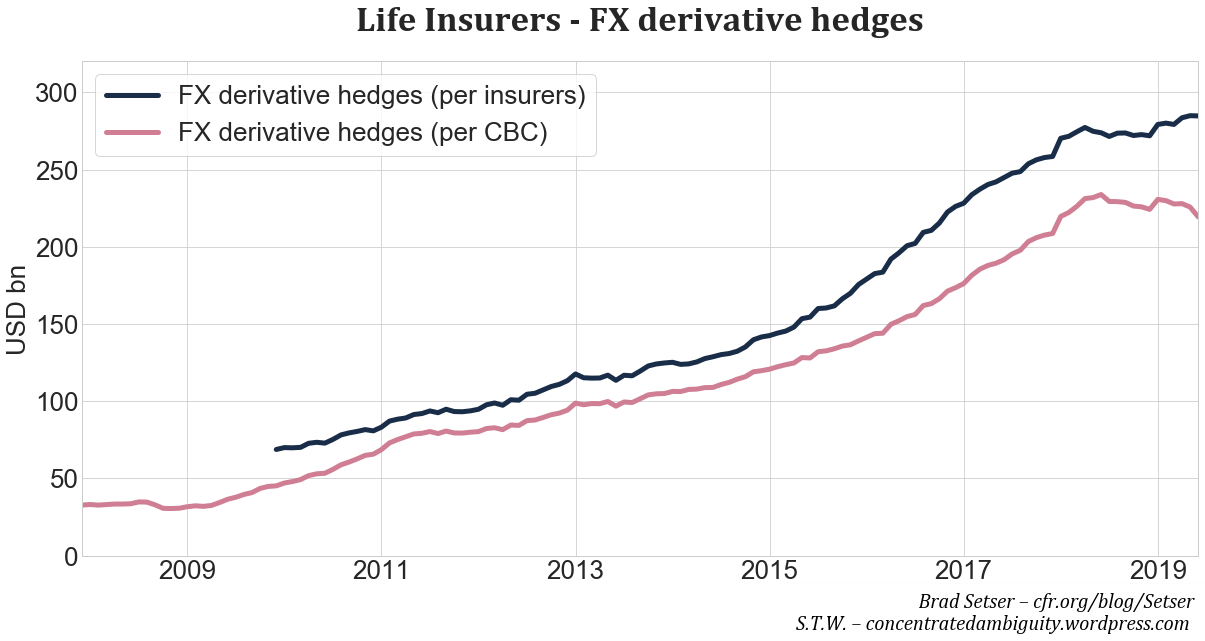

The results of both methods are presented in Fig. 14 & 15 and agree that the share of FX derivative hedges decreased between 2012 and 2016, stayed about flat into 2018, before declining further. The micro-constructed series continuously exceeds the CBC indication, likely due to the inclusion of hedges in the offshore market[13]. The early values in the CBC series appear surprisingly low and do not align with indications from the small number of insurers providing information back then.

Translated into nominal USD values, the two methods put lifers’ position in classical FX derivative hedges at USD 220bn and USD 285bn respectively, with values near USD 250bn seeming a good compromise.

E. The Missing FX Risk Taker

The significant amount of FX hedges established by the life insurance sector challenges simplistic views of Taiwan’s Current Account recycling mechanism. In the Bank of International Settlement’s words, it is necessary to “break[ing] free of the triple coincidence in international finance”[14], which in this case implies a more subtle differentiation between ’asset recycling’ and ’FX risk recycling’.

In terms of asset recycling, it was clearly first done through the CBC’s FX reserve accumulation, then, since 2010, largely by lifers’ overseas debt investments. The CBC also clearly took on the foreign exchange risk associated with its portfolio. But to the extent life insurers have hedged their portfolios, they have shifted the foreign exchange risk to another party.

Conclusive statistics on the currency composition of Taiwan’s trade is scarce[15], but ample anecdotal evidence and FX pass-through to export/import prices[16] makes it safe to state that the largest share of Taiwan’s Current Account transactions are denominated in currencies other than TWD, mostly in USD.

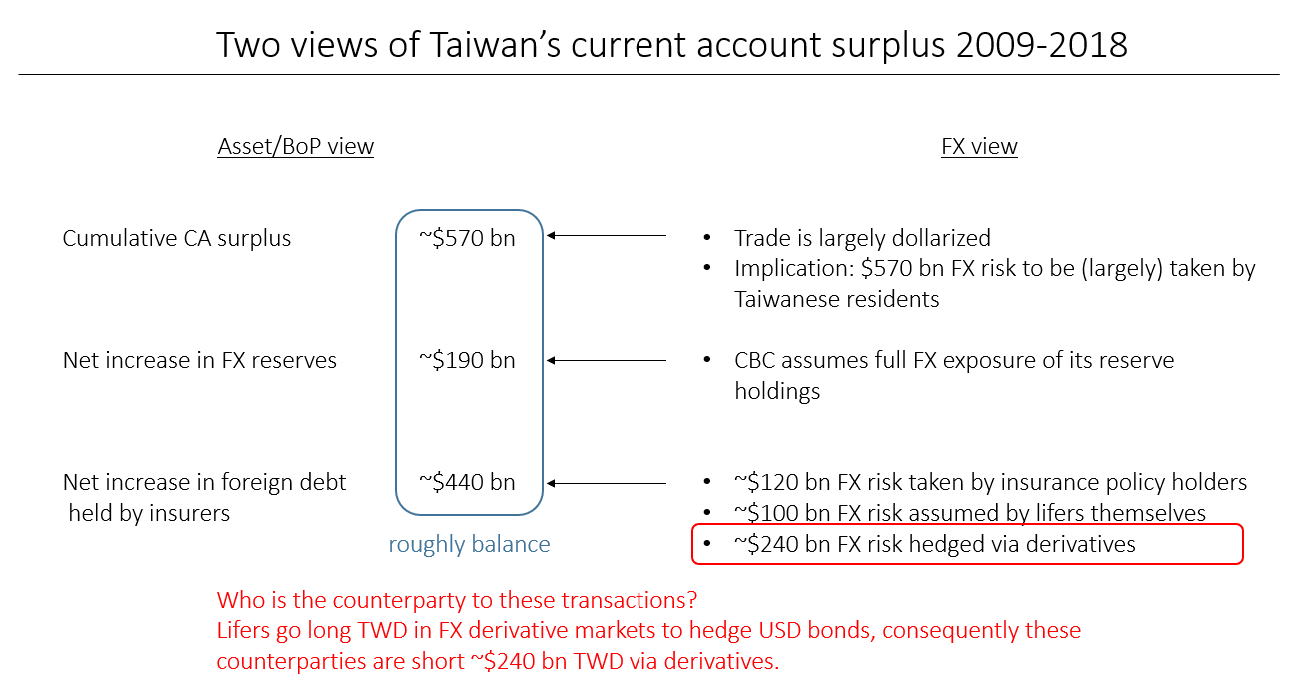

This in turn implies that Taiwan in its entirety assumes FX risk equal in size as surpluses on the Current Account, as Taiwan is receiving more dollars and other foreign currencies than it needs to pay for its imports. More specifically, from 2009-2018, Taiwan’s cumulative Current Account surplus amounts to USD 570bn. The CBC takes on 190bn of FX risk via the net increase in its reserves during the specified time frame. Of the USD 440bn increase in FX risk taken by life insurers as a byproduct of acquiring overseas assets, about USD 120bn and USD 100bn of FX risk was taken by policy holders via USD-denominated polices and lifers themselves as open FX position respectively. The remainder and by far largest portion of USD 240bn, insurers laid off via classical FX derivatives including FX forwards, FX swaps and Cross-Currency Swaps.

These hedging transactions raise two fundamental questions about the core workings of Taiwan’s FX market:

- Who provides lifers the FX hedges?

- If lifers do not take the largest portion of the FX risk resulting from Current Account surpluses, who is?

The opacity of over-the-counter (OTC) derivative markets impedes easy tracking of who ultimately assumes this large amount of FX risk and normally this is where the story would end. In this particular case however, the size of lifers’ hedges are so large (~40% of GDP), that with the right tools and a bit of legwork, a relatively clear picture can ultimately be constructed.

* The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.

** Contact at [email protected]

[1] Based on 2014 World Input Output tables available here.

[2] The slight difference in the two time series is largely due to a) FX accounting effects, as the lifer series is based on current FX rates, whereas the cumulative flow numbers are accounted for at exchange rates present in each quarter; b) accounting differences regarding the issuance of Formosa bonds.

[3] See for instance Setser, B, 2016, ‘The Return of the East Asian Savings Glut’, CFR discussion paper.

[4] Mr. Cline produced regular Estimates of Fundamental Equilibrium Exchange Rates for the Peterson Institute for International Economics until November 2017. Updates are continued at his website Economics International Inc.

[5] Regular updates on the IIF’s FEER models can be found at iif.com.

[6] In Mr. Cline’s public November 2017 version, TWD was undevalued by 33% against USD.

[7] See the post ’FX-hedged yields, misunderstood term premia and $ 1tn of negative carry investments’ for an in-depth discussion regarding the risk of relying on overly simplistic analytical frameworks when comparing FX- hedged overseas debt with local alternatives. The primary concern is over- reliance on the starting yield curve rather than more accurate formulations of term premia embedded in the curve.

[8] This situates lifers among the primary foreign investors in Yankee/Eurodollar issues by European companies, as well as the fast growing Asian Dollar debt market.

[9] See the current ’Insurance Act.’ here, especially Article 146-4.

[10] See the ’Regulations Governing Foreign Investments by Insurance Companies’ update last year here, especially Article 10.

[11] The cross-currency basis is the deviation in the pricing of FX markets for future delivery from theoretical values based on Covered Interest Rate Parity.

[12] Some insurers only report their open FX position together with proxy hedges. Anecdotally, the use of proxy hedging has decreased meaningfully compared to insurers’ incipient ventures abroad pre-2008. Unsurprisingly, if other FX crosses show meaningful volatility vs. USD, a proxy hedge is hardly effective and creates needless basis risk.

[13] Possibly also since the privately held insurers included in the CBC definition are generally considered more aggressive, thus running larger open FX positions.

[14] Avdjiev, S, R McCauley and H Shin (2016): ”Breaking free of the triple coincidence in international finance”, Economic Policy, vol 31, no 87, pp 409–51. Also available here.

[15] The CBC compiled statistics on ’Export and Import Foreign Exchange Proceeds and Payments’ might be the best data available and shows, as expected, the TWD share in export and imports in the tracked sample to be 6.5% and 19% respectively.

[16] In a simplistic two variable regression framework, explaining changes in Taiwan’s overall export price index by the USD/TWD exchange rate and the price of WTI crude, a 1% rise in USD causes a 0.6% rise in Taiwan’s export prices after two months.