U.S. Equities and Korea’s Balance of Payments

Korea’s record current account surplus was offset by large equity outflows. This marks a new era for U.S. balance of payments.

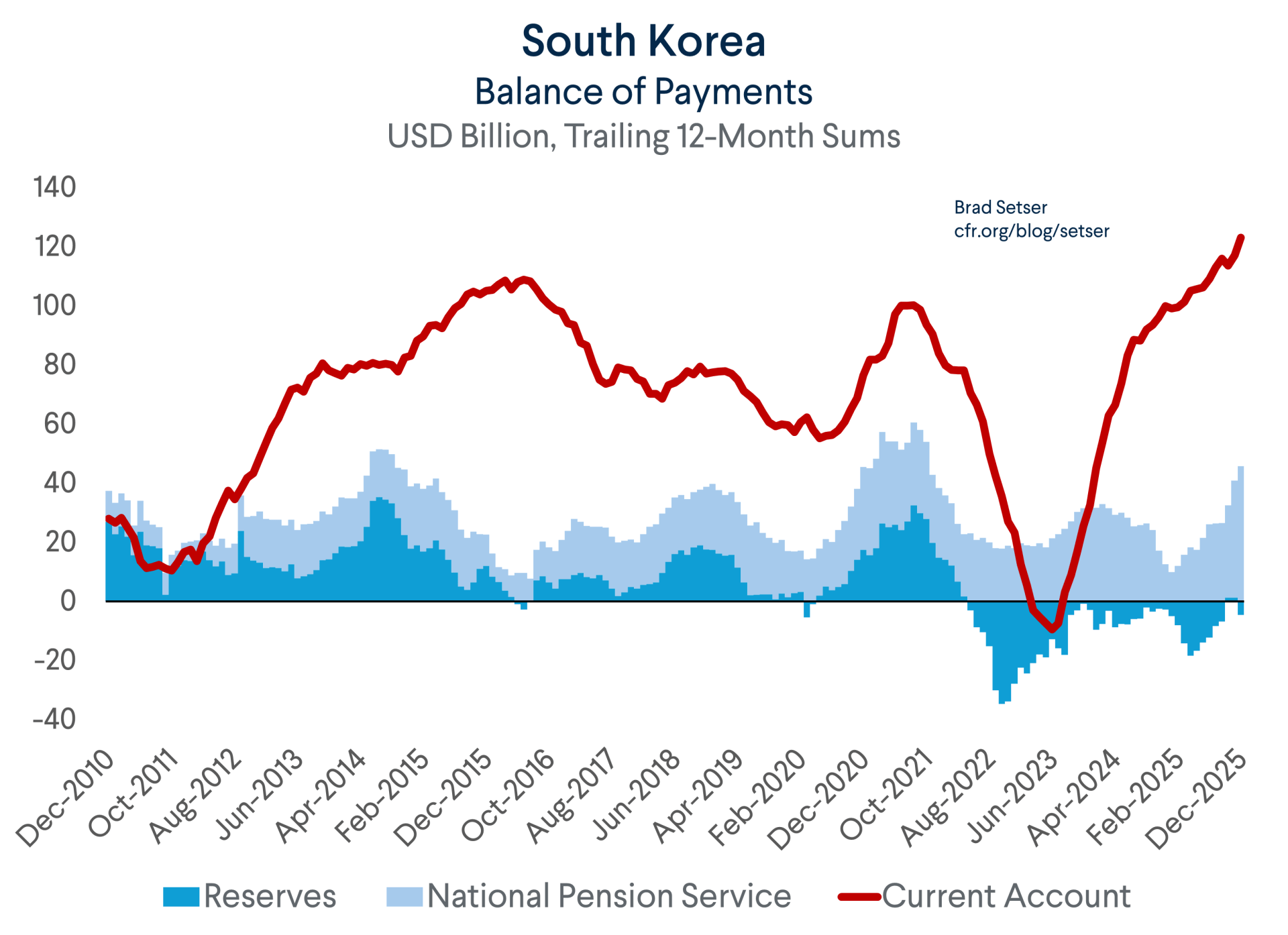

Korea posted a record current account surplus in 2025: $120 billion.

The Korean won also flirted with record lows (1500) against the dollar, and would be very weak in real terms but for the extreme weakness of the yen and the sustained weakness of the Taiwan dollar (manufactured weakness, to be sure).

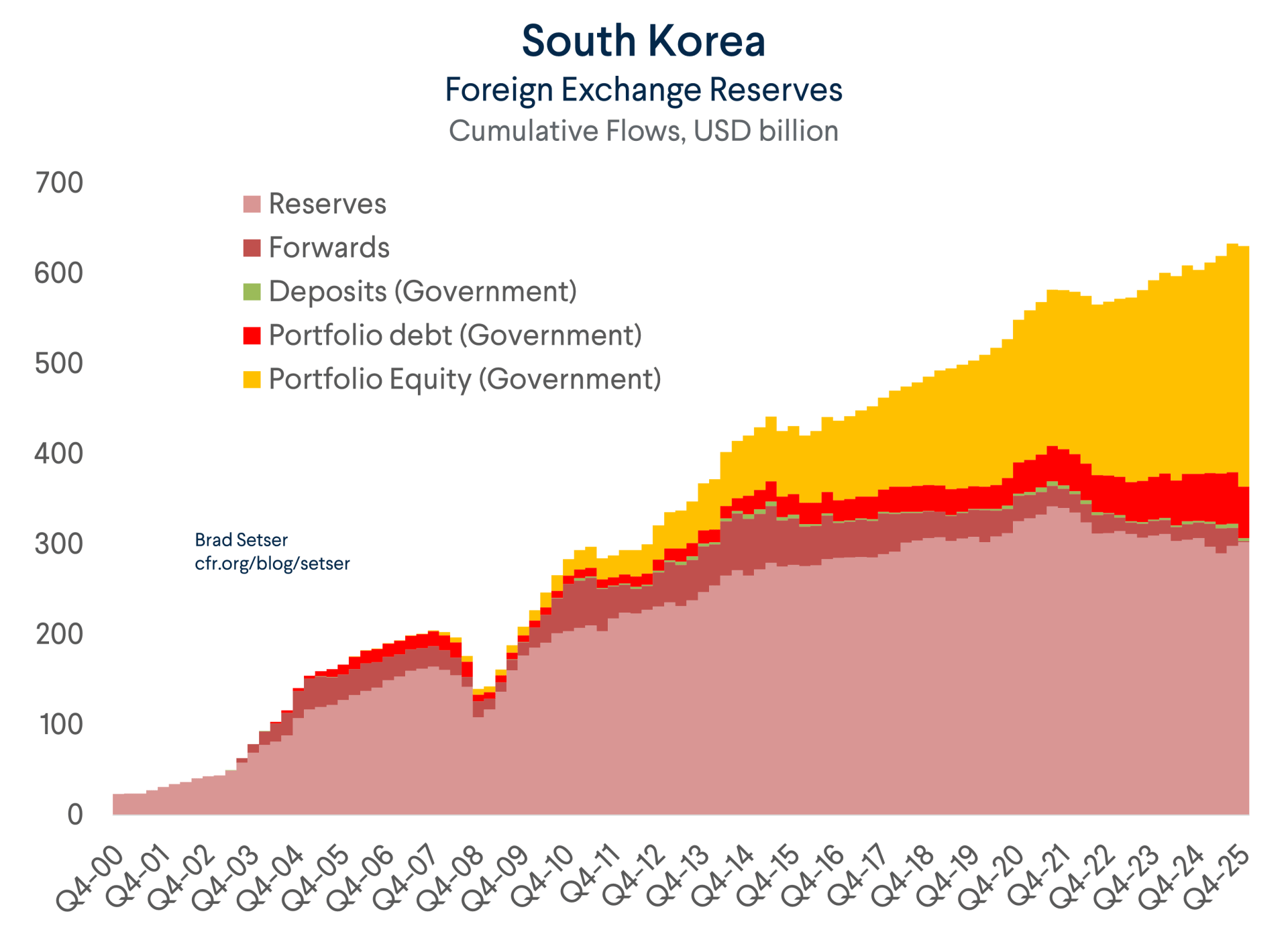

Unsurprisingly, given the weakness in the won, the Bank of Korea didn’t need to recycle Korea’s external surplus—a marked change from ten years ago. In fact, the Bank of Korea sold a bit of foreign exchange over the course of 2025 in an effort to support the won.

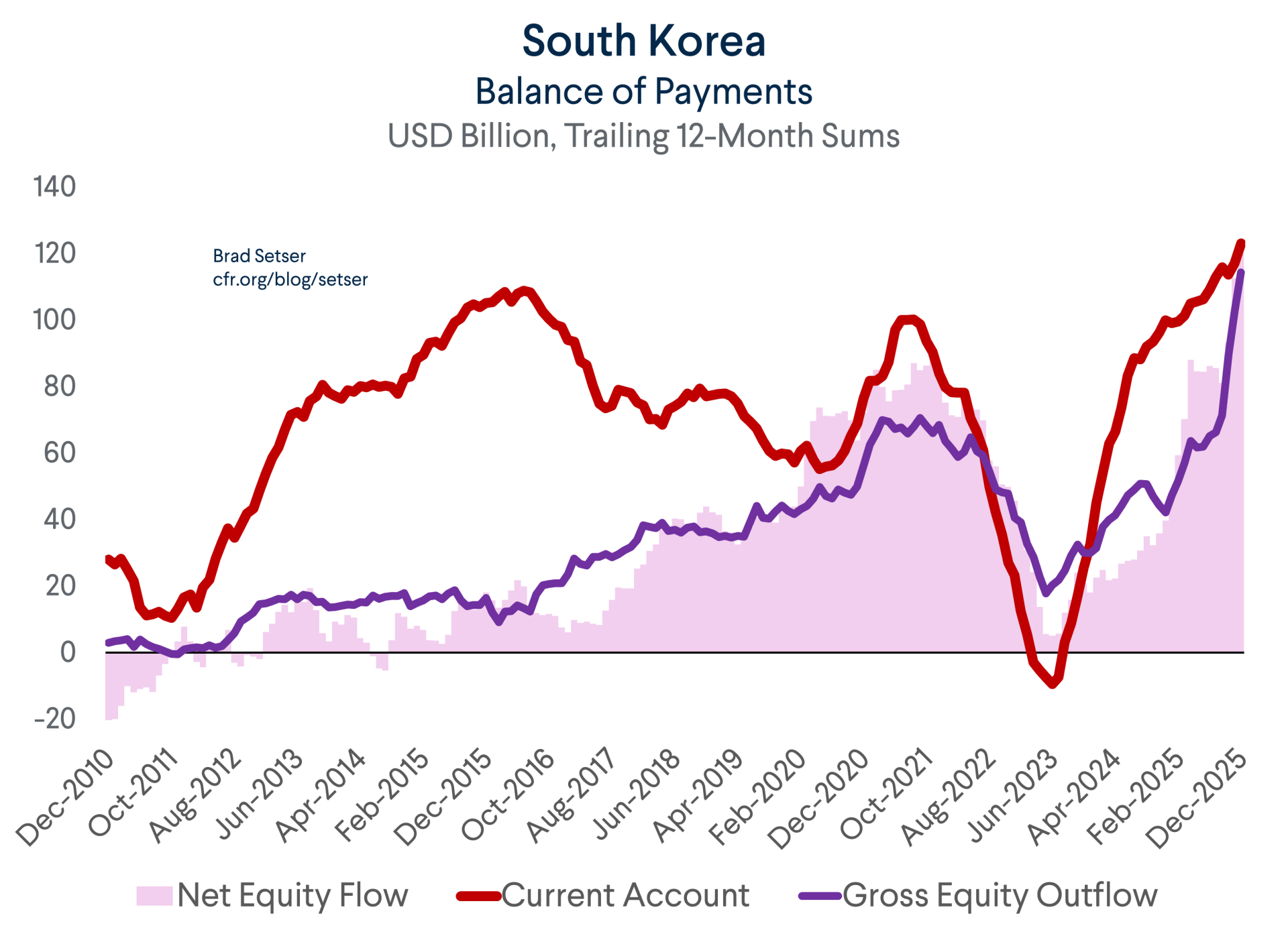

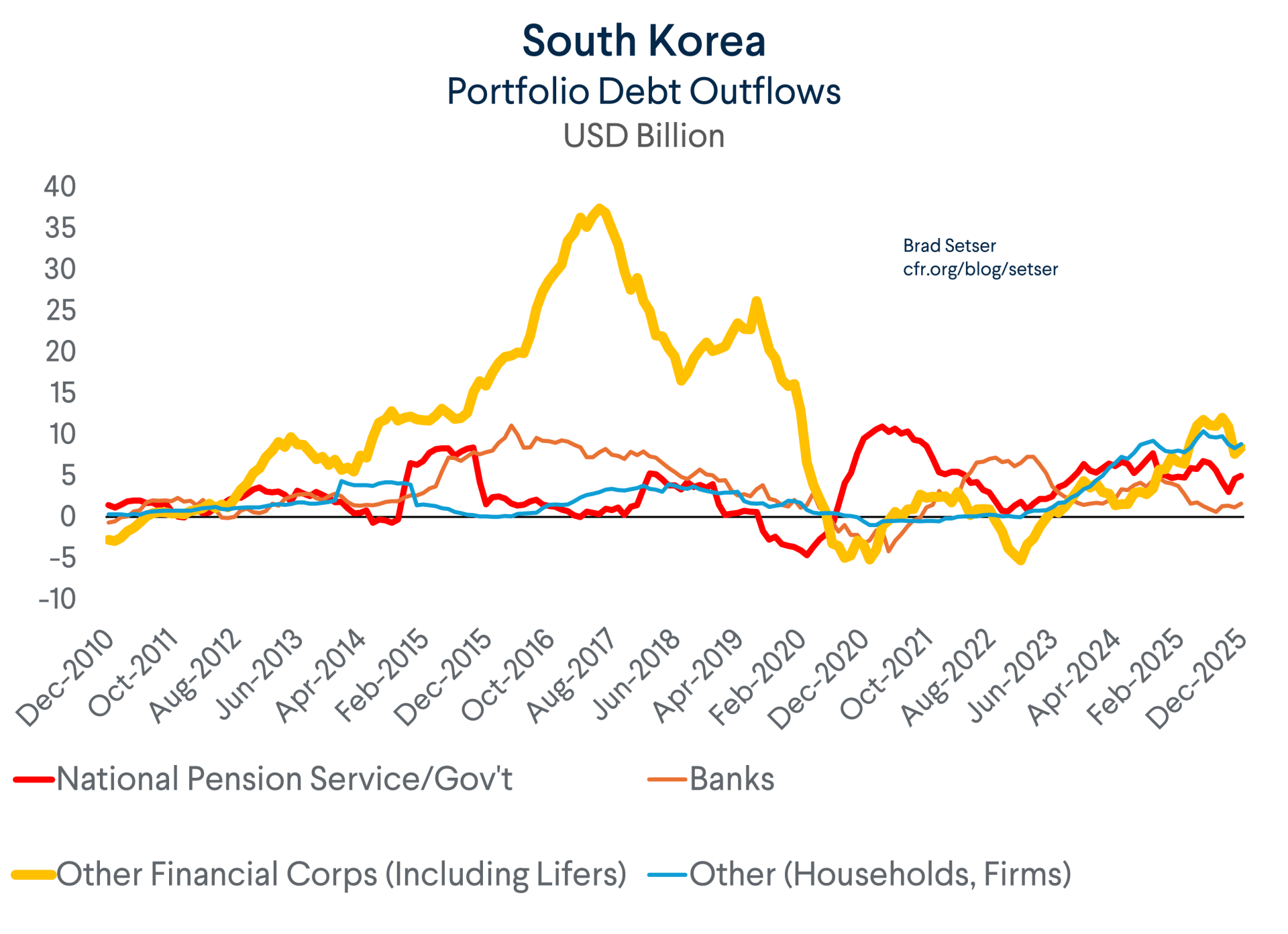

Korea’s surplus was also interesting for another reason: the entire outflow that offset the surplus came from Korean purchases of foreign equities (and a bit of foreign selling of Korean equities). There was no substantial debt outflow.

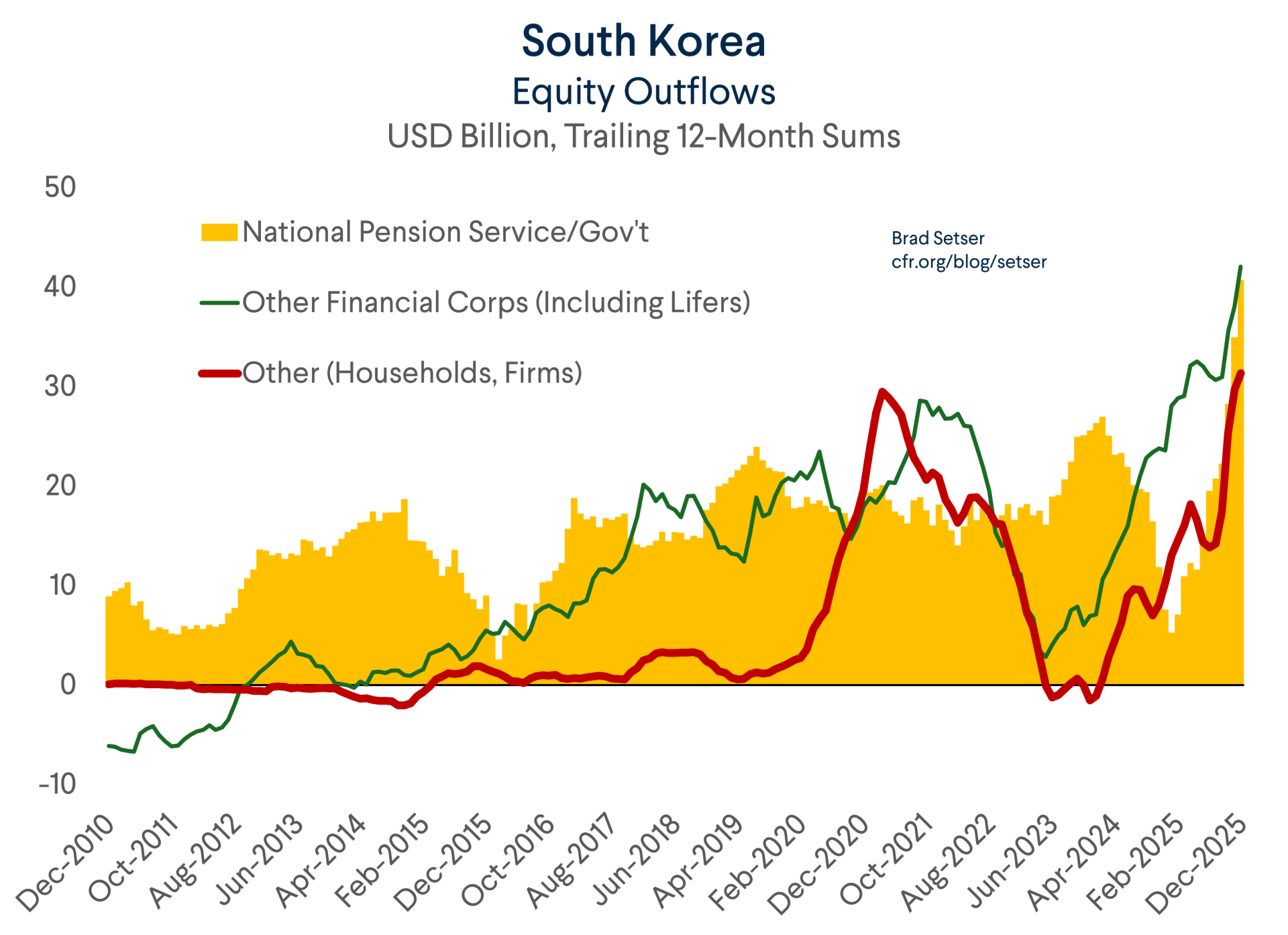

This wasn’t all from Korean day traders, though they were certainly a factor. Korea’s national pension service—a funded government pension fund that is increasing its foreign share—generated a $40 billion equity outflow (over 2 percent of Korea’s GDP). It is now widely recognized that the NPS is the single biggest actor in the market.

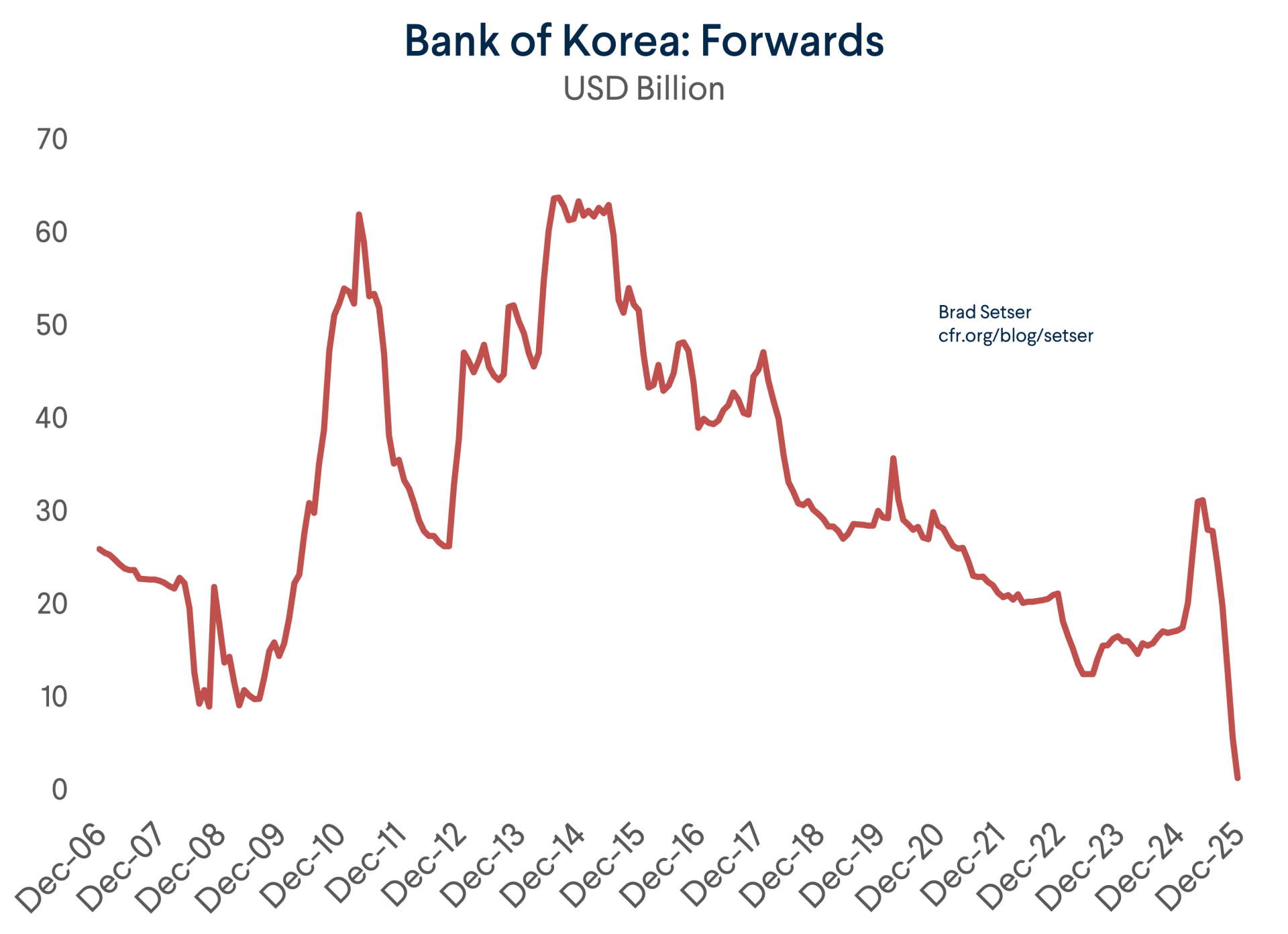

It looks like some of that outflow was hedged in the first part of the year, and then those hedges ran off at the end of the year. That is at least my interpretation of the (large) swing in the forward book of the Bank of Korea over the course of 2025. The rise in the Bank of Korea’s forwards book suggests that the National Pension Service made use of its swap arrangement with the Bank of Korea between January and May, but it appears that those hedges rolled off toward the end of 2025 (and there was an additional reduction in the forward position presumably from other operations of the central bank). The Korea Times reported that the National Pension Service’s hedge ratio had fallen to zero. The NPS can hedge up15% of its foreign portfolio counting tactical hedging, and its foreign portfolio is now 60% of its total assets—so changes in its hedge ratio matter for the market.

Of course, I don’t understand why the hedges were allowed to roll off at the end of the year given the broad weakness of the won. Coordination of policy hasn’t been a Korean forte; the Bank of Korea is now worried about the BOP impact of Korea’s investment commitments in their “trade deal” with the U.S.—which are capped at $20 billion a year and could be funded by external borrowing. That is a fair concern, but both Korea and the U.S. should have thought a bit about this earlier.

But it does seem like the won’s move toward 1500 at the end of 2025 concentrated minds. The NPS started doing “tactical hedging” in early December, which helped stabilize the market. Bloomberg: “South Korea’s National Pension Service has recently started selling dollars to bolster the won, according to a person familiar with the matter.” The NPS also resumed hedging directly with the Bank of Korea later in the month. More recently the NPS indicated that it would invest abroad with a bit more flexibility, and not automatically sell the domestic market and buy foreign assets to rebalance its portfolio as the KOPSI soared. The reduction in the target for foreign equities and increased scope to hold domestic equities should materially reduce the net outflow from the NPS this year.

The Governor of the Bank of Korea, who has long worried about the impact of the NPS on the market, was pleased:

“I believe that the announcement a few weeks ago by the National Pension Service that ”this year we will reduce overseas investments by more than 20 billion dollars“ and that ”we will hedge exchange rates and invest overseas more flexibly“ has made a major contribution. Expectations for further exchange rate increases have diminished, and in recent weeks, companies have also begun selling the dollars they were holding. Currently, capital outflows from overseas investments by the National Pension Service have decreased significantly, but individual investors‘ overseas investments in January and February have been leaving at roughly the same pace as the very high levels seen in October and November last year”

There of course other sources of institutional demand for foreign assets. But some of those sources of demand actually haven’t been as significant. For example, the life insurance outflow—which was significant in the days before Covid—has been muted recently. And partially as a result, the outflow from Korea hasn’t been driven by demand for foreign bonds.

I do wonder if the recent runup in Korean stocks (a weak won + plus rising memory prices = big profits) will lead to some reevaluation of Korea’s fascination with foreign equities. The changes at the National Pension Service may be the leading edge of such a shift.

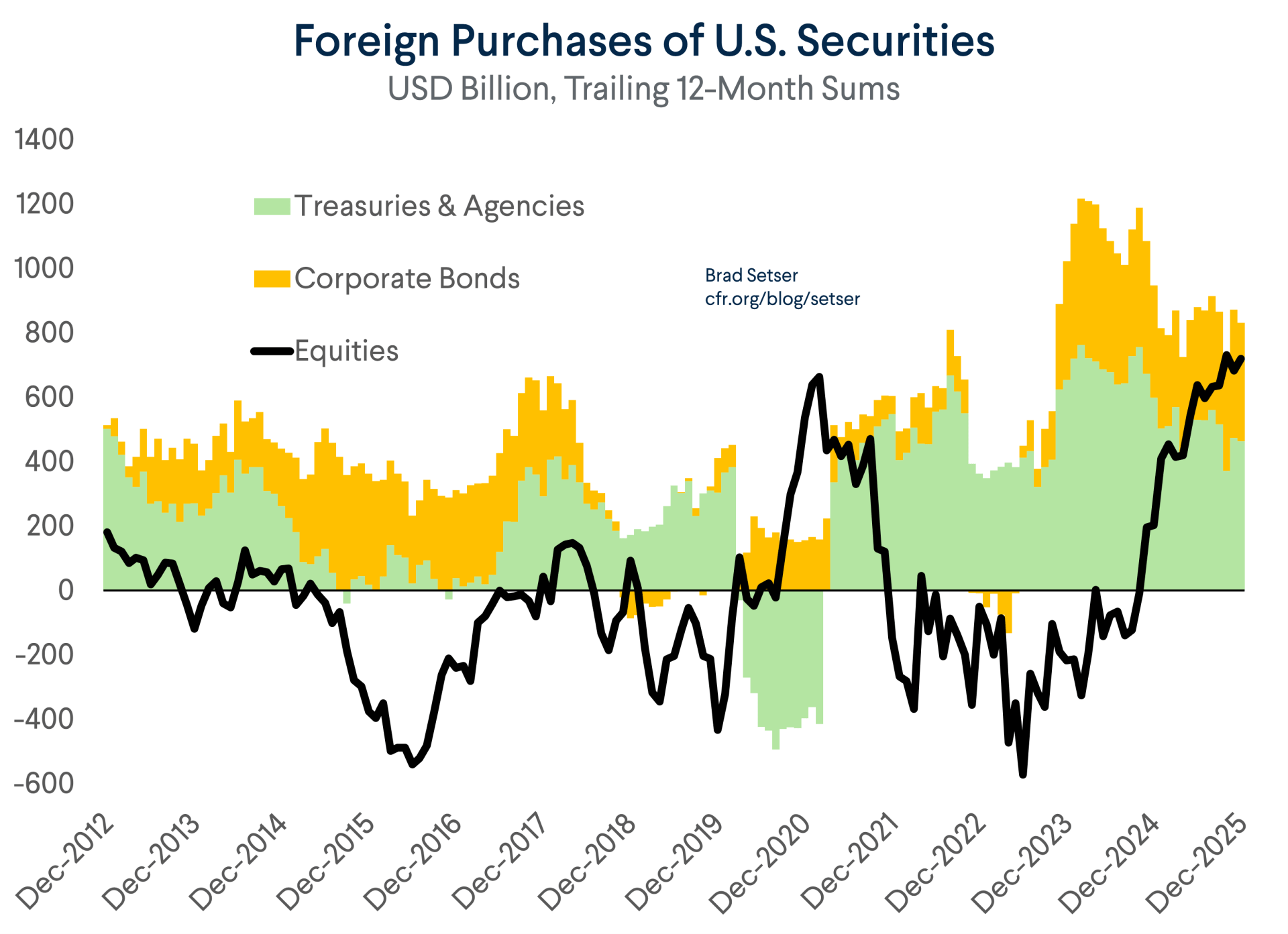

The decomposition of Korea’s financial account is interesting because it provides a concrete example (on the creditor side) of the shift in funding of the U.S. external deficit.

Historically, the U.S. current account deficit has been funded almost exclusively by foreign purchases of bonds—whether by reserve managers, or life insurers and pension funds seeking higher coupons than they could find in their home markets (both on U.S. Treasuries and U.S. corporate credit).

But in 2026, for the first time in a long time, a decent share of the new flow associated with the $1 trillion deficit came from equity inflows.

Of course, that means foreigners had a lot more interest in U.S. equities than Americans can in foreign equities. Indeed, U.S. investors have very little global exposure—most bond holdings are of dollar-denominated bonds, and often dollar-denominated bonds backed by a U.S. company.*

Right now, that big investment in U.S. equities isn’t paying off—both for foreign investors, who have given up returns in their home market, and U.S. investors, who aren’t currently benefitted from an undiversified portfolio.

Bottom line: it is a new world. The U.S. deficit isn’t being funded out of reserve growth (though with the recent surge in the foreign holdings of Chinese state banks, it could soon be funded out of shadow reserves) or even by life insurance flows. A big chunk actually came from momentum-driven flows into U.S. equities. Which only adds to my conviction that the dollar isn’t going to be a good hedge for U.S. equity exposure going forward.

* CLOs are typically a claim on the Caymans, with the Cayman entity in turn holding lots of U.S. loans. The net result is fake foreign exposure.