The US is exporting its recession (by not importing)

The trade deficit continued to shrink in February, even though oil prices stopped falling.

Chalk that up to a huge slide in non-oil imports.

Non-oil goods imports were down 25% y/y. Automobile imports are now down over 50% y/y. Imports from Japan were down close to 50% y/y -- a fall that matches the fall in Japan’s exports. Imports from both the eurozone and the pacific rim were down 30% y/y (not seasonally adjusted, and that may be a factor).

Non-oil exports were a bit higher in February than in January, a very positive surprise. It wasn’t the due to Boeing either. Civil aircraft exports were actually down a bit in February v January. Non-oil exports though are still down 18% y/y.

Alas, I tend to think the improvement in the February data will be hard to sustain, given the bleak global outlook and the lagged impact of the dollar’s rebound from its 2007/ early 2008 lows. I agree with Joshua Shapiro, who noted that the fundamentals still point to further falls in exports:

“Given what is happening in the rest of the world, it is highly unlikely that the February result represents the start of a turnaround in demand for U.S. goods abroad,” Joshua Shapiro, chief United States economist at MFR, wrote in a note.

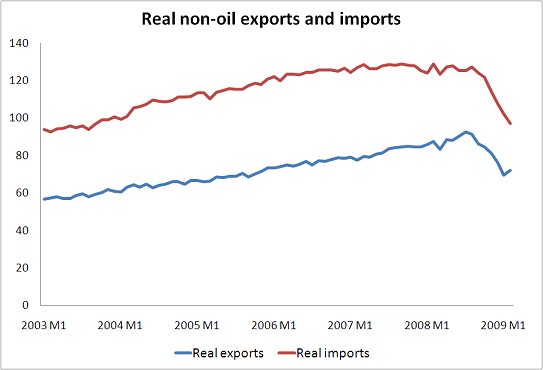

A plot showing real (non-oil) goods imports and exports clearly shows a small bounce in exports in February.

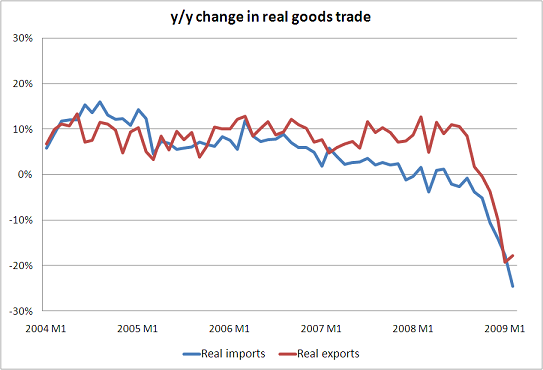

But the main story is that on a y/y basis, both real imports and exports are way down.

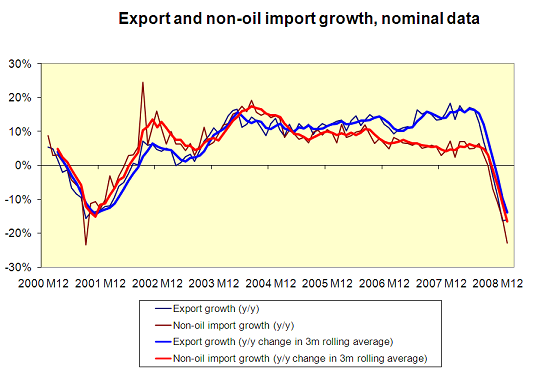

I have a longer time series more readily available showing the change in nominal exports (both goods and services). And the smoothed data (which looks at the y/y change in a three month moving average of non-oil exports and imports to limit the impact of month-to-month noise) shows a large, ongoing slide in both exports and imports.

I don’t see any green shoots in the data. Not yet. Exports and imports are both falling at a rapid pace. And -- as Calculated Risks’ charts make clear -- the fall in both exports and imports is far sharper during this recession than during the 2001 recession.

One last point: Average US oil imports in the first two months of the year were around $15 billion a month. That is down almost $20 billion from this time last year. And it is down over $30 billion from the peak of the summer. The fall in oil prices -- more than anything else -- explains the improvement in the trade balance. Moreover, US petrol import volumes are down 6% y/y, even with lower prices. That suggests that American behavior has changed. Or perhaps it just suggests that the fall in economic activity trumped any response to lower prices.