Make the Foreign Exchange Report Great Again

Overview

The U.S. Department of the Treasury should transform its foreign currency report so it can be used as a tool to combat currency manipulation. This would be an important step toward a more balanced global economy with fewer persistent deficits and surpluses.

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Countering currency intervention by foreign governments should be a top priority of U.S. international economic policy. By shifting the prices of imports and exports artificially, currency intervention undermines public faith that trade is fair. Together with other policy changes that raise demand abroad and help export-driven economies grow on their own, a policy of countering currency intervention could help create a global economy with fewer large trade surpluses and deficits.

Currency intervention by foreign governments usually comes when the U.S. economy is weak, since this is when countries that rely on selling to the United States worry about flagging exports. However, such intervention makes it hard for the United States to grow through exports during economic downturns. It also indirectly puts pressure on the U.S. government to support demand and employment by expanding the federal budget deficit, and to embrace regulatory policies that deliver short-term support for growth by ignoring the accumulation of private risk. In the longer term, intervention weakens the U.S. economy by changing the composition of U.S. employment. An artificially strong dollar shifts jobs out of the export sector toward domestic sectors. The U.S. export sector is now modest in size relative to U.S. imports and to the accumulated stock of U.S. external debt. A more balanced economy would be more resilient to future shocks.

A stronger policy against currency intervention does not require introducing binding provisions on currency into trade agreements. It only requires a credible threat of sanction if a country with a large trade surplus consistently intervenes in the market—and a process for naming and shaming those countries that intervene excessively. The U.S. Department of the Treasury’s semiannual foreign currency report should be transformed to become an integral part of the process for countering currency intervention. The needed reforms could be implemented without any new legislation and at minimal budget cost.

How Currency Intervention Affects the Trade Balance

The governments of many large exporting countries have often given their exports an edge by holding down the value of their currency. They do this by selling their own currencies and purchasing dollar bonds or other foreign assets. The result is large holdings of foreign assets in central banks or sovereign wealth funds (SWFs). A government that rapidly accumulates foreign assets while its economy runs a current account surplus is generally regarded as engaging in currency manipulation.

Currency intervention is currently only a marginal source of the trade deficit. Higher interest rates in the United States than in the other advanced economies have pulled in private funds from Europe and Japan, and private capital is leaving China. This naturally makes for a strong dollar: because the capital flows into the United States largely come from private sources, the U.S. government cannot be said to be manipulating currency.

But at times in the past two decades, currency intervention by central banks and the rising foreign assets of SWFs investing oil surpluses abroad have increased [PDF] the U.S. trade deficit by at least a percentage point of gross domestic product (GDP).

Arguments Against Fighting Currency Manipulation

One argument against a tougher approach toward currency manipulation is that it is impossible to articulate the difference between monetary policy choices that influence the exchange rate and active manipulation. However, monetary policy can be conducted without buying or selling foreign assets. Defining manipulation as intervention in the foreign currency market by countries with large external surpluses and sufficient reserves creates a clear standard that differentiates between countries with weak economies and naturally weak currencies, and countries that are intervening to artificially keep their currencies weak. Intervention for prudential purposes in emerging economies that have external deficits would be explicitly allowed.

Another argument against placing a higher priority on currency manipulation is that it would require confronting many of the United States’ friends and allies, not its geopolitical rivals. It thus could complicate existing alliances, move the focus of negotiations with these countries away from the conventional trade agenda, and potentially undermine any global coalition to push back against Chinese commercial practices.

A security alliance with the United States should not carry with it a free pass to intervene to maintain an undervalued currency.

The goal of a policy shift, though, is not to create conflict with U.S. allies but to manage it. Deterring bad behavior early, before currency manipulation leads to large trade imbalances, makes conflict less inevitable. A security alliance with the United States should not carry with it a free pass to intervene to maintain an undervalued currency. Most countries with large surpluses do not need to rely on exports as heavily as they have in the past, because they have unused capacity to introduce policies that would raise their domestic demand and support their own growth; South Korea, for example, runs an overly tight fiscal policy even as it often intervenes to hold the value of its currency down. Indeed, making it clear that a security alliance does not mean a free pass on currency would be a much less onerous form of burden sharing than proposals that U.S. allies pay the United States for the U.S. contribution to their defense.

Needed Changes to the Treasury’s Foreign Currency Report

A new policy that prioritizes countering excessive currency intervention abroad would require a different kind of foreign exchange report. The Treasury recently took a step in the right direction when it broadened the report’s coverage to all countries with more than $40 billion in bilateral trade. The report previously focused on twelve major trading partners. That was too narrow, as it left out many countries with substantial trade with the United States and large external surpluses, such as Thailand and Vietnam.

Three additional changes to the report are now needed.

Focus on Countries With Large Current Account Surpluses

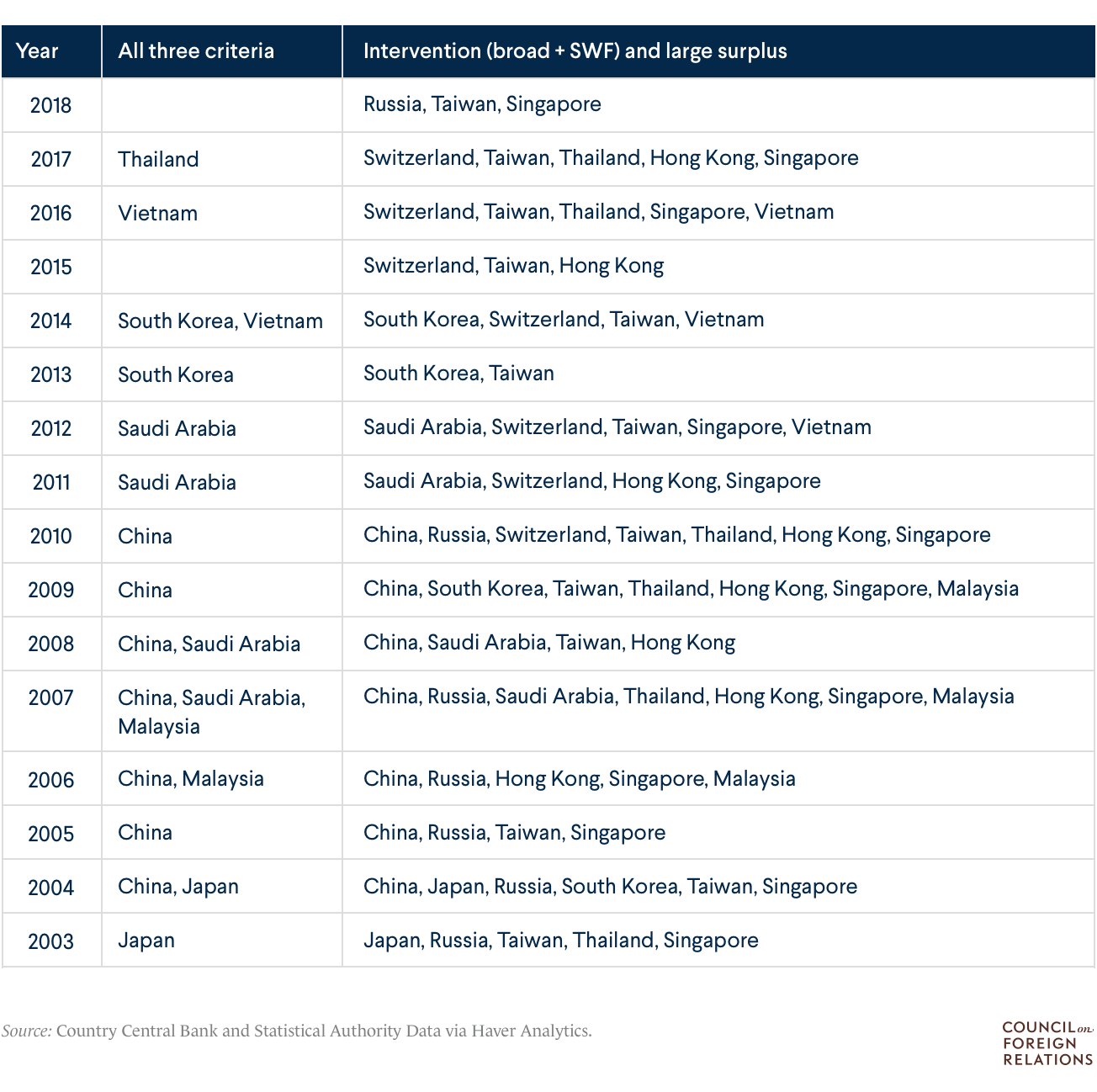

U.S. law requires that the Treasury assess major U.S. trading partners for currency manipulation against three criteria: the bilateral trade imbalance with the United States, the country’s overall current account surplus, and their intervention. Although using these criteria has strengthened the analytical basis of the report, the Treasury’s technical decision to treat the criteria as equally important has had unfortunate consequences. Partners, such as Taiwan, that export parts to China and thus do not directly run a large bilateral trade surplus with the United States—even though they have large overall current account surpluses with the world and a long history of intervention—have dropped off the Treasury’s watch list. Countries that happen to have a bilateral surplus with the United States even though they have an overall current account deficit, such as India, have unnecessarily appeared on the list.

The Treasury could strengthen the report by prioritizing countries with large current account surpluses and substantial overall trade with the United States. Countries without a current account surplus should not be on the watch list (unless there are significant concerns about the quality of measurement of their surplus). Conversely, significant countries with a large surplus should undergo careful scrutiny of the full range of their foreign exchange policies.

This reform would emphasize a country’s overall trade balance while de-emphasizing the balance of its direct trade with the United States. With the development of global supply chains, many countries that have substantial overall surpluses no longer have large direct surpluses with the United States: they export parts to other countries for assembly, and the U.S. trade data only tracks the location of final assembly.

China’s genuinely problematic trade and industrial policies should be addressed directly, not bleed over into the assessment of currency policies.

To be clear, this reform would result in less of a focus on China in the currency report. China has not met all three of the current criteria for manipulation since 2010 and is no longer consistently intervening in the foreign exchange market to hold its currency down (see table 1). The countries in Asia with the largest current account surpluses relative to the size of their economies—and the most persistent pattern of intervention in the market—are the smaller countries on China’s periphery: Singapore, South Korea, Taiwan, and Thailand. In dollar terms, each of these countries’ surpluses were—at least until 2018—smaller than China’s, and combined are around $300 billion. That is roughly the size of the troublesome surplus China ran before the global crisis. China’s genuinely problematic trade and industrial policies should be addressed directly by the Office of the U.S. Trade Representative, not bleed over into the assessment of currency policies in the Treasury’s foreign exchange report.

Table 1. Countries That Meet All Three Criteria Versus Countries That Meet the Intervention and Large Surplus Criteria

Make the Case for the Prosecution, Not for the Defense

The Treasury needs to adopt a more aggressive analytical approach—a new attitude—toward countries with large surpluses. When a country has a large surplus, the Treasury should be willing to look for evidence of intervention that would lead to conviction for manipulation, and not avoid naming the country over fears of complicating international diplomacy.

The standard mechanism for manipulation these days does not involve active intervention to push a country’s currency down. Rather, a country typically intervenes asymmetrically—letting the market push its currency down, and then resisting subsequent market pressure for appreciation. For example, the Korean won depreciated in 2008 as South Korea was hard hit by the financial crisis in the United States and the resulting fall in trade. Yet once Korea started to recover, it did not allow its currency to float up freely. Rather, it intervened on a significant scale to limit appreciation. Even though Korea’s intervention was significant, the Treasury did not make the case that Korea was guilty of manipulation, instead saying Korea was slowly allowing the won to appreciate. Although technically true, it was also an excessively benign interpretation of Korea’s actions.

Identifying manipulation, though, increasingly requires looking at more than a country’s formal intervention in the foreign exchange market. Some countries at risk of meeting the criteria for formal designation as currency manipulators under the current law mask their interventions, whether by encouraging state entities (such as state banks or state pension funds) to accumulate foreign assets or through regulatory actions that encourage private entities to take on more unhedged foreign exchange risk.

One example is Taiwan. Since 2010, Taiwan has encouraged its life insurance providers to invest a large share of their assets abroad; the insurers now hold around 69 percent of their total portfolios in foreign assets. Taiwan is not a member of the International Monetary Fund (IMF) and has not voluntarily chosen to follow the IMF’s standard for reserve disclosure. As a result, unlike other Asian central banks, the Central Bank of the Republic of China has not disclosed its forward purchases and sales of dollars. Despite this opacity, it seems reasonable to suspect that the central bank is helping to shield the life insurers from the currency risk they have assumed. For example, the authorities may be providing banks or insurers with dollars in exchange for the local currency, with a commitment to buying the dollars back in the future. This has the effect of moving dollars off the central bank’s formal balance sheet and disguising currency intervention.

Figuring out the techniques used to hide intervention requires technical expertise and market experience. This would require the Treasury to hire additional staff.

Figuring out the techniques used to hide intervention requires technical expertise and market experience. This would require the Treasury to hire additional staff, or staff with a different set of skills—for example, experience with financial forensics. It would also require taking a broader approach to disclosure than the Treasury has taken in the negotiation of recent trade agreements. The currency provisions in recent trade agreements have emphasized disclosure of direct intervention by the central bank, but they unfortunately have not required the disclosure of changes to other pools of foreign assets under state control.

Looking closely for evidence of hidden intervention in countries with large surpluses would thus represent a significant change of policy. Recent changes in the foreign exchange report have moved in the opposite direction. Some partners with a history of intervention in the market, like Taiwan, have already fallen off the Treasury’s monitoring list, and Korea is poised to drop off the list in the next report.

Develop Credible Sanctions

U.S. law provides little more than a slap on the wrist for most countries that are manipulating their currency. To gain traction in the market, a designation of manipulation needs to lead to the threat of a real sanction. But that sanction should not come through tariffs or other restrictions on trade.

Economists C. Fred Bergsten and Joseph E. Gangon have proposed [PDF] that the United States respond to other countries’ intervention with direct counter-intervention. The basic idea is that if a country intervenes excessively, the United States could respond by intervening on its own to offset the effect of that country’s actions on the market.

This is an intriguing way to break the logjam that has blocked meaningful sanctions against manipulation. It has proven hard to include such sanctions in trade agreements because such deals are supposed to be about reducing tariffs and other legal barriers to trade, not about currency policies. Other countries are reluctant to give the United States the ability to respond to currency intervention through a legal right to reimpose tariffs in a trade agreement, and the U.S. Treasury is reluctant to shift financial diplomacy to the trade lawyers who staff the Office of the U.S. Trade Representative and the Department of Commerce. As an alternative to trade sanctions, the United States should deter currency intervention with intervention of its own—though for global stability, counter-intervention should be reserved for extreme cases that cannot be addressed through dialogue.

Relying on counter-intervention as the ultimate deterrent to excessive intervention could also be simpler than using sanctions as a deterrent.

Relying on counter-intervention as the ultimate deterrent to excessive intervention could also be simpler than using sanctions as a deterrent. Trying to fit such sanctions into the statute governing the introduction of countervailing duties to offset the injury posed by sectoral subsidies would cause technical and legal difficulties.

Conclusion

Foreign exchange intervention abroad has at times accounted for as much as half of the U.S. trade deficit. Right now, the dollar is naturally strong, as U.S. interest rates are higher than the interest rates of most U.S. trading partners. But there is no guarantee that this will continue to be the case. At times, the dollar’s strength has been artificial and largely the function of other countries’ efforts to keep their currencies weak. The Treasury’s foreign currency report should be a careful, but hard-hitting, examination of all countries with large trade surpluses to make sure they are not intervening to hold their currencies down and, in the process, prop up their exports. A new willingness to look more closely for evidence of intervention should be combined with a willingness to use the Treasury’s existing legal authority to create meaningful penalties for persistent manipulation—particularly for those countries that do not change their policies even after a warning.

Transforming the foreign currency report so it can achieve its full potential as a tool to combat currency manipulation would not be a heavy lift and would have a significant payoff. Small countries that have intervened excessively in the recent past would face immediate pressure to change their policies, and large countries like China that once intervened heavily would be put on notice. Such a transformation would be an important first step toward a more balanced global economy with fewer persistent deficits and surpluses.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report