China’s Impact on the U.S. Bond Market Gets Too Much Attention. And Europe’s Too Little

The ECB has almost certainly had a bigger impact on U.S. rates over the last three years than the PBOC, without buying (or selling) any Treasuries.

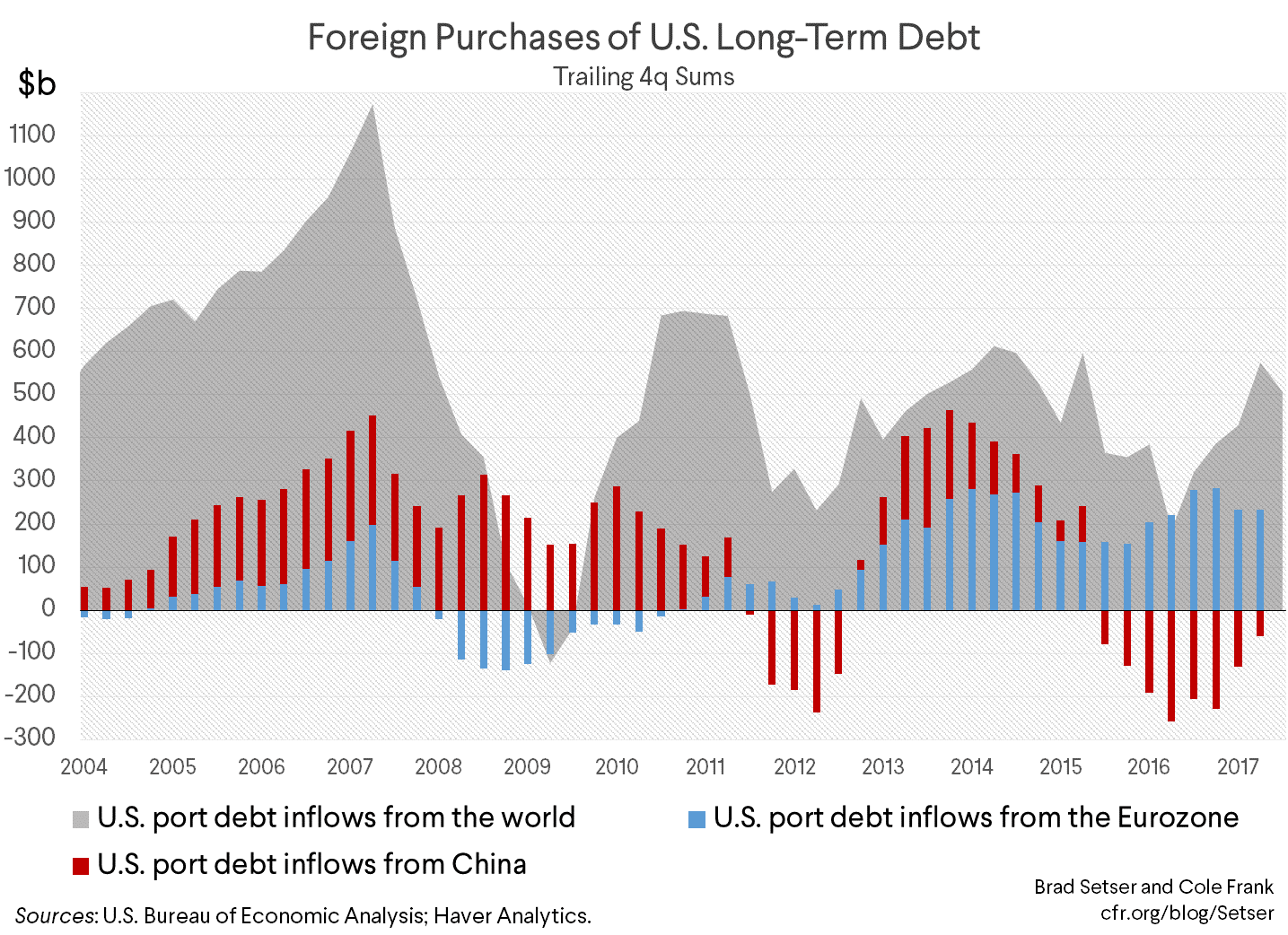

China’s impact on the U.S. bond market gets a lot of attention. China is, after all, still the largest single holder of Treasuries (and it also has a modest portfolio of agencies and perhaps some corporate bonds—though the latter don’t appear in the U.S. custodial data).

But China, in my view, hasn’t had a major impact on the bond market in the past year or so.

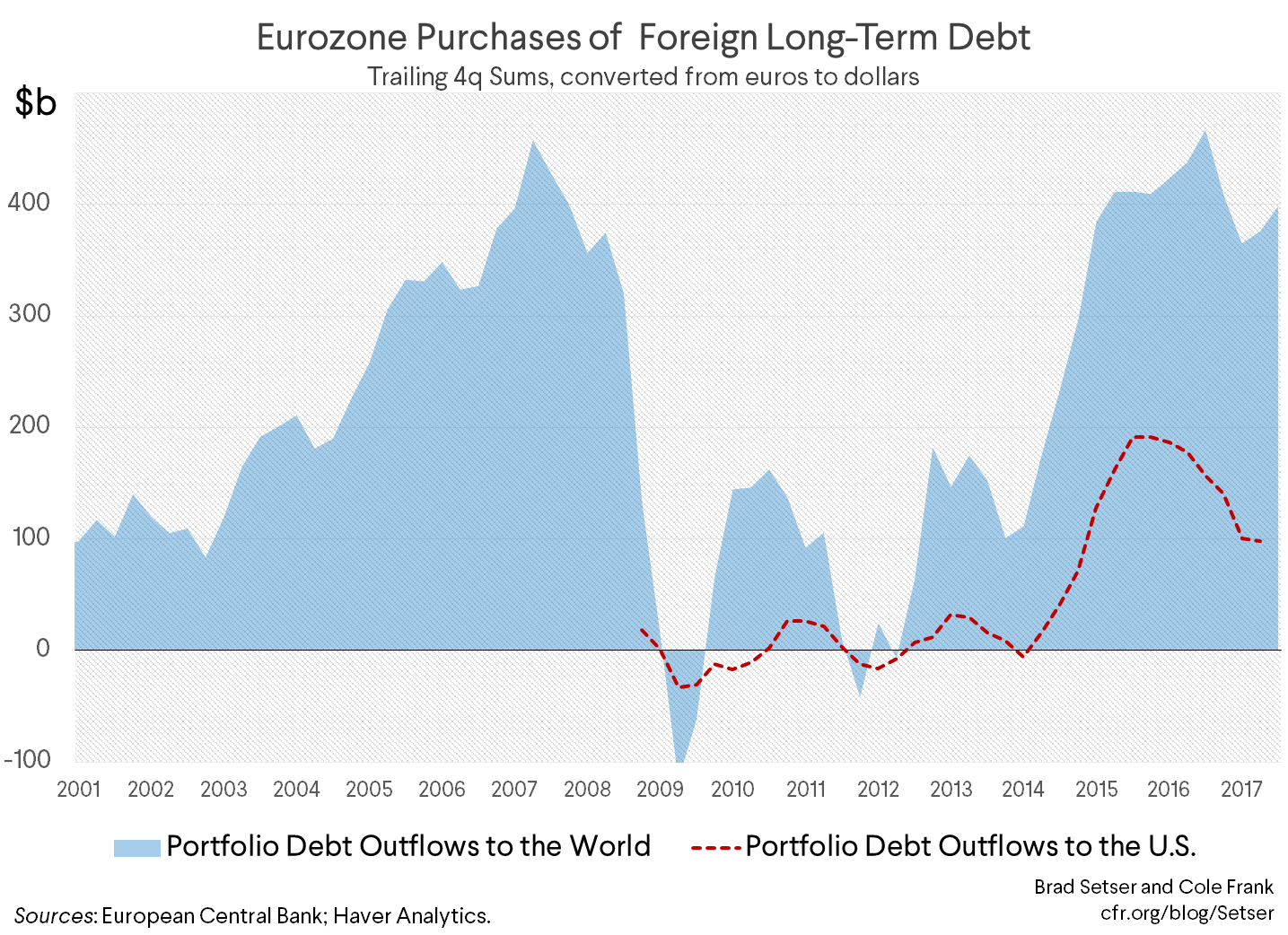

European flows into the U.S., by contrast, almost certainly have had an impact, helping to hold down yields at the long-end of the curve.

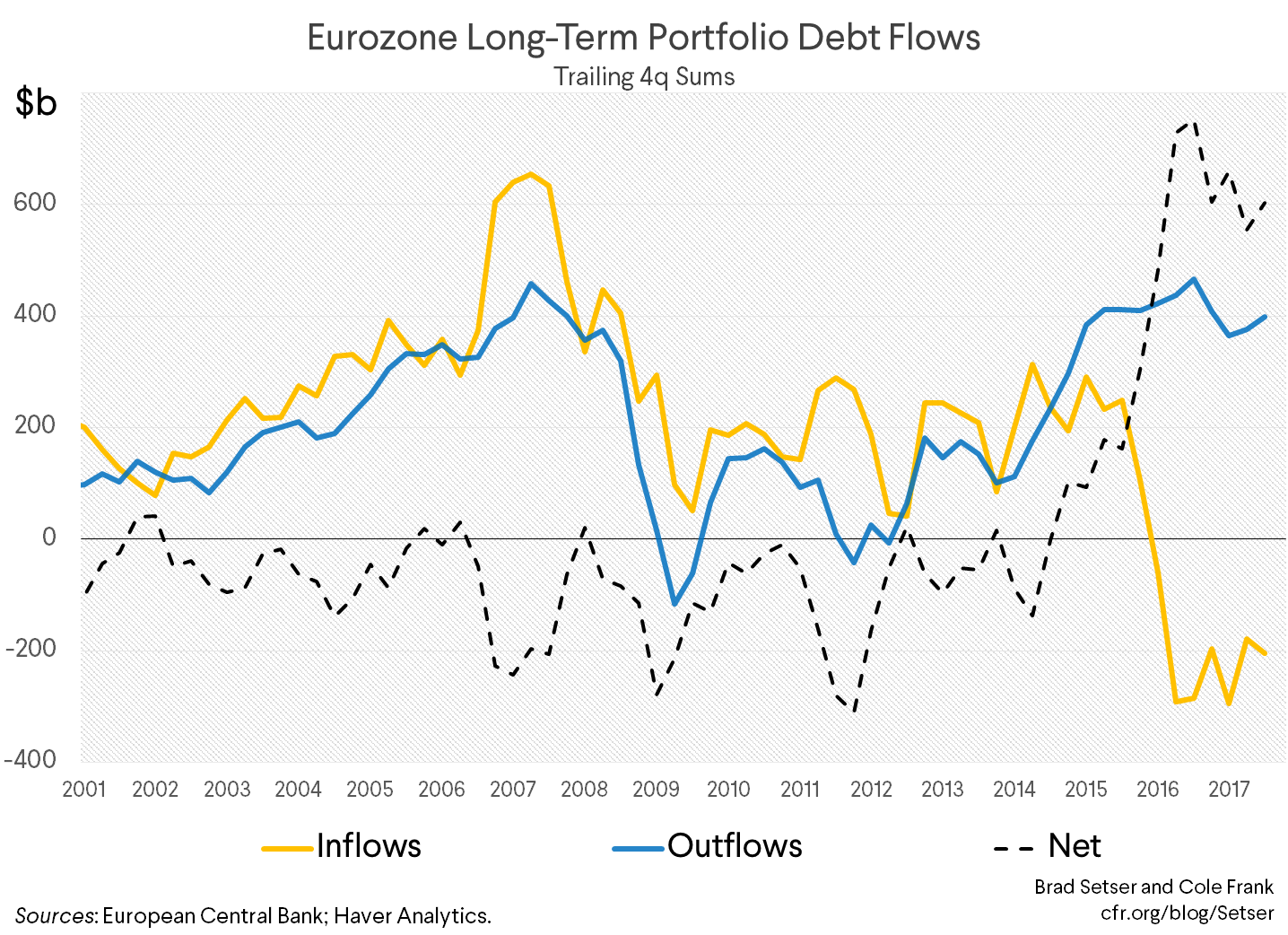

Europe of course isn’t a single actor. The ECB is buying a ton of euro-denominated bonds and it is (almost)* a single actor. But the ECB isn’t directly buying foreign assets—the private outflows stem from the the actions of a host of private investors responding to the incentives created by the ECB.

The ECB’s purchases have reduced the total stock of eurozone government bonds in private hands. Government bonds from some countries (cough, Germany and the Netherlands) are in short supply and generally quite expensive.

As a result, European investors have been adding heavily to their foreign portfolios looking for a yield pickup,** and from the European data, we know that a lot of those funds have flowed into the U.S.

And the European data also indicates that foreign investors have been selling some of their holdings of eurozone bonds—adding to the net outflow from the eurozone. But there isn’t a geographic breakdown of who is selling, so we don’t know for sure just how many eurozone bonds Americans have sold and (likely) put to work in the United States.

Japan of course is similar, though it is a bit harder to track (private Japanese outflows have been large, but—for some reason—they aren’t showing up in the U.S. TIC data).***

I confess that I am a bit late to this story. Cardiff Garcia was on the right trail back in 2015. And Benoit Coure spoke about the large outflow from the eurozone over the summer, and again at the IMF’s research conference last fall.

But it is clear that by far the biggest source of demand for U.S. fixed income assets these days is coming from the eurozone, not China. Europe has a bigger current account surplus than China, and the ECB’s QE and low rates have reduced eurozone bond yields below U.S. yields and created an incentive for fixed income investors to move their funds out of the eurozone.

Cynics even argue that the Germany position on European fiscal integration is designed in part to make sure that eurozone safe assets remain in scarce supply, as they don’t want any inflows that would bid up the euro after the ECB’s QE ends. I wouldn’t go quite that far, even if the effect of Germany’s reluctance to engage in fiscal risk sharing has been to limit the supply of safe eurozone assets.

And thus if a falloff in foreign demand for duration could trigger a jump up in U.S. Treasury yields—and there is a bit of a debate on the mechanics of how foreign inflows impact U.S. markets—a falloff in flows from Europe after ECB QE ends seems to pose far more of a risk than China.

It is just a little harder to see in the U.S. data, as European investors tend to buy a broader range of bonds, not just Treasuries—and the Treasury International Capital (TIC) data on corporate bonds is so polluted by custodial bias that it doesn’t provide much clarity.

Despite Bloomberg’s best effort, the Treasury flow story out of China is, I think, rather boring—and likely to stay boring.

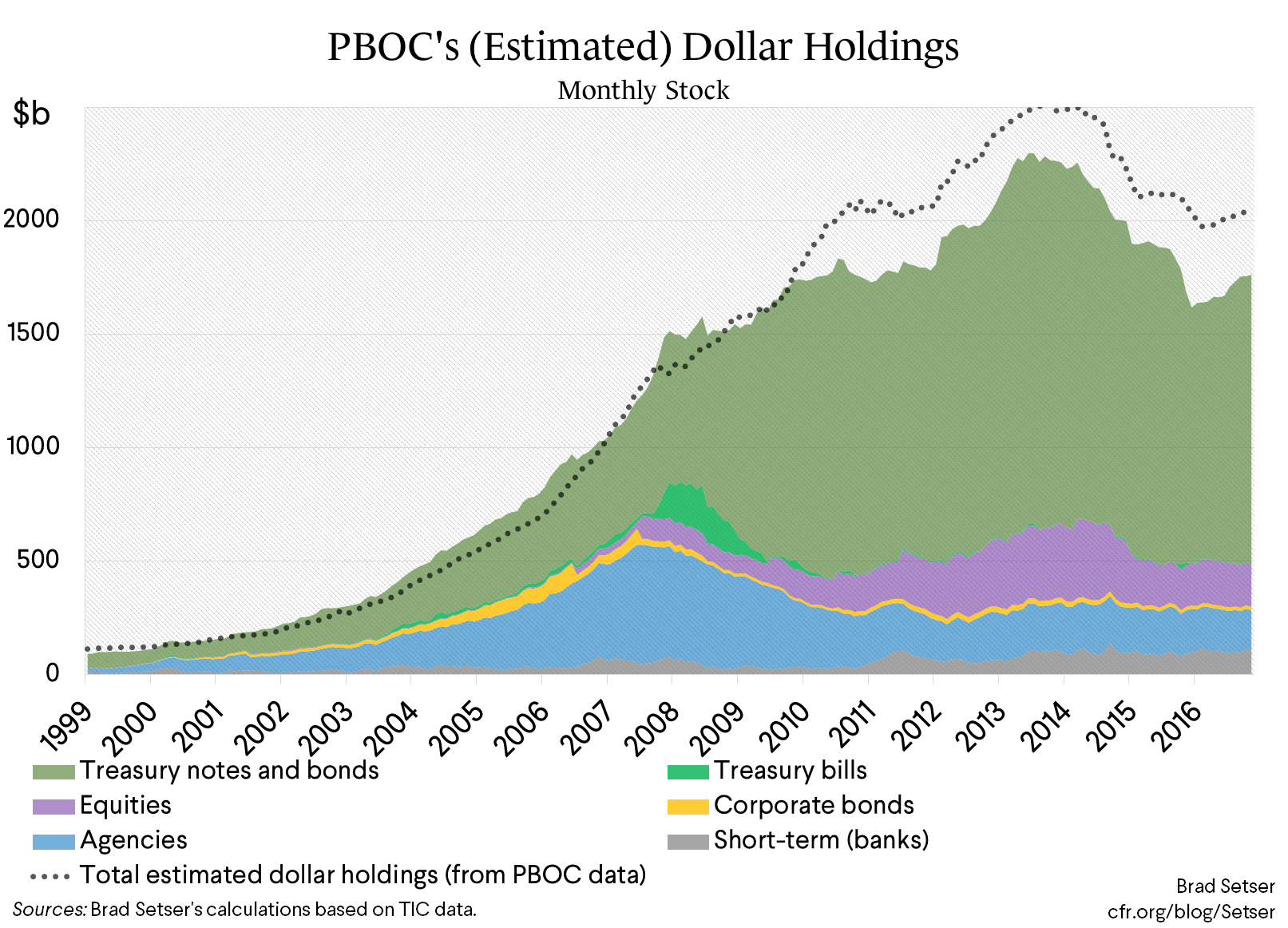

For a simple reason: China’s reserves have been stable, and stable reserves should lead to stable holdings and limited (net) flows, absent an (unlikely) big shift in China’s portfolio. China still has a (modest) current account surplus, so private Chinese investors are still on net moving funds abroad. But private Chinese investors generally don’t buy Treasuries. They may matter for some local property markets, but—absent a big shift in the State Administration for Foreign Exchange’s (SAFE) portfolio—the PBOC isn’t the kind of player in the bond market it once was.

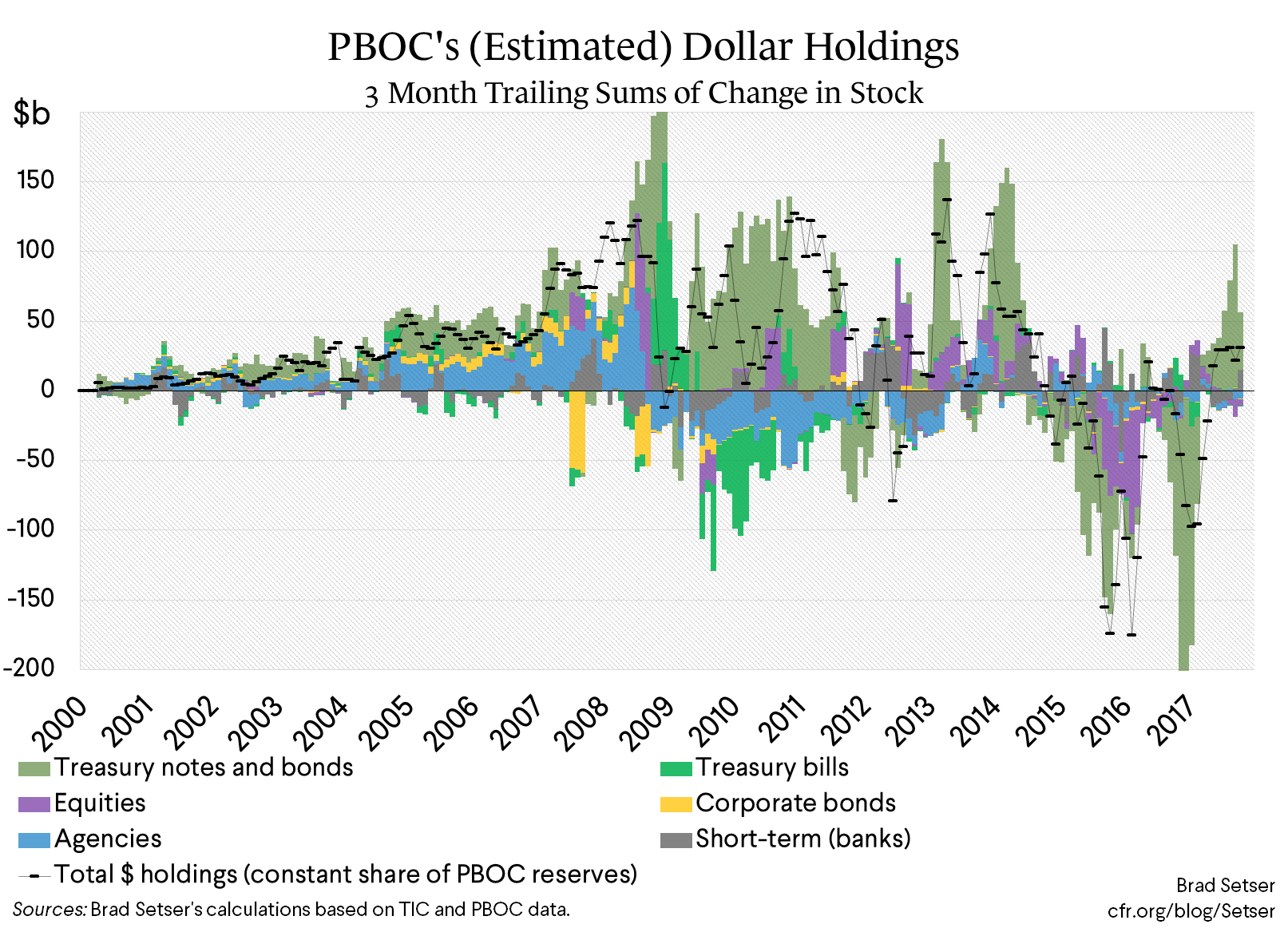

This year has actually seen a rise in China’s reported holdings of Treasuries even as China’s holdings of reserves seem more or less constant—allowing Bloomberg to write about the risks if China’s new purchases slow.

But the recent purchases seem largely to be a mirror of China’s somewhat larger than expected Treasury sales in 2016. China, it seems, wanted to rebuild its liquid portfolio after drawing on it 2016—China historically has kept about 40 percent of its reserves in Treasuries (and a majority in dollar assets of all sorts).

China shed about a trillion of reserves during the 18 months of intense pressure that followed its August 2015 devaluation (technically I guess an exchange rate reform, but it initially looked like a pure devaluation—and it certainly created expectations that China’s authorities wanted the yuan to depreciate that only dissipated in 2017). Initially, though, the fall in reserves didn’t lead to changes in China’s custodial holdings of Treasuries, as the PBOC instead reduced its equity holdings and ran down its “Belgian” account. But from mid-2016 on, the fall in reserves coincided with a fall in SAFE’s headline holdings in the U.S.

My guess is that SAFE’s Treasury holdings fell a bit below its target during this period. And that the rise in SAFE’s Treasury holdings this year thus represents a return to its long-term benchmark.

If that’s true, the absence of pressure on China’s reserves should lead to stable Treasury holdings and a falloff in new inflows from China. That would make China a bit like Japan’s Ministry of Finance (MOF): a big holder of Treasuries, but generally not a big buyer.

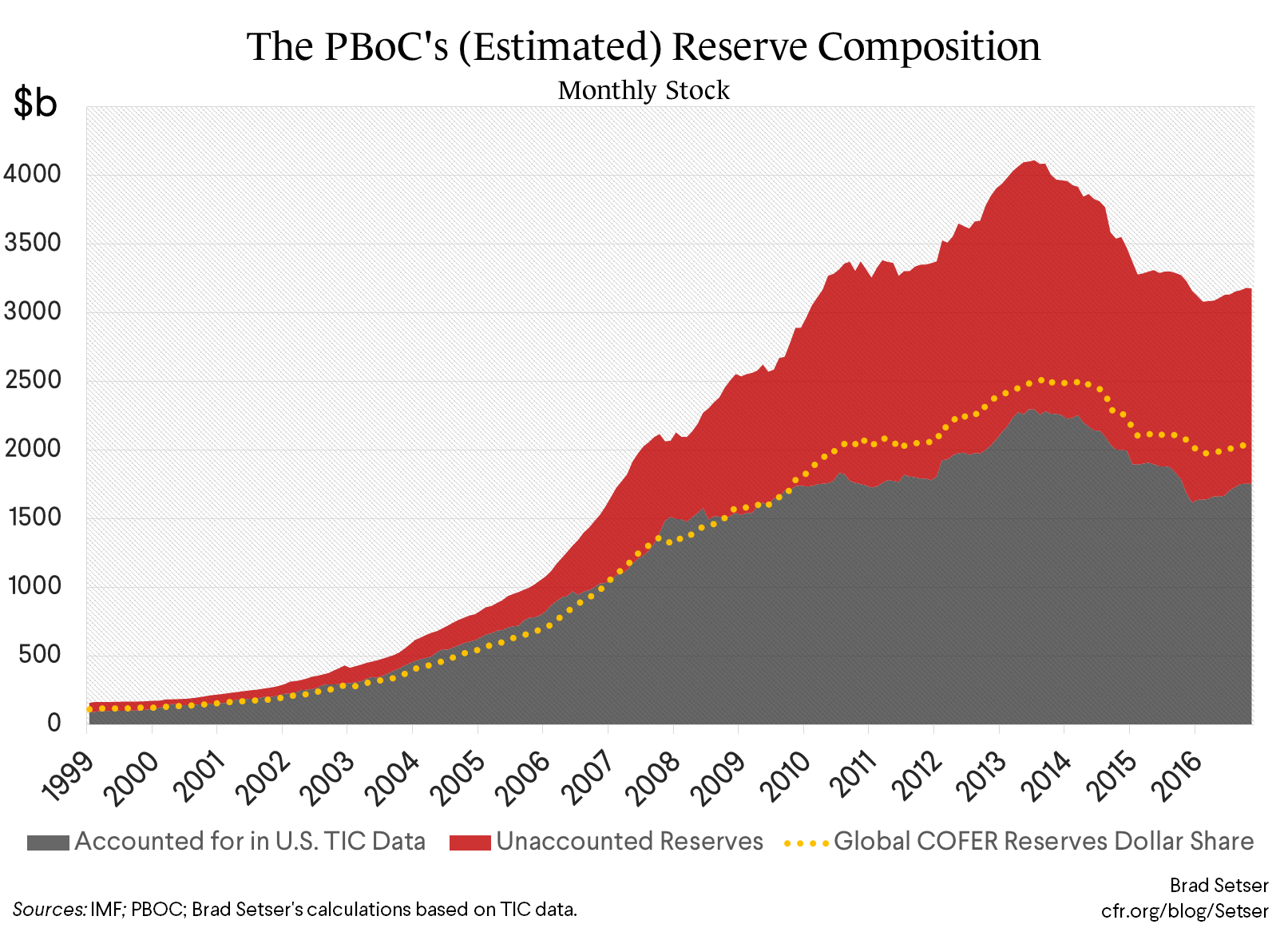

The interesting speculation around China isn’t that it may change its Treasury allocation and shake the Treasury market. Rather it is that China may change what it does with the 60 percent of its reserves that historically have not been in Treasuries—that’s close to $1.8 trillion, and those holdings are much harder to track than China’s Treasury flow.

I think I can identify the bulk of China’s dollar portfolio in the U.S. data—but that’s because Treasuries have traditionally accounted for something like two-thirds of China’s dollar holdings. The flip side is that the U.S. data only reveals about half of China’s current portfolio—and the half that is in the dark is huge, and shifts in that portfolio could have an impact on a range of smaller markets.

* Technically the euro system is doing the purchases, the Bundesbank buying German bonds, the Banque de France French bonds, the Banca d’Italia Italian bonds and so on. So it isn’t quite a single balance sheet. But the ECB’s bond purchases have been coordinated.

** I was surprised to see in a year end review that the yield differential between German and French 10 year bonds and U.S. ten year bonds fell a bit during 2017 (the yield on the ten-year Treasury was basically constant, while yields on German and French bonds inched up on expectations that the ECB will end its QE in 2018 as the eurozone’s recovery continues).

*** I am working on this, but haven’t quite figured it out. Help appreciated! Japan’s custodial holdings can be found here (see section B.2). I also don’t have easy access to the detailed Japanese balance of payments data right now, which has slowed me down a bit.