Are China’s RMB Swap Lines an Empty Vessel?

By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Dinah WalkerAnalyst, Geoeconomics

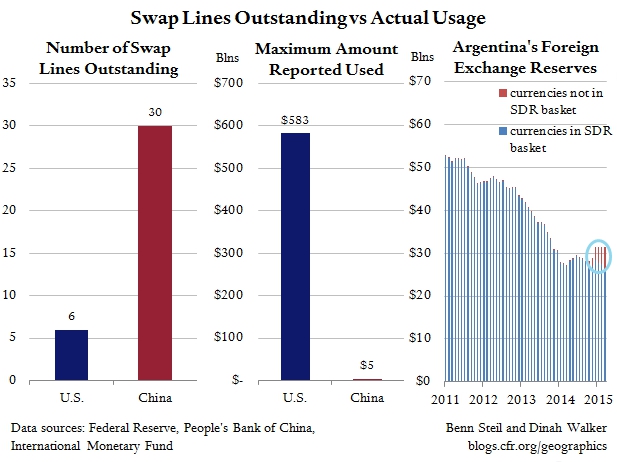

As our recent CFR interactive shows, central bank currency swaps have spread like wildfire since the financial crisis. In 2006, the Fed had only two open swap lines outstanding, with Canada and Mexico, for just $2 billion and $3 billion, respectively. At its high point in 2008, the Fed had fourteen open swap lines, with as much as $583 billion drawn.

The central bank that has been most active in creating swap lines, however, is China; the People’s Bank of China (PBoC) is expected to sign a swap agreement with Chile this week, bringing the total number of outstanding swap lines to thirty-one. The extension of these swap lines is clearly part of China’s high-profile recent initiatives to internationalize the RMB.

What is most interesting about this effort so far is that whereas everyone seems interested in having a swap line with China, almost no one has thus far had any interest in using it. And when they have used it the amounts accessed have been tiny – as shown in the middle figure in our graphic above.

The only actual RMB swap use advertised by China was back in 2010, when it sent 20 billion yuan (about $3 billion) to the Hong Kong Monetary Authority to enable companies in Hong Kong to settle RMB trade with the mainland. But this is basically China trading with itself. The Korean Ministry of Finance publicized a tiny swap in 2013 in which it accessed 62 million yuan (about $10 million) to help Korean importers make payments.

The only interesting case is that of Argentina, which activated its RMB swap line last year, and has reportedly drawn $2.7 billion worth. The effect of the swaps on Argentina’s reserves is shown at the far right of the graphic.

Argentina has the right to draw on a total of $11 billion worth of RMB. Its central bank has made a point of emphasizing that, under the terms of its agreement with the PBoC, the RMB may be freely converted into dollars – which Argentina, whose reserves have plummeted from $53bn in 2011 to $31bn today, is worryingly short of.

In effect, then, what Argentina has done by activating the RMB swap line is to add “vouchers” for dollars, freeing up the actual dollars in its reserves for imminent needs, such as imports and FX market intervention, and signaling to the markets that billions more can be accessed in a pinch.

The take-away is that whereas the RMB is slowly becoming an alternative to the dollar for settling Chinese goods trade, it is still far from being a currency that anyone actually needs – except maybe as a substitute for Fed dollar swap lines, which few central banks currently have access to. If Russia’s dollar reserves continue to fall, therefore, China may be the first place it turns.

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”