Better Late Than Never: The IMF Starts to Recognizes Balance of Payments Reality

The IMF marked its assessment of external imbalances to market, but its model and approach still struggle to get China right.

There are a few things to note in the IMF’s new external sector report:

- The IMF—wisely—chooses to emphasize the (modest) increase in the measured global current account surplus rather than how small China’s reported current account surplus still is.

- The IMF got incredibly lucky that China (apparently) adjusted its own new current account methodology over the course of 2024. If China’s Q2 2024 current account methodology had been carried through the full year, China’s reported surplus would have been 1.5 percent of China’s GDP—only a bit higher than the 1.2 percent of GDP surplus that the Fund’s model “thinks” China should have.

- The IMF’s forecasting of external deficits and surpluses got the U.S. and Chinese external surplus broadly correct, but for the wrong reasons. One interpretation of the large weight of the model on “net foreign assets” is that model expects a big imbalance in investment income. But for China and the U.S., the underlying imbalance is, in fact, all trade.

- The Fund’s statistics division didn’t think through the consequences of its recommendation that countries implement the “transfer of value” principal by using an internal survey rather than customs data to determine the goods balance. China’s new survey is materially reducing China’s reported surplus and reading between the lines, the IMF doesn’t quite trust the numbers that have emerged from China’s adoption of this (poorly thought through) recommendation.

- The IMF still struggles to find a good way to describe the United States’ role in the global financial system. The argument that the U.S. is the world’s banker is dated; the U.S. no longer borrows cheaply from the world to invest in high-yielding assets. A better frame would be that the U.S. has been the main source of relatively safe financial returns for most of the world for the last ten plus years.

- The IMF—like the U.S. Treasury—doesn’t have a good methodology for incorporating backdoor intervention by countries like China or the accumulation of foreign assets by sovereign wealth funds into its balance of payments analysis, and as a result, its “intervention” variable has basically become useless.* Time for a rethink!

The Global Current Account Imbalance is Expanding

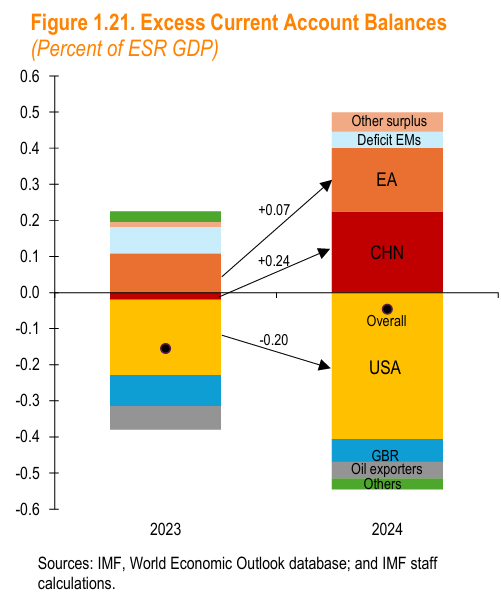

The IMF’s “message” is that the widening of the U.S. deficit and the Chinese surplus over the course of 2024 was unwelcome—it took both countries away from their estimated current account balances (in reality, those estimates are art as much as science, but set that aside for now...) That is clearly the right message.

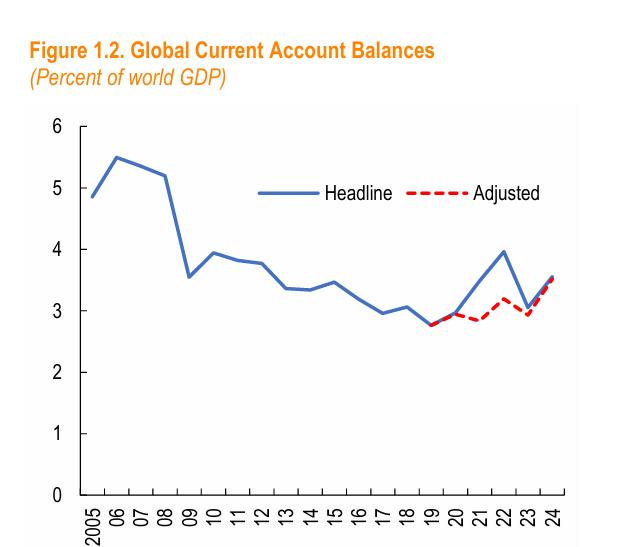

The IMF also didn’t repeat the mistake it made in the summer of 2024, when it looked at the fall in the global imbalance between the end of 2022 and the end of 2023 and ignored higher frequency data indicating that imbalances were in fact widening. It also cleverly constructed a chart showing that the pandemic-adjusted imbalance only really started to widen in 2024 (but for China’s whacky data adjustments it would have started much earlier, keep reading for more).

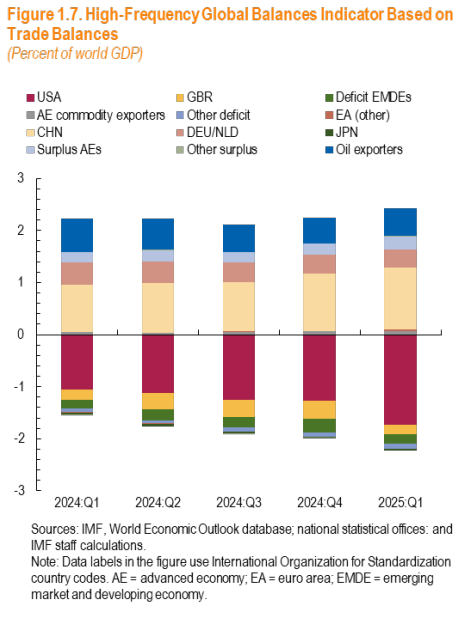

The IMF also provided a supplementary chart on the global goods trade balance (using the BOP goods data, alas) for the first quarter of 2025. That chart even more than the assessment of the reported current account balances shows how big and symmetric the U.S. and Chinese goods deficit and surplus now are: both are now more than 1 percent of World GDP.

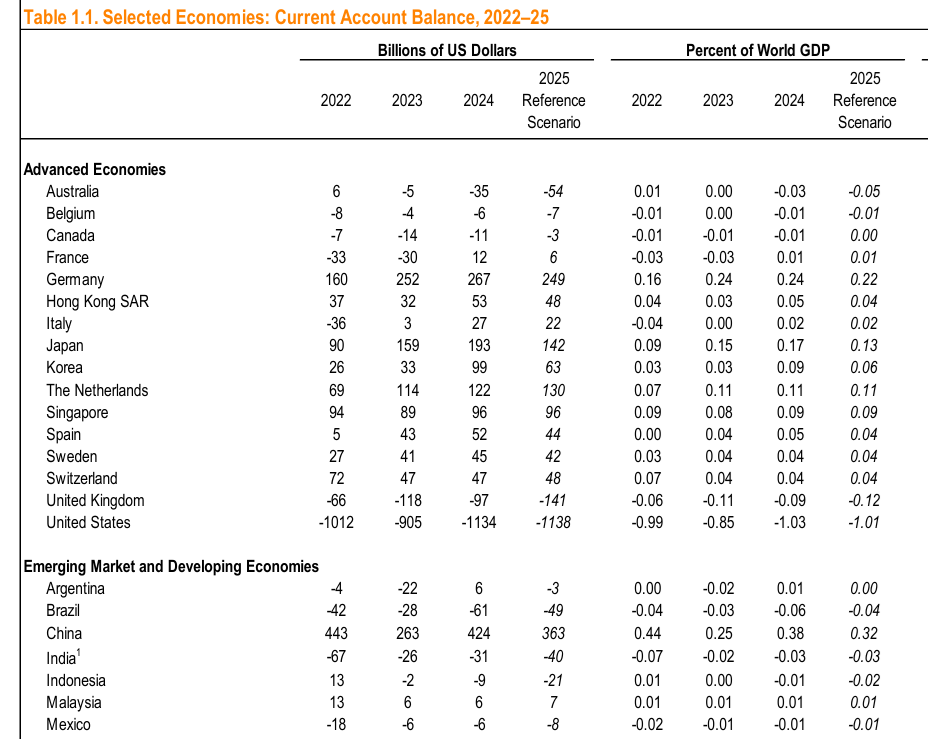

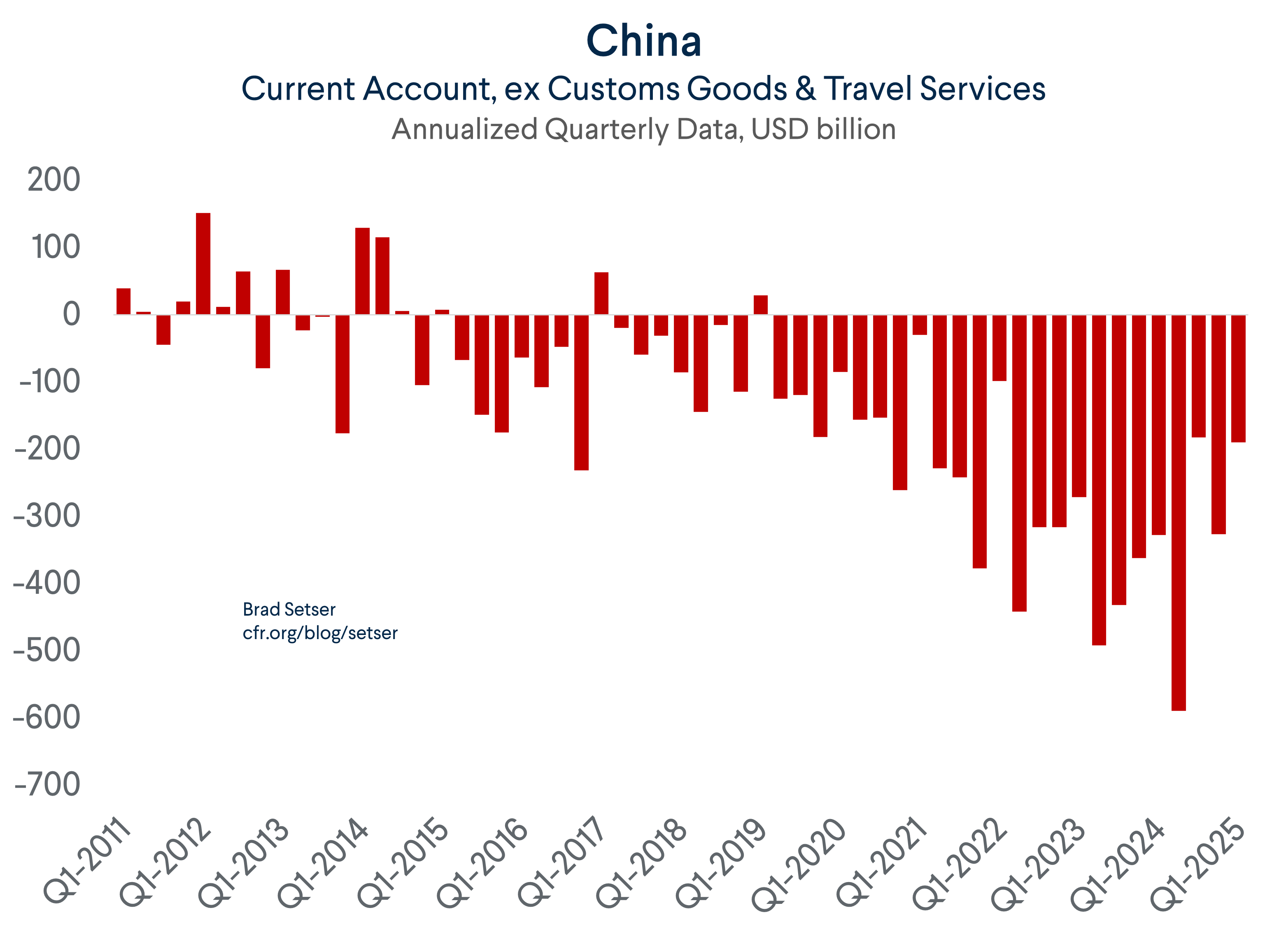

However, the IMF’s forward-looking forecasting of imbalances needs some work; it has the surpluses of China, Japan, and Korea all falling in 2025. China’s surplus falls back to $365 billion even as the high frequency trade data points to a big increase in the trade surplus and even after the CNY depreciated another 10 percent. The customs goods surplus increased by $150 billion in the first half of 2025, and a conversative forecast of the current account surplus through Q2 2025 puts it at just over $600 billion, so the IMF’s forecast is going to be WAY off.**

Come on, man!

The Fund has long been criticized for forecasting future imbalances away. This is a classic case (the 2025 reference scenario is also at odds with the higher frequency data for other important countries; Korea’s surplus, for example, has expanded in H1 2025).

The IMF Got Lucky

I don’t think the IMF fully realizes how fortunate they were in 2024. China, somewhat surprisingly and for unknown reasons, scaled back the “BOP” adjustment from its new survey after the second quarter of 2024. That adjustment in turn led China’s reported surplus to rise by close to $160 billion in 2024, and allowed the IMF to paint a story where “excess imbalances” widened.

But with China’s new methodology for reporting the balance of payments, this rise wasn’t at all a foregone conclusion. At the end of Q2 2024, China’s reported surplus was down to 1.2 percent of GDP on a trailing 4-quarter basis. If the gap between the visible customs balance and the visible tourism deficit present in the second quarter of 2024 has persisted in Q3 and Q4, the reported current account surplus for the full year would only have been 1.5 percent of GDP—in line with the model (see the fall in the red bars in the chart below)

In other words, absent some untransparent adjustments to the new adjustments that China makes to its balance of payments data, the “excess” imbalance in China that the IMF highlights would have disappeared.

More significantly, the reported current account surplus in 2024 is essentially unchanged from its end-2021 level—the 2024 jump is only because the 2023 surplus was incredibly (unbelievably, you might say) small.

Since the end of 2021, China’s surplus in manufactures has increased by $500 billion—a rather big change. Sort of what you would expect from a country that has experienced a massive boom in auto exports after pivoting to manufacturing at end of a property bubble!

Some of that has been offset by higher commodity imports (especially in 2022, when oil prices were high).

Some by the recovery in tourism after the end of China’s Zero-Covid, hermit kingdom days.

But an awful lot is expected by the weird deterioration in China’s income balance and the supposed improvements from China’s IMF approved new BOP methodology.

Net Foreign Assets and the Current Account

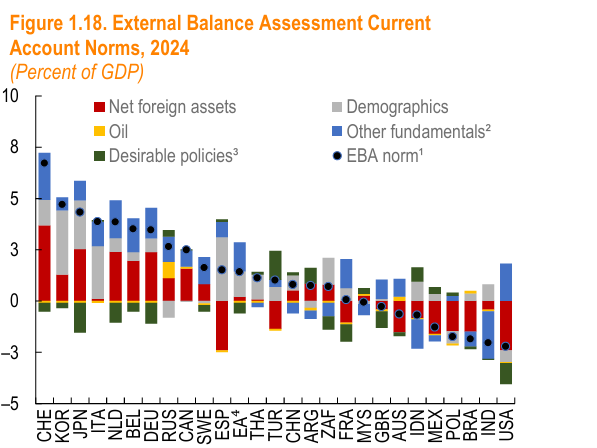

The IMF’s norms for a country’s current account are heavily influenced by a country’s net foreign asset position (which, in theory, either relates to the income balance or is a clever way of working the lagged current account balance into the model as deficits and surpluses have tended to be persistent), demographics, and relative levels of development (poorer countries should have external deficits as they build up their capital stocks and “catch up”).

Policy variables turn out to not be very important—no one has been intervening in the FX market on a scale that matters in a way that the IMF’s narrow intervention metric picks up, and the IMF thinks everyone runs too loose a fiscal policy, so the aggregate impact of fiscal deficits of the surplus and deficit countries largely cancel each other out.

But the key data points from the two largest economies are a bit at odds with the model weight on net foreign assets.

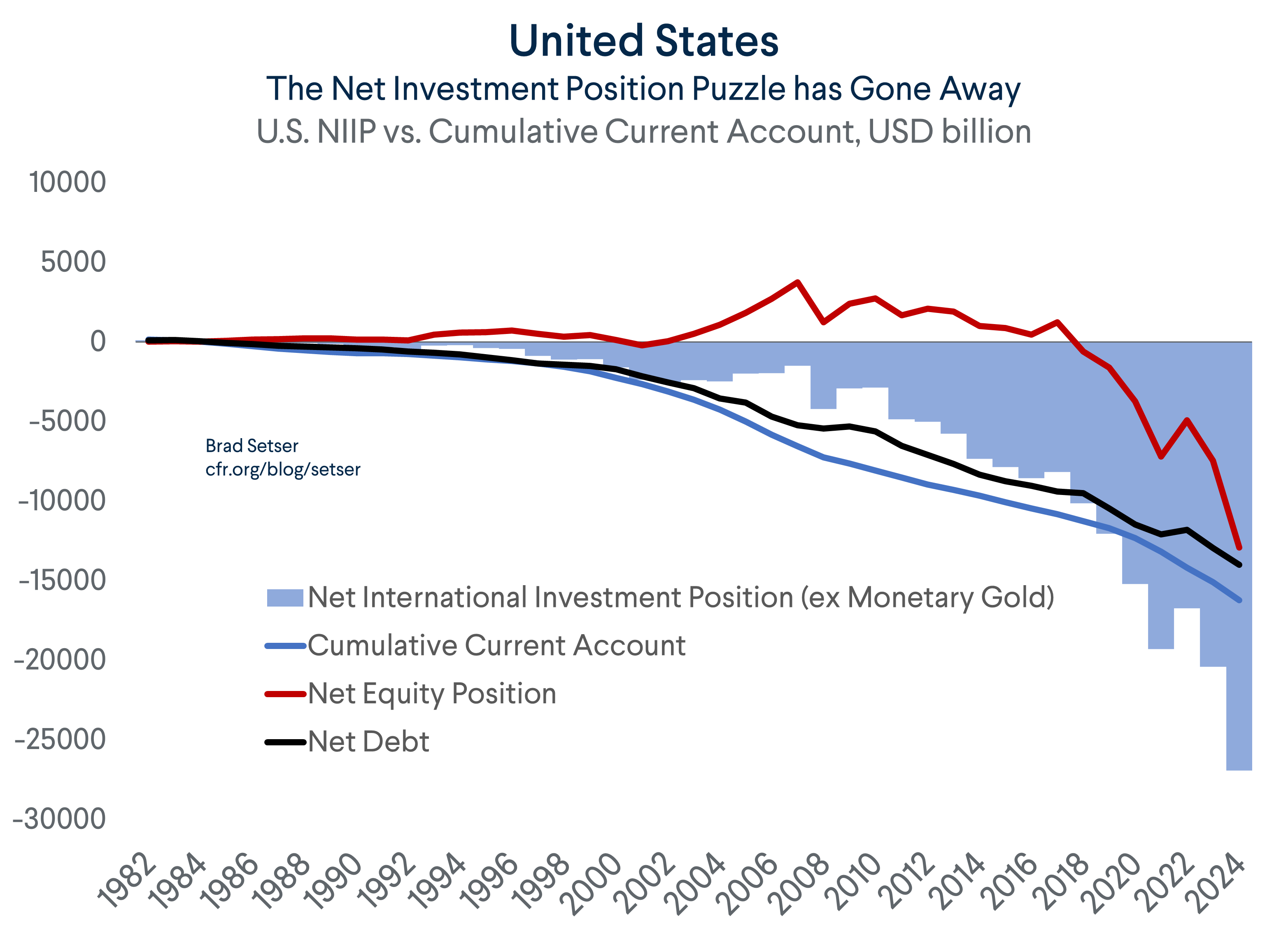

The U.S. has very large negative net foreign assets position (~90 percent of U.S. GDP) thanks to a big net debt position and net equity deficit, but doesn’t run the kind of income deficit that it “should” in the IMF’s model. Because of tax, I would say, interest on debt maps to the net debt position. But the income balance is well in balance while the negative net foreign asset position of 90 percent of GDP alone generates a “current account norm” of around 3 percent of GDP (see the chart above, which really needs to be blown out and also presented as a table in the IMF’s ESR).

China has a modest net creditor position (~18 percent of GDP) that should translate into an income surplus. In other words, there is a massive gap between the “income balance” implied by the model and the the 3/4th of a point of GDP deficit observed in China’s reported data—that gap in effect offsets a Chinese trade surpluses than certainly appears to be much larger than indicated (implicitly) by the model. A half point of GDP “norm” from the income surplus implies a trade surplus of 0.5 to 1 percent of GDP to fit within the overall current account norm of a modest 1 to 1.5 pp of GDP surplus).

A lower weight on net foreign assets, in other words, would generate a much bigger measure of the “excess” imbalance run by both the U.S. and China, which makes sense to me.

The Measuring of Imbalances

Another critical box is Box 1.1 on measuring imbalances. Boring, perhaps—but critical.

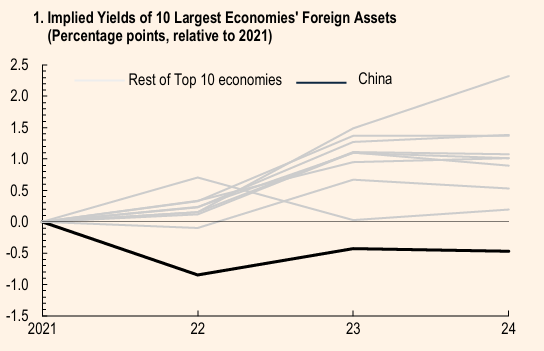

This is where the IMF notes, correctly, that China’s income data makes no sense.

A rising stock position and rising global rates should lead to an improvement in the income balance—and China is reporting a deficit that is far larger than its deficit back in the pre-pandemic days.

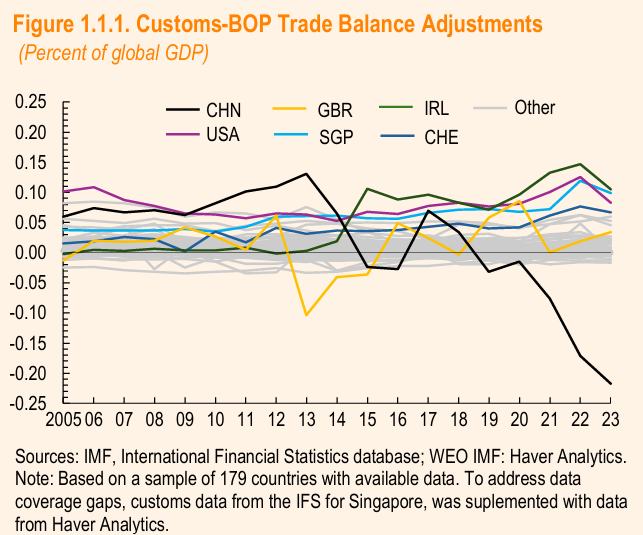

The IMF dances around the issues raised by China’s new methodology for reporting its balance of payments goods data.

The IMF thinks (incorrectly, in my view) that it cannot directly criticize China’s data, because the IMF now recommends using a survey rather than customs data to measure the goods balance on the transfer of value principal that reflects global value chains (essentially contract manufacturers operating in China to make goods for global firms; Hon Hai producing phones for Apple being the most famous example).

But the IMF does note that the application of this new approach by China (but not by others) is producing some potential distortions, and that there is no way to check China’s new data against counterparty data as other large countries don’t use a similar methodology to construct the goods balance in their balance of payments data.

Figure 1.1.1 certainly raises some important questions.

I would additionally argue that the IMF can challenge China’s implementation of the new data standard, as the story that China has provided for the gap between customs and the balance of payments has not checked out.

The argument is that the “customs declaration” price for exports from contract manufactures (like Hon Hai) that is reported in the customs data is higher than the actual payments the contract manufacturer receives from its offshore client (like Apple’s Irish subsidiary). That simply isn’t the case for phones. The customs price is the price that Apple pays. Apple applies its offshore markup in the BOP entity called “Ireland” (hence Ireland’s massive goods surplus, which the IMF should understand well). China hasn’t provided any sector detail that would support a downward adjustment of up to $300 billion (it varies a lot, one quarter it was more like $600 billion annualized) relative to China’s pre-2021 customs-based methodology.

It shouldn’t be hard to provide supporting evidence—as there should be sectors where the new Chinese internal survey identifies a gap in payments relative to what shows up in customs. Those gaps could then be revealed and assessed.

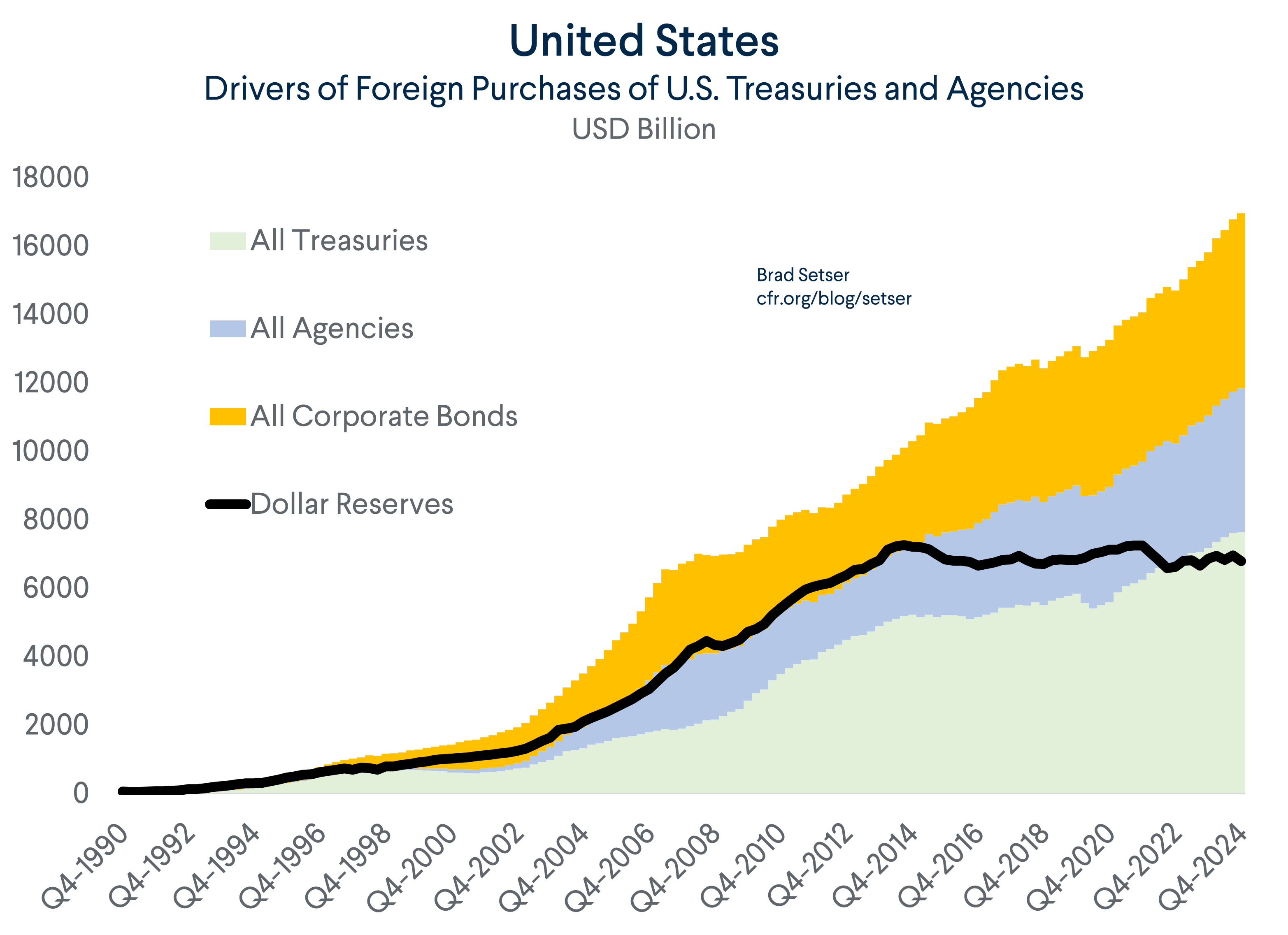

Time to Call the United States a Big Borrower, not the World’s Banker (or PE firm)

The U.S. isn’t the world’s banker, yet the IMF (and others) cannot get around this dated language (see the discussion of the United States in the chapter on the international monetary system).

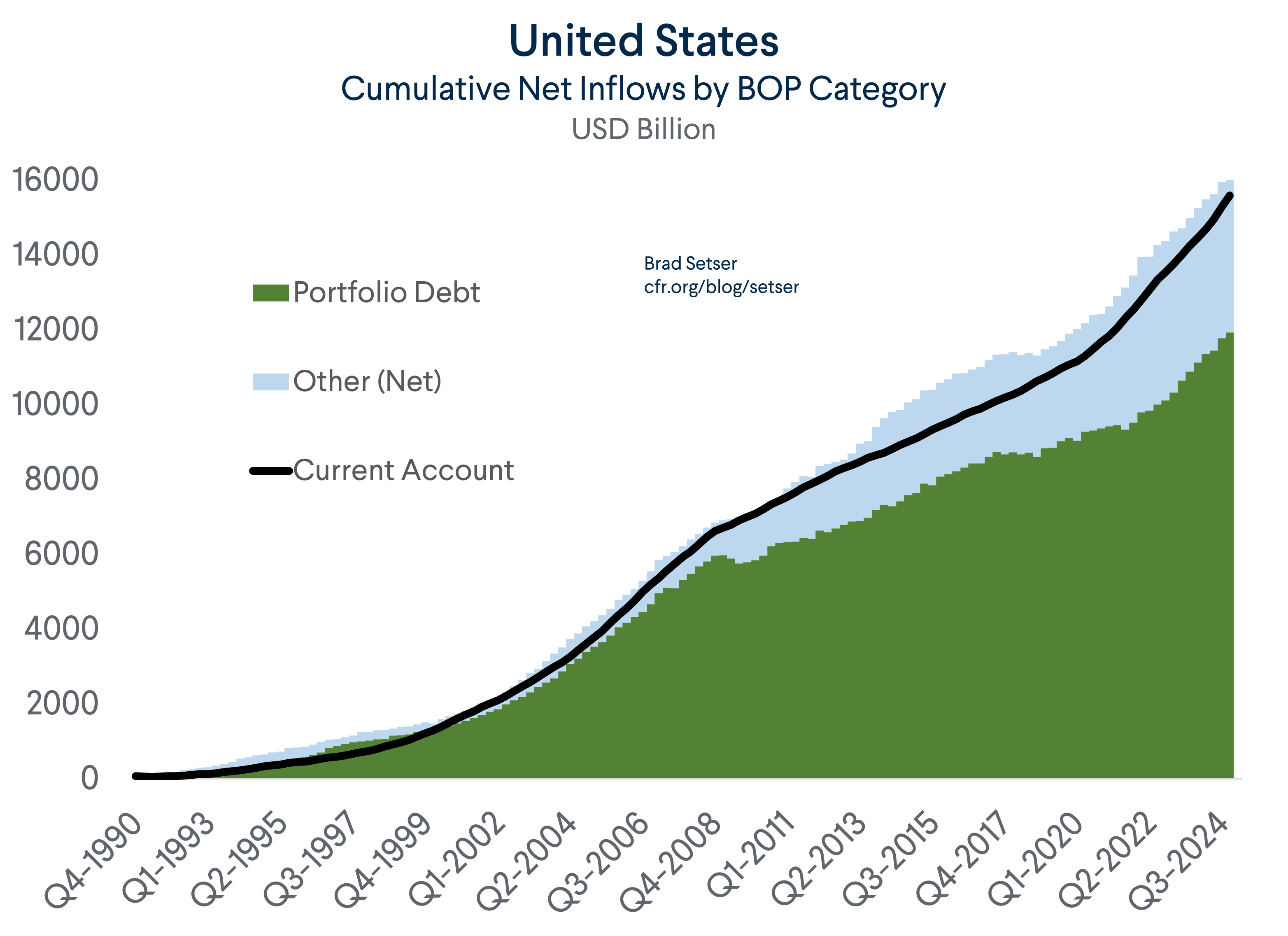

“World’s banker” could have one of two meanings: The U.S. could be borrowing from the world to invest in either risky debt or risky equity abroad. But it isn’t. The debt inflow into the U.S. over time perfectly covers the external deficit. There is nothing really left over to finance the buildup of U.S. external assets. See the following chart, which sums up debt inflows and the current account deficit over time.

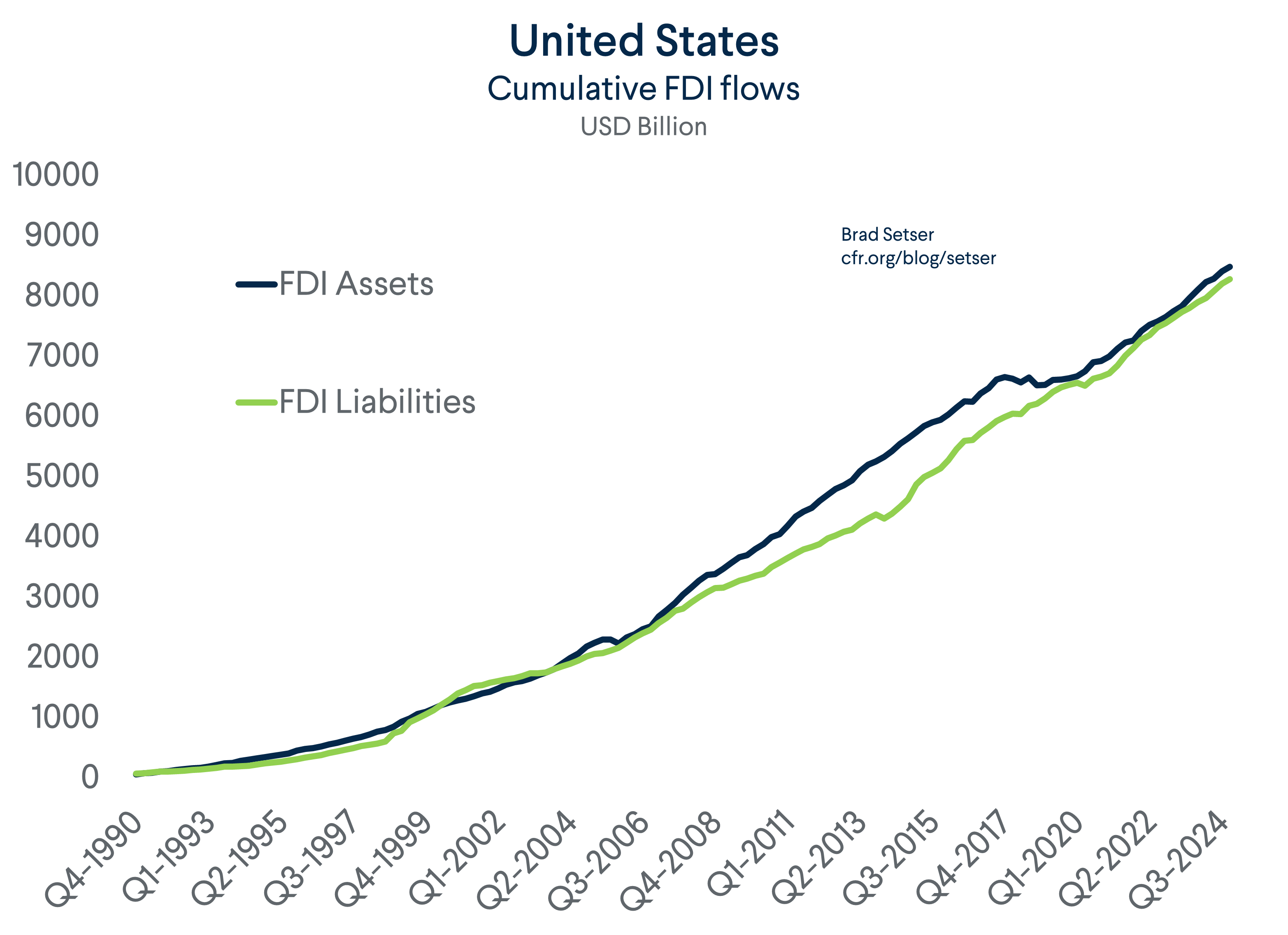

Equity inflows and equity outflows are about equal, so I net them against each other—which I think is a better way of doing this than looking at the share of the flow when there is a big gap between gross inflows and gross outflows. The chart below only covers foreign direct investment; but trust me, the chart on portfolio equity flows over time looks the same.

There is a second possible meaning of the term “the U.S. is the world’s banker,” namely that even without a debt funded equity outflow, the U.S. stock position could be positive and offset a negative debt position. That was indeed once the case (it was the basis of several papers by Pierre-Olivier Gourinchas and Helene Rey). But it is no longer the case—thanks to the run up in U.S. equity prices relative to world equity prices, the U.S. equity position is almost as negative as the U.S. debt position (the FDI component is also mismeasured, see Gian Maria Milesi-Ferretti).

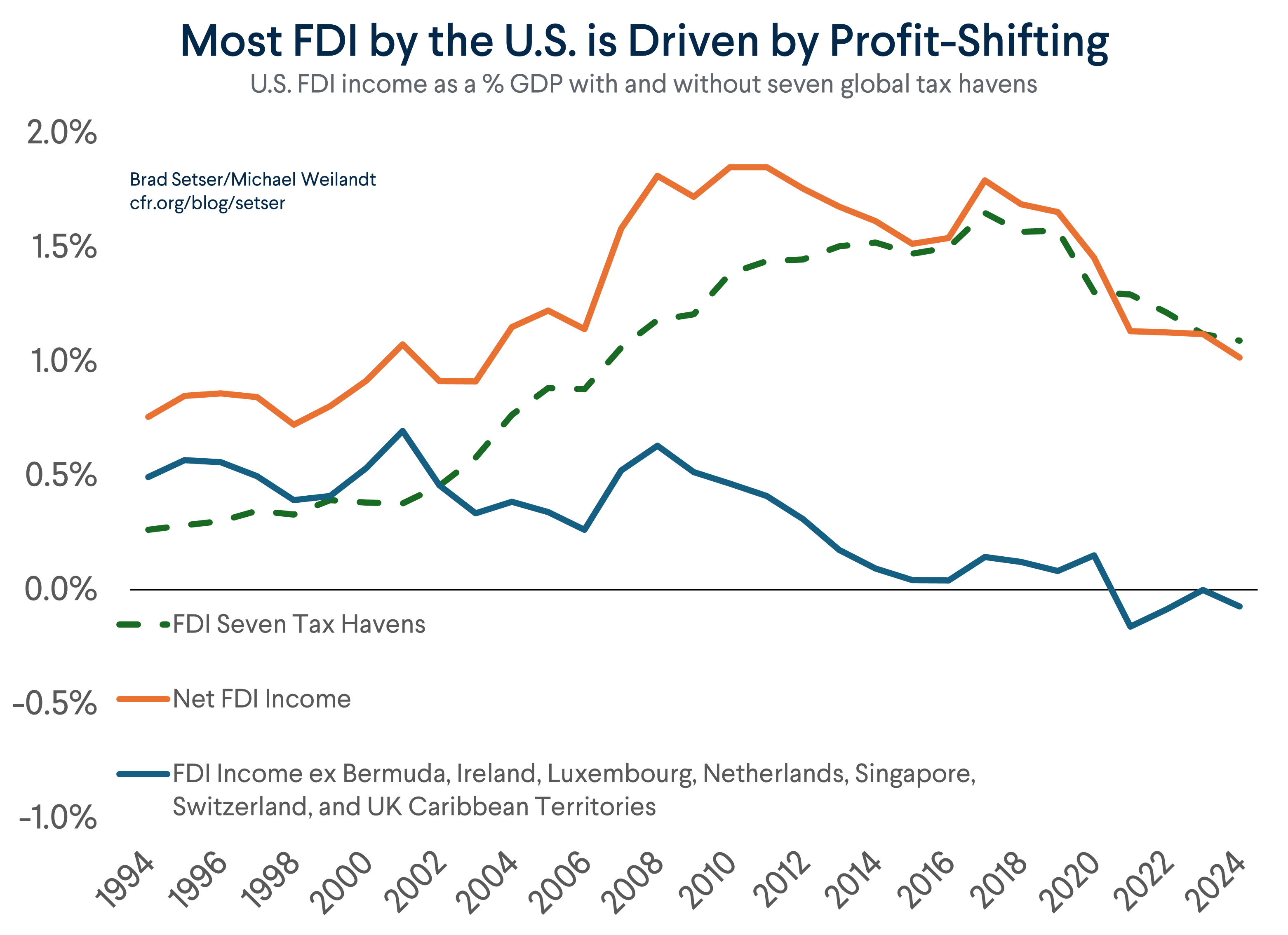

The higher return on U.S. assets than liabilities stems from the higher equity share, but if you look at the equity and debt positions separately (as you should!) the higher equity return is all from excess returns on U.S. FDI, and all of that, in practice, comes from the returns reported in a few tax centers.

The U.S. thus is simply the world economy’s big borrower, and the supplier of yield and equity returns to the global market (Treasury yields may be lower than they otherwise would be absent the dollar’s global role, but they are absolutely higher than the return on the world’s other global currencies, setting the British pound aside; they are no longer absolutely low). Adam Tooze is onto something important in his recent Substack.

One further quibble: the loss of the “premium” on U.S. borrowing isn’t just from the rise in U.S. fiscal and external debt, it is also a function of the absence of any growth in the world’s stock of formal reserves over the last ten years. That is the kind of thing that is missed by looking only at the dollar’s share of global reserves, and not factoring in actual global reserve flows.

A final point: the IMF doesn’t look at sovereign wealth funds or sovereign pension funds, and never has understood either how SAFE moved reserves off its balance sheet with “entrusted loans” and other “diversified uses” of SAFE’s FX holdings (SAFE has more FX than it reports as reserves, in other words, thanks to its “co-financing funds” and its undisclosed stock of interest income) nor how the big state banks have now been enlisted to keep the yuan in the band. The IMF’s current intervention variable thus doesn’t matter, because the IMF isn’t even really trying to measure the actual intervention done by the world’s big surplus economies. But that is a topic for another time.

Bottom line: The IMF’s 2025 External Sector Report is an improvement over the Fund’s 2024 report, but it still downplays China’s contribution to an unbalanced global economy and lacks the needed sense of urgency and alarm. And it is critical that the IMF not forecast away problems -- and thus get its forward looking analysis of Asia’s still rising external surplus right.

* The intervention variable was aways interacted with capital controls, so it “drops” out of the analysis if a country has an open capital account. In other words, the model assumes away intervention by Japan’s Ministry of Finance and the Swiss National Bank (which is obviously wrong in the case of Switzerland). It thus reverts to being a variable that measures China’s formal intervention, as China is the only big economy with a mostly closed financial account, and no longer intervenes through the PBOC’s visible balance sheet.

** I do commend the IMF for recommending (in Chapter 3) that China adopt a “More expansionary fiscal policy, with greater support for consumption (scaling up social spending) and the property sector (to finance completion of unfinished housing).” That is a noticeable shift from the 2024 Staff Report, which recommended a 0.7 pp of GDP fiscal consolidation in 2025 (and every year thereafter...)

*** Gagnon and Bayoumi have a box on the new standard as well, which argues that the standard should lower China’s imports and exports as Apple Ireland more or less “owns” the production of iPhones for the global market, and the imported parts for Chinese iPhone assembly shouldn’t be counted in China’s balance of payments (conceptually, they are Irish imports, as the phone is owned by Apple Ireland) and all that should appear in the Chinese data are the Chinese parts embodied in the exported phone and a service export for “assembly services.” That though clearly is not what China is doing. Most obviously, the new data raised, rather than lowered, imports relative to customs, and there was no big shift to assembly services. Note that the consistent application of this principal shouldn’t have an impact on the current account, and China’s new approach clearly reduced the current account relative to what it would have been using the customs-based methodology (which is easy to replicate).