G-3 Coordination Failures of the Past Eight Years? (A Riff on Cœuré and Brainard)

The world would be in a better place today if the ECB and BoJ had joined the Fed in quantitative easing early on. Their lag in easing contributed to the policy gap that led to the dollar’s large 2014 appreciation.

Both the Fed (Brainard) and the ECB (Cœuré) have been thinking about the impact of “QE” on exchange rates and global flows in the last few months.

Cœuré‘s early July paper focuses on the recent past. ECB “QE” looks to have induced a significant rebalancing of global portfolios away from eurozone government bonds. Judging from the composition of flows into the U.S., eurozone investors look to have bought a decent amount of U.S. corporate bonds as a substitute for the eurozone government bonds in short supply (thanks in part to the eurozone’s relatively tight fiscal policy). And U.S. investors seem to have left European debt markets and returned home. Cœuré does a nice job of assembling the data, showing how ECB QE likely helped induced a rise in portfolio outflows from the eurozone (link to his graphs here). Those outflows are now the main counterpart to the eurozone’s external surplus.

Brainard’s recent speech also looks back a bit, but it is mostly about the future—one where central banks can choose among multiple tightening tools. The Fed, after all, has signaled that it is about to start reducing the size of its balance sheet (and laid out a plan for how to ramp up the pace of balance sheet reduction). If the Fed starts to reduce its balance sheet in September, it will be selling while the ECB is still buying—adding to the gap between the Fed’s policy stance and the ECB’s policy stance. (“Selling” is a bit of a metaphor—technically the Fed won’t rollover its existing portfolio, so the stock of Treasuries the market needs to absorb will rise—and exceed the Treasury’s net issuance for a period).

Right now, though, the market seems to be looking past the Fed’s expected decision to start reducing its balance sheet in September (or once the debt limit has been raised). It seems more interested in the possibility that the ECB will taper its own bond purchases in 2018 than in the Fed’s expected combination of balance sheet rolloff and further (perhaps modest) policy rate rises, especially with speculation that the Fed’s hiking cycle might end relatively soon if inflation remains weak and the pace of U.S. growth doesn’t materially pick up.

But rather than looking forward I want to look back a bit—as I think there have been (subtle) coordination failures over the past eight years. That is one reason why I would argue that central banks should put a bit more weight on the international spillovers of their actions.

The usual story told in official circles is one where central banks came together—after a difficult 2008—to restore confidence to global market and ward off the risk of a second great depression. The period of the global crisis was the high-water mark for G-20 coordination. And so on.

There is much truth to that story too, the G-20 really did have some early successes.

But within that broad story there were also, in my view, a couple of notable failures.

The global pivot to fiscal consolidation that was enshrined in the Toronto G-20 communique was wildly premature. It put a ton of pressure on monetary policy to support demand. Too much pressure. It slowed the global recovery. It was actually a pretty well-coordinated move, just in the wrong direction.

And I think that there was a second failure. In the face of a set of fairly common shocks—the slow global recovery, the premature fiscal pivot—G-3 monetary policies diverged a bit too much.

The Fed famously and controversially did QE2 back in 2010. That was the right call, for the U.S. and for the world. The global recovery was weak: it needed more, not less policy support.

The problem wasn’t that the Fed acted. It was that the other major central banks didn’t.

The BoJ didn’t really start to ease until early 2013.

The ECB didn’t do quantitative easing until 2014, though the LTROs (long-term loans at fixed rates to European banks) did provide some balance sheet expansion in 2012. Indeed, monetary conditions inside the eurozone tightened significantly in 2011 and the first part of 2012 even as the eurozone was doing a major fiscal tightening—helping to create the double dip recession.

At the end of the day, the rest of the G-3 followed the Fed—the ECB’s balance sheet is now bigger than the Fed’s, and Japan’s balance sheet expansion is much more aggressive than anything the Fed did.

But the other large advanced economies followed the U.S. with a lag.

And that lag had exchange rate consequences.

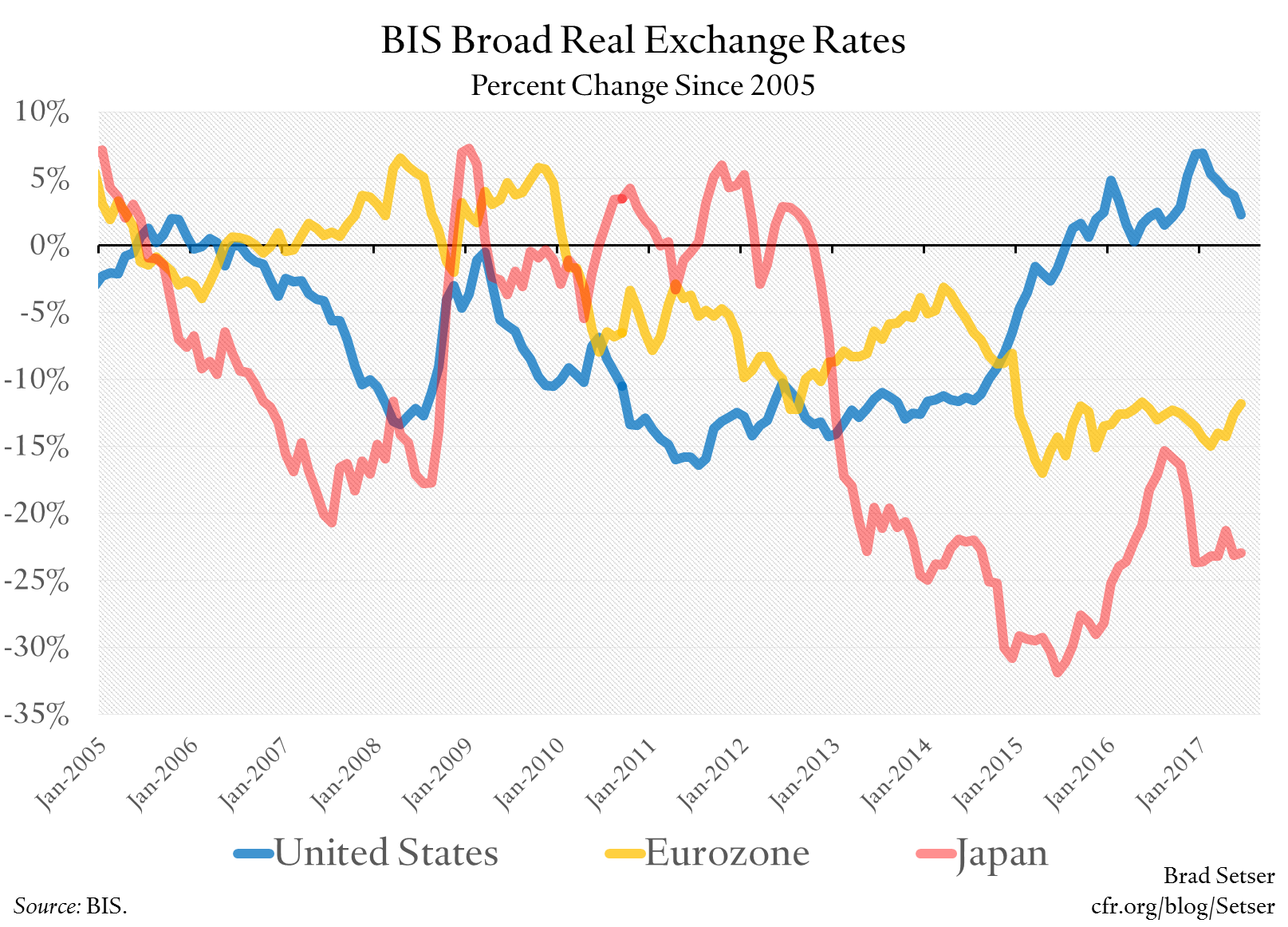

With hindsight, it seems that QE2 and QE3 helped keep the dollar relatively weak from 2010 to 2013 even though the eurozone was economically in worse shape. That wasn’t totally clear at the time. Neither the announcement nor the implementation of the Fed’s QE has much of an immediate impact on the dollar, and thus event studies tended to infer a small exchange rate impact. But I suspect it still had an impact, as in the absence of QE the dollar might have rose.

I confess that at the time I didn’t exactly mind. The weak dollar helped keep the U.S. current account deficit in check at a time when the U.S. recovery was weak: the U.S. at the time was clearly short demand, and sharing demand with the rest of the world would have slowed the U.S. recovery. Basically, the U.S. at the time was struggling to get demand back above its pre-crisis levels (let alone back to trend) and wasn’t strong enough to absorb the drag from a deterioration in the U.S. real trade balance, at least not easily.

But the policy divergence that helped keep the dollar weak against the majors through 2013 helped create the policy divergences in 2014 (Fed tightening, ECB easing) that pushed the dollar up. And the strong dollar has had more or less the expected impact on U.S. net exports (certainly it has had the expected impact on exports) over the last three years.

And the strong dollar in turn added to the pressures on China. That made for a difficult 2015 and 2016. For a while it seemed like the yuan might go into free fall, delivering a nasty global shock (fortunately that risk has receded, as China used its excess reserves to pull off what now looks to be a controlled depreciation—one that is starting to drive renewed rapid growth in China’s exports).

All in all I suspect the world would have been better off with more coordinated easing—with other central banks acting when the Fed acted, not with a lag—back in 2010 and 2011 and 2012. Instead it more or less got a coordinated fiscal tightening and an uncoordinated monetary offset.

Call it a missed opportunity. One that contributed to the uneven global recovery and the policy divergences that now have put some of the progress made on reducing external trade imbalances during the crisis at risk, with the dollar (still) too strong for the traded part of the U.S. economy (see Bill Cline’s forecast for what would happen to the trade balance if the dollar stayed at its pre-election level last fall, or this post)

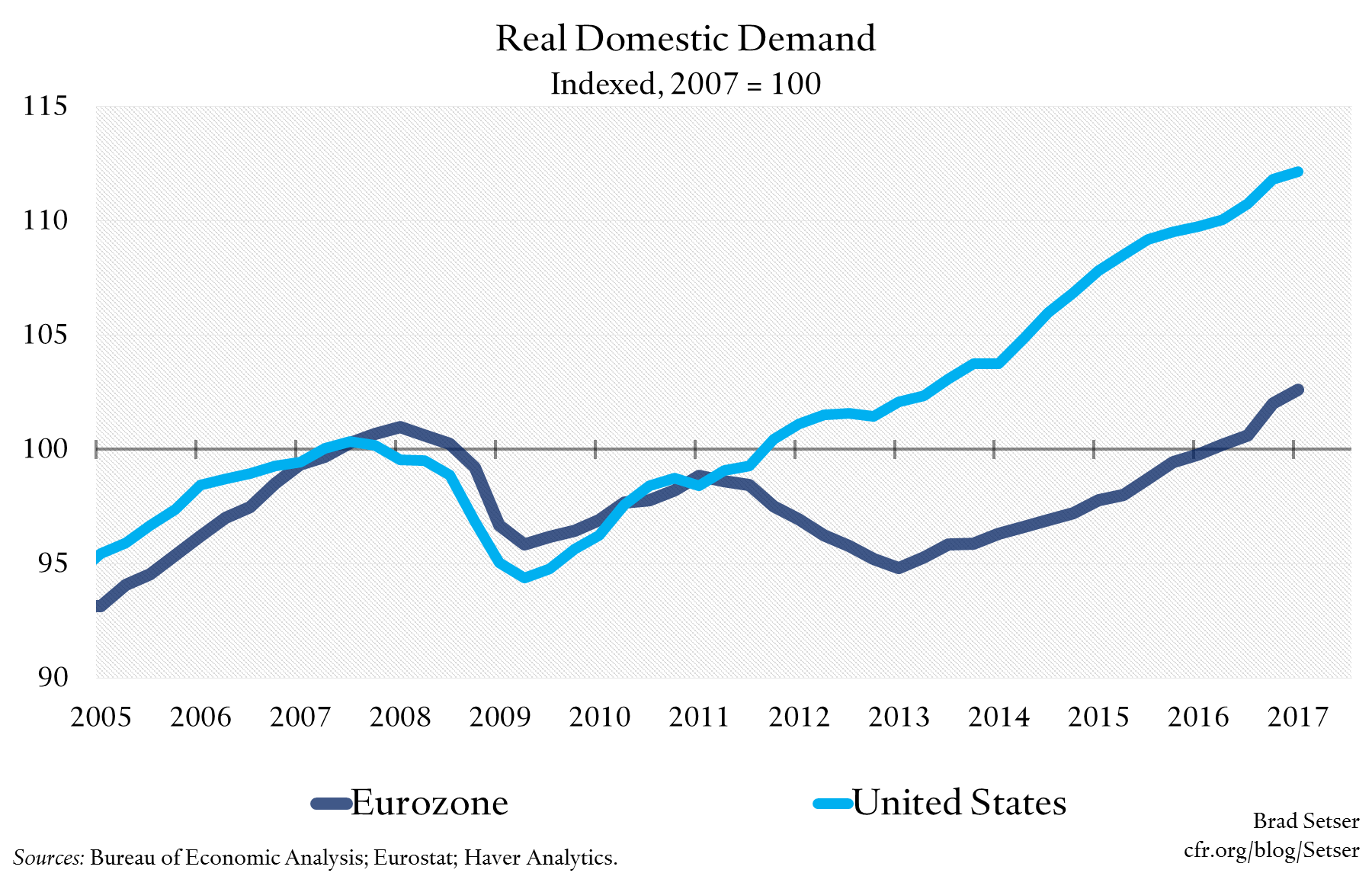

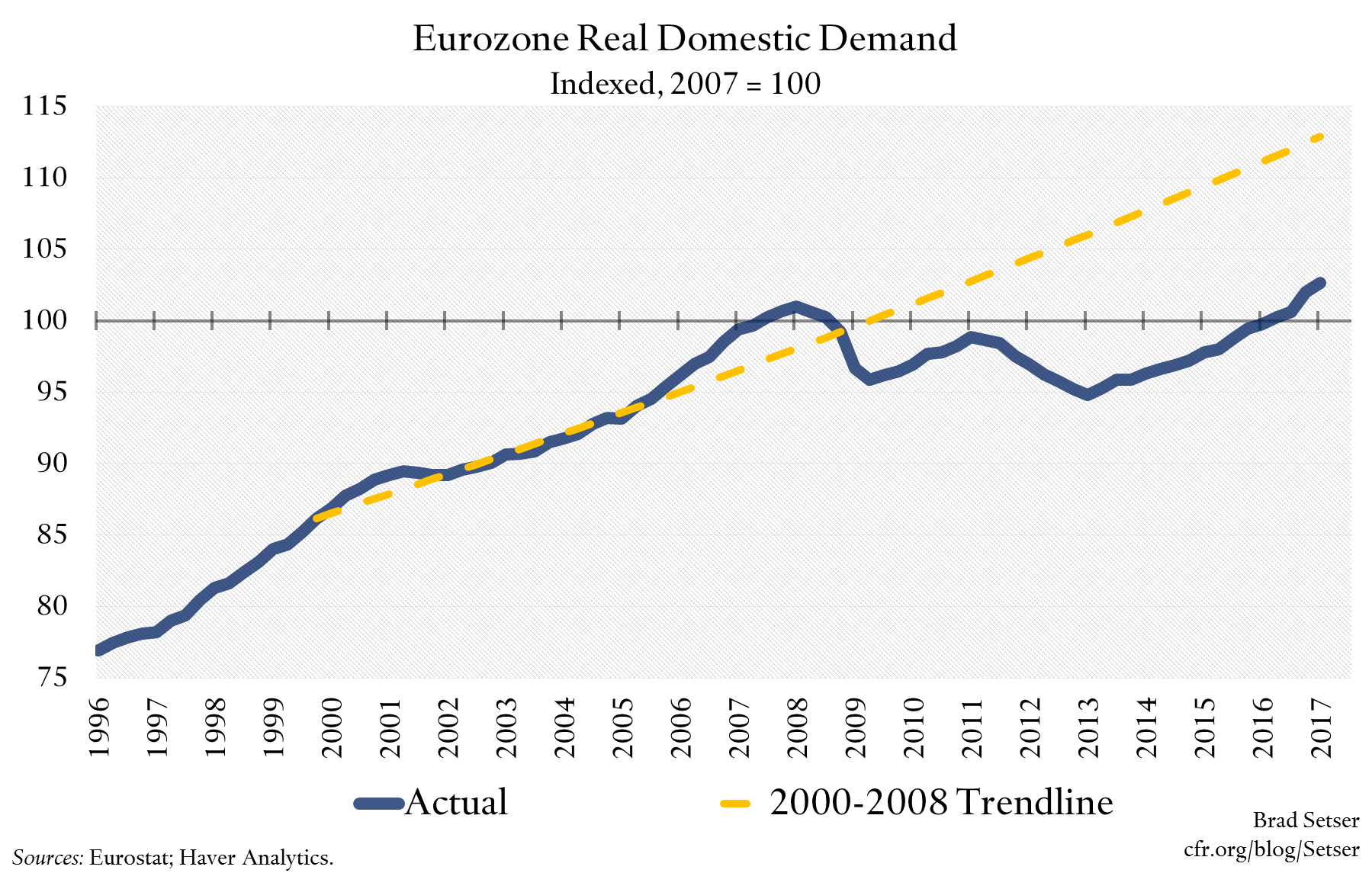

And now I worry that the Europeans have gotten perhaps a bit too fond of the policy mix that produced a weak euro—with Europe’s relatively tight fiscal policy (the structural deficit of the eurozone as a whole is about 1 percent of its GDP, well below the structural fiscal deficits of its main trading partners) offset by a relatively large external surplus.* Even now the eurozone’s domestic demand is far below what I consider a reasonable estimate of where it should be...

*/ Weak German export performance in June was probably a bit of a blip. Monthly trade data is volatile. But I wasn’t impressed by grumblings about how it showed that the “strong” euro was starting to weigh on Germany. Not when Germany has plenty of unused domestic fiscal space to do more to support its own demand, and its own growth (see the IMF’s Article IV report). And the basic point here applies more generally. The eurozone’s recovery now has a bit of momentum and as Cœuré notes in his speech, domestic demand has driven the recovery not net exports (in part I suspect because the commodity shock slowed everyone’s exports). But if France and Spain now move to tighten their fiscal policies without any offsetting easing in Germany or the Netherlands, the ongoing recovery may not do much to bring down the eurozone’s external surplus. Or, put differently, an fiscal drag inside the eurozone could maker harder for the ECB to scale back its easing, as there won’t be enough domestic demand growth to make up for any significant drag from net exports.